Homeowners in almost every corner of the U.S. are having to pay higher annual insurance premiums, worsening the struggle to find affordable housing, according to a major study released today by the nonprofit Consumer Federation of America.

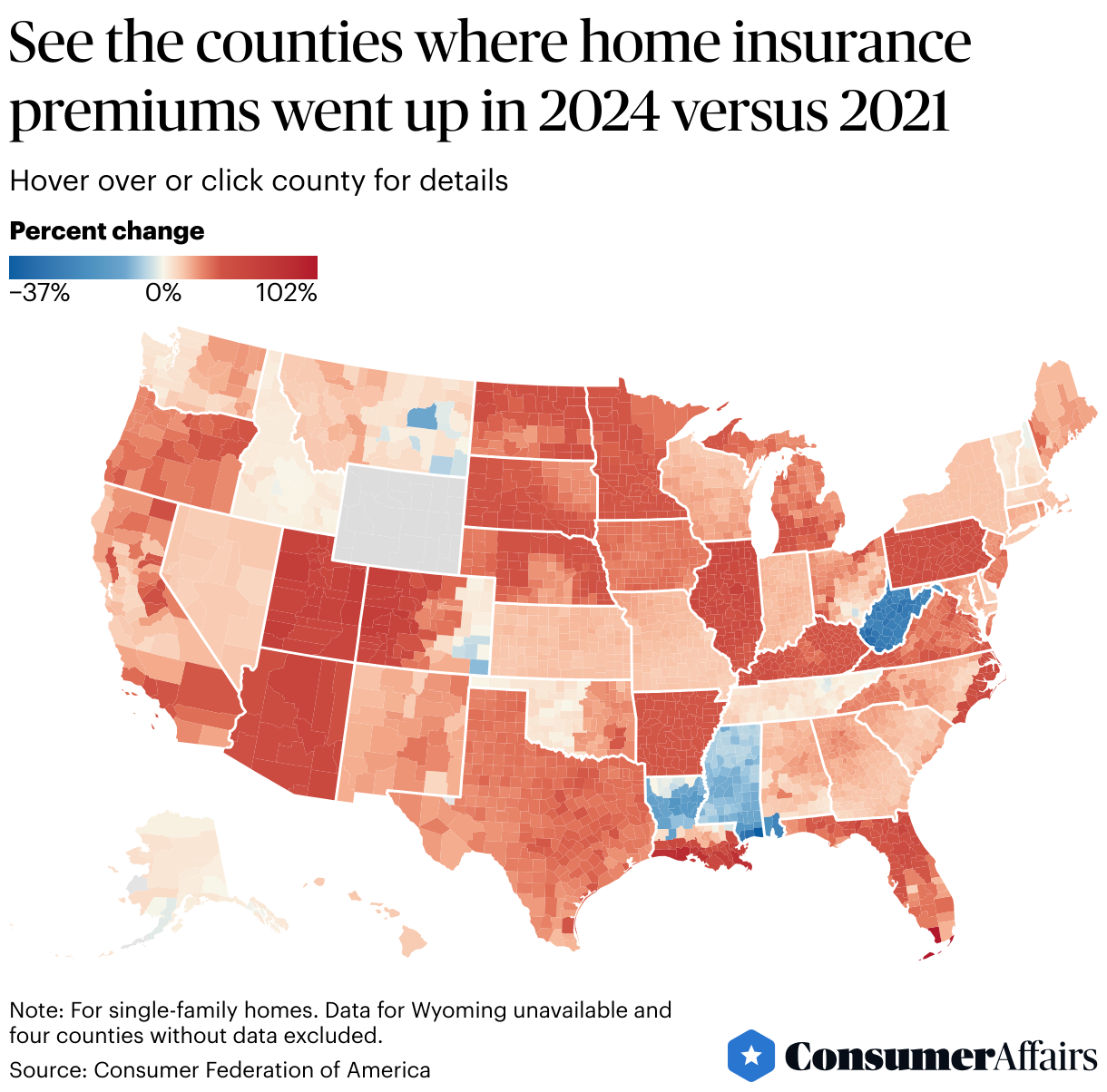

Insurers raised homeowners insurance premiums for single-family homes in 95% of U.S. ZIP codes in 2024 compared with 2021, the study found. And among 3,116 counties with data, there were only 191 where annual homeowner insurance premiums fell.

