- Drivers with a perfect driving record can pay twice as much for car insurance if they have bad credit.

- Improving a credit score from "very poor" to "exceptional" can yield car insurance savings of 273%.

- Recent laws, although not widespread, are delivering car insurance savings for drivers with bad credit.

Car insurance is another reason to aim for a good credit score.

Drivers with bad credit can pay $4,500 more a year for car insurance than drivers with perfect credit, even if they have a flawless driving record, according to an analysis by insurance-comparison website The Zebra.

By comparison, a driver guilty of a hit-and-run would see their car insurance costs go up $2,088 on average.

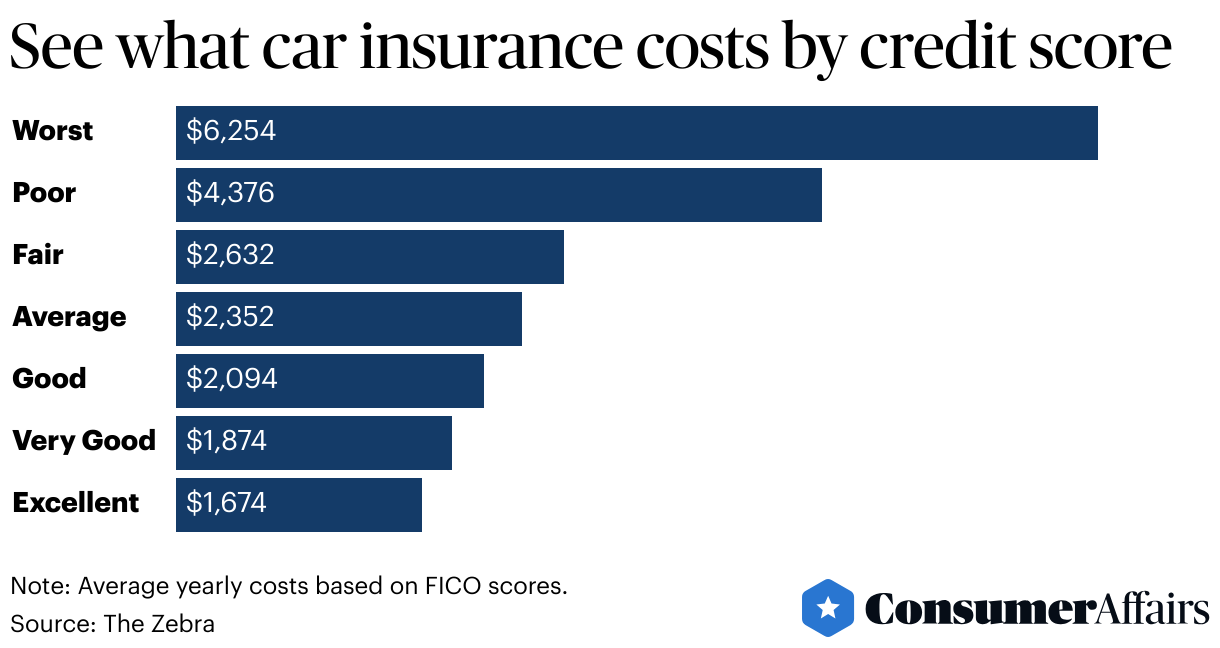

Drivers with a "very poor" credit score, or under 523 per FICO, pay an average of $6,254 a year for car insurance, compared with drivers with "exceptional" scores, or above 823, who pay $1,673.

Improving a credit score by just one tier can reap 54% in savings in car insurance on average, The Zebra said. Moving from the lowest tier to highest tier can deliver 273% in savings.

Car insurance rate increases based on bad credit vary by state, ranging from as little as a 74% increase in North Carolina to 285% in Minnesota.

Laws on credit scores and car insurance

Most states allow car insurance companies to consider credit, but four states have banned or significantly limited the use of credit scores: California, Hawaii, Massachusetts and Michigan.

For instance, The Zebra said without Michigan's law passed in 2020, drivers with "very poor" credit scores would be paying $8,640 on average instead of $3,096 today.

But drivers should check the laws since other states, such as Pennsylvania, North Carolina and Oregon, have some restrictions on using credit in determing car insurance rates.

There has been an effort at the national level to help drivers with poor credit get better car insurance rates.

Sen. Cory Booker (D-NJ) introduced a bill in 2020 that would ban credit as a car insurance rating factor, but the bill hasn't moved passed committee since 2023.