High-yield savings account definition

A high-yield savings account is the same as a traditional savings account, except it earns a higher annual percentage yield (APY). This means the money you hold in the account will grow at a faster rate. A high-yield savings account rate can be 10 to 15 times higher than a traditional savings account rate.

The primary benefit of a high-yield savings account is the potential to earn more interest. So, this account is best if you plan to only use the money you deposit if a major need arises, such as an emergency. High-yield savings accounts are not ideal for bill-paying since you won’t earn interest on funds you take out of the account.

How do high-yield savings accounts work?

High-yield savings accounts work the same as traditional savings accounts. Unlike with a checking or money market account, you can’t write checks out of a savings account. You also can’t use a debit account to pay for purchases out of your account.

Additionally, some banks and credit unions limit the number of transactions you can make each month with a high-yield savings account. For example, you may be unable to make more than six transfers or withdrawals from your account each month. If you exceed the limit, the bank might convert your account to a checking or money market account.

Additionally, in some cases, you may incur a fee if your balance falls below a certain amount (e.g., $1,000, $10,000). Make sure you can meet any balance minimums before opening this type of account.

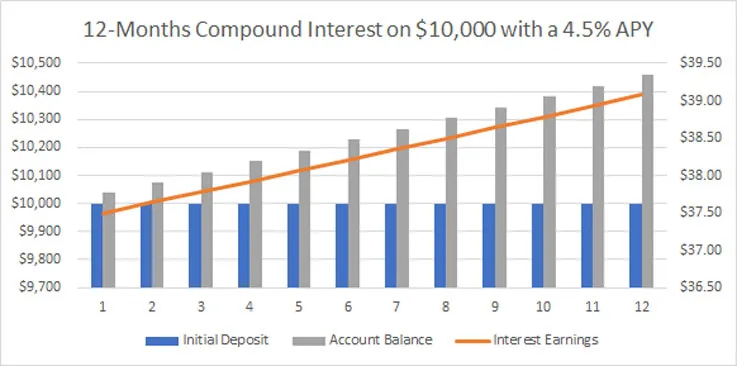

One of the best features of traditional and high-yield savings accounts is compound interest. As you earn interest on the funds you have saved each month, these interest earnings are added to your principal balance. The next month, you’ll earn interest on your initial principal balance plus the interest you previously earned.

For example, let’s say you maintain $10,000 in deposits for a year at an interest rate of 4.5%, with interest compounding monthly. In this case, you would earn $459 in interest. That’s $9 more than the $450 you would earn in a year if the interest wasn’t compounded monthly.

How to choose a high-yield savings account

The primary factors you should consider when choosing a high-yield savings account are:

- APY: The APY is the interest rate you earn on the money in your account. Since the interest rates on high-yield savings accounts are variable, this rate will go up and down with changes in the market and economy.

- Bank fees: Some banks charge fees for high-yield savings accounts, but these fees might be waived if you meet certain requirements. For example, you might not need to pay fees if you maintain a minimum balance or transfer money into the account monthly.

- Initial deposit: You may be required to make an initial deposit of $500 or more to open a high-yield savings account.

- Minimum balance requirements: Some banks require you to maintain a minimum balance (e.g., $1,000, $10,000) to keep the account open or avoid fees.

- Transaction limits: Some banks limit the monthly withdrawal or transfer transactions you can conduct. For example, you may not be allowed to make more than six transfers out of the account each month.

Gary Zimmerman, the founder and CEO of MaxMyInterest, an online marketplace that matches investors and banks, said, “As long as the account is FDIC-insured, it really doesn’t matter much which bank you pick.” With an FDIC-insured bank or NCUA-insured credit union, $250,000 of your total deposits are backed by government deposit insurance.

Zimmerman went on to explain: “When it comes to savings accounts, the interest rate is the most important factor. But banks’ needs for deposits change from time to time, and so do their rates. As a result, you shouldn’t think about picking one savings account; you should have multiple savings accounts and be ready to move funds to whichever bank is offering the highest rate.”

How to open a high-yield savings account

The four basic steps to open a high-yield savings account with a bank or credit union are:

- Shop for the best rate. Banks and credit unions frequently change the rates on their high-yield savings accounts to attract more business or reflect market changes. This makes it especially important to shop around for the best rate.

