Understanding amortization can help you see how much of your monthly payment goes to principal versus interest over time. Initially, more of your monthly mortgage payment will go toward interest. Over time, as you make monthly payments, less of your payment will go toward interest and more will go toward reducing your balance. Learn more about amortization and how it works below.

Mortgage amortization is the gradual repayment of a home loan through set monthly payments of principal and interest.

Jump to insightBorrowers will steadily build equity in their home with each monthly payment.

Jump to insightAn amortization schedule breaks down how you’ll replay your loan over time.

Jump to insightAmortization, defined

Amortization is when you reduce your mortgage debt over time through set payments of principal and interest.

“Amortization refers to the gradual process of paying off your mortgage debt over time through regular monthly payments,” said Alex Shekhtman, CEO and founder of LBC Mortgage. “These payments are thoughtfully structured to cover both the interest and a portion of the principal amount.”

When you first start repaying your mortgage, you will pay more toward interest than principal. Additional principal payments can accelerate the mortgage payoff process, saving you on interest costs and shortening the loan term.

“In the early stages of your mortgage term, a larger proportion of your monthly payment is allocated toward interest, while a smaller fraction contributes to reducing the principal,” Shekhtman said. “As you consistently make payments over the years, the balance shifts, and more of each payment is directed toward reducing the principal.”

How amortization works

Understanding how amortization works can help buyers better understand their mortgage payments.

“For buyers, comprehending amortization helps in grasping how their monthly payments are distributed and how their equity in the property grows with time,” Shekhtman said. “It also presents an opportunity for loan acceleration and reduction of overall interest paid through making extra payments.”

Builds home equity

Mortgage amortization allows a borrower to build home equity with each monthly payment they make, Shekhtman said. As the principal is paid down, the homeowner increases their equity, or ownership, in the property. Equity can be useful if the homeowner chooses to sell or refinance the property.

Less goes toward principal initially

With amortization, you aren’t paying off much of the principal in the beginning. Interest is calculated from the remaining balance, so your interest costs are pretty high until you start to make a dent in the principal. The longer the loan term, the greater your interest costs will be.

“As you consistently make payments over the years, the balance shifts, and more of each payment is directed toward reducing the principal.”

Potential for changing payments

Some mortgage types, such as balloon mortgages, are not fully amortized and may have low monthly payment amounts until a large lump-sum payment is due. This means facing a significant payment at the end of the loan term and a potential foreclosure if you haven’t saved up enough money to cover that huge payment.

» MORE: How does a mortgage work?

What is an amortization schedule?

An amortization schedule is a table that outlines the repayment of a loan over time. It breaks down each periodic payment into two components: the principal and the interest.

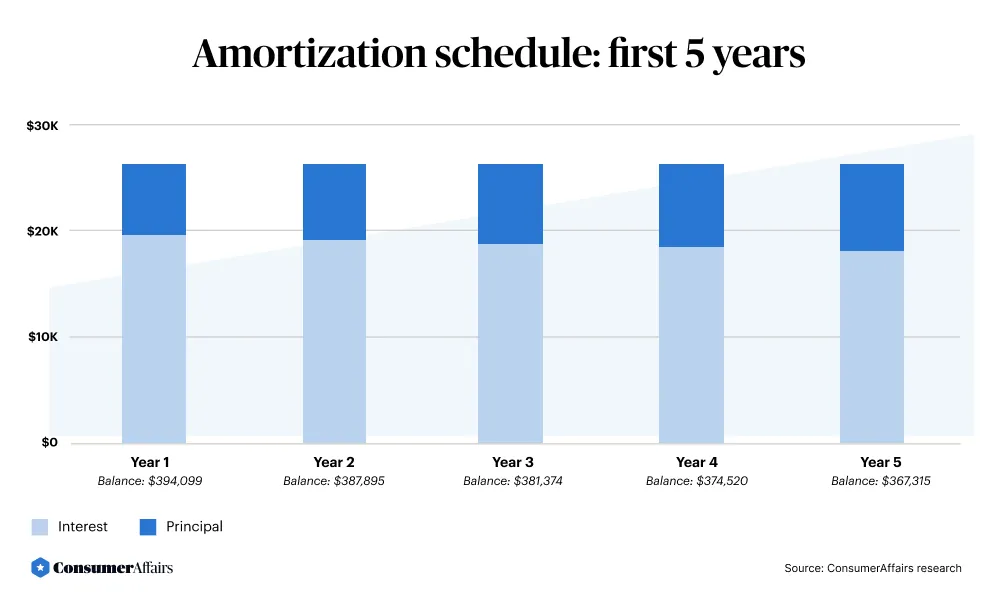

Below, we’ll take a look at an example amortization schedule for a mortgage of $400,000 with a fixed interest rate of 5% and a 30-year term.

