Where today's job seekers have the best chance of getting hired

The U.S. economy added 172,000 jobs in May, more than double economists’ expectations, while unemployment held steady at 4.3%. Leisure and hospital…

The U.S. economy added 172,000 jobs in May, more than double economists’ expectations, while unemployment held steady at 4.3%. Leisure and hospital…

Nearly 6% of U.S. home listings were pulled off the market in April, tying the highest level since the start of the pandemic. Sellers are increasin…

The average rate on a 30-year fixed mortgage fell to 6.48% this week from 6.53%, according to Freddie Mac, marking a modest improvement for homebuyers.…

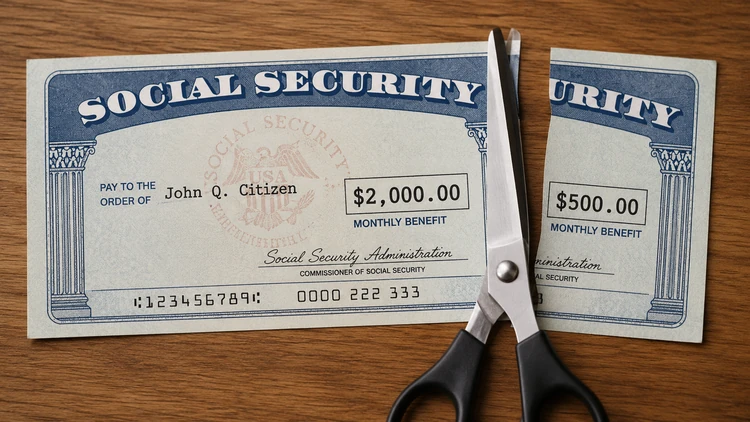

A projected Social Security insolvency in 2032 would trigger an automatic 24% benefit cut under current law, reducing monthly retirement benefits by an ave…

Paying cash? You’re subsidizing the rewards that credit card users get

The spring housing market is smiling on renters

Remote work is still hiring: 10 entry-level jobs new grads should be watching in 2026

Investors are snapping up fewer houses. Is that good for buyers?

Feds are overhauling student loan payment plans: What borrowers need to know

Feeling financially stuck? A money expert says these 5 moves can help you regain control

Summer camp now costs more than $2,200 a week in some states

Mortgage rates edged higher this week

Inflation showed signs of acceleration in April

Mortgage rates are rising again: Does an adjustable-rate loan make sense?

Treasury launches Trump Accounts app ahead of July 4 rollout

Here are the cities where $300,000 still buys a starter home

Consumer sentiment hit an all-time low in May

Beef prices soar as Americans prepare for Memorial Day cookouts

Mortgage rates jumped this week, rising 15 basis points

New report reveals wide gap in household bill costs across the U.S.

Medicaid changes could mean more missed cancer screenings

Fake job listings are fueling new anxiety for today’s job seekers

Here are the credit cards that provide the best deals on gas prices

Economic conditions now favor people who save money: Here’s why

Using a single real estate agent can be costly, report says

Bank of America agrees to $2.25 million settlement over ATM fees at 7-Eleven stores

Many graduates are financially unprepared for how fast bad credit can hurt them

Foreclosure activity increased 18% in April

Mortgage rates seemed to stall this week

Did you get a CP53E notice from the IRS? Here’s how to tell if it’s a scam

The spring housing market features slow sales and rising inventory

Grocery prices are rising at the fastest rate in four years

Household debt increased in the first quarter, but credit card debt declined

Inflation picked up speed in April, led by gas prices

Looking for a job? These industries did the most hiring in April

20 remote jobs you can land without a college degree — and some pay surprisingly well

UnitedHealthcare pledges to reduce some prior authorization requirements

Is ChatGPT the new financial advisor?

Moving in with Mom and Dad is becoming more common

FAIR Health expands cost transparency tools with new interactive features

Home prices are still rising, but not everywhere

Gallup poll finds Americans increasingly worried about affordability

The price of gold has been especially volatile since the start of the Iran war

Lawmakers push for federal sports betting safeguards

The Iran war is beginning to affect supply chains

Fidelity highlights financial scams that are growing more dangerous

Are you skipping health insurance? More Americans are asking that question

Consumer sentiment falls to record low in April

The post–Tax Day scam targeting your refund (and how to avoid it)

15 high-paying jobs that actually make a difference in people’s lives

Mortgage rates eased again this week

The ‘heat or eat’ reality: Why 1 in 5 Americans are skipping meals to stay warm

Pending home sales edged higher in March

Here’s why food prices could rise even more

More homebuyers are walking away from contracts

How reverse mortgages work: What borrowers should know

Home insurance costs are climbing — and first-time buyers are feeling the squeeze

Renting now beats buying across major U.S. metros

Here are some hacks for stretching your household budget

Americans aren’t slowing down their spending (even with higher prices)

Mortgage rates drop to a four-week low

Americans are losing nearly $1,000 a year to confusing money terms

Gen Z and Millennials don’t see tax refunds as 'extra money' anymore

Americans spend $25,000 a year on essential bills

This may be why there are fewer buyers in the spring housing market

The best employee discounts in retail (and which ones are actually worth it)

Divorce after 50 can impact long-term retirement plans

Wholesale inflation increased in March, but not as much as expected

Existing home sales dropped sharply in March

Consumer sentiment hits a historic low as inflation fears intensify

The tax filing deadline is April 15: Are you ready?

Sharply higher gas prices sent inflation higher in March

Rising property taxes are adding to the burden on homeowners

Tap-to-pay 'ghost tapping' scams are rising — Here’s how to protect yourself

Warning: Check washing can drain your bank account

For the first time in months, the average house payment rose in March

How much does it really cost to raise a child in the U.S.?

The tax-filing deadline is approaching: What you need to know

Inflation at the grocery store may be worse than at the gas pump

Amazon is hiring independent delivery drivers — Is Amazon Flex worth it?

Betting on trouble? How sports gambling could be hurting your finances

While prices of everything else keep going up, egg prices are still falling

Mortgage rates climb to a seven-month high, adding pressure on spring housing market

Beware the new ATM ‘trap door’ scam

Houses are going begging as the spring housing market ramps up

Social Security advocates say benefits should be capped for the wealthy

Mortgage rates surge as Iran war ripples through U.S. housing market

OECD warns inflation is likely to nearly double in 2026

Postal Service seeks fuel surcharge on package deliveries

Rising energy costs threaten to derail the spring housing market

The best time to sell your home is just weeks away

Rising grocery costs push Americans to rethink how they shop

Rising energy costs are making grocery shopping more expensive

Here’s why the price of gold is falling

Four reasons why mortgage rates are moving higher again

Here are the ‘hidden’ costs that may be holding you back

The “anti-hustle hustle” is booming — and it’s built on what you already know

Change in insurance requirements may lower costs for homeowners

US Postal Service sounds financial alarm

Inflation is surging at the wholesale level: Are consumer prices next?

Homeowners insurance rates are projected to rise again in 2026

‘Accidental landlords’ are increasing, and that may benefit renters

Tax scams surge during filing season as fraudsters refine tactics

Senate passes legislation aimed at making homes more affordable

Gallup finds many Americans are making financial trade-offs to pay for health care

Egg prices are falling fast after last year’s ‘eggflation’ surge

Mortgage rates moved slightly higher this week

There’s good news and bad news for renters

IRS expands office hours at taxpayer assistance centers during filing season

Many prices are rising as Iran war rattles global markets

Consumer prices rose at a moderate pace in February

Treasury, IRS propose rules for opening and managing Trump accounts

Housing market shows early spring momentum as home values edge higher

The U.S. economy lost jobs in February

What impact are data centers having on your electric bill?