“The skyrocketing price of insurance premiums is deepening the housing crisis from Salt Lake City to New Orleans and beyond – and homeowners across the country are feeling the strain,” said CFA’s Director of Housing Sharon Cornelissen, a lead author of the report, in a news release.

“If we want to protect affordable homeownership, federal and state policymakers need to take action to address the rising costs and reduce risk for individuals and communities,” Cornelissen said.

A typical homeowner saw their annual homeowners insurance premiums rise $648 across the country, and collectively Americans have paid around $27 billion more over the past three years, the study said.

Increases have often been steep: In a third of ZIP codes, homeowners saw their premiums rise more than 30%.

The rising cost of homeowners insurance is making it harder to mortgage a home and people who fully own their homes are increasingly foregoing the insurance if they can, putting them at risk of financial ruin. Other homeowners are buying cheaper, weaker insurance.

For homeowners with a mortgage, homeowners insurance isn't optional because it's required by lenders.

The insurance covers monetary damages from unexpected events, including a burst pipe, hailstorm, fire or hurricane, but it generally doesn't cover flooding that homeowners living in Federal Emergency Management Agency-designated (FEMA) areas have to pay for.

"Homeowners may be forced to sell their home or risk defaulting on their mortgage if they can no longer aord the combined costs of high insurance premiums and their mortgage payments," the study said, pointing to how a premium increase of $500 was linked to a 20% higher rate of mortgage default.

Why is homeowners insurance getting more expensive?

The study said homeowners insurance has been going up for a lot of reasons: More expensive construction and building materials, a costlier global reinsurance market, weak government oversight and climate change.

"While hurricanes and wildfires often attract most attention, a rise in extreme weather events is impacting almost all parts of the country, including many states in the Midwest," the authors said.

Another driver of the increases is more expensive reinsurance, which is insurance for insurers that is unregulated at the global level.

Reinsurance companies, often based in Europe and Bermuda, have increased their prices for U.S. insurers for six years in a row, the study said.

In terms of government involvement, homeowners insurance is regulated at the state level and the rules vary in their toughness, with fewer states requiring a review or approval of a premium increase before it can be charged.

"Many of the insurance commissioners tasked with overseeing the insurance market in their state have proved to be exceedingly deferential toward the insurance companies they ostensibly regulate," the authors said. "Without public policy interventions, it seems likely that insurance affordability and availability pressures will only grow more intense, and more homeowners will struggle to find insurance products they can afford."

A closer look at where homeowners insurance is getting more expensive

Some states have seen much steeper hikes in homeowners insurance.

Homeowners insurance premiums were rising fastest in Utah, with a an average 59% increase, followed by Illinois (50%), Arizona (48%), Pennsylvania (44%) and Nebraska (35%).

In dollars, the biggest premium hikes were in Florida by $2,118, Louisiana ($1,775) and Kentucky ($1,426).

Florida is the most expensive state to buy homeowners insurance: A Florida homeowner with a mid-range credit score and a $350,000 replacement value home could expect to pay $9,462 per year for insurance, equal to $789 per month in 2024, the study said.

Only two states had an average decline in homeowners insurance premiums: West Virginia with -24% and Mississippi with -15%.

Cities have also seen varying severity in hikes.

Salt Lake City, Utah had the biggest spike in premiums among major cities, with a 62% average increase, followed by New Orleans (58%), Phoenix (47%), Chicago (46%) and Omaha (39%), the study said.

Tips for lowering homeowners insurance premiums

The Insurance Information Institute has suggestions to lower homeowers insurance bills:

- Shop around: Compare multiple insurers, contact your state insurance department, check consumer guides, speak with insurance agents and use online comparison services to get a good price.

- Raise deductible: Increasing your homeowner insurance deductible, or what you pay towards a loss, from typically $500 to $1,000 can lower the amount you pay in monthly premiums.

- Bundle insurance: Buying both your car and home insurance from the same provider can get you a discount.

- Stay with insurer: Keeping the same insurer for several years can get you a discount as a long-term policyholder.

- Improve disaster resilience: You may be able to save on premiums by adding home upgrades such as storm shutters, reinforcing your roof and buying stronger materials.

- Improve security: Installing burglar alarms, dead-bolt locks, smoke detectors and fire sprinklers can lower your monthly homeowners insurance premiums.