Balloon mortgages are short-term loans that begin with a series of fixed payments and end with a final, lump-sum payment.

Jump to insightSome borrowers may struggle to make the balloon payment, leading to potential foreclosure or the need to refinance.

Jump to insightBalloon mortgages aren't structured to be paid off through normal monthly payments alone, making them different from traditional fixed mortgages.

Jump to insightHow does a balloon mortgage work?

A balloon mortgage is a type of home loan where you make regular, often lower, monthly payments for a set period — typically five to seven years. After this term ends, your remaining loan balance is all due at once. This is the “balloon” payment.

If you can't afford to pay off the rest of the loan, you will need to rely on refinancing, selling or modifying your loan. In the worst-case scenario, a lender will foreclose your home if the other options do not work out.

While balloon mortgages can be risky, the initial period of lower payments can be appealing for buyers expecting a significant increase in income or planning to sell or refinance the home before the balloon payment is due.

Balloon mortgage rates

Balloon mortgage rates can vary depending on several factors, including the mortgage lender, the borrower's creditworthiness and market conditions. At the time of publishing, Fannie Mae balloon mortgage rates range from 6.49% to 7.81%.

Kristen Conti, broker-owner of Peacock Premier Properties, a real estate company, discusses ARM loans with balloon payoffs with her clients when interest rates are high.

“The way this works is that they can begin their mortgage journey at a lower rate,” she said. “Sometimes this can be as much as 1% to 2% lower than a 30-year fixed.”

The way this works is that they can begin their mortgage journey at a lower rate. Sometimes this can be as much as 1% to 2% lower than a 30-year fixed. ”

Types of balloon mortgages

While all balloon mortgages are similar, there are some variations. There are three main types of balloon mortgages, and the type you choose affects how large your monthly mortgage payment is.

Interest and principal payments

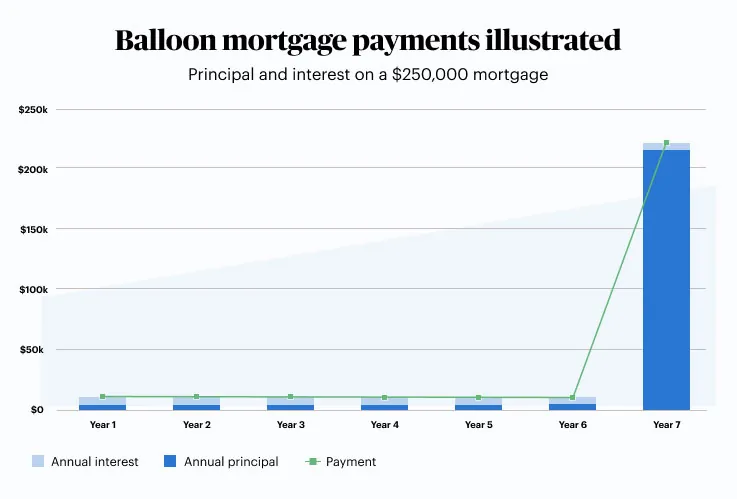

Your payments may be put toward a combination of interest and principal if you decide to obtain a balloon mortgage. Say you take out a $250,000 loan at 3% for seven years. Your loan may still be amortized like a 30-year loan, but the remaining balance is due at the end of seven years. With a traditional loan, the sum of all of your payments over 30 years would pay off your entire balance.

In this scenario, your monthly payment would be $1,054.01, which includes principal plus interest. On a standard amortization schedule, each payment will have you paying off slightly more principal as you approach the end of the term.

For example, with your first monthly payment, $429.01 is put toward principal, and $625 is put toward interest. The final monthly payment at the end of seven years would include $526.49 for principal and $527.52 for interest. The lump sum due at the end is $211,009.36.

Interest-only payments

With an interest-only mortgage, your monthly payments won’t be allocated to the principal — instead, they’ll just cover the monthly interest. At the end of the loan term, the entire principal will be due in one lump-sum payment.

In the scenario above, your monthly payment would be $625 and remain fixed during the loan term. At the end of your loan term, you would owe $250,000.

No monthly payments

With a zero-coupon balloon mortgage, you would make no monthly payments at all, but would instead pay one large lump sum (the full principal plus all accumulated interest) at the end of the loan term.

This type of mortgage is not typically available for the everyday homebuyer, but it is instead used by commercial borrowers with clean records.

Pros and cons of a balloon mortgage

For some buyers, balloon mortgages can help them secure a home loan at a lower interest rate. But it is a gamble that you’ll be able to repay or refinance the loan by the end of the term.