IRS publishes filing instructions for ‘no tax on tips’ and other new tax breaks

Why the war with Iran is making mortgages more expensive

10 high-paying jobs that are helping shrink the gender wage gap

State Farm sending $5 billion back to car insurance policyholders

A key mortgage rate crossed a critical threshold this week

The states where groceries hurt the most — and what you can do about it

Buy now, pay later services surge in popularity as risks grow

Trump proposes American Retirement Plus plan

No experience? No problem: 25 remote jobs you can start now

Mortgage rates have fallen: Is now a good time to refinance?

Home affordability has improved in early 2026

What to ask when considering a pre-paid funeral plan

United Airlines boosts its MileagePlus Card perks

Part-time remote jobs with real benefits: where to look and what to expect

Home price growth slows as buyers gained negotiating power in January

Mortgage rates fall to a more than three-year low

Prospects continue to brighten for renters

Do you qualify for the new tax deduction for auto loan interest?

The Consumer Price Index rose 0.2% in January

Mortgage rates continue to inch toward the 6% level

Existing home sales plunged in January

Back to the office? Here’s what it’s really costing you

The economy created 130,000 jobs in January, more than expected

Love and lower premiums? How marriage can affect your insurance rates

Mortgage rates have leveled off near 6% — what buyers should know

Here’s why it’s getting harder to find a job

Think that IRS message is real? It might be AI

Homebuyers scored the biggest discounts in more than a decade in 2025

The cost of hosting a Super Bowl party is a little higher than last year

Part-time, real perks: 7 companies that treat hourly workers right

IRS urges taxpayers to establish Individual Online Accounts

Feds overhaul credit score rules for conventional mortgages

Why your raise doesn’t feel like a raise anymore

The Producer Price Index suggests more inflation could be ahead

It’s getting harder to sell a house: deal cancellations surged in December

Amazon lays off 16,000 workers as AI strategy accelerates

Here are the most buyer-friendly housing markets for 2026

New study finds renting is now cheaper than owning in every major U.S. metro

Gold surged to new record highs this week

Six savings challenges to try to boost your finances in the new year

Consumers started 2026 in a sour mood

IRS confirms military 'Warrior Dividend' payments are not taxable

When to update your income with your credit card or bank

Glassdoor reveals the best places to work in 2026

Winter weather tips every small business owner should know

The economy may be in better shape than predicted

Pending home sales plunged nearly 10% last month

Mortgage rates still expected to stabilize in 2026, not plunge

Global gold rally intensified this week amid rising uncertainty

Trump signs executive order barring Wall Street from buying single-family homes

Can President Trump really cap credit card interest rates at 10%?

Bill would renew Biden caps on credit card late fees

Here’s a warning to last-minute tax filers

Affordability returning to 20 large housing markets, Zillow reports

Car insurance is eating up more of your paycheck

Americans are cutting back just to get by — and the financial stress is piling up

Federal Reserve report finds a mild upswing in the economy

Existing home sales surged in December

Tax season scams are back — and they’re getting harder to spot

Medical debt linked to housing instability

'Click to cancel' may be revived

Consumer prices rose 0.3% in December, led by shelter and recreation costs

Gold prices surge to yet another record high

Trump shifts focus from housing to credit-card debt, dreams of a 10% interest rate

Senators working to restore Obamacare subsidies

It’s getting harder to find a job, with hiring down in December

Trump floats plan to lower mortgage rates

Trump seeks to ban large investors from owning single-family homes

Chase poised to take over Apple credit card program

IRS announces start of 2026 tax filing season: January 26

Here’s how long it takes to save for a down payment on a house

When Americans moved in 2025, they chose Texas and Florida the most

IRS urges taxpayers to prepare now for tax-filing season

Grocery prices show mixed movement in December

Homebuyers likely to remain in the driver’s seat throughout 2026

Obamacare subsidies have expired; big increases arriving soon

Three financial New Year’s resolutions that can actually build wealth

Hot jobs, hotter raises: 10 careers set to see pay boosts in 2026

How 2026 redefines the US tax landscape

What are the likely effects on consumers of Trump's Venezuela incursion?

10 jobs for associate-degree holders that pay more than you think in 2026

Mortgage rates hit a 2025 low heading into 2026—what comes next?

Consumer confidence continued to erode in December

10 low-stress, high-paying jobs to watch in 2026

Single-family rent growth slows sharply in October: Cotality

Considering just one mortgage offer could be costly

Inflation rose more slowly than expected in November

Inflation is cooling, so why is there an ‘affordability crisis?’

Will gold keep its shine in 2026?

Earn big without a Bachelor’s: 15 high-paying jobs you can get in 2026 without a college degree

PayPal takes a big step toward becoming a bank

Employment grew slightly in November, suggesting a stable labor market

When getting care feels too costly: Why millions of Americans are skipping the doctor

Home listings fell sharply in early December

Grocery prices showed mixed trends in November

Mortgage rates edged higher this week after two weeks of declines

These housing markets may see prices rise the most in 2026

What will the Fed’s latest interest rate cut mean for consumers?

Dems propose a temporary Social Security boost to relieve inflation

Fed cuts rates again but signals pause amid rare internal split

Remote work isn’t just a perk anymore — it’s a priority, report finds

Women are saving far less than men — and feeling the stress, report finds

Hassan presses corporate mobile-home park owners over rent hikes, poor conditions

Homeowners sue Big Oil over soaring insurance rates

Here’s where home values are falling the most

Consumer sentiment improved slightly in early December

AI is transforming home buying and renting — and raising new risks

Colorado credit repair company shut down for deceptive 'piggybacking' scheme

Here’s why it’s so hard to find a job

Mortgage rates retreated again this week

What are Trump Accounts, and who can benefit?

Remote work isn’t dead: 20 employers offering six-figure WFH jobs

Holiday shoppers embraced planning over impulse spending as BNPL use surged

Here are the predictions for the housing market in 2026

Financial advisors losing access to clients’ Fidelity 401(k) accounts

Black Friday deals spark overspending as holiday shopping ramps up

The best high-paying jobs for introverts in 2026

Consumer confidence slides in November

Here’s why your car insurance costs keep going up

Home prices are still high, but they’re getting lower

What's behind America’s growing affordability crisis?

Veterans get relief from $272 million in surprise medical bills

Wells Fargo and Robinhood lead the pack as AI transforms wealth management apps

States crack down on rental junk fees as tenants pay hundreds of millions annually

Congress may soon make payday loan apps more predatory

What's behind rising insurance premiums? Surging advertising costs, for one

L.A. County probes State Farm over wildfire claims handling

IRS boosts retirement contribution limits for 2026

Colorado wins key ruling on interest rate caps for out-of-state banks

US Mint ends penny production: What it means for consumers

Is a 50-year mortgage the answer to the housing crisis?

