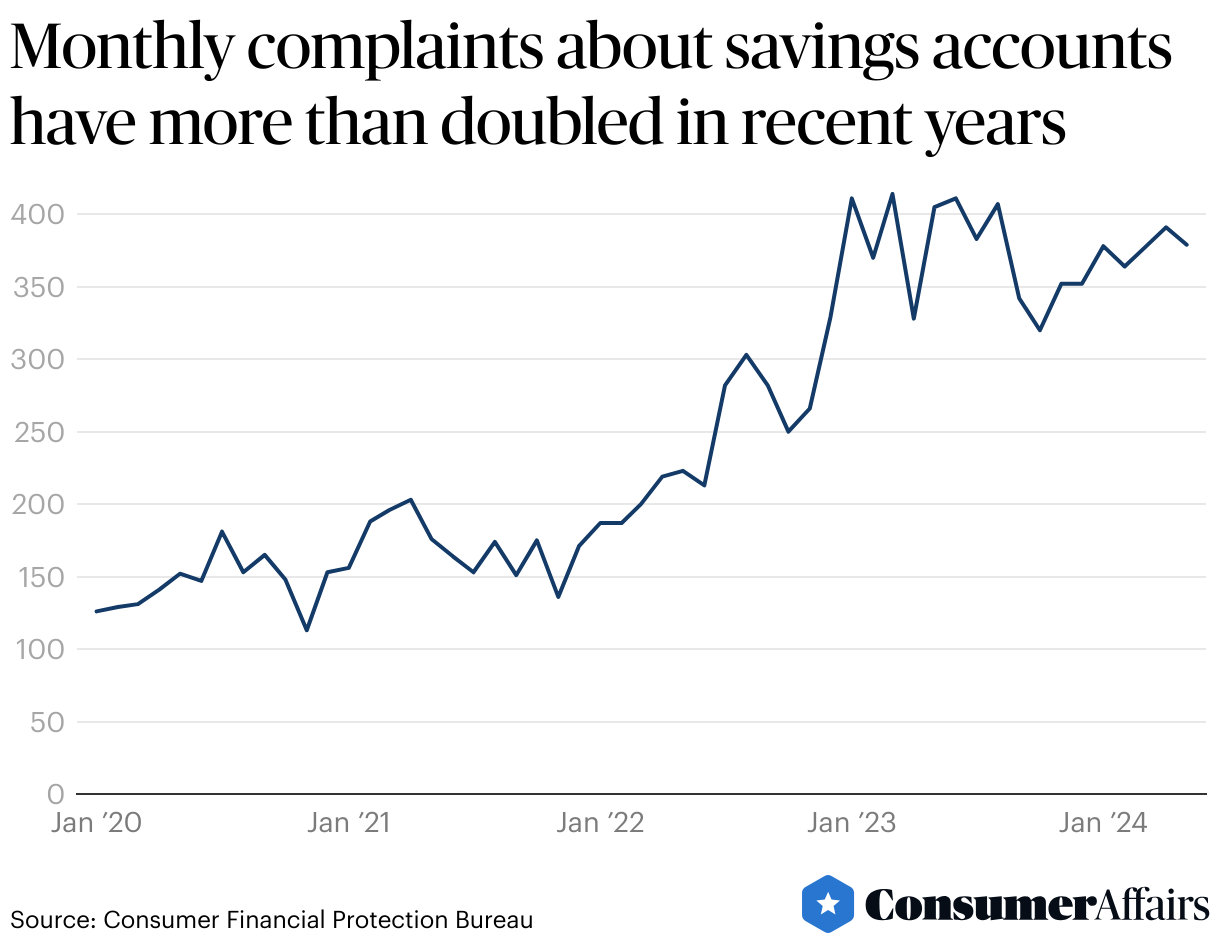

Bank customers probably expect that their savings account is just like savings accounts have always been – a place where you can save money and earn a little interest.

That would be a bad guess, however. The number of monthly complaints about savings accounts at the Consumer Financial Protection Bureau (CFPB) has more than doubled in recent years.

