Simpler retirement account statements increased savings when firms had strong returns

But for poorly performing firms, simplification actually reduced contributions

Findings challenge assumptions of policy experts and have major implications for global savings policy

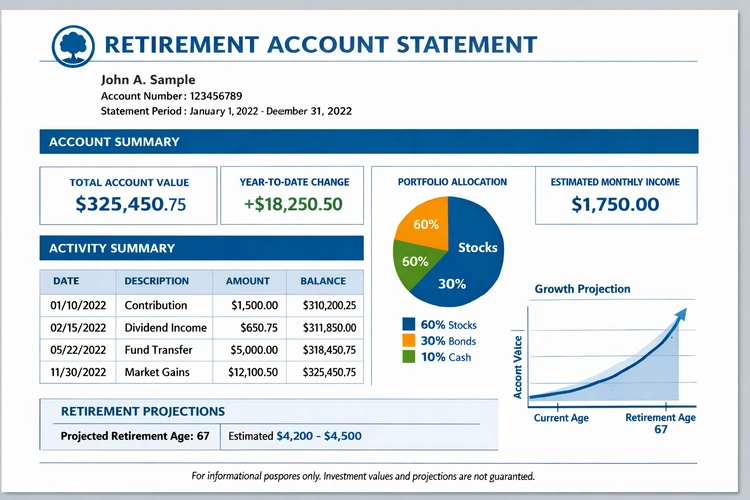

A new academic study reveals that simplifying retirement account statements can encourage people to save more—but only if they’re invested with a well-performing firm. When consumers saw clearer, easier-to-read statements from firms with poor returns, they actually contributed less.

The research, based on two large-scale field experiments involving more than 127,000 customers in Mexico, challenges the widely held belief that simpler communication always leads to better financial outcomes.

While simplification made key information easier to understand and remember, it also amplified consumers’ focus on whether their retirement provider was performing well—leading many to reduce contributions if the firm was ranked low.

The study was recently publishes in the Journal of Consumer Research.

A surprising backfire for low-ranked firms

The study, conducted in partnership with two Mexican retirement firms, found that simplified statements led to increased voluntary savings among customers of the higher-ranked firm, but reduced savings among customers of the lower-ranked one.

This result caught both researchers and policy experts off guard. In surveys before the experiment, none of the 74 policymakers and marketing experts polled predicted that simplification could lead to a negative effect. Over 70% assumed that simpler statements would boost savings across the board.

Even a follow-up survey of 200 everyday Mexican citizens showed most people believed simplified forms would improve savings—regardless of firm performance.

Why simplification had mixed results

The researchers suggest the key lies in a concept called processing fluency—how easily people can absorb information. When people better understand their account statements, they’re more likely to act on what they learn.

That can be good news if the information is positive—such as a high-performing fund—but bad news if it highlights poor returns. In those cases, the study suggests, simplification may unintentionally discourage people from saving altogether.

Laboratory experiments confirmed that people who saw simplified statements remembered their firm’s rank more accurately—and that this clarity amplified their response, either positively or negatively.

A path forward: Help people switch

To counter the negative effects for customers in poorly performing funds, the researchers tested a new approach: simplifying the process for switching to a better provider. When customers received clearer instructions on how to switch firms, those with low-ranked providers were significantly more likely to move their savings.

This finding points to an important policy opportunity. By not only simplifying statements but also making switching options more transparent and accessible, policymakers could help boost retirement savings even for those in underperforming funds.

Implications for global retirement policy

With millions worldwide facing retirement savings gaps, governments and financial institutions have increasingly embraced "nudge" strategies to encourage better financial behavior. Simplifying forms has become the most common intervention used in nearly 36% of policy experiments worldwide, according to a recent meta-analysis.

But this new research suggests that simplification alone isn’t a silver bullet. Instead, it must be paired with strategies that help people act on the information they understand—especially when that information reveals problems with their current financial provider.

The study adds to a growing body of behavioral economics research that urges policymakers to look beyond good intentions and understand how real people react to clearer information.

As the researchers conclude, “Improving the ease of processing information can change behavior—but whether that change is helpful or harmful depends on the message the information is sending."