How identity theft insurance works

Identity theft insurance is similar to other types of insurance: You purchase a policy, pay a monthly or annual premium and get coverage for qualified expenses if someone steals your identity. Many insurance companies offer this protection, and it's often available as an add-on to homeowner’s insurance, auto insurance and other policies.

If you’re a victim of identity theft, you’ll typically need to follow these steps with your provider:

- File a claim. Contact your insurer to let them know your identity was compromised, and provide them with your plan of action for restoration. Make sure you also follow the proper protocol for notifying authorities, banks and credit bureaus.

- Provide documentation. Send documentation for all expenses related to your claim to your provider, including legal fees, notary costs and lost wages. They will decide to approve or deny based on your coverage.

- Stay in contact with your provider. Your insurer will assign a case manager or fraud specialist to your case. Keep in touch to track reimbursement and send additional documentation, if necessary.

- Monitor for reimbursement. Check your accounts for the reimbursement of approved funds, and follow up with your case manager if something wasn’t covered that should have been.

- Ask about next steps. Confirm with your case manager that they will initiate the included safety measures, like helping you freeze your credit and setting up alerts for future red flags.

What does identity theft insurance cover?

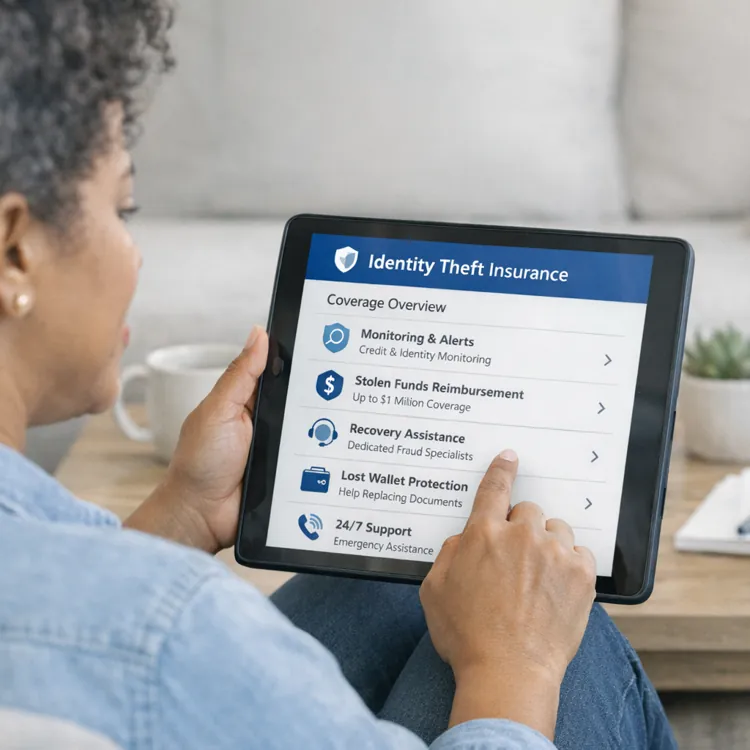

Identity theft insurance doesn’t guarantee that your identity won’t be stolen, but it can reduce the risk. More importantly, it provides reimbursement for expenses related to restoring your identity or reporting identity theft. Coverage depends on your insurer and the plan you choose, but you should look for plans that cover:

- Legal fees if you need to hire a lawyer

- Postage fees for mail or certified mail

- Fees related to document duplication

- Notary costs if you need documents notarized

- Out-of-pocket costs related to restoration

- Lost wages for the time you take off work to resolve your issue

- Charges incurred for checking your credit report or freezing your credit

- Costs for restoring computers or data after a cyber attack

Less common features include:

- Credit and dark web monitoring

- Lost wallet assistance and emergency funds after loss

- Advances for stolen funds before they’re returned

- Replacement of stolen funds from retirement accounts or health savings accounts (HSAs)

- Ad blockers and other cybersecurity features

All identity theft insurance policies will cover some expenses related to identity restoration, but the actual protections and the reimbursement amounts will depend on the provider you choose and the plan you pick. Generally speaking, higher coverage amounts will mean higher insurance premiums.

Make sure you review coverage limits before choosing a plan, and pay attention to your deductible to avoid surprises if you ever need reimbursement.

What does identity theft insurance not cover?

