Personal loan scams are becoming increasingly common, often targeting individuals seeking quick financial solutions. Understanding how these scams operate and recognizing their warning signs can help protect your finances. We’ll cover how to spot a potential scam, how to protect yourself and what to do if you fall victim to a scam.

Personal loan scams are usually fake offers of money in exchange for stealing your money or personal information.

Jump to insightThese scams typically target a wide range of people in hopes of catching at least a few people in a vulnerable moment.

Jump to insightSome red flags include requiring wire transfers, gift card purchases or large upfront fees.

Jump to insightWhat is a personal loan scam?

A personal loan scam is a fake offer to loan you money that’s actually designed to steal your money or personal information. These scams can occur via phone, email or text message. They typically require large upfront fees for “paperwork processing,” but they take your money and never give you a loan. Or, after you’ve given the scammer your Social Security number for a fake application, they steal your identity and open accounts in your name.

If you get a suspicious call, don’t answer it, even to opt out. Just block the number.

Any time you receive an offer for a personal loan you didn’t apply for, it’s almost certainly a scam. This differs from predatory lending, which are loans with expensive terms like very high interest rates or massive penalties for late payments.

The Federal Trade Commission (FTC) warns that you should never answer phone calls about loans you didn’t apply for. This means you shouldn’t even respond to opt out of communications. Instead, just block the number. Even if the number on your caller ID seems legitimate, it might not be. Spoofing, or impersonating a real phone number, is a common tactic that scammers use to make calls look like they’re from someone local or a real company, according to the FTC.

How personal loan scams work

Personal loan scams generally target a wide range of people in hopes of luring a few people or even a particular person. They target people of all ages, from college students to senior citizens.

“Scammers use a variety of tactics,” said Matthew Stern, CEO of CNC Intelligence, a company that helps consumers get their money back after being scammed. “[They] become skilled at learning what our vulnerabilities are and how to exploit them.”

“Once a scammer obtains your personal information, like family members’ names, pets’ names or public information such as your address or contact details, they can use them in order to try and gain access to your accounts, or impersonate you to your loved ones,” Stern said. “They can also use recordings, voice and video, to impersonate you via AI.”

Never make decisions under pressure. It is always best to speak with a financial advisor before making any financial decisions.”

Stern said people fall victim to scams because we tend to make emotional and often impulsive decisions if under pressure. The more pressure a scammer puts on us, the more likely we are to make a quick decision without thinking it through completely.

“Never make decisions under pressure,” Stern said. “It is always best to speak with a financial advisor before making any financial decisions.”

» MORE: Are online loans safe?

Types of personal loan scams

Personal loan scams typically have similar tactics. They’ll usually offer you money you didn’t ask for in exchange for fees or your sensitive information. Here are some scams to watch out for:

Advance fee loan scam

This scam occurs when a lender promises you a personal loan after you pay various upfront fees. In cases like this, the scammer’s only goal is to get the upfront fee, Matthew Stern said. They will then likely target their victims again for another fee, for another reason.

Government grant scam

Government grant and loan scams are where a person calls and guarantees a grant or loan from the government in exchange for a seemingly small fee. Usually, the scammer’s goal is to collect the fee and move on to the next victim.

Online personal loan scam

If you click on an online ad for fast, guaranteed approval for a personal loan, it’s likely a scam. No legitimate personal loan lender will offer guaranteed approval as approval is never guaranteed.

Wire transfer and gift card scams

Some scammers request that you send money via wire transfer or gift cards as an upfront fee for a personal loan. Money wires and gift cards can be difficult to trace, so scammers use this method frequently.

Personal loan red flags

Watch out for red flags like:

- Guaranteed approval

- Loan offers you didn’t apply for

- Logos that are very similar to large, well-known banks

- Requiring vague upfront fees

- High-pressure tactics

- Requests for sensitive information, like your Social Security number

- Lack of a physical address or phone number

How to protect yourself from loan scams

Generally, if you didn’t directly apply for a personal loan, the too-good-to-be-true loan offer you’ve received is most likely a scam. Here are some tips for protecting yourself:

Don’t answer unsolicited calls, texts or emails

The first step to avoiding scams is to not engage with any unsolicited contact, Matthew Stern said.

Don’t start conversations with people that contact you out of the blue, especially if they’re reaching out about financial opportunities.”

