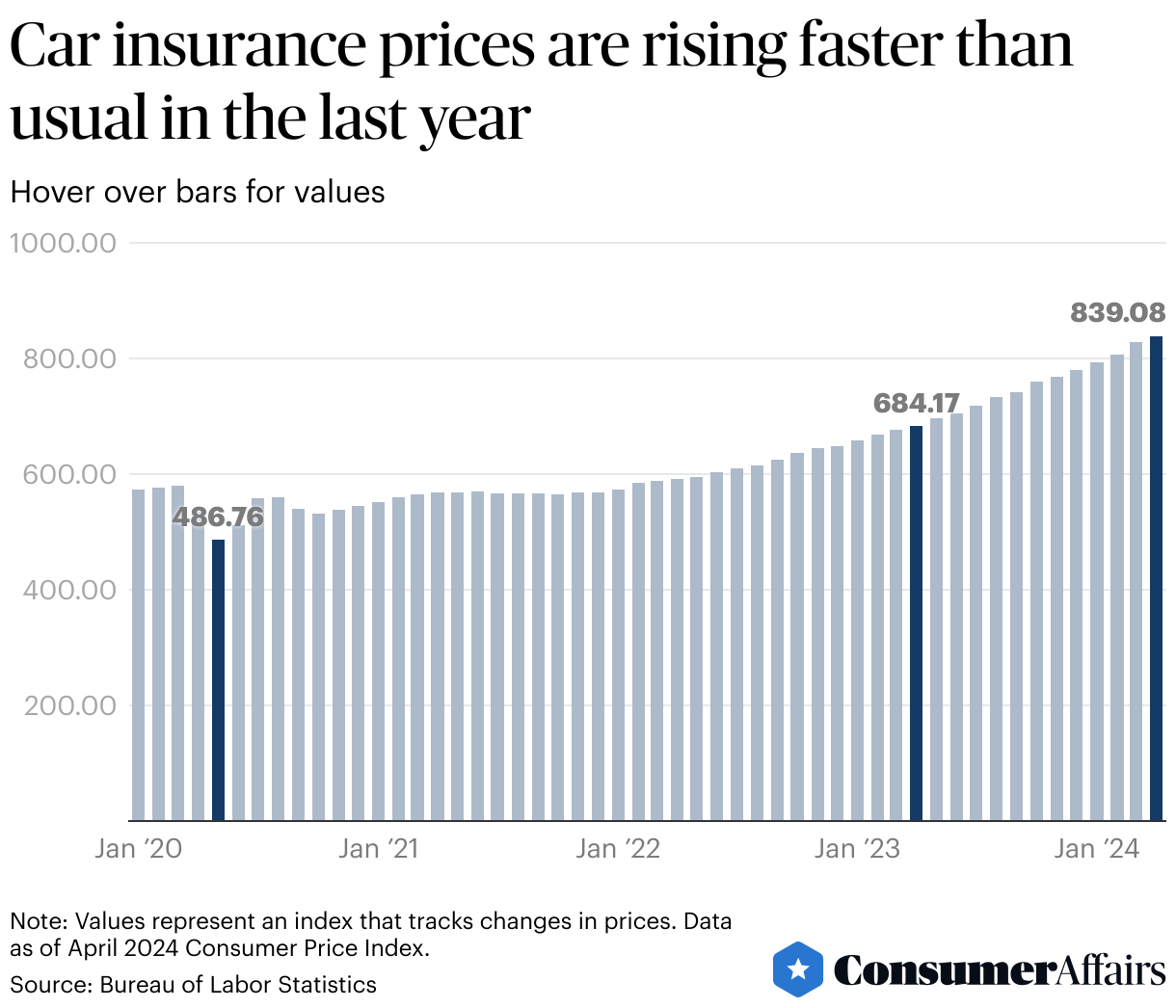

Car insurance costs keep climbing rapidly and are showing no signs of letting up.

The average price of motor vehicle insurance shot up to 22.6% in April 2024 from a year ago, slightly rising from 22.2% in March, the Bureau of Labor Statistics said. That also comes far above the average April yearly uptick of 8.5% since 2020, a ConsumerAffairs analysis finds.