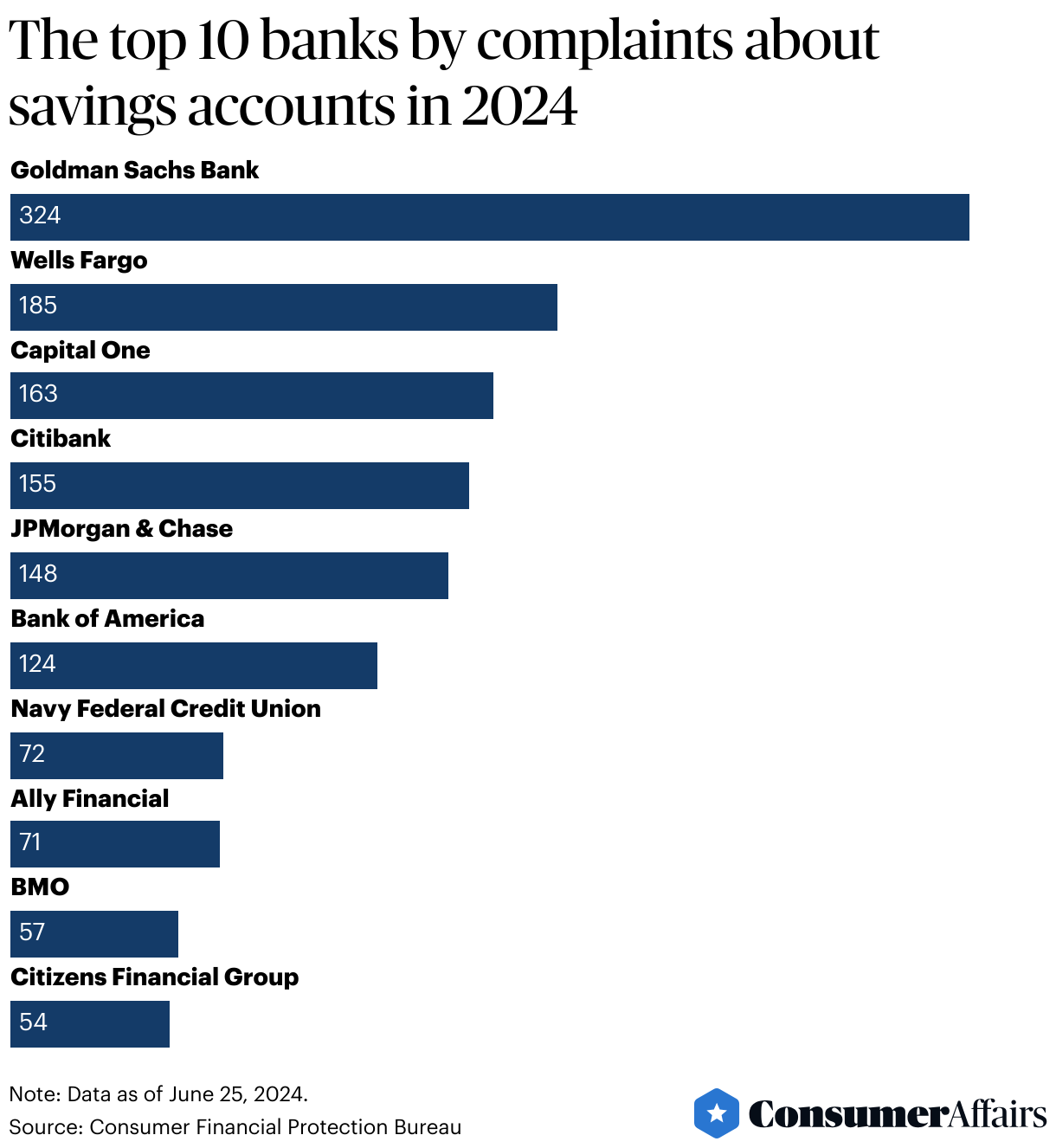

What banks got thrown under the bus the most? Goldman Sachs, Wells Fargo, and Capital One top that list. Here's what the CFPB data showed:

