Carrie Joy, founder of WorkMoney, says the path to financial stability isn't a perfect budget — it's a handful of small wins that create momentum.

Many consumers spend hours hunting for deals but never make the phone call that could save them hundreds of dollars a year in interest charges.

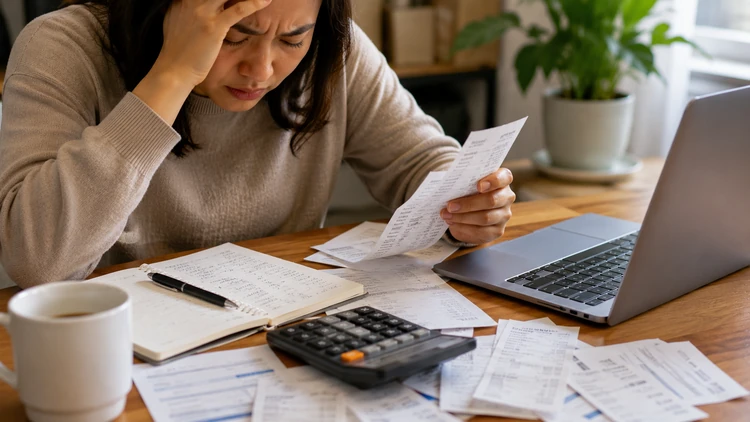

From canceling forgotten subscriptions to building a $1,000 "Life Happens Fund," these simple habits can help reduce financial stress and put you back in control.

If it feels like your paycheck disappears faster than ever these days, you're definitely not alone.

Many Americans are working hard, earning more than they did a few years ago, and still feeling financially stressed. Grocery prices remain stubbornly high and insurance premiums keep climbing. Not to mention that rent, healthcare, and utility costs continue to eat away at household budgets.

To learn how consumers can stop feeling financially stuck, ConsumerAffairs spoke with money expert Carrie Joy, founder and CEO of WorkMoney.org, a nonprofit organization that helps more than nine million Americans navigate money.

Joy’s approach is different from the typical financial advice that focuses on cutting every possible expense or creating a perfect budget. Instead, she encourages people to focus on building momentum through small wins that create a greater sense of control.

Here are five moves she recommends making right now.

1. Make one phone call that could save you hundreds

If Joy could recommend just one financial task for consumers to tackle this week, it would be surprisingly simple.

Call your credit card company today and ask for a lower interest rate.

According to a recent LendingTree survey, consumers who asked for a lower interest rate received an average reduction of about seven percentage points. Most consumers never even think to ask!

On a $7,000 credit card balance, that can translate into roughly $400 to $500 in annual savings. That's a pretty solid return for a five-minute phone call.

"They would rather keep you paying something than lose you altogether," Joy says. So they’ll often help you out by giving you a lower interest rate.

Not sure what to say? She recommends a straightforward approach:

"Hi, my name is [your name]. I've been a customer for [X] years. I'm calling because I've seen other cards offering lower rates than the [XX%] you're giving me now. I'd love to keep my account with you, but I need a better rate. What can you do for me?"

Before calling, know your current APR, how long you've been a customer, and what competing cards are offering.

And don't stop with the interest rate. The same LendingTree survey found that:

- 95% of people who asked had an annual fee waived.

- 89% had a late fee removed.

Pro tip: If the first representative says no, ask for the account retention department. These teams often have more flexibility when it comes to offering discounts and rate reductions. If you get no help, hang up and call again the next day. There’s a good chance the next rep you speak with can help you out.

2. Change your money story

Joy believes many financial problems start before money ever enters the picture. They start with how people think about themselves.

One exercise she frequently recommends is creating a simple positive money statement and repeating it daily. The phrase that helped her during her own financial struggles was: "I can be good at money."

It sounds almost too simple. But behavioral science suggests people are more likely to take positive action when they believe change is possible.

For consumers who have spent years feeling behind, ashamed, or overwhelmed, changing the narrative can be a powerful first step.

Pro tip: Write your money statement on a sticky note and place it somewhere you'll see every day. The goal isn't motivation, but rather building a healthier relationship with money over time.

3. Hunt down the subscriptions you're not using

As I’ve talked about before, subscription creep is a real thing, and it has become a real budget problem for families.

A recent CNET survey found that Americans spend an average of about $1,080 annually on subscriptions, with roughly $205 going toward services they don't actually use.

The sneaky part is that many of these charges are small enough to go unnoticed. Common offenders include streaming services, fitness apps, food delivery memberships, cloud storage plans, and premium shopping memberships.

Joy strongly recommends reviewing the last three months of bank and credit card statements and looking for those recurring charges.

Then ask yourself one question, "Have I used this in the last 30 days?" If the answer is no, cancel it.

Netflix, Hulu, Spotify, and countless other services will gladly take you back later if you change your mind.

Pro tip: Those food delivery memberships like DashPass, Uber One, and Grubhub+ are among the easiest subscriptions to forget about because they quietly renew month after month.

4. Build a 'Life Happens Fund'

Traditional financial advice often tells consumers to save six months of expenses. But for many households right now, that feels completely unrealistic.

Joy recommends a different approach. Start with just $1,000. She calls it a "Life Happens Fund," because life inevitably throws expensive surprises your way.

Things like car repairs, vet bills, broken appliances, and medical expenses are inevitable. And if you have a small fund to help with those expenses, it “keeps you from running back to a credit card every time something breaks.”

According to the Federal Reserve, 37% of Americans would struggle to cover a $400 emergency using cash. That's why Joy says the first $1,000 matters so much. It creates that much needed distance between an emergency and a credit card.

"Money is math and feelings," she says. The math is saving consistently (even $10/week) and the feelings part is celebrating your progress towards reaching $1,000.

Joy encourages consumers to recognize milestones rather than waiting until they achieve some perfect financial goal. When you hit $500, acknowledge it by buying yourself a small treat. When you hit $1,000, celebrate it. Building that confidence is all part of the process.

Joy knows firsthand how challenging it can be. As a single mother, it took her a year and seven months to save three months of bare-bones living expenses. But she says the peace of mind was life-changing.

"Money might not buy happiness," she says, "but it sure did buy me a lot less fear and anxiety."

Pro tip: Automate a transfer of just $10 or $20 a week into a separate online savings account. Small automatic deposits are often more successful than ambitious savings goals that never get started.

5. Stop letting convenience sabotage your budget

One of Joy's biggest money rules is surprisingly simple: Make impulse spending harder.

She personally avoids ‘Buy Now, Pay Later’ services and removes shopping shortcuts from her phone that encourage unnecessary purchases.

That includes removing things like food delivery apps, one-click purchasing, Apple Pay autofill, and shopping apps (especially Amazon) that she doesn't regularly use.

Instead, she keeps a simple wish list. When she wants something, she writes it down and waits until the end of the week. The strategy creates a pause between the impulse and the purchase. Most of the time, she discovers she no longer wants it and the desire to buy the item passes.

Stop using shame as a budgeting strategy

Lastly, perhaps Joy's most important advice has nothing to do with saving money at all. It's all about giving yourself some grace.

Many consumers make a financial mistake and then avoid looking at their finances altogether. They stop opening bills, stop checking balances, and flat-out stop paying attention. That's when small problems roll into bigger ones.

Joy believes shame is one of the least effective financial tools available. Mistakes happen. The key is to acknowledge them, learn from them, and move forward.

"Make the mistake, name it, remember you're not alone, and get back on track," she says.

Financial success isn't about perfection. It's about persistence. And for consumers feeling overwhelmed by today's economy, that may be the most valuable money lesson of all.