The cost of a traditional Thanksgiving dinner has jumped 7% this year

Inflation continues to linger at the grocery store

Missouri tells insurers to hold off on condo policy cancellations after storm damage

Veteran homebuyers face affordability challenges compared to a decade ago

Visa, Mastercard are close to a deal with merchants — how it could change what card you use

10 work-from-home side jobs that can earn you $1,000+ a month

Trump proposes allowing 50-year mortgages to lower monthly payments

What's wrong with insurance? Just about everything

Mortgage rates edge higher after hitting a 12-month low

More than 150,000 people lost their jobs in October

Here’s why it’s still hard to buy a house to live in

Due diligence can keep zombie businesses from eating your money

Insurance executives take home big bucks, stiff policyholders: CFA

Mortgage rates dipped slightly again this week

ACA Marketplace health insurance premiums could rise 26% in 2026

Federal Reserve cuts interest rates to lowest point since 2022

What’s the real cost of showing up to work?

ACSI report reveals the best and worst mortgage lenders for customer satisfaction

Gas prices inched up this week due to a Midwest refinery fire

Americans losing grip on debt as delinquencies surge and borrowing costs bite

Here's how a U.S.-China trade deal could help consumers

The Consumer Price Index rose 0.3% in September

The average 30-year fixed rate mortgage rate continues to fall

NBA player and coach detained in FBI sports gambling probe

Single-family rent growth hits 15-Year low

Why your health insurance premiums keep rising

Gold prices suffer their biggest decline since 2013

Some cities will still pay you to move there

Austin is now the strongest buyer’s market in the nation

Trump administration agrees to reinstate student loan forgiveness

California shuts down 'health sharing plan' in $34 million settlement

IRS announces 2026 tax brackets

Is it too risky to buy gold at these record highs?

The hidden cost of being a sports fan

Mortgage rates fell again this week

15 best remote jobs for stay-at-home moms in 2025

Amazon plans 250,000 U.S. holiday hires — here’s what applicants should know

Holiday spending may increase over last year, but not by much

Delayed CPI report adds to delay of Social Security COLA announcement

Essentials take a bigger bite of consumer spending, survey finds

Consumer sentiment stays stable in October, despite economic turbulence

How to stretch your budget after a layoff

The country’s not in a recession, but your state could be

Mortgage rates reversed course this week, giving buyers a break

U.S. sees a steady climb in foreclosure activity

Coffee prices perk up as cereal cools

Gold prices are at a record high: Now what?

Consumers are facing ‘sticker shock’ at the beef counter

Gold prices poised to hit $4,000 an ounce this week

Mortgage rates edge higher for a second straight week

Goldman Sachs study finds more Americans living paycheck-to-paycheck

Title lock system foils reverse mortgage scam against elderly homeowner

National Flood Insurance Program lapses, stalling home sales

Federal layoffs beginning to be felt as DOGE cutbacks take effect

Gold prices hit another record high

There’s a standoff between buyers and sellers in the housing market

Nearly 3/4 of consumers lie about their spending, survey finds

Sales of existing homes stalled in August

Millions of student loans are delinquent, threatening borrowers' futures

New home sales shot higher in August

Home price growth moved slightly higher in August

Homebuyers are taking another look at ‘fixer-uppers’

Federal flood insurance program faces Sept. 30 deadline

Here’s more evidence the housing market is cooling down

The Fed cuts interest rates by .25%

Nearly half of U.S. homeowners hit with insurance rate hikes

Consumers' credit scores have dipped in 2025

Democrats move to ban credit checks in hiring

Rent is rising in most large housing markets

Homeowner equity stalls as more borrowers slip underwater, report finds

Here are the cities where residents have the highest bills

The decline in mortgage rates is picking up speed

Inflation increased in August as food and housing costs rise

Consumers are saving more money, with young Americans saving the most

Robinhood launches a social network for traders, raising FOMO fears

U.S. job growth has been far weaker than previously reported

Trump signs measure to strengthen privacy protections for homebuyers

Will the Federal Reserve cut interest rates next week?

Grocery prices flashed mixed signals in August

Vacation home sales begin to fall

Gold surges to record heights: What’s fueling the rally?

Housing market shows rising inventories in July as sales cool

Retirees face shrinking gains: rising healthcare costs may eat up 2026 COLA

Study finds real estate agents steer buyers away from low-commission homes

Are you going into credit card debt with back-to-school shopping?

Mortgage rates continued to tick lower this week

Here are the 10 states where ‘stagflation’ is the biggest threat

If homeowners' insurance is expensive, where you live may be a reason

More prime borrowers are falling behind on paying their bills

Consumer confidence dips slightly in August

How is homeowners insurance impacted by natural disasters?

Worried about inflation? These tips may help you stay ahead

Volvo launches insurance agency in U.S.

Homebuyers canceled contracts at a record pace in July

School supplies, lunches cost a little less in 2025

Sales of existing homes jumped in July

Home values are falling in half of the top 50 metros, report finds

Top 10 best jobs for older people in 2025

Consumer sentiment dips for the first time since April

The hidden cost of today’s housing market

More than half of credit card users are carrying balances

How much are your monthly bills compared to the rest of the U.S.?

Mortgage rates fall to lowest level since October

Wall Street eyes the Fed as PPI and jobless data emerge

Tariffs show up in July’s Producer Price Index

Zelle sued by New York over rampant fraud, $1 billion in losses

Rents went down in July for the 24th straight month

These new SUVs and trucks may be the cheapest to insure in 2025

Report: Low credit scores can double home insurance costs, outweighing disaster risk

Home prices continued to rise during the second quarter of 2025

Inflation remained stable in July, thanks to lower gas prices

New York indicts two under the state's new deed theft law; how to protect your home

Teen drivers, dorm parking and insurance: What to know before the fall semester

Mortgage rates continued to fall this week

Lead-generation firms fined $145 million for deceiving health insurance customers

Reaction is muted as Trump's tariffs take effect

Congress bans sale of mortgage 'trigger leads' in landmark privacy bill

Grocery prices registered a significant rise from June to July

Consumer debt hit a record high in the second quarter

Reversing course, CFPB says it will issue revised open banking rule

More consumers are using BNPL to buy groceries, survey finds

Push Notifications, High Stakes: Report slams sports betting ad tactics

Home prices fell in 14 of the most expensive housing markets in July

New mortgage relief law will help thousands of veterans avoid foreclosure

Consumers are using their credit cards more as debt rises

The housing market is in the dumps, except in one category

Here are the food costs that have gone up the most this summer

Affordability is likely to limit home sales for the rest of 2025

Mortgage rates continued to move higher this week

Mortgage applications fell by 10% in just one week

State Farm hits Illinois homeowners with double-digit rate hikes

Inflation disappeared at the wholesale level in June

Data show a big increase in Americans planning to leave expensive cities

What unexpected expense keeps you up at night?

What you don’t know about car insurance can be costly

Court strikes down Biden-era rule banning medical debt from credit reports

Inflation ticked higher in June, led by electricity prices

CFPB settles with FirstCash over Military Lending Act violations

More homeowners are falling behind on their mortgage payments

Rhode Island caps payday loans at 36%

Debt Collection Calls Surge in 2025, Hitting Georgia and Atlanta Hardest

Here’s a big reason why home prices are still going up

Condo prices dropped 2.2% in May, the second-largest decline

The economy added 147,000 jobs in June

Why you shouldn’t buy a home with someone with a low credit score

Consumer group condemns withdrawal of Navy Federal penalty

Nearly 6% of the people selling homes stand to lose money

Mixed signals define consumers' mood as summer settles in

Capital One hopes to use Discover to fuel big expansion plans

Americans’ income declined in May after a dip in government benefits

Mortgage rates dipped slightly this week

The U.S. economy shrank in the first quarter by 0.5%

Buy Now, Pay Later loans will soon affect your credit score

Housing affordability hits historic lows

Consumer confidence falls sharply in June

Sales of existing homes rose slightly in May

Looking for a side job this summer? Here are 10 remote options.