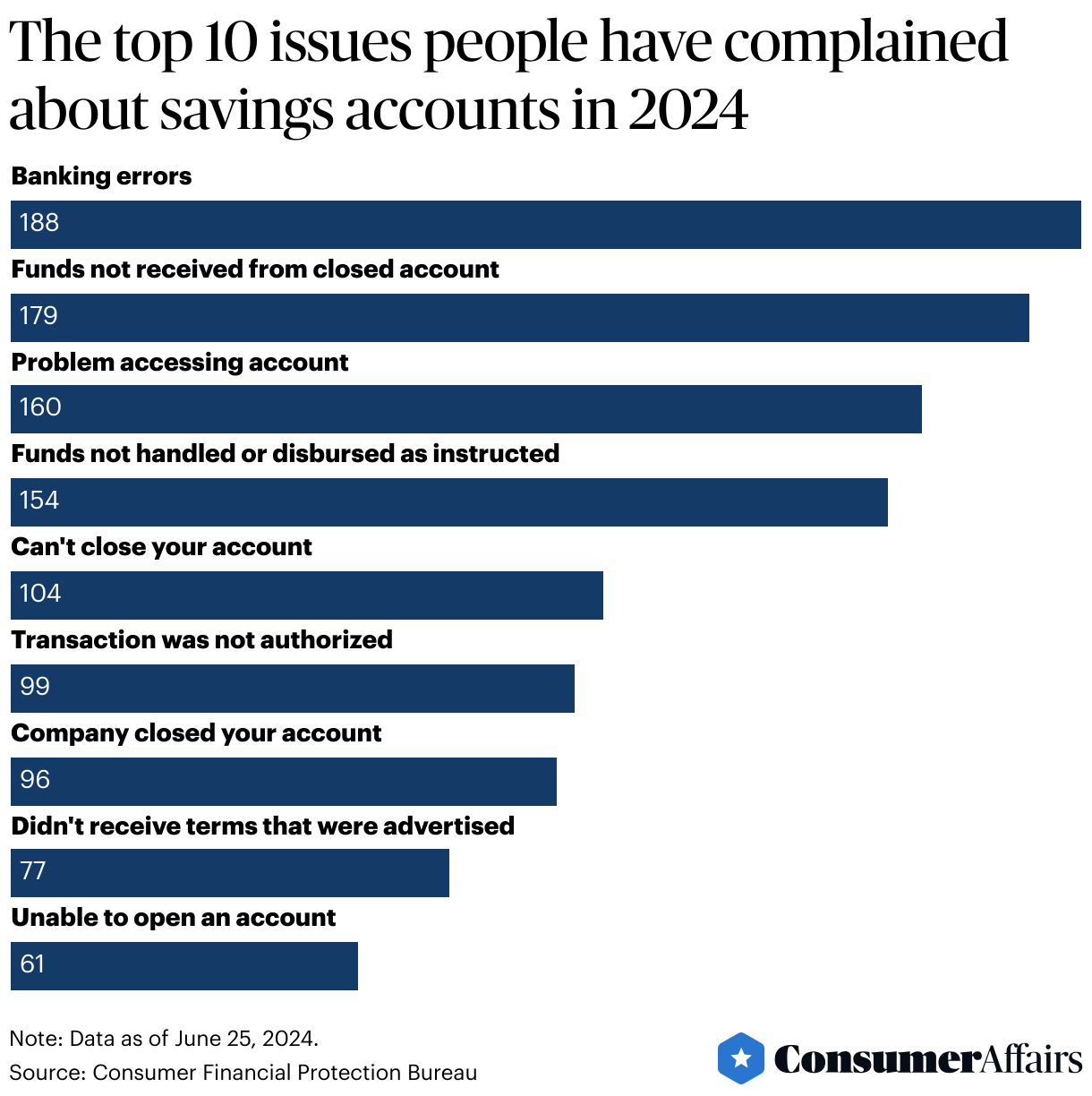

But there are wrinkles inside of those complaints

ConsumerAffairs dug into the narratives of a couple of complaint areas that bank customers might not be fully aware of. Here's what we found:

Delays

Much of the chatter about banks and scams usually revolved around checking accounts, but one of the primary rising issues is the increase in unauthorized withdrawals or fraudulent activities in savings accounts. This includes issues like scams, phishing attacks, and unauthorized account access leading to stolen funds.

