Your monthly mortgage payment consists of both the loan principal and interest.

Jump to insightYou might receive a lower interest rate by raising your credit score, increasing your down payment and comparing different lenders.

Jump to insightMaking extra mortgage payments each month can reduce the total amount of interest you’ll pay on your house.

Jump to insightWhat is mortgage interest?

When you take out a mortgage to buy a home, you must pay interest to the institution lending you money. Interest is a fee that helps offset the risk the lender takes when letting you borrow their funds.

Your monthly payment includes the original loan amount (the principal) and interest. At the beginning of your mortgage, your payments mostly go toward the interest on your loan. As time goes on, your balance decreases, and you start paying more on the principal and less on interest.

How is mortgage interest calculated?

Your lender will create a payment schedule using an amortization formula that divides your principal and interest into monthly payments.

The lender applies the interest, expressed as a percentage, to your outstanding principal. Your interest rate directly influences your monthly payment amount and the total amount you will pay for your home by the end of the mortgage.

If your mortgage has compounding interest, you’ll pay on the principal and any previously accrued interest. The more frequent the compounding, the more interest you will pay.

Tax implications of mortgage interest

Depending on the situation, there may be some tax deductions for homeowners, such as the interest they pay on their mortgage. However, you can only take advantage of a mortgage interest deduction if you’re not already taking the standard deduction on your return.

Factors that affect mortgage interest rates

While several factors can influence your mortgage’s interest rate, here are some of the main ones to watch out for.

- Credit score: Borrowers with higher credit scores can typically secure better mortgage rates.

- Down payment: A larger down payment often results in a lower interest rate.

- Loan term: Loans with shorter terms, such as a 15-year mortgage, often provide lower rates. However, the monthly payments are typically lower with lengthier mortgages, so they may be more manageable.

- Loan type: If you choose an adjustable-rate mortgage (ARM) vs. a fixed-rate mortgage, you may get a lower interest rate at the beginning of the loan. However, once the introductory period ends, your interest rate can change, and you may pay a higher rate.

- Market conditions: Lenders often set the interest rates according to the federal funds rate. Whether the Fed cuts or raises the benchmark interest rate depends on economic indicators such as inflation, unemployment and gross domestic product (GDP).

How to lower your mortgage interest

Although some factors, such as market conditions, may be out of your control, there are some ways to get a low mortgage rate:

- Improve your credit score: Lenders typically offer the best interest rates to borrowers with very good or excellent credit scores (between 740 and 850).

- Save for a bigger down payment: While lenders frequently only require 3% to 5%, a larger down payment can lower your interest rate because you're borrowing less money.

- Compare rates at different lenders: Interest rates often vary between mortgage lenders; requesting quotes from multiple institutions can help you find the best rate.

- Look into an FHA loan: If you have a low credit score, you may qualify for a lower rate through an FHA loan.

You may also be able to refinance for a lower interest rate a few years into your mortgage. However, refinancing comes with its own closing costs, so you’ll have to weigh whether it’s a good strategy for your situation.

The impact of extra payments on interest

Making extra mortgage payments is tax-free and risk-free, and can be a good strategy for paying off your mortgage faster.

“When paying down your mortgage, your best bet is to make extra principal payments,” said Jay Zigmont, a certified financial planner and founder and CEO of Childfree Wealth, a financial planning firm for people without children. “When you pay down the principal, it lowers the amount going to interest with future payments. You may be able to automate your extra principal payments by adding on money to your monthly payment.”

Zigmont also suggested making biweekly payments to increase the amount you put toward your mortgage each year.

