Types of IRS notices and their implications

When you fail to file your tax return or pay your taxes in full, you will receive a letter from the IRS with a bill. If you do not make a payment, the IRS will begin collection and pursue that debt until it’s paid or until the statute of limitations expires.

Nathan Goldman, a member of the American Accounting Association and an accounting professor at NC State University, explained the basics of IRS notices.

“An IRS notice is a written communication that the IRS sends to a taxpayer to inform them about a tax-related issue,” he said. “It can result from a balance that is due, a need for additional information or documentation, a notice to correct errors on the return or inform the taxpayer of penalties, interest or refunds.”

If you receive an IRS notice, be sure to review it carefully so you understand why you are receiving the notice and what steps you must take to resolve it.

This usually includes Notice CP14 for individual taxpayers or CP161 for business taxpayers, but official IRS notices include a CP or LTR number in the right corner. Subsequent bills typically include Notices CP501, CP503, and CP504.

Common IRS Notices

| Notice | Type of Notice |

|---|---|

| Balance due notice |

|

| Subsequent notices of past due debt |

|

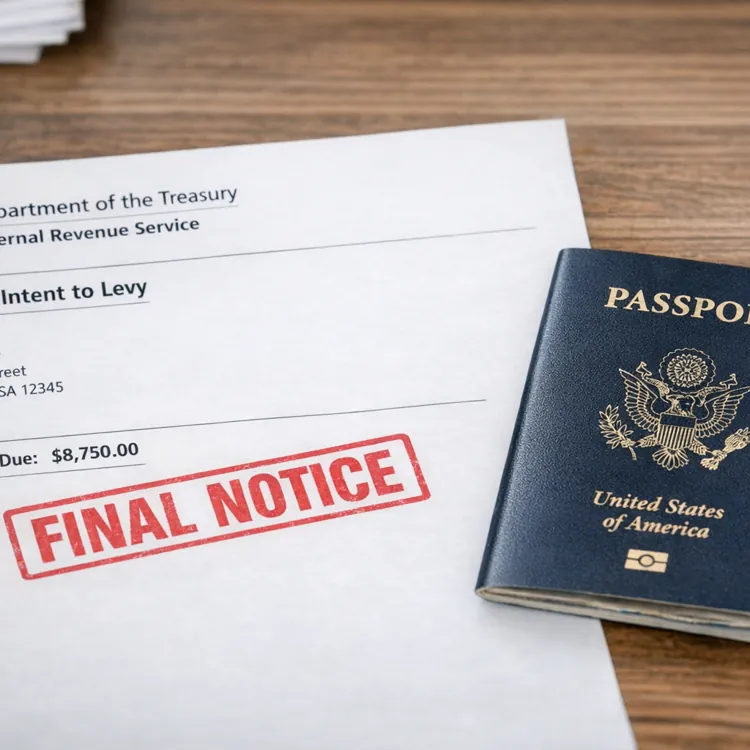

| Final Notice of Intent to Levy |

|

| Final Notice, Notice of Intent to Levy and Your Right to a Hearing |

|

| Changes to Your Form 1040, Amount Due |

|

Your notice may be sent by regular or certified mail, depending on the notice type. The IRS will never contact you by email or phone.

Consequences of ignoring IRS notices

When you receive an IRS notice, it is important that you make a payment or set up a payment plan immediately. The last thing you want is for the IRS to charge you with tax evasion.

“The process typically begins with warning letters, but if there’s no response, penalties and interest will add up,” said J. Anton Collins, a tax attorney at Tax Law Offices Business Tax Resolution in Naperville, Illinois.

Let’s say you file your tax return, usually by April 15th for individuals or quarterly for businesses, and the IRS sends you the first bill for any taxes due. If you do not make a payment, the IRS sends at least one more notice before starting the collection process.

If there’s no response, penalties and interest will add up.”

The debt collection process can affect you negatively in several ways, from extra penalties and interest to seizure of your assets. Your account may also be sent to a private collection agency, but the IRS will notify you to let you know.

A revenue officer may visit your home or business to try to settle the balance. These visits are typically scheduled in advance.

Other consequences include a levy, lien or revocation of your passport.

Penalties and interest

Your IRS notice will detail your balance, including any penalties. It’s critical that you do not ignore this notice, or you could face severe penalties.

You’ll also owe interest, which begins accruing on the tax due date and compounds daily. A monthly late payment penalty will be assessed, up to the maximum allowable amount.

Until your debt is resolved, the IRS may apply any future tax refunds to satisfy your balance. Note that if your debt is due to an individual shared responsibility payment under the Affordable Care Act, it is not subject to the failure to pay penalty, levies or liens.

Federal tax lien

A tax lien is a legal claim against current and future property. This includes not only physical assets such as your home and vehicle, but also your bank accounts and salary.

The IRS will file an official Notice of Federal Tax Lien with the appropriate state or local authorities, which serves as a public notification of the lien to creditors and bill collectors. It also prioritizes the IRS over other outstanding debts.

This lien can make it extremely difficult for you to get credit in the future, whether from a lender, employer or landlord. Because of this, it’s crucial that you pay the full balance as soon as possible.

The Notice of Federal Tax Lien will only show your total debt as of the date of notice. You can call 1-800-913-6050 (or 859-3203526 for international callers) for the full payoff amount, which will include IRS penalties for both the filing and the release of your lien.

The IRS may withdraw a Notice of Federal Tax lien under the following terms, provided via IRS Form 12277, Application for Withdrawal of Filed Notice of Federal Tax Lien:

- You have enrolled in an IRS payment plan.

- It is in your or the government’s best interest to dismiss the lien.

- The lien was applied during a bankruptcy automatic stay period.

- Correct IRS procedures were not followed.

