Payday lenders took in $2.4 billion in fees from cash-strapped consumers in a single year, a report from the Center for Responsible Lending (CRL) finds.

In brief ...

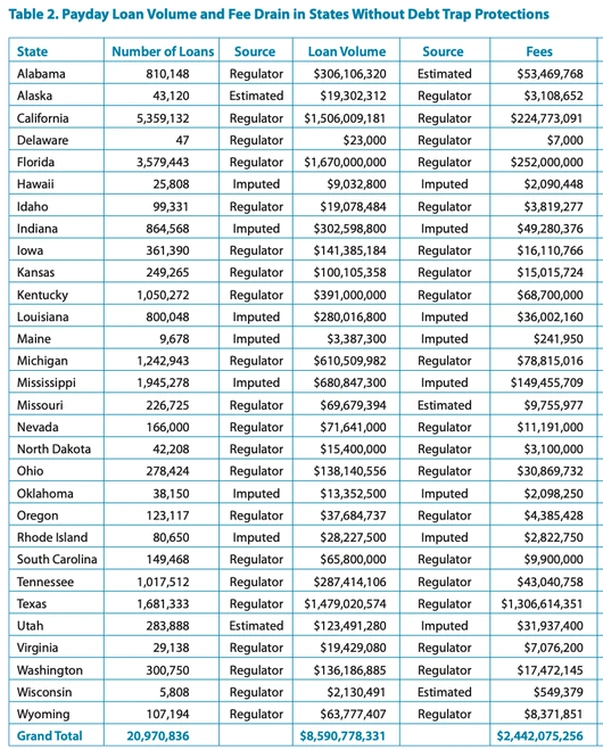

Texas the largest offender: Texas accounted for over $1.3 billion in payday loan fees, more than half of the national total.

Fee increases: From 2021 to 2022, payday loan fees increased significantly in several states, including:

- California: 20% increase

- Texas: 22% increase

- Florida: 17% increase

States with the highest payday loan fees: Texas, Florida, and California led the country in payday loan fees, with Mississippi and Michigan following, with Mississippi's fees being disproportionate to its population size.

Online payday lending growth: The share of online payday loans grew in Alaska (from 55% to 57%) and California (from 25% to 49%) between 2019 and 2022.

About the report

“Payday loans are designed to trap people in debt and this report shows the scale of the harm,” said report co-author Yasmin Farahi, CRL's deputy director of state policy and senior policy counsel.

“Predatory lending is a public policy choice. Twenty states and DC protect their residents from the payday loan debt trap with strong interest rate caps at no higher than 36% APR," he said. "Congress and policymakers in states without common-sense interest rate limits should enact these usury laws and the executive branch has a duty to enforce them – that is how to keep payday loan sharks at bay.”

Based on 2022 data, the report reveals that payday lenders collected $2.4 billion in fees from borrowers nationwide in that year alone. The state of Texas bore the brunt of these fees, accounting for over half of the total amount with $1.3 billion in payday loan fees.

Despite a slight decline in payday loan fee volume at the start of the COVID-19 pandemic, the report shows a $200 million rebound from 2021 to 2022. This increase reflects the growing financial strain on consumers, many of whom turn to payday loans to cover urgent expenses. Yet, these loans are designed to trap borrowers in cycles of debt, making it nearly impossible to escape without significant financial damage.

Most vulnerable states

The report breaks down payday lending fees by state, revealing that some states, like Texas, Florida, and California, are particularly vulnerable to payday lending practices.

In Florida, for instance, residents paid more than $252 million in payday loan fees, while in California, the amount was over $224 million. Mississippi, despite its smaller population, saw payday loan fees totaling more than $149 million. The report emphasizes that these high fees disproportionately affect low-income communities, many of whom can least afford them.

Online loans show strong growth

Online payday lending also saw significant growth in recent years, particularly in Alaska and California, the only two states that report statistics on online lending.

In Alaska, the share of online payday loans increased from 55% in 2019 to 57% in 2022. In California, the increase was even more dramatic, rising from 25% to 49% over the same period. This shift towards online payday loans raises concerns about the accessibility of these high-cost loans, especially for individuals in underserved or rural areas.

Stronger protections needed

The report calls advocates for stronger regulatory protections, including interest rate caps, to prevent payday loan providers from exploiting vulnerable consumers.

As the CRL report points out, 20 states and Washington, D.C. have taken steps to protect residents by capping payday loan interest rates at a more reasonable 36% APR. However, many other states remain without such protections, leaving their residents exposed to predatory lending practices. The report calls on lawmakers to take action and implement these protections to safeguard consumers from payday loan sharks.