Car insurance keeps reaching eye-wattering prices across the U.S., but some states have it worse.

The average annual cost of full-coverage car insurance is expected to hit $2,469 at the end of 2024, up from $2,019 in 2023, according to insurance comparison service Insurify.

That is a 22% spike in one year.

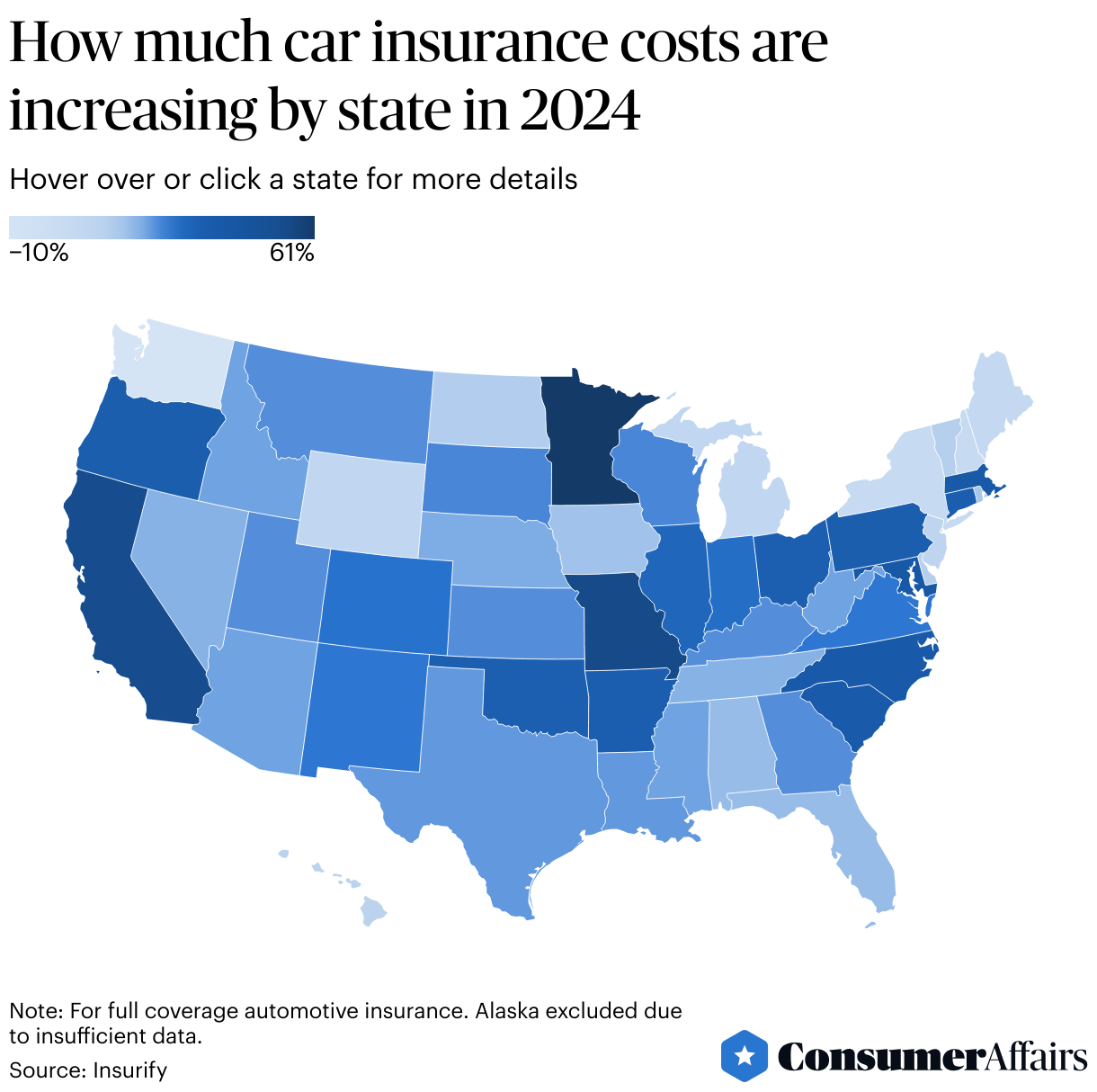

But 27 U.S. states are expected to see cost increases above the country's average, while 19 states are on track to see their costs grow below the average.