- Select a bank or credit union. Consider things like minimum deposit requirements, possible fees and the ease of accessing your funds.

- Submit an application. In most cases, you can complete the application online. You’ll need to provide personal information, like your name, address, Social Security number and phone number.

- Fund your account. After your account is opened, you’ll need to add funds. You can usually do this by electronically transferring the funds from another bank or account. You can also deposit funds by check.

Alternatives to high-yield savings accounts

Some of the best alternatives to high-yield savings accounts are CDs, Treasury marketable securities, IRAs and money market accounts.

CDs and Treasury marketable securities (like Treasury bonds) are good if you won’t need your funds for a long period. This is because you’ll earn a fixed rate for a set term (e.g., six months, two years). Plus, CDs from FDIC-insured banks are backed by deposit insurance, and U.S. Treasurys are backed by the full faith and credit of the U.S. government.

However, Levi Sanchez, a certified financial planner and the founder of Millenial Wealth, noted that you can’t access your funds as easily with these types of accounts. If easy access is important to you, consider a money market account. This type of account works similarly to a savings account but often has more features, like check-writing abilities.

Another good alternative to a high-yield savings account is an IRA, which comes with tax advantages. However, you’ll pay additional taxes if you need to access the funds before you reach retirement age. Plus, there are limits on how much you can contribute to an IRA each year. For example, in 2023, you can contribute $6,500 annually if you’re younger than 50 and $7,500 if you’re 50 years or older.

FAQ

What interest rate can you earn with a high-yield savings account?

High-yield savings account rates can be as much as 10 to 15 times higher than APYs on traditional savings accounts. So, if the rate on a traditional savings account is 0.33%, you might get an APY as high as 3.30% to 4.95% on a high-yield savings account.

Keep in mind the interest rates on high-yield savings accounts are variable, meaning they increase or decrease with changes to the market and economic environment.

High-yield savings account vs. traditional savings account – what’s the difference?

The main difference between these types of accounts is that high-yield savings accounts carry a much higher interest rate than traditional savings accounts. As a result, a high-yield savings account might have a minimum deposit requirement, and you may need to maintain a higher balance to keep the account open or avoid fees.

However, maintaining a higher balance in a high-yield savings account may be worth it, as the APY could be as much as 10 to 15 times higher than with a traditional savings account.

Do you pay taxes on a high-yield savings account?

You’ll pay taxes on the interest you earn on a high-yield savings account at the same rate as your ordinary income. You’ll need to report earned interest of at least $10 on IRS Form 1099-INT.

Are high-yield savings accounts safe?

Deposits in a high-yield savings account will not decrease because they aren’t tied to an index, like the stock market. Additionally, if your account is held by a government-insured financial institution, you’re protected from losses if the institution fails or goes bankrupt.

Deposits at these financial institutions are protected by up to $250,000 per account holder by the Federal Deposit Insurance Corporation (FDIC) for FDIC-insured banks and by the National Credit Union Administration (NCUA) for NCUA-insured credit unions.

Bottom line

While you’ll earn a higher interest rate on a high-yield savings account than a traditional savings account, it’s important to consider all the account features and your financial goals before opening one. For example, some banks may require you to maintain a minimum account balance to keep the account open or avoid fees, which could eat into your interest earnings.

If you don’t need to access the funds regularly, you might earn a higher rate and have more predictable earnings with a CD. If your goal is to save for retirement, an IRA may be a better option. High-yield savings accounts are better if you want to access your funds easily, such as for an emergency fund.

By considering your financial goals and the account features, you’ll be better equipped to decide if a high-yield savings account or an alternative is right for you.

Article sources

- Federal Deposit Insurance Corporation, " Bankers Resource Center - National Rates and Rate Caps ." Accessed Jan. 30, 2023.

- Federal Deposit Insurance Corporation, " Deposit Insurance - Your Insured Deposits ." Accessed Jan. 30, 2023.

- MyCreditUnion.gov, " Share Insurance Toolkit for Consumers ." Accessed Jan. 30, 2023.

- IRS, " IRA FAQs ." Accessed Feb. 2, 2023.

- IRS, " Topic No. 403 Interest Received ." Accessed Jan. 30, 2023.

- TreasuryDirect, " About Treasury Marketable Securities ." Accessed Feb. 2, 2023.