Consumer sentiment shows marked improvement in June

MoneyGram paying $250,000 for consumer protection violations

The housing market continued to favor buyers in May

California launches probe of State Farm over wildfire claims

May’s inflation rate was lower than expected

Fireworks prices surge ahead of Independence Day

These suburbs are the most popular destinations in 2025

Beer taxes are highest in these states

Auto insurers shift from survival to service, but customers not very happy

At mid-year, the housing market is flashing mixed signals

Seniors won't face garnishment of Social Security payments on student debt after all

Burned-out LA homeowners sue insurers

Equifax gives its credit report a makeover

Long, hot summer in store as economic friction grows

U.S. job growth remained stable in May

Rent is falling in most major metros

Grocery prices continued to trend lower in May

Home listings hit record $698 billion in April

Another survey shows Americans are tightening their belts

Dollar General reports higher-income consumers are frequenting its stores

Complaints by servicemembers and veterans against financial firms soar 165%

Apartment rental activity is rising as the summer begins

High-paying remote jobs are out there

Banking apps reach a plateau: Satisfaction up, innovation urged

Mortgage rates rose slightly this week but remain under 7%

Consumer confidence reversed months of declines in May

Home prices may drop by the end of 2025

The US is saying goodbye to the penny

Existing home sales fell again in April

‘Energy poverty’ is a growing problem, study finds

The House passed the tax and spending bill: Here’s what’s in it

The cost of your Memorial Day cookout is a little higher than last year

FTC shuts down transnational student loan scam

Mortgage rates spike after Moody's downgrade of US debt

Moody’s downgrade of U.S. debt: What it means for your wallet

Only 21% of homes are affordable for a family earning $75,000 a year

These five things affect your car insurance rates the most

Tiny apartments are popular in these cities

Housing costs are reshaping career decisions

Feds tame student loan debt relief operation

Home buyers remain cautious while their options increase

Consumer sentiment continues to slide

Americans are buying fewer second homes

NY sues Capital One, accuses it of 'cheating customers' out of interest payments

New report shows deep disparities in the cost of core household bills

Most popular cities for renters in early 2025

College graduates face a shifting job market

These California cities are drawing the most movers

Consumers found a little price relief at the grocery store in April

Buy Now, Pay Later firms push back against consumer protection rules

States with the most uninsured children under 6 years old

Health insurance covers fewer medications than years ago

Here's how much income is needed to afford the median-priced home

FTC shuts down $9.7 million debt collection scheme

Aetna is withdrawing from the Affordable Care Act marketplace

April job creation topped estimates with 177,000 new jobs

Mortgage payments are falling in some major metros

How credit scores affect car insurance rates

Home asking prices are too high in today's buyer's market

FTC sends $18 million in refunds to Publishers Clearing House customers

The U.S. economy shrank in the first quarter of 2025

Here are the best months to sell and buy a home

Consumer confidence plunges to pandemic-era lows

Prescription drug prices have outpaced inflation and tariffs would make them pricier

Starter homes cost at least $1 million in over 200 cities

Best states for affordable housing in 2025

Mortgage rates bucked the trend of rising bond yields and fell this week

Sales of existing homes plunged 5.9% in March

A growing number of consumers struggle to manage their debt

Best states for low property taxes

The housing market may have flipped in March, with more sellers than buyers

Regulators approve the Capital One acquisition of Discover

Metros where adults are most likely to live with their parents

Penalties for driving without insurance: A state-by-state breakdown

Mortgage rates shot higher this week

Coffee prices could be set to soar

Worried about your job? You aren’t the only one

Best states for young people to buy a home

Tax Day is here, ready or not. You must pay up and file a return or extension

The ConsumerAffairs Datasembly Shopping Cart Index dipped in March

Consumer sentiment has fallen sharply since December

States with the biggest tax refunds

Income gap to buy a home versus rent is widening

Best cities for big apartments in 2025

Inflation falls at the producer level in March, suggesting inflation is easing

Mortgage rates continue to fall

Do residents of Appalachia need flood insurance?

Where Americans benefit from ban on medical debt in credit reports

House votes to throw out consumer protection overdraft rule

Condos are getting harder to sell in the spring housing market

Uh-oh, used car prices are already starting to rise

Justice Department opens probe of nation’s largest egg producer

Home insurance premiums rising as much as $3,000 in 2025

Home ownership is taking a growing bite of Americans’ monthly income

These banks made the most money on overdraft fees in 2024

Defying a growth scare, the economy added 228,000 jobs last month

The best states for taxes in 2025

Americans spend nearly a third of their income on ‘essentials,’ study finds

Homebuilders warn the home affordability crisis is getting worse

Credit unions continue to outperform banks in customer satisfaction

Zelle is moving away from its standalone app

How states tax marijuana in 2025

Economists are worried about stagflation: What does that mean for consumers?

Homeowners insurance is costing more nearly everywhere in the U.S.

It's hardest to buy a home in these neighborhoods in 2025

Consensus is growing that consumers are worried

Consumer sentiment about the economy got worse in March

Mortgage rates resumed their decline this week

The Fed’s favorite inflation gauge rose more than expected in February

Senate votes to allow steep overdraft fees, potentially killing a Biden-era rule

Claim denied? State Farm can now loan you money

Selling a home this year? Here’s the ideal time to list it

Deportations could raise restaurant wages by $3 an hour, study finds

U.S. consumer confidence fell sharply in March

United and Chase increase the perks and the prices of their co-branded credit cards

Home remodeling in ‘phenomenal boom’ despite challenges

Home flipping is declining. Why that’s good for home buyers

Florida weighs historic move to eliminate property taxes

Consumers feeling shaky, Dollar General CEO finds

Home sales perked up unexpectedly in February

Insurance identity theft is on the rise

Inflation was less than expected in February

FTC sending $15 million in refunds to Career Step customers

Egg prices continued their surge in February

Good news for homebuyers: Sellers are beginning to cut prices

New York attorney general sues insurance companies over data breaches

You don’t have to call the IRS to check your tax refund status

The decline in mortgage rates is picking up speed

The labor market remained solid in February

Average tax refund up $233 in February, IRS says

Lower mortgage rates drew more homebuyers last week

These counties had the highest and lowest property taxes in 2023

Liberty Mutual to retire Safeco brand in 2026

Only 3% of U.S. homes had government flood insurance in 2024, report says

First it was eggs, now it's beef prices that are surging

Mortgage rates move lower for another week

Pending home sales hit a record low in January

These are the best ZIP codes for renting affordable, upscale apartments, report says

Consumer watchdog CFPB dismisses $2 billion case against Capital One

Housing affordability crisis is getting worse, homebuilders warn

Here are 15 high-paying, low-stress remote jobs for 2025

Consumer confidence tanked in February as recession worries rose

Consumers' inflation fears soar to 30-year high

Feds probing UnitedHealth Group's Medicare billing practices, reports say

Typical apartment rent costs 106 hours a week of minimum wages in 2025, report says

Buyers were largely absent from the housing market in January

Inland Florida condo prices rise after buyers flee high costs on the coast, report says

Sorry, homebuyers aren’t that interested in your fixer-upper

Housing shifts to buyer's market first time in six years, Redfin says

Need help filing a tax return? Here are some IRS resources

Cost of living prompting many baby boomers to rethink retirement

Grocery price tracker shows prices of many items are falling

Six tips to make tax-filing season easier

Affordable housing is a much bigger challenge for singles

Blue Cross Blue Shield sending $2.67 billion to subscribers

Rising chocolate prices could make Valentine’s Day celebrations more expensive

The economy added 143,000 jobs last month, slightly fewer than expected

Buying a home is cheaper than renting in these U.S. counties in 2025, research says

Mortgage rates pulled back this week

Are you suffering from Virtual Meeting Fatigue?