“Don’t open text messages or emails from unknown senders,” Stern said. “If someone who you did not contact first calls you, hang up right away or simply don’t answer. Don’t start conversations with people that contact you out of the blue, especially if they’re reaching out about financial opportunities.”

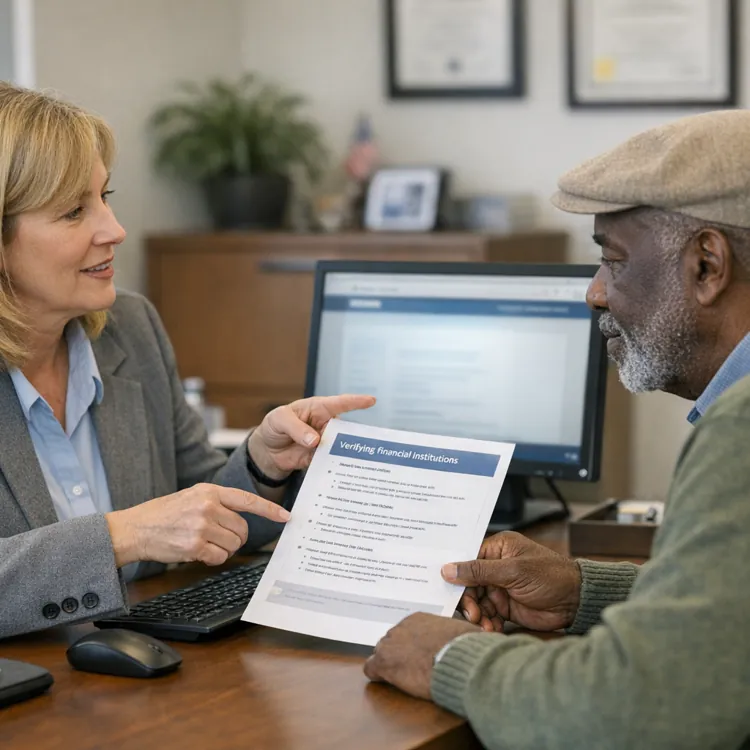

Verify financial institutions’ credentials

Before moving forward with any personal loan, verify the credentials of any bank or financial institution you use for a loan. You can verify authenticity by looking up the company’s credentials on the Nationwide Multistate Licensing System (NMLS).

Any bank or financial institution you use should also have its deposit accounts insured by the Federal Deposit Insurance Corp. (FDIC). While this should be listed on an institution’s website, you can also look it up on the FDIC’s website.

Check website addresses

Stern said to type website addresses into web browsers rather than copying and pasting them.

“Scammers can use hyperlinks and website addresses that look the same as legitimate websites, but are actually cloned sites,” Stern said.

» RELATED: How to avoid debt relief scams

What to do if you’ve been scammed

It can be difficult to get your money back if you fall victim to a scam. But there are steps you can take to protect your identity and potentially recover lost funds. Here’s what to do:

- Immediately stop communicating with the scammer.

- Report the crime to the local police and with the Internet Crime Complaint Center (IC3).

- Contact your bank(s), credit card issuer(s), mortgage lender and any other financial institutions you use to inform them of the scam so they can be aware of future suspicious account activity.

- Freeze your credit profiles with TransUnion, Experian and Equifax to protect your identity and credit.

- Change financial account passwords.

The FTC also encourages scam victims to report fraud to the FTC and to report cases of identity theft.

FAQ

How can you verify whether a loan company is legit?

If a loan company reaches out to you without you having filled out a request for a personal loan, assume it is not legit. Before working with any company, look it up online and check customer reviews. You can also verify the credentials of any bank or financial institution by looking it up with the NMLS or FDIC.

How do personal loan scams work?

Personal loan scams work by pressuring you into paying a fee or giving your personal information in exchange for funding that you never receive. These kinds of scams may use pressure tactics or guaranteed approval to make the offer seem more attractive.

How can I protect myself from loan scams?

The best way to protect yourself from loan scams is to avoid any type of contact with any company you didn’t directly reach out to. Any company that reaches out offering you a loan, especially if it uses high-pressure tactics or requires an advance payment, likely isn’t legitimate.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Federal Trade Commission, “Ignore Unexpected Calls About Loans You Didn’t Apply For.” Accessed March 26, 2026.

- Federal Trade Commission, “What to Do if You Were Scammed.” Accessed March 26, 2026.