Amortization schedule: first 5 years

The buyer can expect to pay more money toward interest in the first five years.

In the first year, you’ll pay $19,865.98 in interest. From the first year through year five, you’ll pay a total of $96,152.12 in interest.

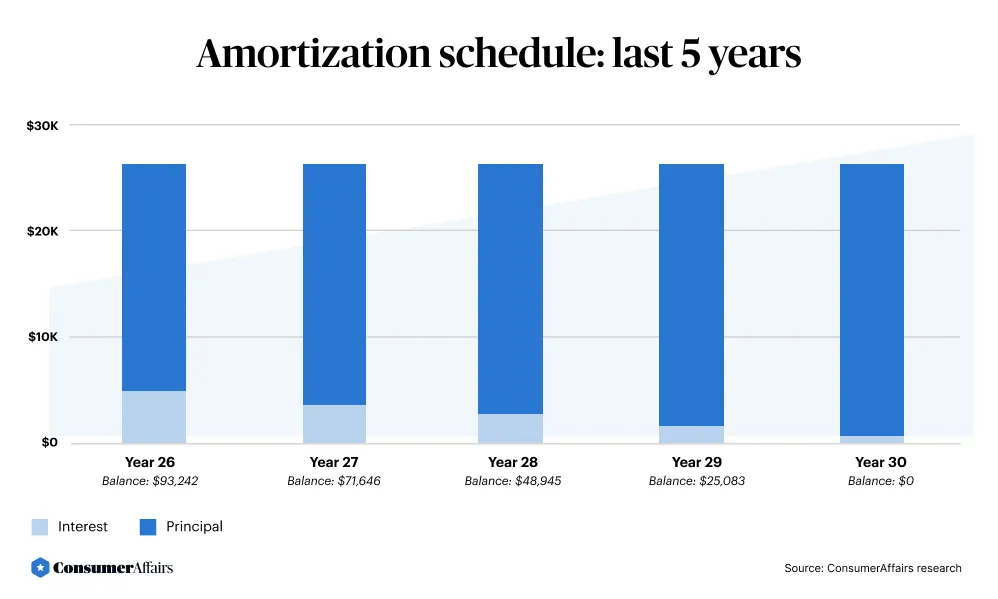

Amortization schedule: last 5 years

Here’s what the last five years of the amortization schedule would look like:

When you make the final payment at the end of 30 years, your loan will be completely paid off. You’ll have paid a total of $373,023.14 in interest over the life of the loan. This is in addition to the $400,000 paid toward the principal, bringing the total amount paid to $773,023.14 over 30 years.

» MORE: How much house can I afford?

Amortization vs. depreciation

Amortization is similar to depreciation in that both concepts reflect a gradual reduction in the value of specific items. But the two terms have slightly different meanings. Amortization refers to how the value of an intangible item, like a mortgage, decreases over time.

In comparison, depreciation refers to how a tangible asset, like a car, loses its value over time. If you bought a car a few years ago, it’s likely not worth as much now as it was when you first purchased it. Similarly, businesses can depreciate their assets and assign expenses to these devaluations each year.

FAQ

How can you calculate amortization?

The general formula for calculating how much of your monthly payment goes toward principal and how much goes toward interest is: Monthly payment - interest due for the period = principal payment.

Can I change my mortgage’s amortization schedule?

In some cases, borrowers can modify their amortization schedules through refinancing. Refinancing allows a borrower to adjust their loan’s term, interest rate or payment structure to better suit their financial goals or current circumstances.

How do additional principal payments affect the amortization process?

Making additional principal payments can significantly impact the amortization process, but it is important to let your mortgage lender know that the extra payments are going to the principal only. Extra payments reduce the outstanding principal balance, leading to lower overall interest costs and shortening the loan term.

What is negative amortization, and should I be concerned about it?

Negative amortization occurs when a borrower’s mortgage payment is not sufficient to cover the interest due. As a result, the unpaid interest is added to the loan's principal balance. Negative amortization can be a concern with payment-option adjustable-rate mortgages (ARMs), but it won’t affect most homebuyers with standard mortgages.

Bottom line

An amortization schedule provides a roadmap for a borrower, letting them know how much of their monthly payment will go toward principal and interest. Understanding how significant a role amortization plays in your loan can help you decide between a fully amortized mortgage with stable payments and an alternative mortgage type, like a balloon mortgage. It can also motivate you to pay off your mortgage early.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Consumer Financial Protection Bureau, “What Is Negative Amortization?” Accessed Dec. 6, 2025.