IRS offers advice for a fraud-free tax season

Two polar opposite senators back bill to cap credit card interest rates

State Farm General seeks 22% hike in California homeowner policy rates

Home listings increased in January, giving buyers more choices

How will the new U.S. tariffs on Canada, Mexico and China affect consumers?

Uber says it's being taken for a ride by insurance scammers

These grocery prices have risen the most in the last 12 months

What to do if you can’t afford homeowners’ insurance or don’t get renewed?

Here are the tax changes for 2025

Sales of existing homes fell to the lowest level since 1995 last year

Is a housing price correction on the way?

Texas sues Allstate for collecting and selling data about its customers' movements

Buy Now, Pay Later popular among younger, poorer consumers

Here's why scammers are texting you with fake job offers

Some H&R Block customers will share in $7 million settlement

Which states are raising the minimum wage in 2025?

Feds charge mobile-home loan company set families up to fail

Despite a slight improvement in 2024, a home purchase remained out of reach for most

Mortgage rate hit their highest level in nearly six months

Insurance CEOs draw huge salaries while regulators stand by, advocates say

Egg prices are surging again. Here's why

Realtors pick housing hot spots for 2025

Health insurance industry needs a make-over, experts say

IRA Required Minimum Distribution deadlines are coming up: are you ready?

Mortgage rates continue to fall

Latest job scam asks consumers to try their hand at app optimization and product boosting

These housing markets could provide the most opportunity in 2025

FTC warns companies not to misrepresent health plans

November inflation was slightly hotter

Social Security changes in 2025 you might not know about

Who killed UnitedHealthcare CEO Brian Thompson, and why?

$1.8 billion going to victims of credit repair scam

Mortgage rates fall again, drawing homebuyers back to the housing market

Zillow sees some shifting housing trends in 2025

Here are the cities with the highest and lowest cost of living

Mortgage rates dipped this week

Consumer confidence continued to rise in November

The cost of gifts in ‘The 12 Days of Christmas’ is rising faster than inflation

Home prices may still be rising but rents are falling

Your morning cup of coffee could soon cost more

Report finds high medical costs for many who have health insurance

Banks have long knives out for consumer watchdog CFPB

Egg prices surge just before the holidays: Here's why

A Thanksgiving Day dinner costs 5% less this year

Congressional Dems oppose Capital One's acquisition of Discover

Retailers voice concern about Trump’s proposed tariffs

Sales of existing homes jumped in October

Mortgage rates are headed higher again

Survey reveals housing struggles for low-income Americans and Gen Z

Senate considers bill providing alternatives to Visa and Mastercard

Consumers found it harder to obtain credit in 2024

Student loan report shows record number of complaints from borrowers

Credit card debt rose by $24 billion in the third quarter

After the election, mortgage rates level off

North Dakota outpaced the U.S. in domestic migration in 2023

The cost of housing continues to drive inflation

Home prices rose nearly everywhere in the third quarter of 2024

Here are the top 5 home trends for 2025

Beware of growing student loan forgiveness scams

Inflation increased at the supermarket last month

Is there a property tax revolt building in the US?

Experts don't see falling mortgage rates anytime soon

Mortgage rates continue to rise

Navy Federal Credit Union ordered to refund more than $80 million

Renters grew three times faster than home buyers in the third quarter

Consumer group claims big insurance savings for California residents

Home price growth cooled further in September

As home prices rise, buyers are older and wealthier

Nearly half of recent homebuyers have a mortgage rate below 5%

Rising mortgage rates pick up speed

Florida, Tennessee taking a close look at insurance claim denials

The housing market gained momentum in September

Consumer confidence surged in October

If you think it’s getting harder to find a job, you’re right

Private equity firms driving up rent around the country, Senators charge

Gen Z is the most rent-burdened generation

Climate risks making it hard to buy or sell a home in California

Mortgage rates went up again this week

People can switch banks easier under new government rule

Problem gambling grows along with revenue, a Massachusetts study finds

Contractors building fewer single-family homes and more townhouses

Here's why mortgage rates are going up

Earned Wage Advance is "a loan shark in your pocket," critics charge

Rent is rising in the Midwest but falling in the South

Mortgage rates increased again this week

These mortgage lenders got good reviews in 2024

September’s housing trends may hold good news for buyers

Life insurance too complicated, survey finds

Over 80% of job recruiters admit to posting 'ghost' jobs, study finds

Nearly every homeowner will help pay the price of hurricanes Helene and Milton

Gasoline prices keep falling in 2024. Here's why

Student loan borrowers got tricked by Ejudicate. Now it's banned from arbitration

Mortgage rates jump because of bond market weakness

Inflation picked up a bit in September, led by higher food and shelter costs

Banks and social media: Not a good mix, regulators warn

Lawmakers target food companies they accuse of shrinkflation

Inflation is still present at the grocery store, though some prices are falling

Supply chain experts expect ports to return to normal soon

Required minimum distributions from retirement accounts may rise in 2025

With falling mortgage rates, real estate listings are increasing

Strike at East Coast and Gulf Coast ports suspended

Rent increases are forcing people to move in these cities and states in 2024

In a sudden shift, the economy added 254,000 jobs in September

20,000 plus Bank of America customers surprised with 'zero balance' notice

Mortgage rates ticked up this week

The East Coast and Gulf Coast port strike may cost the economy $540 million a day

Consumers should prepare for shortages and higher prices, experts say

Renters paid 15% or less of their income in these cities and states

Postal Service seeks five stamp price increases in next two years

Insurance industry uses kickbacks to boost sales, Senate report finds

Mortgage rates fell again this week

Surviving spouses, debt burdens, and nasty debt collectors

Most renters are paying more than they can afford in these cities and states

As rates fall, mortgage applications are surging

Will lower mortgage rates keep home prices high?

U.S. Justice Department sues Visa, says it has monopolized debit card networks

Suddenly, consumers aren’t nearly as confident as they were

Concern grows about a potential East Coast and Gulf Coast dock workers' strike

Mortgage rates appear ready to slip below 6%

Renting? You might be able to buy a home in 22 of the top 50 housing markets.