Over five years from April 2019 to April 2024, car insurance costs have risen 47%, largely after spikes in recent years.

By month, car insurance prices picked up 1.4% in April from March, down from the 2.7% increase between March and February. The last time car insurance prices fell was Dec. 2021, but only by 0.06%.

Over five years, the biggest monthly drop in car insurance premiums was nearly 9% in May 2020 during the pandemic when people drove less and there were fewer accidents.

“There’s no simple reason car insurance is going up,” said Michael DeLong, research and advocacy associate for fair auto insurance at the nonprofit Consumer Federation of America.

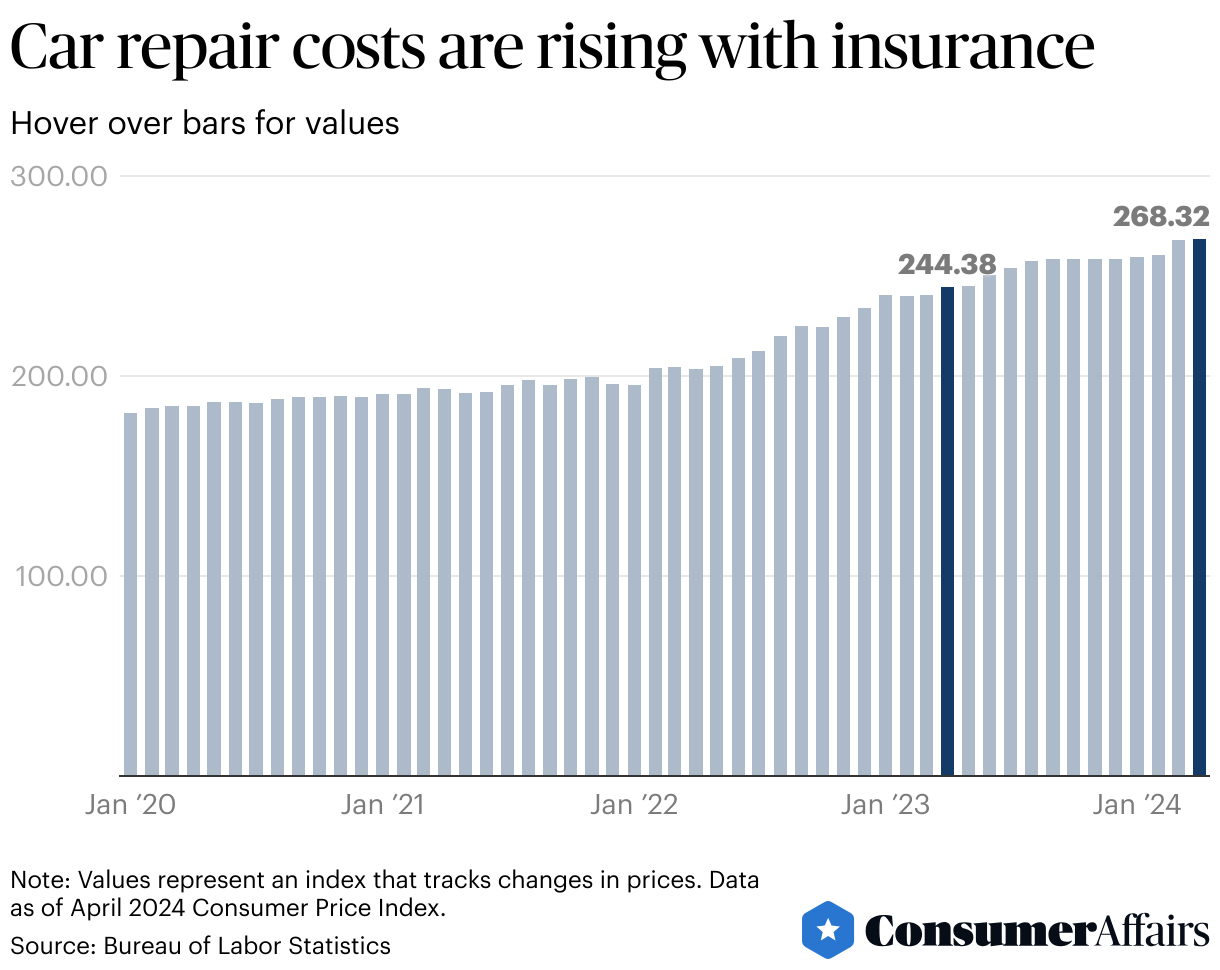

A lot of factors are hiking car insurance up, he said, including higher costs for repairs and elevated levels of reckless driving. Today’s cars also have increasingly expensive technology that makes them costlier to insure, such as sensors and cameras that can get damaged in a minor fender bender. And all too often, he said insurers are boosting prices to rake in profits and regulators aren’t doing enough to stop them.

Auto insurers decide what they charge based on a wide range of criteria. They consider your driving record, such as how much you drive, tickets and crashes, but also socioeconomic factors, DeLong said, including your education level, your job, if you own or rent a home, where you live and even your gender. Some insurers charge men more, others women more, he said.

Credit is another big reason people pay extra. Even if you have a perfect driving record, an insurer can charge you double if you have a poor credit score. “It ought to be based only on your driving record,” he said.

Still, the main reason that car insurance costs are going up is because years of inflation have raised the cost of repairing and replacing cars, said Bob Passmore, department vice president of personal lines at industry group American Property Casualty Insurance Association.

“Even if a driver has not had a claim or a ticket, auto insurance premiums have been on the rise for the simple reason that the cost of what goes into auto insurance has been rising,” he said.

“Insurers are advocating for better infrastructure, including reliable supply chains for critical auto parts and safer roads, which should result in fewer crashes, and controlling claims costs to help keep insurance premiums affordable for consumers,” he added.

What could bring overall auto insurance prices down

“Unfortunately, auto insurance prices usually go in one direction: up,” DeLong said. “You have this product the government is forcing you to buy, but they aren’t doing enough to make sure it is affordable for drivers.” He said Americans need to pressure the government to act, but that is difficult because most people are unfamiliar with the landscape.