You may also qualify for a discharge of your lien if you meet the terms outlined in IRS Publication 783, How to Apply for a Certificate of Discharge of Property from Federal Tax Lien.

Federal tax levy

The IRS may also issue a federal tax levy, which enables the organization to seize your property and satisfy your tax debt.

Assets that are potentially vulnerable to this levy include:

- Homes

- Vehicles

- Wages

- Bank accounts

- Retirement accounts

- Social Security payments

Levies do not apply if you enroll in a payment plan or an offer in compromise. The IRS may also dismiss your levy due to economic hardship.

If you do experience property seizure, call the number on your notice to get help, or 1-800-829-1040 for individuals or 1-800-829-4933 for businesses.

Options for resolving tax issues

You have several options for resolving tax issues, from enrolling in a payment plan to filing an appeal.

If you wish to make a payment, you can do so online via the Online Payment Agreement application, or you can scan the QR code on your notice. This will give you access to the IRS Document Upload Tool, allowing you to upload your documents for faster processing.

If you do not qualify for online payment or you filed for bankruptcy, call the phone number on your notice immediately. You will need to provide your monthly income and expenses.

It is important to pay your tax debt in full. If you cannot pay, the IRS may offer you one of these alternative payment options to help resolve your debt:

- Short-term payment plan. You may be able to enroll in a short-term payment plan that allows you to pay off your debt within 180 days. To qualify, your maximum debt must be less than $100,000 in combined tax, penalties and interest.

- Installment agreement. This payment plan breaks your debt into more manageable monthly payments so you can pay it over time rather than in one lump sum. The exact terms vary based on your personal financial situation.

However, Goldman noted, “The amount owed still accrues interest.”

You may also qualify for currently not collectible (CNC) status or an offer in compromise.

Currently not collectible (CNC) status

You can request that the IRS put off collection and find your account currently not collectible due to financial hardship. This is only temporary, but it gives you a chance to breathe until your finances improve.

To enroll, you may need to complete a Collection Information Statement (Form 433-F PDF, Form 433-A PDF, or Form 433-B PDF). You may also need to provide proof of your financial status detailing your monthly income, expenses and assets.

Keep in mind, however, that penalties and interest will continue to accrue. The IRS will not issue a levy during this time, but it may still file a Notice of Federal Tax Lien.

Offer in compromise

An offer in compromise (OIC) is a form of tax relief that allows you to make the IRS an offer to pay less than you owe. If the IRS accepts your offer, it will forgive a portion of your balance and your total debt will be reduced.

To be eligible for an OIC, you must have received a bill for a tax debt covered in the offer. All your tax filings must be up to date, with all required estimated payments for the current year paid. You also cannot be in open bankruptcy proceedings.

The Offer in Compromise Pre-Qualifier tool can help you determine your eligibility for this type of tax relief. If you qualify, you can apply online, call the number on your official notice or complete and mail IRS Form 9465 (Installment Agreement Request), along with your bill. Be aware that a user fee may apply, although it may be reduced, waived or reimbursed for low-income taxpayers.

“Most compromise offers are rejected,” Goldman cautioned. “Successful ones are when the taxpayer cannot faithfully fulfill the amount owed.”

In the meantime, be sure to file and pay your taxes as normal to avoid any additional debts. If you fall below the maximum income requirements, you may be able to benefit from representation from the Low Income Taxpayer Clinic (LITC).

“Most of these consequences can be prevented,” Collins said. “The IRS typically steps up its enforcement only after a number of attempts to communicate with the taxpayer, so there are plenty of opportunities to take care of it before it starts to interfere.

“Engage early and respond even if you don’t know what to say,” he added. “The key is not waiting until your first collection letter from the IRS arrives. After collections start, flexibility falls.”

Professional support can be an enormous help, as well. “If you are ever in a situation where you are receiving IRS notices for not paying your taxes, you should consult with and hire a CPA or tax attorney,” Goldman said. “They can successfully help you navigate the different options for seeking relief or leniency on your repayment.”

FAQ

What happens if you ignore an IRS notice?

The IRS will pursue collections against you if you ignore an IRS notice.

How much will the IRS usually settle for?

The IRS determines settlement amounts on a case-by-case basis, depending on factors such as your finances, tax return issues, tax filing status and the total amount due.

What happens if we do not respond to an income tax notice?

If you do not respond to an income tax notice, the IRS can file a lien or levy to seize your assets. You may also lose your passport.

Is it always bad news when you get a letter from the IRS?

No, you could receive an official IRS notice stating that you overpaid your taxes and that a refund is due. You may also get a letter offering you a payment plan or informing you of reduced or waived tax liability.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- IRS, “Topic no. 201, The collection process.” Accessed Jan. 17, 2026.

- Taxpayer Advocate Service, “Taxpayer Roadmap Tool.” Accessed Jan. 17, 2026.

- Taxpayer Advocate Service, “Responding to IRS Collection Notices.” Accessed Jan. 17, 2026.

- TurboTax, “Don't Fear the Tax Man: Handling IRS Letters & Notices.” Accessed Jan. 17, 2026.

- IRS, “Publication 594.” Accessed Jan. 17, 2026.

- IRS, “Publication 4518.” Accessed Jan. 17, 2026.

- IRS, “Private debt collection.” Accessed Jan. 17, 2026.

- Jackson Hewitt, “Why you should never ignore an IRS tax bill.” Accessed Jan. 17, 2026.

- IRS, “Form 12277.” Accessed Jan. 17, 2026.

- IRS, “Offer in compromise.” Accessed Jan. 17, 2026.

- IRS, “Offer in Compromise Pre-Qualifier.” Accessed Jan. 17, 2026.

- Taxpayer Advocate Service, “Collection Appeals Program (CAP).” Accessed Jan. 17, 2026.