If you’re a Fingerhut shopper looking for ways to reduce your personal debt, bulk up your savings account or otherwise improve your financial bottom line, the single best thing you can do is stop buying things from Fingerhut (or any so-called “credit shopping” retailer).

Fingerhut is a mail-order company whose tagline is “Now You Can!” The bar across the top of its website’s front page boasts of offering “Buy Now Pay Later Credit Shopping.”

The problem with such credit shopping is that when you pay later, you also pay more. Lots more. Fingerhut’s business model is similar to that of so-called “rent-to-own” or “lease-to-buy” stores, offering instant gratification in exchange for enormous price markups.

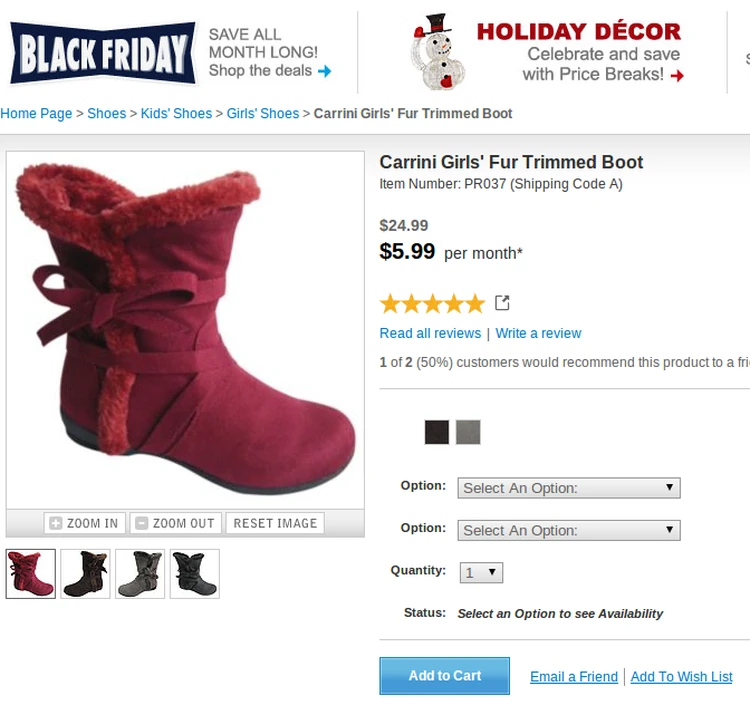

For example (all quoted prices here are as of Nov. 14), when we clicked on Fingerhut’s “Kid’s Shoes” category, the first offering listed was a “Carrini Girls Fur Trimmed Boot” [sic] priced at $24.99, or $5.99 per month.

Clicking on the image brings you to the order page for that pair of boots. Scroll down near the bottom, and there’s another link reading “See Full Cost of Ownership.” That link takes you away from the Fingerhut.com address into some Adobe Scene 7 software (impossible to see unless your computer allows Java). You end up with a 121-page chart listing the initial costs of Fingerhut purchases, the monthly payments and the ultimate cost of repayment.

Depending on your computer monitor’s resolution the screenshot we took might be difficult for you to read, since Scene 7 has extremely limited zoom-in capacity. However, if you check page 12-13 you’ll notice that a $24.99 Fingerhut item with monthly payments of $5.99 will cost $26.41 if you make five monthly payments, or $37.67 over seven months.

Depending on your computer monitor’s resolution the screenshot we took might be difficult for you to read, since Scene 7 has extremely limited zoom-in capacity. However, if you check page 12-13 you’ll notice that a $24.99 Fingerhut item with monthly payments of $5.99 will cost $26.41 if you make five monthly payments, or $37.67 over seven months.

Of course, higher-priced items have correspondingly higher markups: a $50 item costs $74.20 after eleven payments of $6.99. Buying $88.95 worth of stuff at $13.99 per month can cost you up to $204.62 by the time it’s paid off.

But what if you really want those $89 worth of Fingerhut products, only you can’t afford them right now? The harsh truth is: if you can’t afford to pay $89 up front for something, you definitely can’t afford to pay $205 for the same thing. And if your finances are tight enough that it’s hard to scrape together $25 for a kid’s pair of boots, paying $38 for the boots plus finance charges will only make matters worse.

Samuel Vimes

Coincidentally, boots are at the center of one of the most famous contemporary economic paradoxes: the Samuel Vimes ‘Boots’ Theory of Economic Unfairness. Vimes is a fictional character, a policeman in the Discworld series of books by comic-fantasy author Terry Pratchett.

“The reason that the rich were so rich, Vimes reasoned, was because they managed to spend less money.

Take boots, for example. He earned thirty-eight dollars a month plus allowances. A really good pair of leather boots cost fifty dollars. But an affordable pair of boots, which were sort of OK for a season or two and then leaked like hell when the cardboard gave out, cost about ten dollars. Those were the kind of boots Vimes always bought, and wore until the soles were so thin that he could tell where he was in Ankh-Morpork on a foggy night by the feel of the cobbles.

But the thing was that good boots lasted for years and years. A man who could afford fifty dollars had a pair of boots that'd still be keeping his feet dry in ten years' time, while the poor man who could only afford cheap boots would have spent a hundred dollars on boots in the same time and would still have wet feet.

This was the Captain Samuel Vimes 'Boots' theory of socioeconomic unfairness.”

Granted, Vimes’ particular problem — keeping his feet shod in shoddy boots — probably doesn’t apply to Fingerhut shoppers; though we haven’t tested this ourselves, we’re sure that Carrini boots or Reebok sneakers bought from Fingerhut are just as good as Carrini or Reebok items bought elsewhere.

But the point of his paradox still applies: paying little bits of money in regular increments can ultimately be far more expensive than paying a larger sum of money all at once. Paying $20 a week for a big-screen rent-to-own TV is ultimately two to three times as costly as saving $20 a week until you can buy that TV for cash, and the “buy now pay later” price for household goods bought on credit is almost guaranteed to be higher than the “buy now pay now” price for those same items.