The Federal Reserve cuts interest rates for the first time in four years

Banks charging overdraft fees without permission, feds find

More Americans say they plan to rent their homes indefinitely

Fake credit card sued for gounging families with hundreds of dollars of fees

How this week’s Fed meeting might help auto loan borrowers

A dock workers strike would devastate the US economy, experts say

Some health insurance customers clicking on social media ads instantly regret it

TD Bank to pay customers $7.76 million for wrecking their credit reports

Mortgage rates are the lowest since February 2023

US bans Navient from servicing government student loans

Consumer prices rose slightly in August as inflation continues to cool

Household income finally outpaced inflation in 2023

The cost of a typical shopping cart of groceries jumped last month

Progressive not writing new homeowners policies in Texas

A potential dock workers' strike could be a big headache for consumers

Jobs were harder to find in August

FTC questions income claims made by multi-level marketers

Nearly a third of homeowners say they are ‘house poor’

Over 80% of workers are considering delaying retirement due to finances, study finds

Debt collectors hounding consumers for medical & rental debts they don't owe

How has the legalization of sports betting affected consumers' finances?

Mortgage rates remain steady as buyer conditions improve

Pending home sales plunged in July. Good news for buyers?

How’s the economy? Sausage may provide a clue.

Mortgage rates dipped for another week, drawing more buyers back into the housing market

Do you know how deeply in debt you really are?

Your Labor Day cookout will cost just a little more this year

Here are the states and metros where grocery prices have risen the most

More evidence the housing market is starting to flip toward buyers

The Postal Service proposes more changes to mail delivery

Justice Department claims real estate software firm helps landlords collude on rents

Mortgage rates continued to dip lower this week

Workplace insurance costs are projected to rise sharply next year

Is the housing market shifting to benefit buyers?

New survey finds 35% of consumers aren't saving for retirement

Gold prices notch another record high

How the new real estate commission rules hurt homebuyers

Auto insurance is outpacing inflation and getting worse

Electric bills are rising four times faster than groceries

Mortgage rates remain as low as they’ve been in more than a year

What recession? Consumer spending is booming.

Mortgage refinancing is surging: Should you join in?

The cost of shelter keeps climbing as overall inflation slows

Most consumers still struggle with the effects of inflation

Buying a home is about to get a little more complicated

Should you trust those TikTok’s side hustle videos?

How long will it take to sell a home? It depends on the state where you live.

Feds reportedly considering requiring banks to cover Zelle scam losses

Mortgage rates fall to their lowest rate in a year

Consumer credit card debt accelerated in the second quarter

Prices of many grocery items showed stability in July

Mortgage rates are falling. You can thank the weak jobs report.

Gold and Bitcoin haven’t been spared from the stock market sell-off

When the Fed cuts rates, what will it mean for consumers?

Can Congress force banks and Zelle to cover your scam losses?

The economy is growing, but so are auto repossessions. That doesn’t sound right.

Nearly 8 million renters can afford to buy a home, study finds

Mortgage rates barely moved this week

See where Americans think cost of living went up in just two months

Feds are investigating firms that use personal data to set prices

Here's how prices of key goods and services changed in the first half of 2024

Here's how grocery prices of everyday items changed in the first half of 2024

Could home prices be about to dip?

The slowdown in home improvement spending could be ending

Americans mostly unprepared for 'the great wealth transfer,' study finds

Price of gold hits new record high

Crooks exploit 'convenient' credit card feature, drain accounts even after cancellation

Interest rates will soon fall, Fed officials suggest

Here are the surprising cities where rent is growing fastest

Fifth Third Bank slapped with a $20 million fine

Mortgage rates ticked lower this week and remain below 7%

Inflation cooled in June, helped by lower gas prices

Today's rental game is loaded with pitfalls, the FTC says

Inflation at the supermarket eased in June

Feds scrutinize medical credit cards sold by dentists and doctors

Wells Fargo gets sued for not backing up scammed customers

Chase Bank warns CFPB rule would result in new fees

Here are the most and least expensive metro areas for renters

Mortgage rates rise but stay under 7%

Complaints about savings accounts have doubled!

Pending home sales plunged in May. Is the market at a tipping point?

Adobe’s not alone in being difficult to cancel. There’s a parade of others.

Mortgage rates dipped again this week, but not by much

Freddie Mac gets approval to buy second mortgages on single-family homes

Want to save as much as 25% on your car insurance?

Did Saudi Arabia just doom the dollar? Economists weigh in.

The pros and cons of paying rent with a credit card

These days, a six-figure down payment may be needed to buy a home

Looking for a remote job this summer? Check these companies.

Mortgage rates continue their downward trend

Do you have enough to feel financially prepared in case of an emergency?

Utilizing AI can be beneficial for people on the job hunt

Here are the car insurance companies that provide the most customer satisfaction

Deep in debt? Personal finance experts offer some solutions.

Home prices have hit a record high, according to an industry report

Mortgage experts offer advice for getting the best interest rate

What’s the short-term outlook for mortgage rates? Experts weigh in.

Inflation stalled in May, helped by lower gasoline prices

Major IRS 'Payment Due' glitch discovered

The average nationwide rent is now $1,653, the highest since October 2022

Feds go after companies that put 'gotchas' in their fine print

Some grocery prices dipped slightly in May

Mortgage rates move back above 7%

The IRS’s free Direct File will become permanent

Insurance industry sues to overturn new rule to protect retirement savers

Americans might be feeling better about the economy after all

Do you really need a college degree? More Americans have their doubts.

Inflation is pushing familiy expenses up more than income

Mortgage rates fall below 7% again

Home buyers still balk at high interest rates and rising prices

Proposed rule will give buy now, pay later customers greater protection

What will hurricane season mean for homeowners insurance rates?

These towns and cities will pay you up to $20,000 to move there

Why the price of car insurance is surging and what you can do about it

Here’s how much more your Memorial Day cookout will cost over last year

Mortgage rates fall for a second straight week

Stubborn inflation may boost 2025’s Social Security increase

Americans are falling behind on credit card payments. Here's who can help.

Inflation slowed in April as consumers paid less for groceries

Got a big tax refund coming? If so, the IRS says you may be a scam victim.

Can cashback credit cards fill in the gaps that inflation is causing?

Worried that inflation is sticking around? You aren’t alone.

Washington and airlines may be about to clash over credit card points

Court blocks limits on credit card late fees

Will the tornado outbreak cause your insurance rates to go up?

April’s Shopping Cart Index shows grocery prices are stabilizing

Competition from investors may be why you can't buy a house

How close is the U.S. to a debt crisis?

How will the new ‘fiduciary’ requirement for retirement planners affect you?

Turns out that everything that glitters is not gold after all

There’s good news and bad news about household debt

Here’s the new standard your retirement planner must meet

If you buy gold, how do you go about selling it?

Mortgage rates are rising, home sales are falling

Did you have to pay taxes this year? Here’s how to stop that.

A quarter of home sellers don’t plan to use a Realtor, survey found

Gold gets a new price target - $3,000 an ounce

How’s your bank’s customer service? Study suggests it could be better.

Nearly half of Americans struggle to pay for housing

Just how 'free' are 'free' tax filing services?

Here are some last-minute tax-filing tips

If the economy isn’t bad, why does it feel like it is?

These 10 banks produce the most complaints about fees

Deadline is approaching for over $1 billion in unclaimed tax refunds

Mortgage rates level off below 7%

Thinking of switching banks? Here’s what you need to know.

The surcharge for using a credit card may be about to fall

Did you really win the Mega Millions jackpot or is it a scam?

If you enrolled in a short-term health plan, you could get a refund

New real estate selling rules: More questions than answers.

Big shakeup for real estate fees!

Attention student loan borrowers! Limited-time chance to cancel your debt!

Did you receive a large medical bill? Make sure it's not affecting your credit score

Gold prices hit record high. Is there still room to run?

