Mortgages are secured loans that let you buy a home and pay it off over time.

Jump to insightMost mortgage payments include principal, interest, taxes and insurance.

Jump to insightThe mortgage process moves from preapproval to closing with several required steps in between.

Jump to insightAmortization shifts your payments from mostly interest to mostly principal over time.

Jump to insightWhat is a mortgage?

A mortgage is a type of loan that’s used to buy real estate, residential or commercial. In a mortgage, the property itself serves as collateral for the loan. That means if you don’t pay your mortgage, the property can be taken away from you by the issuing bank.

Most mortgages extend many years or even decades, with the two most common mortgage loans lasting 15 and 30 years. Since a mortgage loan is tied to a tangible asset — the home itself — it’s considered a secured loan, which means there’s less risk to the bank that issues the mortgage.

This means you can expect to find lower interest rates than you would for credit cards or personal loans. This is an important point, since a mortgage is likely the largest loan you’ll ever hold.

Types of mortgages

There are several major types of mortgages, each tailored to different borrower needs and situations, Marc Halpern, CEO of Foundation Mortgage, a lender in Florida, told us. Here are some common mortgage types:

- Federal Housing Administration (FHA): Lower down payments and more flexible qualification requirements

- Adjustable-rate: A low interest rate to start that adjusts over time based on market fluctuations

- VA: Easier to obtain and less stringent down payment requirements for those who have served in the armed forces

- U.S. Department of Agriculture (USDA): For low-to-moderate-income buyers in rural areas

- Nonqualified mortgages (non-QM): For buyers with low credit scores or financial challenges that prohibit them from qualifying for a traditional mortgage loan

- Interest only: Low monthly payments that only go toward interest for a fixed amount of time, followed by payments based on market conditions

Mechanics of a mortgage

A mortgage works by letting you buy a home without paying the full price upfront. The lender gives you funds to purchase the property, and you repay the loan over time through monthly payments. The home serves as collateral, meaning the lender can take it if you fail to pay.

How amortization works

Amortization is the gradual payoff of a loan over time. In the early years, most of your mortgage payment goes toward interest, with only a small portion reducing the principal, Halpern said. Over time, this flips as more of your payment goes toward the loan balance. As you keep paying, your ownership stake in the home (equity) grows.

“The flip we mentioned above, where your payments gradually move from mostly interest to mostly principal, is called amortization. Most mortgages are fully amortizing, meaning the loan will be paid off in full by the end of the term, assuming on-time payments,” Halpern said.

Before you sign your mortgage agreement, your bank or lender will provide you with an amortization schedule that details your payments, along with other crucial aspects of your loan, such as total cost including interest, repayment period, any penalties for early payment and other information.

Parties involved in a mortgage

It’s accurate to say that a mortgage is a business transaction between you and your bank or lender. But there are other parties that may be present during the process as well, and it’s a good idea to understand their roles in case you need assistance with your mortgage.

Here’s a breakdown of the key parties involved in the mortgage process:

- Borrower: When you apply for a mortgage through any institution, you’re known as the borrower.

- Lender: This is the bank or lending company that originates your mortgage.

- Legal advisor: Many large transactions, such as mortgages, will have a legal advisor on hand to assist with any questions that may arise.

- Real estate agent: You’ll likely work with a real estate agent to find the home or property you want to buy. This person also helps review paperwork for accuracy during the mortgage process.

- Escrow agent: This person sets up and manages the escrow account, which holds money for taxes and insurance until bills are due.

- Home appraiser: The home appraiser is responsible for inspecting the home or property you’re purchasing and determining the fair market value of the home based on its condition.