Example of how extra payments affect interest

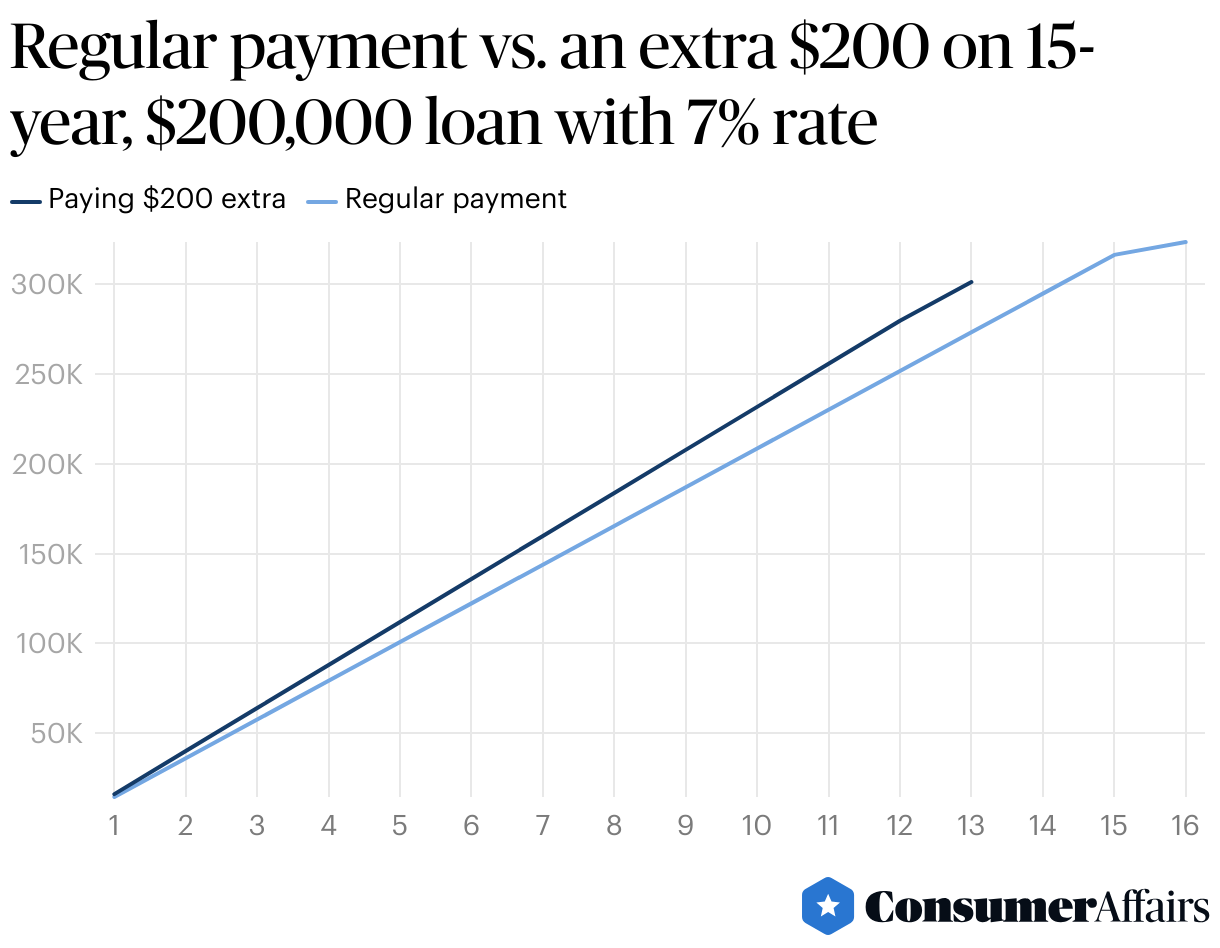

Let’s look at an example of how paying just $200 extra on your mortgage can affect the total amount paid.

The following chart illustrates a 15-year mortgage with an original balance of $200,000 and an interest rate of 7%.

As you can see, paying an extra $200 on your mortgage each month results in a shorter payoff schedule and lower total costs than if you had only paid the regular monthly payments.

In total, you would save $22,330 and pay off the loan two years and five months early.

» MORE: Mortgage APR vs. interest rate

FAQ

Does my interest rate change over time?

If you have a fixed-rate mortgage, your interest rate will stay the same throughout the life of the loan. However, with a variable-rate mortgage, your interest rate could change periodically.

Can I negotiate my mortgage interest rate?

Yes, you can negotiate your mortgage interest rate. You’ll be in a better position to negotiate if you have a good credit score.

What’s the difference between the interest rate and APR?

While the interest rate only includes the fee for borrowing money, APR also encompasses other charges such as loan origination fees, discount points, mortgage insurance and closing costs. Therefore, APR more accurately reflects the cost of your loan.

Bottom line

Your monthly mortgage payment consists of both the amount you borrowed (the principal) plus interest. Interest is the amount the lender charges for taking on the risk of lending you money.

While some factors that influence mortgage rates are outside your control, you may get a lower rate if you improve your credit score, increase your down payment and compare different lenders.

Furthermore, you can minimize how much interest you pay over the course of your loan by contributing extra payments toward your principal each month.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Federal Reserve Economic Data, “Median Sales Price of Houses Sold for the United States.” Accessed Nov. 18, 2025.

- Equifax, “What is a Good Credit Score?” Accessed Nov. 18, 2025.

- Consumer Financial Protection Bureau, “Determine your down payment.” Accessed Nov. 18, 2025.

- Consumer Financial Protection Bureau, “How to decide how much to spend on your down payment.” Accessed Nov. 18, 2025.

- IRS, “Publication 936 (2024), Home Mortgage Interest Deduction.” Accessed Nov. 18, 2025.