Auto insurance is regulated at the state level, which is why DeLong said voters should write to and call state politicians and departments overseeing insurance to encourage them to rein in prices. The strictest rules empower states to approve car insurance costs before they go into effect.

Yet, a lot of agencies don’t have strict regulations and are too cozy with the industry, DeLong said. The top 10 auto insurers, including AllState, Farmers and Geico, have won regulatory approval to boost rates by more than 20%, S&P said in January. The increases topped 30% in 16 states, including hikes of nearly 46% in Texas and 39% in Ohio.

“Some regulators aren’t very interested in protecting consumers at all and just give the insurance industry what they want,” DeLong said. “Some are even captured by the insurance industry because their commissioners or senior executives come from the industry or they want to leave and get jobs as insurance executives.”

How to save money on car insurance

Insurance experts say there are many ways to bring your auto insurance costs down and decide on the best car insurance company.

Shop around: If you have the time, spend up to a couple hours plugging in your information at various providers to make sure you get many quotes to compare. You can also use websites to quickly compare prices, such as and Value Penguin.

Speak with insurance agents: An agent might know about current deals and smaller, cheaper companies that aren’t as well known.

Bundle insurance: You can get discounts for combining your auto insurance with other insurance like homeowners, renters and motorcycle insurance.

Improve your credit: Check for errors in your credit score and pay off debt.

Pay-as-you go: A lot of insurers will slash premiums based on how much you drive, which is especially helpful if you work from home.

Pay in full: Some insurers give discounts if you pay your premium in full, including in six-month installments, instead of monthly.

Telematics: If you are comfortable with your data getting collected, you can plug in a device in your car or download an app on your phone that watches your driving behavior and calculates your insurance premium, such as if you speed or you slam on the brakes a lot. Telematics can significantly lower costs if you are a good driver.

Bare-bones coverage: This makes more sense for older, less valuable cars. It is risky, but you can opt only for liability coverage if you damage another person’s vehicle, instead of additional coverage if you damage your car or it is stolen.

Miscellaneous discounts: Some insurers give discounts if teenagers have good grades, you are a member of the military, have an anti-theft device on your car or if you have a paperless insurance policy.