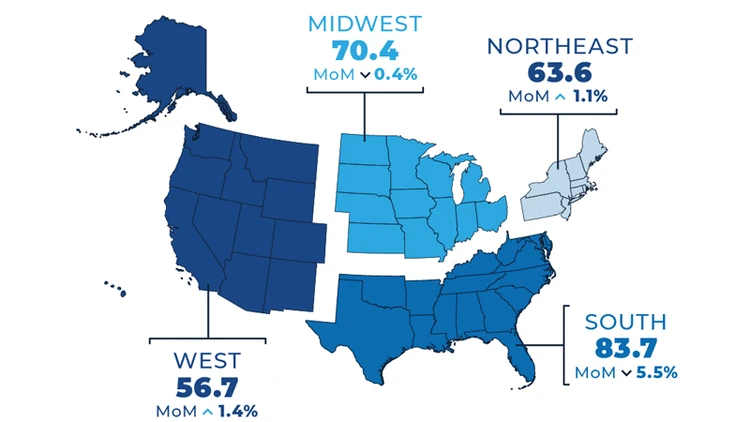

Pending home sales, one of the most forward-looking indicators of housing market health, plunged 2.1% from April. Sales were down 6.6% year-over-year, according to a report by the National Association of Realtors (NAR).

Pending home sales measure the number of contracts that were signed during the month, with completed transactions taking place over the following 60 days. May’s number was a six-month low.

It follows a report earlier this week that new home sales fell nearly 12% in May. Could the long-awaited home price correction be about to take place?

Until now, home prices have continued to rise because there were enough buyers who could afford both high home prices and 7% mortgage rates. But has the housing market finally run out of those buyers?

‘At an interesting point’

“The market is at an interesting point with rising inventory and lower demand,” said NAR Chief Economist Lawrence Yun. “Supply and demand movements suggest easing home price appreciation in upcoming months. Inevitably, more inventory in a job-creating economy will lead to greater home buying, especially when mortgage rates descend.”

But Yun is not predicting that prices will go down anytime soon. In its report, NAR said it expects the median existing-home price will increase to a record annual high of $405,300 in 2024, from $389,800 in 2023. It also expects the median home price to rise to $412,000 in 2025.

But an absence of buyers could lead to price reductions in some markets – a trend that might be offset should mortgage rates begin to come down and bring more buyers to the market. Shmuel Shayowitz, president of Approved Funding, a mortgage lender, says lower rates all depend on how the Federal Reserve views inflation.

“The Federal Reserve is waiting for convincing data to show that inflation has eased, and I believe we will start seeing this with the June CPI (Consumer Price Index) readings,” Shayowitz told us recently. “The two biggest components to look out for in the CPI data are Shelter and Motor Vehicle Insurance. Shelter makes up 45% of the core inflation reading and is the single biggest component, while Motor Vehicle Insurance makes up 3.6% but has spiked over 23% year over year.”

The Labor Department will report June’s Consumer Price Index during the second week of July.