How many days each month do you have to work in order to own a home? It depends on where you live.

According to new data from Realtor.com, the average homebuyer now needs to work 10 days each month just to afford their mortgage payment on a median-priced U.S. home. And for some, that figure stretches well beyond two work weeks.

The national median home price now stands at $412,000, with the typical mortgage payment, including taxes and insurance, reaching levels that demand a growing share of household income. Charlie Lankston, executive editor at Realtor.com, points to two key culprits: runaway home prices and persistently high mortgage rates.

According to Lankston, home prices have risen faster than incomes, widening the gap between earnings and housing costs. But the gap is greater in some states than others

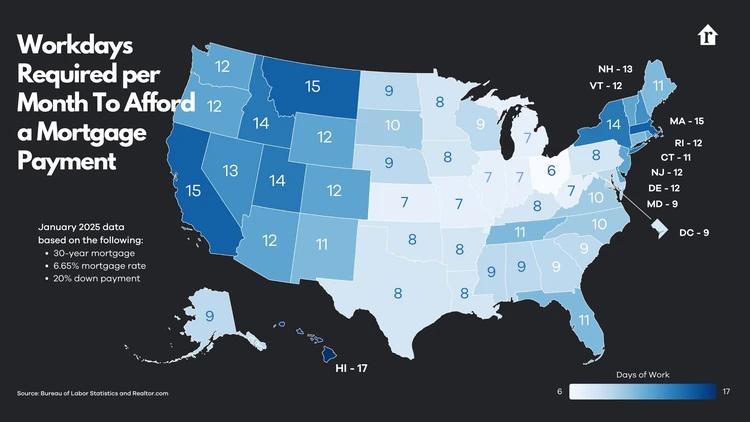

Nowhere is the pressure more acute than in Hawaii. With its unmatched scenery and enviable climate, the state also boasts the highest median list price in the country—$796,947. Homeowners there must work 17 days per month just to afford the average $5,222 monthly mortgage payment. That’s more than three-quarters of a standard work month.

California residents are close behind, requiring 15 workdays to cover a monthly mortgage of $4,773. In Montana, where housing costs have surged amid population growth and the rising popularity of cities like Bozeman, the average homeowner must also work 15 days to manage a mortgage on a $613,275 home.

California residents are close behind, requiring 15 workdays to cover a monthly mortgage of $4,773. In Montana, where housing costs have surged amid population growth and the rising popularity of cities like Bozeman, the average homeowner must also work 15 days to manage a mortgage on a $613,275 home.

The Midwest holds the line on affordability

By contrast, homebuyers in the Midwest and parts of the Southeast enjoy a far lighter burden. In West Virginia and Ohio, where the median home list prices are $247,000 and $259,450 respectively, monthly mortgage payments can be managed with just six to seven workdays.

Kansas, Missouri, Indiana, Illinois, Michigan, and other central states also allow buyers to cover housing costs with roughly a week of work per month. These regions remain some of the few where housing affordability has not spiraled out of reach for the average wage earner.

The geographic disparity highlights the widening gap in housing affordability across the U.S. While many buyers in the heartland still find a feasible path to homeownership, those in high-demand states face a significantly tougher climb.

As policymakers and economists continue to debate solutions, one thing is clear: for most Americans, affording a home now takes more time on the clock – literally. Whether it’s six days or 17, the cost of owning a piece of the American dream is being paid in work hours, and the clock is ticking.