Rising federal debt, persistent inflation fears, and uncertainty about future Federal Reserve policy have pushed Treasury bond yields to their highest levels in years.

Higher yields translate into more expensive mortgages, auto loans, credit cards, and business borrowing costs.

Savers are finally earning meaningful returns again on CDs, money market funds, and Treasury securities.

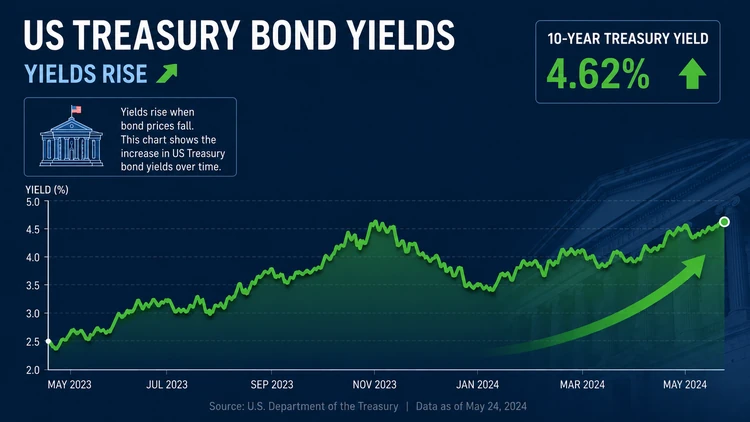

For years, interest rates on savings accounts were next to nothing — good for borrowers but bad for savers. But in recent weeks, there has been a sharp rise in U.S. Treasury bond yields, lifting borrowing costs for consumers while creating some of the best opportunities for savers in more than a decade.

The yield on the benchmark 10-year Treasury note — a key indicator that influences everything from mortgage rates to corporate loans — has climbed to levels not seen since before the 2008 financial crisis. Financial markets are signaling that investors now expect interest rates to stay higher for longer, even as inflation cools from its pandemic-era peak.

Treasury yields rise when investors demand higher returns to lend money to the federal government. Bond prices and yields move in opposite directions, meaning yields surge when investors sell bonds.

Growing debt load

Several forces are driving the increase.

One major factor is the federal government’s growing debt load. Washington continues to run large budget deficits, requiring the Treasury Department to issue massive amounts of new debt. As supply increases, investors are demanding higher yields to absorb it.

Investors are also increasingly concerned about rising prices. While inflation has slowed significantly from the highs reached in 2022, investors worry it could remain above the Federal Reserve’s 2% target for years. Higher inflation erodes the value of future bond payments, so buyers want greater compensation.

In addition, the Federal Reserve has kept short-term interest rates elevated in its effort to control inflation. Even though many investors once expected rapid rate cuts, the economy has remained surprisingly resilient, with strong employment and steady consumer spending reducing pressure on the Fed to ease policy quickly.

Global factors

Global factors are contributing as well. Foreign governments and central banks have reduced some of their Treasury purchases, while geopolitical uncertainty has made investors more cautious about long-term debt holdings.

The consequences are being felt throughout the economy.

Mortgage rates have climbed because they tend to track the 10-year Treasury yield. Higher home financing costs have made affordability worse for many buyers, slowing home sales and keeping pressure on the housing market.

Auto loans and credit card rates have also risen. Consumers carrying balances are paying substantially more in interest than they did just a few years ago. Businesses face higher financing costs as well, which can discourage expansion and hiring.

For the federal government itself, higher yields mean rising interest expenses on the national debt. Interest payments are becoming one of the fastest-growing components of federal spending.

Good news for savers

But the news is not all negative.

Savers, who endured years of near-zero returns after the Great Recession, are benefiting from higher interest rates. Banks, online savings accounts, certificates of deposit, and money market funds are offering yields that would have seemed unusually generous just a few years ago.

Treasury securities themselves have become attractive to conservative investors seeking relatively safe returns. Short-term Treasury bills now often pay more than many traditional savings products.

Retirees and income-focused investors, long starved for yield, are also finding new opportunities in bonds and fixed-income investments.