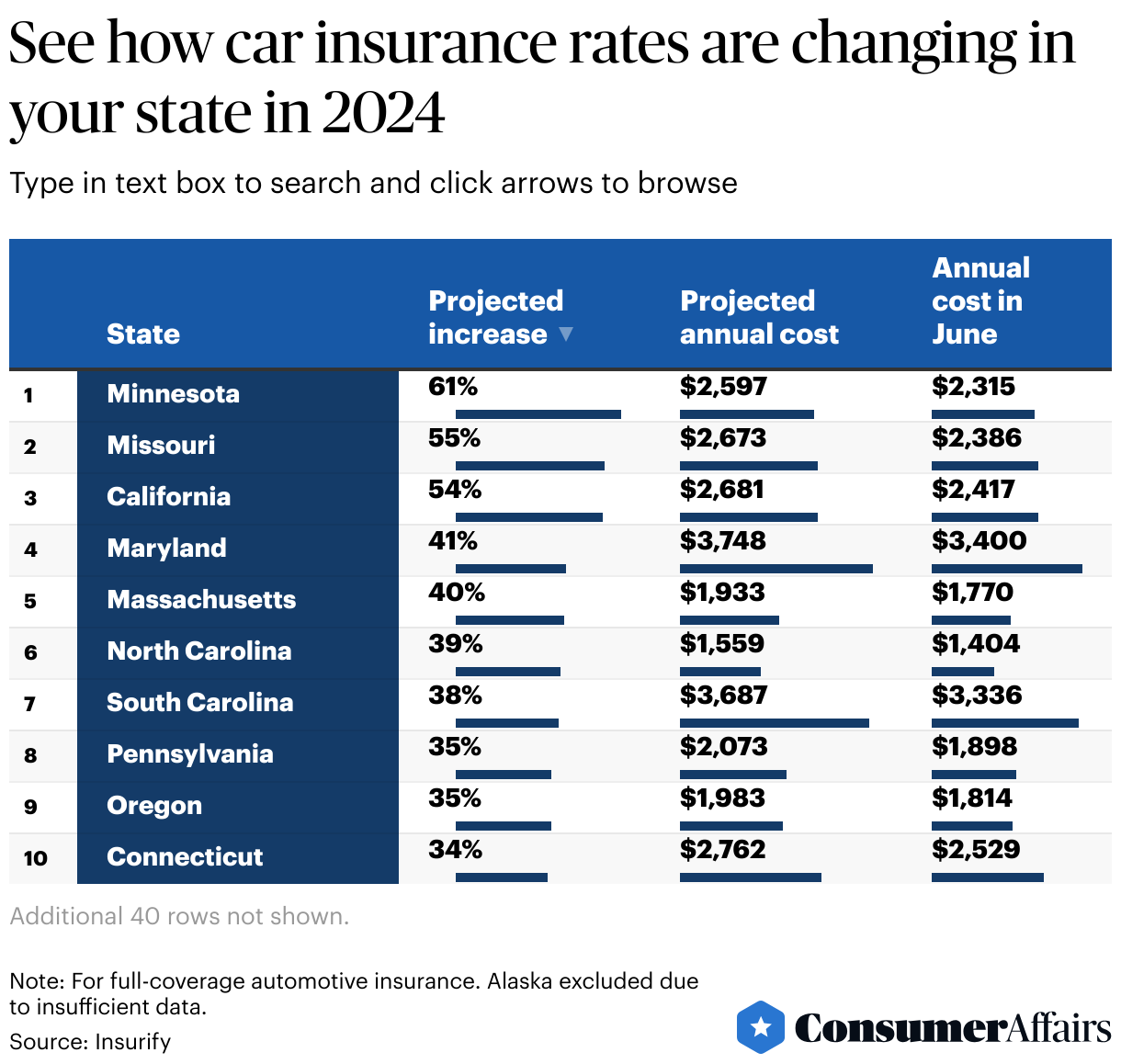

The five states with the highest projected increases are Minnesota (61%), Missouri (55%), California (54%), Maryland (41%) and Massachusetts (40%).

The five states with the lowest projections are Washington (-10%), New Hampshire (4%), New York (4%), Maine (6%) and Wyoming (8%).

The average cost for full-coverage car insurance varies wildly from state to state.

A variety of reasons cause car insurance prices to differ by state, including cost of living, crime rates, extreme weather and minimum insurance required by law.

The five states expected to have the highest annual full-coverage car insurance costs in 2024 are Maryland ($3,748), South Carolina ($3,687, New York ($3,484), Nevada ($3,531) and Florida ($3,444).

The five states projected to have the lowest costs are New Hampshire ($1,053), Maine ($1,263), North Carolina ($1,559), Vermont ($1,499) and North Dakota ($1,511).

What is making car insurance more expensive?

There isn't one reason car insurance is costing more, experts tell ConsumerAffairs.

A main reason automotive insurance prices have risen is because years of inflation have raised the costs of repairing and replacing cars.

Other reasons are higher levels of reckless driving since the pandemic and increasingly expensive technology in newer cars, such as sensors, cameras and driver assistance.

Still, there may be some hope on the horizon: Some insurers are now lowering rates after hiking them up to account for more frequent and severe losses due to bad driving behavior and inflation of vehicle maintenance and repair prices from the pandemic.

“Some insurers have started making downward adjustments in areas where they’ve found opportunities to operate profitably while charging lower rates,” said Mallory Mooney, director of sales and service and a licensed insurance agent at Insurify.

“Generally, consumers will continue to see rates rise with inflation, or in areas where traffic accidents are increasing, but in some states, they could see premiums decrease a little again," she added.

Tips to lower your car insurance

There are a quite a few ways to lower car insurance costs. Here's some advice experts have shared with ConsumerAffairs:

Shop around: If you have the time, spend up to a couple hours plugging in your information at various providers to make sure you get many quotes to compare. You can also use websites to quickly compare prices, such as The Zebra and Value Penguin.

Speak with insurance agents: An agent might know about current deals and smaller, cheaper companies that aren’t as well known.

Bundle insurance: You can get discounts for combining your auto insurance with other insurance like homeowners, renters and motorcycle insurance.

Improve your credit: Check for errors in your credit score and pay off debt.

Pay-as-you go: A lot of insurers will slash premiums based on how much you drive, which is especially helpful if you work from home.

Pay in full: Some insurers give discounts if you pay your premium in full, including in six-month installments, instead of monthly.

Telematics: If you are comfortable with your data getting collected, you can plug in a device in your car or download an app on your phone that watches your driving behavior and calculates your insurance premium, such as if you speed or you slam on the brakes a lot. Telematics can significantly lower costs if you are a good driver.

Bare-bones coverage: This makes more sense for older, less valuable cars. It is risky, but you can opt only for liability coverage if you damage another person’s vehicle, instead of additional coverage if you damage your car or it is stolen.

Miscellaneous discounts: Some insurers give discounts if teenagers have good grades, you are a member of the military, have an anti-theft device on your car or if you have a paperless insurance policy.