ConsumerAffairs is linked to new Supreme Court Internet freedom cases. Here’s how.

Wow – another Social Security stimulus check so soon?

Here are the best and worst states to buy rental property

Free file fiasco: Deceptive ads, hidden costs, and data deletion

What car insurance company has raised rates the most?

IRS scammers on the loose! File taxes safely with this trick.

Here’s why you’re paying so much more for car insurance

What you should know before choosing a tax preparer

Where are gold prices headed? UBS says ‘higher.’

What bills can consumers negotiate? Believe it or not, quite a few!

Credit cards to get a lot safer and harder for you to be scammed

Can you afford your rent? A Harvard study finds 50% of renters cannot.

IRS 'refund' scam letters are in the mail. Be careful.

Do you use TurboTax? Do you know what it means when it says 'free?'

How to reduce credit card debt in 2024

Can you trust financial advice from TikTok?

White House tries again to forgive some student loans

Three things consumers need to know in the days ahead

Many economists say the consumer is ‘just fine.’ Are you?

You can now buy a Bitcoin ETF -- but should you?

Inflation ticked up in December

Government money for your phone, internet, heating, and cooling bills

Will 2024 be a better year to buy a house?

Federal government updates how to find unclaimed money

When buying gold you aren’t limited to using dollars

U.S. Bank to send nearly $6 million to consumers

IRS waives penalty fees for some back taxes

Living paycheck to paycheck? Here’s how to stop.

Costco has sold $100 million in gold bars since September

Tax season: what to know before you file in 2024

Amid high inflation, gold prices hit a record high

Have you fallen victim to an imposter scam on Zelle? A refund could be in your future.

The cost of heating your home may be less this winter

IRS unveils new brackets and other tax changes for 2024

Feds seek more regulation of fintech apps to protect consumers

Butter, coffee led October food prices higher

Has your bank account been closed? You aren’t alone.

Childcare costs have surged 30% in four years

The government proposes new protections for retirement savers

Why do some Realtors discourage solar panels? It’s complicated.

Consumers can add Venmo, PayPal, and debit cards to Apple Wallet

Here’s how much you have to earn to afford the median home

Credit reports are now free every week of the year

Rite Aid files for bankruptcy and will close some stores

Home sales have dipped and in some cities, so have prices

Biden adds some muscle to his fight against junk fees

Need help managing debt? Here are some tips.

Costco has begun selling gold bars

Here’s why buying a home is getting harder and more expensive

Buy Now Pay Later companies try to woo more customers

Inflation roared back in August, thanks to gas prices

Zillow launches 1% down mortgage plan

Here’s how to lower your homeowner's insurance costs

How satisfied are you with your credit card?

Pet scams, pet trips, and pet insurance -- what you need to know

Two legendary Wall Street investors turn bearish

Orange juice is about to get more expensive. Here’s why.

Sitting on an expired gift card? You have options, including a possible class action lawsuit.

More heat to worry about: Three very hot IRS scams

More companies are piling on fees. Can you spot them?

UPDATE: Mega Millions bring out mega scammers

President Biden is making another attempt to forgive student loan debt

A majority of seniors regret their retirement planning decisions

Farmers is the latest insurance company to pull out of a state

The cost of living slowed in June unless you rented an apartment

Wronged Bank of America customers to receive $100 million

Stamp prices are going up again Sunday

Are you ready to resume student loan payments? A financial adviser has some advice.

Credit card swipe fees could drive up families’ Fourth of July costs a half billion dollars

Will the stock market rally continue in the second half of 2023? Experts weigh in

President Biden gets some major players in the 'junk fees' game to change their tune

Why State Farm has decided not to insure homes in California

How rewarding are rewards programs? Not as much as in the past.

Are you a Bank of America customer? You may have money coming to you

Getting a medical procedure? CFPB warns consumers healthcare financing is loaded with pitfalls

Seniors looking to pick up a little extra money have more options than they might think

Are you ‘trapped’ in your home by your low mortgage rate? Many homeowners are, survey shows.

401(k) retirement accounts could see some big changes

Overspending on homes and cars lands many people in financial hot water

Amazon pierces the veil of high prescription prices

Using your credit card at public terminals is getting even more dangerous

Rocket rolls out a credit card it says will help users buy a home

Nearly 80% of young adults get their financial advice from guess who?

CFPB throws the book at one of the biggest debt collection companies in the U.S.

CFPB roots out illegal bank junk fees

An extension to file taxes doesn't mean an extension to pay taxes, IRS says

Thinking of moving to a cheaper state? We break down the numbers

What’s behind the decline in consumers’ satisfaction with banks?

Mortgage insurance premiums will go down for FHA borrowers

Are you eligible for the IRS's Credit for Other Dependents

Senior and low-income taxpayers can file their taxes with the IRS for free

Taxpayers can get assistance on 2022 taxes with new Saturday hours at Taxpayer Assistance Centers

Low and moderate income taxpayers can benefit from the Earned Income Tax Credit

Personal finance guru Suze Orman warns many consumers are already in a recession

The IRS offers these tips for taxpayers to prevent errors when filing taxes

Taxpayers can officially start filing 2022 taxes

Wells Fargo payments to wronged customers are going out now. Here’s what you need to know

IRS shares tax tips for gig economy workers

Consumers appear to be rebelling against high prices

Inflation ticked lower in December. Here’s what went up and here’s what went down

IRS issues tax relief for victims of California storms, extends filing deadlines

IRS urges taxpayers to prepare for a surge in scam phone calls

More Americans are feeling economic burnout as they enter 2023

Suddenly, home sellers are ready to deal

Would travel insurance have saved the day for Southwest travelers? Experts offer their opinion.

Wells Fargo fined $3.7 billion, with $2 billion going to customers

Instacart is helping consumers make the most of FSA funds before they expire

Mortgage rates are falling. Here’s why

In the wake of the FTX scandal, what is the future of cryptocurrencies?

The IRS is cracking down on online sellers paid through apps

IRS wants taxpayers to get ready for changes and has built a new tool chest to help out

IRS boosts standard deduction for 2023 tax year to account for inflation

IRS reports huge increase in texting scams and warns taxpayers to stay vigilant

The Fed has hiked interest rates again. Here’s how it may affect the stock and housing markets

The housing market moves closer to a correction

Grocery price increases hit a 43-year high in September

Rail lines and unions head off a potentially devastating strike

Here are the states where solar panels save the most money

Investors may be one reason you’re still having trouble buying or renting a home

Did you hear about the student loan forgiveness? Scammers did, too

The cost of raising a child is over $300,000

Changing real estate market puts consumers on the move

Having a ‘fair’ credit score in this housing market is costly

IRS warns taxpayers about new, hard-to-grasp “transaction” scams

Buy now, pay later comes with the risk of fraud, a new study suggests

Online banks win customer loyalty with personalized service

Bitcoin rebounds slightly, but making alternative investments may be wise

Gemini introduces new credit card that pays rewards in cryptocurrency

Housing market already shows signs of slowing down, experts say

FTC sues Intuit for falsely claiming TurboTax is 'free'

Legislators introduce E-cash as a way to digitize the American dollar

IRS warns consumers about cryptocurrency question on tax returns

Owning a home is now cheaper than renting in some housing markets

Social Security Administration changes full retirement age to 67

States take steps to protect patients from staggering medical bills

Bitcoin and Ethereum fall to their lowest values in six months

Gift cards carry a high risk of fraud, expert warns

Vanilla Prepaid gift cards trigger a string of post-holiday complaints

Target employees to make extra $2 per hour for working peak days during the holidays

Navient seeks to sell its student loan servicing business

Inflation increased 0.3% in August

Study finds a third of buy now, pay later consumers are behind on payments

Mastercard is replacing the magnetic stripe on its cards

Respect in the workplace is more important than perks for younger employees

New credit card pays rewards in bitcoins

Circle K jumps into cryptocurrency by rolling out a huge Bitcoin ATM network

Rude behavior in the workplace isn't too widespread, study finds

Consumer group says homebuyers should always have their own agent

Bitcoin price falls below $32,000 for the first time in months

Consumers spent $900 billion more online last year

Being more educated may not make you more satisfied with your job, study finds

Biden administration to give full debt relief to students defrauded by private, for-profit colleges

Homeownership prospects are improving in 2021, survey suggests

Will companies allow employees to work from home after the pandemic?

