Defaulting on a personal loan severely impacts your credit score, making future borrowing more difficult.

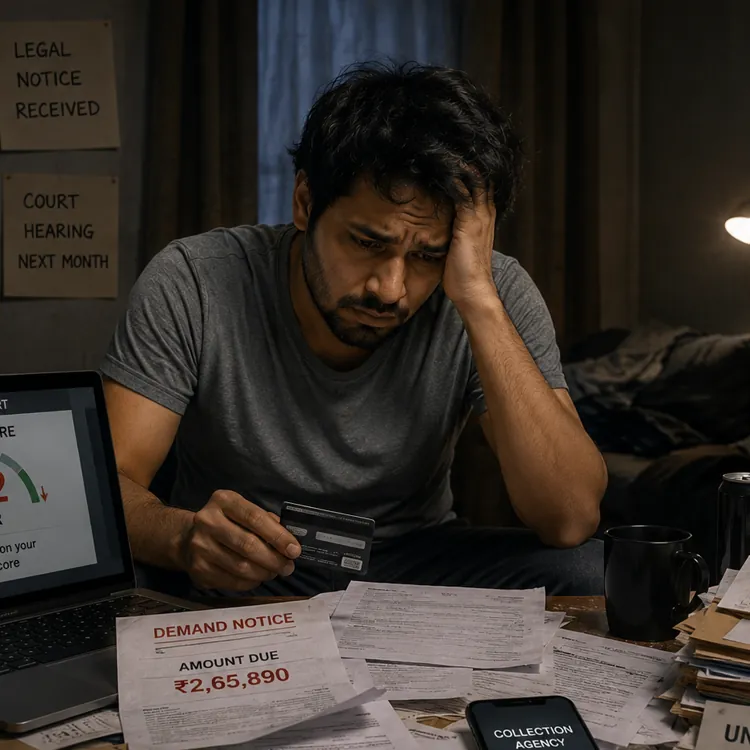

Jump to insightLegal actions, including wage garnishment, may follow if the debt is not resolved.

Jump to insightProactive communication with lenders can help reduce the consequences of default.

Jump to insightHow loan default works

Your loan is considered delinquent as soon as your payment is late. Payments are generally considered to be late if they’re made between one and 30 days past the due date. If you don't pay after 30 days, your late payment will be reported to the credit bureaus, which will likely lower your credit score.

A loan will typically be in default if you don't make a payment for 90 days.

“The day after the due date of a loan, the loan becomes delinquent,” Seann Malloy said. “Default, on the other hand, carries a more serious consequence. It comes after a period of sustained nonpayment, typically 90 to 180 days, depending on the lender’s policy.”

If you don’t make payments on the loan for 90 days, your account will go into default and collection efforts will begin. Once the late payment reaches 120 days, it's common for the lender to charge off the loan and sell it to a collection agency.

| Days late | Status | Consequence |

|---|---|---|

| 1 to 30 days | Late | Possible late fee |

| 30 to 90 days | Delinquent | Reported to credit bureaus |

| 90 to 120 days | Default | Collection efforts |

| More than 120 days | Charged off | May be sold to a collection agency |

Consequences of defaulting on a personal loan

Credit bureaus will generally be notified as soon as your payment is 30 days late. But the more delayed the payment, the greater the penalty.

Payment history is 35% of your FICO credit score.

Your credit score will drop

Letting your loan go into default will have a major impact on your credit score. By the time your loan is in default, you’ll have several reported late payments. Payment history, or paying your bills on time, makes up 35% of your FICO credit score. And the later the payment is, the more damage it does to your credit score.

Late payments will stay on your credit report

Late payments and default will remain on your credit report for seven years, even if you later pay the loan off in full.

You’ll risk repossession for secured loans

If the loan is secured, say with your vehicle, you will risk repossession of the asset. If you don’t pay the loan based on the agreed-upon terms, the lender has the legal right to seize the asset and sell it in an attempt to collect the balance of the loan. Repossession will also negatively impact your credit.

» RELATED: Secured vs. unsecured loans

Legal implications of loan default

There can be legal implications for defaulting on a personal loan.