» FIND OUT: Finding a real estate agent

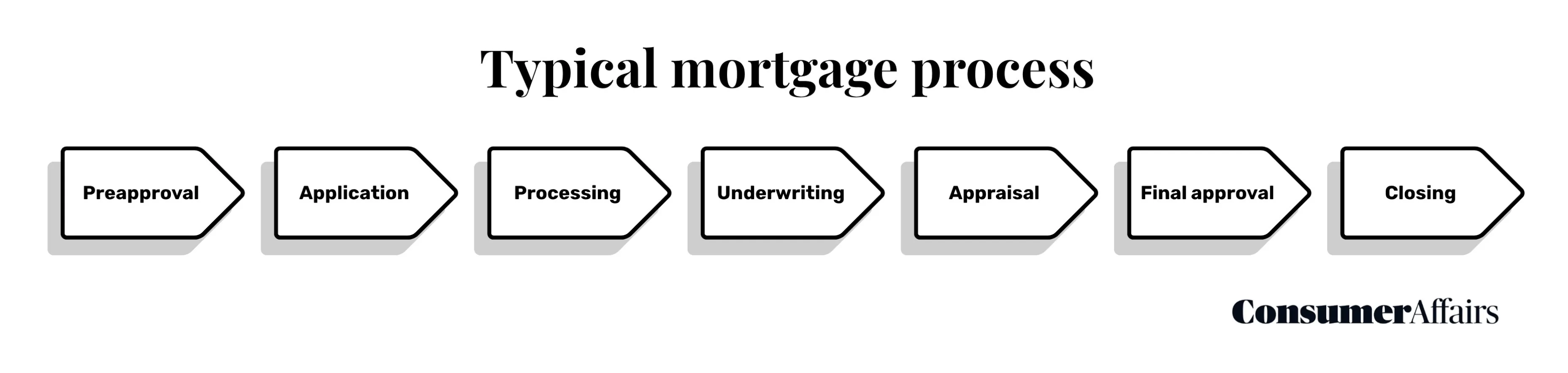

The mortgage process

Securing a mortgage typically follows these steps:

Preapproval gives you a sense of your buying power, Halpern told us. Once you apply for a mortgage, the lender reviews your income, assets, credit and debts. During underwriting, the company assesses the risks and ensures the loan meets guidelines. A home appraisal is then ordered to confirm the property’s value.

Once everything checks out, you’ll receive a closing disclosure and then sign final documents on closing day. “With Non-QM loans, the process is similar, though documentation requirements are more flexible — such as using bank statements, profit and loss statements, or asset verification instead of traditional W-2s,” Halpern said.

What’s in a mortgage payment?

Your mortgage payment is likely the biggest bill you’ll pay each month. It covers more than just the cost of your house. Most monthly mortgage payments include four key parts, known by the acronym PITI: principal, interest, taxes and insurance.

- Principal and interest: These are the two main components of any mortgage payment. Principal pays down your loan balance over time, while interest is the cost of borrowing money.

In the early years of a mortgage, you’ll pay mostly interest, then shift toward more principal as the loan matures. Some loans, like interest-only mortgages, delay principal payments for a set period.

- Taxes and insurance: Property taxes and homeowners insurance are often collected each month and managed through an escrow account.

- Escrow: An escrow account is a separate account your lender manages to hold money for taxes and insurance. “Instead of paying these large bills directly, your lender divides them into monthly installments and pays them on your behalf. This simplifies budgeting and ensures critical payments are made on time,” Halpern said.

- Mortgage insurance: Mortgage insurance helps protect the lender if you can’t make payments. Private mortgage insurance (PMI) applies to conventional loans with less than 20% down. “PMI can often be canceled once you reach 20% equity,” Halpern said. FHA loans use a mortgage insurance premium (MIP) with upfront and monthly fees, which can last for the life of the loan unless you refinance.

Understand your mortgage payment

Your mortgage payment follows the PITI formula:

Principal

Interest

Taxes

Insurance

FAQ

How much is a $200,000 mortgage payment for 30 years?

It depends entirely on the interest rate you qualify for and the down payment you’re able to make. Without factoring any down payment into the equation, a mortgage payment like this at 5% interest would result in a payment of about $1,272. However, with a 2% interest rate, the payment would be much less, at $937.

How does a mortgage payment work?

A mortgage payment is a once-per-month payment you make toward the loan balance on your home. While large, the monthly mortgage payment includes the loan principal amount, a certain amount of interest (based on the rate and the amortization schedule), taxes, escrow and insurance.

You’ll receive paperwork before closing that will give you a detailed breakdown of your monthly mortgage payment.

What are the two types of mortgage loans?

The two most common types of mortgage loans are conventional and government-backed. Conventional loans are those not backed by the government. They come in various forms, like fixed-rate, adjustable-rate and interest-only. Government-backed loans include those issued by the VA and USDA.

How to get a mortgage

For most people, getting a mortgage is a long-term goal — something they’ve thought about, considered and potentially saved for over many years. So it’s safe to say that the first step in getting a mortgage is to plan for it financially.

Saving money toward a down payment and figuring out how much you can afford to pay each month on a mortgage payment is the first step in obtaining a mortgage. Getting your credit score as high as possible and having a solid credit history (ideally one that goes back several years) is also important.

Once you’re ready to secure a mortgage, you’ll fill out an application and provide documentation, such as proof of income and assets. Your lender will use this information to review your credit and financial history for preapproval. After you’re preapproved, you can start looking for a home or property you’d like to purchase (if you haven’t done this already).

After you’ve selected a property and it’s been appraised, you’ll eventually go through underwriting and finally, closing. Most closing processes occur in person, where you’ll sit down with an attorney who will walk you through all the documents you’ll sign in order to become the official owner of your home.

» MORE: Top-rated mortgage providers

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Ramsey Solutions, “What Is an Amortization Schedule and How Does It Work?” Accessed June 25, 2025.

- Quicken Loans, “Who Are The Parties to a Mortgage?” Accessed June 25, 2025.

- Consumer Financial Protection Bureau, “What is mortgage insurance and how does it work?” Accessed June 26, 2025.