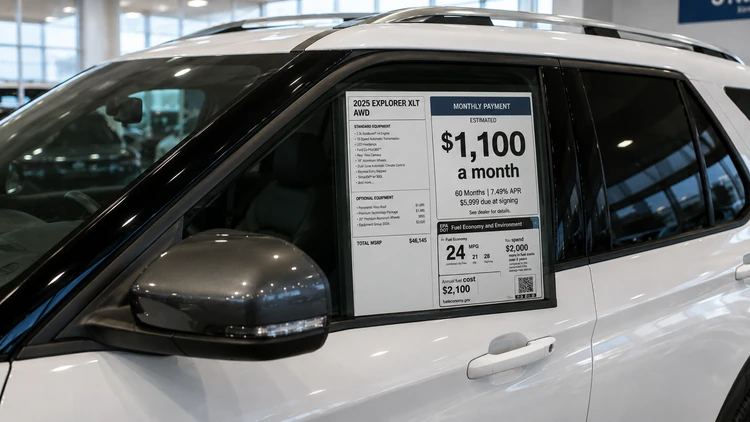

More Americans are taking on monthly vehicle payments of $1,000 or more, according to new Experian Automotive data.

Rising vehicle prices, elevated interest rates, and longer loan terms are pushing payments higher.

Analysts warn the trend could increase financial stress for consumers already dealing with inflation and higher borrowing costs.

A growing share of Americans are committing to monthly vehicle payments of $1,000 or more, demonstrating how higher vehicle prices and elevated interest rates continue to strain household budgets.

New data from Experian Automotive show the percentage of consumers with four-figure monthly car payments increased during the first quarter of 2026, reflecting ongoing affordability challenges in both the new and used vehicle markets.

Analysts say several factors are contributing to the trend, including persistently high vehicle transaction prices, higher financing costs, and consumers stretching loan terms to make payments more manageable.

Worsening affordability

“Vehicle affordability remains a significant concern for many buyers,” Experian Automotive said in its latest market analysis. “Even though some prices have moderated compared to pandemic-era peaks, higher interest rates continue to elevate monthly payments.”

The increase in $1,000-plus monthly payments comes as consumers face larger economic pressures, including higher costs for housing, insurance, and everyday necessities. Financial experts warn that large auto payments can leave households vulnerable if incomes decline or unexpected expenses arise.

According to Experian, buyers are increasingly financing larger amounts and choosing longer repayment periods. While extended loan terms can lower monthly payments somewhat, they often increase the total amount paid over the life of the loan and can leave borrowers owing more than the vehicle is worth for extended periods.

Record transaction prices

The trend is especially pronounced among new-vehicle buyers, where average transaction prices remain near record levels. Trucks, SUVs, and luxury vehicles continue to dominate sales, contributing to higher financing amounts.

Higher interest rates have compounded the problem. Borrowers with weaker credit profiles are facing especially steep financing costs, although even consumers with strong credit are paying significantly more than they did several years ago.

Industry analysts say some consumers are responding by delaying vehicle purchases, buying used vehicles instead of new ones, or holding onto existing vehicles longer.

Incentives are not helping that much

Automakers and dealers have increased incentives in some segments to stimulate sales, but affordability remains a central challenge for the industry.

Consumer advocates caution buyers to carefully evaluate how much vehicle they can realistically afford before signing long-term financing agreements.

Experian’s findings suggest the issue is unlikely to disappear quickly unless interest rates decline significantly or vehicle prices ease further.