"Once a personal loan goes into default, a lender has some legal options,” Seann Malloy said. “For an unsecured loan — or a loan for which there is no collateral, such as a credit card debt or medical bill — lenders can sue the borrower in civil court for a judgment and, depending on the state, pursue wage garnishment or asset liens.”

If the lender sues you, don't ignore the court notices. It's best to respond by the date specified in the court documents. You may also want to get a lawyer to assist you. Responding to the lawsuit gives you an opportunity to negotiate the debt or get it removed completely. Lenders need to prove that the debt is valid. If they are unable to do so, you won’t be required to pay.

If you don't respond, it's likely the judge will issue a default judgment in favor of the lender. This gives the lender more tools to collect the debt from you, such as garnishing your wages or putting a lien on your property.

Know your rights

If you have an aggressive debt collection agency, you'll want to know your rights under the Fair Debt Collection Practices Act. For example, debt collectors aren’t allowed to call you before 8 a.m. or after 9 p.m. or at a place they know is inconvenient, such as your workplace. If you get an attorney, all communication must go through your attorney.

What to do if you’re at risk of default

If you’re struggling to stick to your loan terms, you should contact your lender right away. You may be able to renegotiate the terms of the loan to fit your budget more comfortably.

"As soon as you feel that you may miss a payment, you should contact your lender,” Seann Malloy said. “Many of them have hardship programs, or they can provide you with altered payment plans. When you wait until a point that you’re in default, that really [narrows] your choices down a lot."

Lenders are much more agreeable if you are communicative than if you ignore them.”

But you should still reach out, even if you've already missed some payments.

"Be assertive — detail your circumstances, supply the evidence and request written confirmation of any new terms,” Malloy said. “Putting your head in the sand does not make this go away; lenders are much more agreeable if you are communicative than if you ignore them.”

How to recover from loan default

It helps to first contact the lender to see what your options are. If the lender is unable to assist you, you may want to consider debt consolidation or credit counseling. Both are useful if you have several loans that you are having trouble paying.

Negotiate a settlement

If you currently have a loan in default, contact your lender and see if there are any remedies available. You may be able to negotiate a settlement, where you make a lump-sum payment for less than the amount owed.

Consider debt consolidation

With debt consolidation, you’ll take out a new loan that combines some or all of your current debt into one new payment. The idea is to lower your total monthly payments to a level that you can maintain. It's important to do this before your credit begins to drop or you’ll have trouble getting a new loan.

Look into credit counseling

Credit counseling may put you on a debt management plan with a payment that is lower than the combined amount of all your loans. You'll make a monthly payment to the credit counseling company, which will then distribute the funds to your loans.

Repair your credit

When the time is right, you can start rebuilding your credit by making on-time payments on all your bills and debts. It also helps to keep your credit utilization ratio low (usually below 30%), since that’s the second biggest factor of your FICO credit score.

FAQ

How bad is defaulting on a personal loan?

Defaulting on a personal loan will severely impact your credit and may result in a lawsuit and wage garnishment. You don't want to default on a loan unless you have no other choice. Contact the lender right away if you find you’re unable to make payments.

Can you be sued for defaulting on a personal loan?

Yes, you can be sued for defaulting on a personal loan. If the lender wins the lawsuit, it may be able to garnish your wages or put a lien on your property.

How can I avoid defaulting on a personal loan?

Avoid defaulting on your loan by ensuring you have a budget and are borrowing responsibly. If you realize that you won’t be able to make payments, contact the lender immediately and see if other arrangements can be made.

Can defaulting on a loan affect my ability to get future credit?

Yes, defaulting on a loan will have a severe impact on your credit score, and it will affect your ability to get future credit. The late payments and default will be reported to the credit bureaus and the negative mark will remain on your credit report for seven years.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Consumer Financial Protection Bureau, "What Should I Do if I’m Sued by a Debt Collector or Creditor?” Accessed May 18, 2026.

- Consumer Financial Protection Bureau, "What Laws Limit What Debt Collectors Can Say or Do?” Accessed May 18, 2026.