Identity theft insurance does not guarantee your identity won’t be stolen. While policies can include protections, like credit monitoring or identifying data breaches, they cannot prevent identity theft.

Actual monetary losses also aren’t always included in identity theft protection coverages. Instead, federal protections limit your exposure to losses from fraud by requiring reimbursement from financial institutions.

» LEARN: How to prevent identity theft

When you file an Identity Theft Affidavit with the Federal Trade Commission (FTC), you can use the report you receive to dispute fraudulent charges on your credit cards and fraudulent activity on your credit report. You may also be able to recover stolen funds from bank accounts and investment accounts with limited liability, depending on how quickly you report the loss.

In addition to these primary exclusions, all policies will have a list of excluded items you won’t get coverage for, as well as coverage limits. These vary based on your insurer and your plan.

How much does identity theft insurance cost?

Identity theft insurance usually costs between $7 and $30 per month, or between $84 and $360 per year. The actual cost of coverage depends on your provider and the plan you choose. More expensive plans with higher premiums typically mean the following:

- Lower deductibles and out-of-pocket costs

- Higher coverage limits

- More add-on services and protections

You should always read through a complete list of coverages, exclusions, fees and terms before enrolling in a policy.

| Allstate | NordProtect | IDShield | |

|---|---|---|---|

| Plans available | 4 | 4 | 2 |

| Cost range (monthly) | $3 to $19 (individual)$6 to $36 (family) | $0.99 to $6.99 (2-year)$1.49 to $7.99 (1-year)$5.99 to $31.99 (1-month) |

$14.95 (individual)$29.95 (family) |

| Maximum coverage for expenses | $25,000 to $1 million | $1 million | $3 million |

| Additional coverages/services | Up to 62 | Up to 15 | Up to 40 |

Is identity theft insurance worth it?

Whether or not identity theft insurance is worth it for you depends on your tolerance for risk, your ability to cover out-of-pocket costs, how often you check for identity theft, how much time you can invest to restore your identity and your overall risk for identity theft.

Identity theft insurance might be valuable especially for individuals who are at greater risk of fraud, including:

- Profiles with a strong online presence

- Public-facing figures

- Persons with high net worth or income

- Previous ID theft victims

- Children

- The elderly, especially those with medical bills

However, identity theft insurance provides protection regardless of your income, age and online activity — and for many people, that peace of mind is well worth the investment. If you’re unsure if it’s the right move for you, consider the following pros and cons.

Pros

- Provides peace of mind

- Can save time and money in case of fraud

- Often includes monitoring afterward to help prevent future attacks

Cons

- Costs between $12 and $360 per year

- Doesn’t prevent identity theft

- May duplicate coverages from financial institutions or credit card companies

FAQ

Is identity theft insurance worth getting?

Identity theft insurance is worth getting if you want peace of mind and don’t want to spend time monitoring your accounts for fraudulent activity. It can identify issues immediately to maximize your chances of quick recovery and reimbursement for stolen funds.

What happens when you claim identity theft?

When you report identity theft to the FTC and local authorities, you can then use your reports to reverse some fraudulent activity on your accounts. It’s also a good idea to freeze your credit and set up fraud alerts for the future.

What does identity theft insurance not cover?

Identity theft insurance doesn’t cover funds lost from financial accounts and doesn’t guarantee that you won’t fall victim to fraud. However, federal protections should help you recover financial loss independent of insurance coverage.

How does identity theft insurance help in recovery?

Identity theft insurance often includes access to a case manager or ID theft specialist who can walk you through the process of identity recovery and even complete the legwork for you. An insurance policy can also cover out-of-pocket expenses and even provide reimbursement for lost wages as a result of the time and effort it takes to recover your identity.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Allstate Identity Protection, “Introducing cybersecurity and restoration for the whole family.” Accessed Jan. 21, 2026.

- Consumer Financial Protection Bureau, “Liability of consumer for unauthorized transfers.” Accessed Jan. 21, 2026.

- IdentityTheft.gov, “What To Do Right Away.” Accessed Jan. 21, 2026.

- NordProtect, “NordProtect: Get back on track with identity theft recovery.” Accessed Jan. 21, 2026.

- Office of the Comptroller of the Currency, “Identity Theft.” Accessed Jan. 21, 2026.

- State Farm, “Identity restoration can help if identity theft protection fails.” Accessed Jan. 21, 2026.