Another consumer complaint is that they’ve had problems with accessing their funds due to unexpected holds or delays in processing deposits or transfers. This can cause financial hardship and frustration.

Fees

Some consumers have raised concerns about unexpected fees, changes in interest rates without proper notice, or discrepancies between advertised and actual interest rates. Like this Citibank customer who complained to the CFPB:

“Citibank called me today to tell me my free savings account was overdrawn. I asked how it could be overdrawn. Citibank said that my free savings account now costs {$15.00} per month. I told them I was not going to pay this fee and they can close the account,” the consumer wrote.

“I have an existing business account and Citibank solicited me to open a free checking and savings account because of my business account. Citibank started charging fees for my checking account without notice. Citibank stole all the money out of my checking account and said they would refund only {$75.00} to me which they never refunded. Now the same game with the free savings account.”

Unexpected rate changes

Consumers also complained about out-of-nowhere interest rate changes -- decreases, misleading promotional rates, and a lack of transparency about those rate changes.

For example, some consumers have expressed frustration that banks aggressively raise interest rates on loans and credit products when the Federal Reserve increases rates but are slow to pass on those increases to savings account holders.

That cups-and-ball trick spills over to high introductory interest rates a bank uses to attract new customers, but then rates often expire after a short period, leaving consumers with much lower returns than expected.

One consumer complained about such an issue with US Bank. They said that after seeing an advertising flier promoting a certain savings account interest rate, they asked the banker for details.

One detail they wanted to know about was “introductory rates” and said that they read the fine print on the flier to see if this rate was one. Nothing in the fine print, so they asked a banker. They said the same thing

Of course, what was pitched was not delivered. But wouldn’t you know it – the rate did drop. So they asked someone for an explanation.

“She then conveys to me that my rate drop is due to it being "XXXX months'' since I opened my account," the consumer wrote "I explain that this was not stated in any of the disclosures I read. She stated that ‘rates are subjected to change at any time’. … She expresses that there are others that have been impacted as well and there is nothing she can do. I tell her that I feel completely deceived. She again states that there is nothing she can do.”

The consumer went on to validate her situation, adding that the rate plan which she signed up for was still being advertised by US Bank.

"It's on their website and the paper adverts are still there. I feel deceived. This feels entirely like a bait and switch scheme.”

Say something!

What happened with these customers aren’t isolated instances. Fixing these issues probably isn’t going to be a top priority anytime soon at the bank level, so savings account holders need to watch their accounts with the same proactive concern they use with their checking accounts.

And, if you say something to someone at your bank and it goes nowhere, you should think seriously about filing a complaint with the CFPB. It’s a lot less stressful than hours on the phone trying to plead your case to someone at the bank.

Plus, complaints are effective. When ConsumerAffairs looks at the complaints the agency receives, there are many banks that sit up, take notice and fix what happened in a timely fashion. In fact, 98% of complaints sent to companies get timely responses, the agency claims.

The CFPB makes it easy and secure to submit a complaint and track your status. The fastest way to get started is to go consumerfinance.gov/complaint. If you get stuck and need help while you’re online, you can chat with one of its team members on that same site.

You can also submit a complaint over the phone by calling the agency at (855) 411-CFPB (2372), toll free. The agency’s call centers are U.S.-based and can help you in over 180 languages, as well as taking calls from consumers who are deaf, have hearing loss, or have speech disabilities.

For details on what makes an effective complaint and what happens after you file a complaint, the agency answers those questions, here.

Dieter Holger contributed graphics to this article.