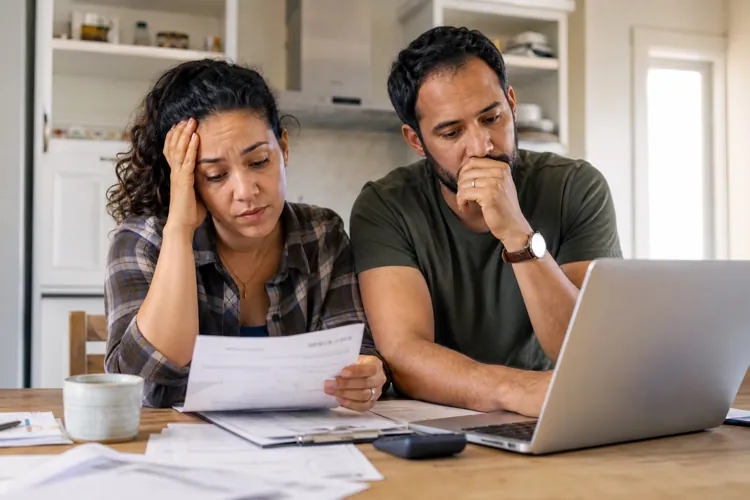

Many parents are taking on debt to keep their children from feeling left out, with social pressures and rising costs driving many spending decisions.

Financial experts say hiding debt can increase stress, strain relationships and make it harder to get back on track financially.

Open conversations about money, realistic budgeting and teaching kids healthy financial habits early can help families break the cycle of debt.

Parents want to give their children every opportunity they can, whether that means signing them up for sports, paying for school activities, or simply making sure they don't feel different from their friends.

But for many families, keeping up with those expectations comes at a financial cost that's largely hidden from view.

A new survey from MoneyLion found that 40% of parents have gone into debt so their children wouldn't feel left out, highlighting the growing financial pressure many families are facing. While parents often shoulder that burden quietly, the emotional impact can be significant, with many feeling guilt, shame and worry about how their debt could affect their children's future.

ConsumerAffairs interviewed Certified Financial Health Counselor Rudri Patel who explained why so many parents feel compelled to make these sacrifices and how families can navigate financial stress without carrying it alone.

Survey highlights

Over 1,000 U.S. parents were surveyed about their finances. The findings suggest that financial stress is affecting far more than household budgets — it's also shaping parents' decisions and emotional well-being.

Here are some of the key findings from the survey:

Four in 10 parents said they've gone into debt to make sure their children don't feel left out.

Among parents ages 25 to 34, that number rises to half.

More than half of respondents fear their debt could follow their children into adulthood.

Nearly four in 10 parents worry their financial situation could limit their children's future opportunities.

About 41% of Americans — and half of those currently carrying debt — said they've hidden how much they owe from someone close to them.

Nearly six in 10 respondents said they've borrowed money or relied on credit cards to pay for groceries and other household essentials

More than 40% reported delaying or skipping medication because of the cost.\

More than 80% of respondents said they believe it's acceptable for parents to take on debt for their children, suggesting that many parents may judge themselves more harshly than others do.

FOMO fuels decisions

According to Patel, the fear of missing out (FOMO) is one of the biggest drivers of financial decisions.

“With the influx of social media, parents and kids have multiple ways to compare themselves to orchestrated posts and highlight reels,” he said. “Parents feel the need to overspend on extracurricular activities, products, and vacations. This curated feed is financed through charging on high-interest credit cards and loans.

“In addition to the comparison culture, if parents are working full-time and feel that they aren’t spending enough time with their kids, they may overspend to make up for the guilt.”

The long-term risks of hidden debt

Hidden debt can also have physical and emotional weight for parents. Overspending is causing people to forego day-to-day expenses and health needs, which can carry long-term risks.

“Secrecy about finances is a risk that may be overlooked but may do long-term damage,” Patel said. “Over 40% of those surveyed have not told loved ones about what they owe and 35% don’t feel comfortable talking about money with close family members. Secrecy creates anxiety and delays which could lead to compounding financial problems. It makes it harder to stop poor finance behavior because there is little to no accountability involved.

“Hidden debt can delay life milestones. Over 30% of Americans have put off getting married because of debt, and nearly 35% have delayed having children. The longer debt is not talked about, the more it can impede a family’s entire life trajectory.”

Budgeting strategies

For parents who want to take control of their finances and budget accordingly, Patel shared his best tips based on his experience as a financial expert:

Start small. You likely won’t fix everything at once. One quick way to get a jump start is to call your credit card issuers and find out if they will lower interest rates. If you’re a long-time customer and have been consistent about making timely payments, chances are the issuer will lower your interest rates.

Create an emergency fund. Having $500 to $1,000 in an emergency fund can make a difference. You’ll want to prevent an unexpected expense from derailing your entire budget. Instead of charging on a high-interest credit card or getting a personal loan, you can withdraw from your emergency fund.

Be honest about your debt. Although these conversations may feel uncomfortable, you’ll need to have conversations with loved ones regarding your debt. Start by having monthly check-ins. Transparency is the key to reducing shame regarding debt.

Limit social media usage. If you’ve recognized that comparison tends to fuel unnecessary spending, limit your social media usage. Minimizing triggers that lead to comparison can help with having a grounded approach to spending.

Track your spending. Be ruthless with your budget. This means keeping track of every small or large expense.

Talk to your kids about money

The survey found that more than 50% of parents are worried about how their debt will impact their children as they grow into adulthood. But it doesn’t have to!

Patel recommends that parents start talking to their kids about money early, as it can help them be more aware of finances from a young age.

“Between ages 3 to 5, introduce the concept of money and let them choose one thing to buy at the store,” Patel said. “By ages 6 to 8, it’s a good idea to teach children about an allowance and let them decide how they want to spend, save, and donate.

“As children get older and hit their early teens, give them a debit card so they can understand the concept of credit, debt, and interest. Introduce them to budgeting apps so they understand the different categories that will likely be relevant as they get older. As they hit their late teens, getting a checking account, credit card, and a part-time job can teach them practical basics about money. You can start by having conversations about personal loans and cars, how to pay for college, and taxes.”