Costco to raise its minimum wage to $16 an hour

Mortgage delinquency rate falls below 6 percent for the first time in a year

Ben & Jerry’s parent company announces new living wage initiative

Cryptocurrency market takes a $200 billion tumble as Bitcoin loses ground

Small businesses can apply for a second round of PPP benefits starting today

Unequal compensation leads to less motivation in the workplace, study finds

IRS offers last-minute advice with July 15 tax-filing deadline quickly approaching

Older women are less protected by age discrimination laws than older men

Americans have taken full advantage of loan forbearance programs during pandemic

Target raises minimum wage to $15 an hour

HR managers predict working from home will continue for at least another year

Offering incentives may help sell your home in this turbulent market

IRS clears the air on why all stimulus checks aren’t the standard $1,200

Credit card companies lower credit limits as coronavirus pandemic rolls on

More than 26 million people have lost jobs during the coronavirus shutdown

Wells Fargo closes the Paycheck Protection Program loan window

More Americans are raiding their retirement accounts, study finds

Wells Fargo settles fake account scandal for $3 billion

Most consumers entered 2020 stressed out over debt, survey finds

What’s your biggest financial regret of the decade?

University of Phoenix to pay $191 million to settle charges that it deceived students

Consumer debt reaches record-high of $14 trillion

Report shows consumers are spending more with plastic instead of cash

Shopify complaints mount from online retailers and consumers

Online banking has become more widespread among consumers, survey finds

CFPB rolls out a new initiative to help consumers at tax time

Americans think financial education classes should be mandatory, survey finds

Researchers say Trump’s Fed criticism is hurting the central bank

Building a swimming pool in the backyard could boost home value, study finds

Ten percent of college students think credit cards are ‘free money,’ survey finds

New investors often fail to diversify their stocks, which could lead to disaster

Survey shows 45 percent of couples borrow money to pay for weddings

Hidden fees have become more common and more costly

Real estate study finds vacant homes sell for less

Consumers not using a travel-related credit card are leaving a lot on the table

Credit card companies increase their charge-offs of bad loans

New home sales surge in March while existing home sales decline

Study finds homeowner’s insurance rates have surged in the last decade

Major changes for consumer credit reports are starting to roll out

Ethical leadership in the workplace can create a positive work environment

It’s tax season. Are you ready for all the new changes?

World economists predict another great recession by 2021

Young adult cancer survivors faced with issues related to work and money

Home affordability is at its lowest level since just before the housing crash

Consumers getting refunds from record fraud judgment

Update to credit file law allows consumers to freeze their credit reporting

Checking work emails while commuting should count as part of the workday, study suggests

Average cost of childcare almost as much as rent

Floridians are clamoring for medical marijuana jobs -- but state laws limit opportunity

Chase teams with Expedia to beef up travel card perks

Expectations to answer work emails after hours hurts employees’ health, study finds

Mississippi sues Navient, claiming student loan abuses

New York City commission proposes minimum wage increase for Uber and Lyft drivers

Despite low unemployment, many college grads are out of work

What you don’t know about credit cards can hurt you

Report shows Social Security will pay more than it collects this year

Nearly 51 million households can’t afford basic necessities

Study finds gig economy is changing the future of retirement

Many companies still score low when it comes to ending the gender pay gap, report finds

Experian launches free tool to remove mistakes from credit reports

Consumers' top financial regrets and how to avoid them

Are you being overcharged for insurance?

Is the Consumer Financial Protection Bureau mission changing?

Federal proposal would allow employers to pool their workers’ tips again

Citibank to compensate some student loan borrowers

With federal flood insurance, corporations get a third of premiums and taxpayers get the bill

Hurricane Harvey likely to swamp not just Texas but also the federal flood insurance program

Survey finds owning a home still biggest part of American Dream

Reverse mortgage a risky way to increase Social Security payments

The changing face of job-hunting

How raising the minimum wage by $1 could reduce cases of child neglect

Average student debt doubles in a decade

Poll: consumers back the Consumer Financial Protection Bureau

A turnaround for new home construction

Consumers support strong regulation of Wall Street, poll finds

Most Americans can't afford a new car, study finds

Study finds Millennials spend far too much on vices

Consumer groups seek expansion of CFPB's authority

Six good credit cards for gasoline purchases

The growing conflict between insurance companies and repair shops

Education Department blasted over $6 billion in improper student aid payments

More employers planning to offer student loan repayment benefit

Court order shuts down 11 debt settlement companies

Here are some alternatives to taking out a payday loan

Why home prices may not level off anytime soon

One professor’s convoluted journey through FedLoan student loan forgiveness

Report: consumers' out-of-pocket medical expenses rising

What's your retirement strategy?

Why world tensions are making mortgages cheaper

How financial literacy can help ease anxiety about growing old

Class action suit claims BlackRock mismanaged employees' retirement funds

Education Department may renege on student loan forgiveness program

Average credit card interest rate at record high

Survey finds consumers don't know about the Consumer Financial Protection Bureau

Consumer groups file motion supporting CFPB in court battle

Feds sue student loan servicer Navient

Xerox pays $2.4 million to settle illegal debt collection charges

Health insurance industry rakes in billions while blaming Obamacare for losses

Experts: fewer illegal immigrants means higher housing costs

Study finds that more expensive weddings often lead to shorter marriages

Feds fine Clarity Services Inc. $8 million for consumer credit violations

Latest health insurance hacking compromises confidential data of 10.5 million people

FTC toughens rules barring "implied tying" of warranties to specific parts or service providers

Green Tree Servicing to pay $63 million to settle federal charges

The suspiciously large first paycheck: how does this job scam work?

Five myths about filing for college financial aid

Employers must follow strict rules for independent contractors

Online tool helps nail down real cost of college

“Replay” lets fraudsters disguise fake credit card charges as legitimate chip-card transactions

Inflation is low but the cost of living isn't

Could you get $2,000 in an emergency? 40% of Americans can't

Bank of America to pay $727 million for deceptive marketing of credit card add-ons

What you should know before trying Progressive's Snapshot

How to find a good bail bondsman

Foreclosure Backlog Will Take Decades to Clear Out

Payday Loan Lawsuit Brings $18 Million Settlement Against Advance America

CitiGroup Settles Predatory Lending Charges for $215 Million

Renting A House or Apartment - Your Rights as A Renter