Here are some other pros and cons of balloon mortgages to consider.

Pros

- Lower initial payments

- Lower interest rates

- Short-term benefits if you don’t plan on living in the home long

Cons

- Large balloon payment due at the end of the loan term

- Slow equity building

- Risk that you won’t be able to refinance, meaning you could get stuck with a higher rate

Paying off a balloon mortgage

Even if you have several years before your balloon payment, it is still essential to have a plan. This is where the risk factor comes in; you don’t know what the future of your finances or the real estate market will look like.

These are your best options for paying off your balloon mortgage:

- Refinance: “If interest rates go down, they may have the option to refinance during the initial time period,” said Conti. “The decision on whether or not to refinance can be made 90 days prior to the maturity of the adjustable period.” Refinancing involves taking out a new loan, either with your original lender or a new one. You will need to meet your lender’s eligibility criteria and pay closing costs.

- Sell your home: Selling is always an option, especially if you don’t love the home or neighborhood. This move is best suited for those who will earn enough proceeds from the sale to cover the balloon payment due.

- Pay it off in full: If you can set aside the right amount of money each month, your balloon mortgage could end with a fully paid-off home.

- Reset option: Check with your lender if your balloon mortgage comes with a reset option. This will allow you to reset the terms and rate of your loan without having to refinance.

What if you can’t pay the balloon payment?

If you find yourself unable to make the balloon payment when it comes due, it’s important to act quickly. Contact your lender as soon as possible to discuss your options. Depending on your situation and the lender’s policies, you might be able to negotiate a loan modification, apply for an extension or transition into a different loan product. Ignoring the payment could lead to default and foreclosure.

If you can't negotiate new terms, you may be forced to sell the home under pressure, which could limit your sale price. In some cases, a deed in lieu of foreclosure or a short sale may be considered to avoid full foreclosure proceedings. Consulting with a housing counselor or financial advisor can help you understand your rights and possible alternatives.

Should you get a balloon mortgage?

Balloon mortgages are not right for everyone. Not many lenders even offer them due to their risky nature.

Janis, a reviewer from Ohio, got stuck in a tricky situation due to a balloon mortgage. “I cannot refinance because it is a mobile home. I have asked other lenders to finance and they will not finance what is owed because it does not appraise for the amount we need,” she said.

You should consider balloon mortgages only if you are able to repay the loan in full or can make increased payments on your loan — for example, if you are expecting a large income increase. A balloon mortgage might also be right for you if you don’t plan on staying in your home for long, such as if you are planning to flip the home for profit.

In any case, you should keep your credit score high just in case you need to refinance your balloon mortgage before the lump sum payment is due.

» LEARN MORE: What is owner financing and how does it work?

FAQ

How is a balloon mortgage different from a regular mortgage?

A balloon mortgage differs from a regular mortgage primarily in its repayment structure. With a traditional mortgage, you make regular payments of both principal and interest over a set term, typically 15 or 30 years, by the end of which the loan is fully paid off.

In contrast, a balloon mortgage has lower regular payments that cover only the interest and a small part of the principal for a shorter term. Then, you can expect the full amount to be due at the end of the term.

Are balloon mortgages legal?

Yes, balloon mortgages are legal, but you will notice that they are less common today because of regulations that require lenders to ensure borrowers have the ability to repay their loans. These regulations were put in place after the 2008 financial crisis to protect consumers from risky lending practices.

Why are balloon mortgages risky?

Balloon mortgages are risky for several reasons, mostly because such a large amount of money will be due at the end of the term. This forces buyers to be dependent on future financing options and can even leave homeowners upside-down on their mortgage.

Is a balloon mortgage better for investment properties?

Balloon mortgages can be useful for investment properties if the investor plans to sell the property before the balloon payment is due. The lower initial monthly payments may help with cash flow in the short term. Still, this approach carries risk if market conditions change or the property doesn't sell as planned.

Do balloon mortgages affect your credit score?

A balloon mortgage affects your credit score in the same way as other loans. Making on-time payments can help improve your score, while missed or late payments — especially on the balloon payment — can cause significant damage. Foreclosure due to a missed balloon payment will severely hurt your credit and remain on your report for up to seven years.

Bottom line

Balloon mortgages are risky. If you are the right type of buyer (someone who wants to avoid high interest rates without putting off buying a home), then this type of mortgage can be your creative solution to do so. You will just need to plan ahead and decide how you will repay the balloon payment without derailing your finances.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Consumer Financial Protection Bureau, “What is a balloon payment? When is one allowed?” Accessed July 31, 2025.