Financial goals and knowledge gaps

+1 more

Most Americans have several financial goals they strive for each year. Whether you want to purchase a home, save for retirement or pay for your children’s education, achieving these objectives takes time and know-how.

For example, building a reliable credit history is vital before applying for a mortgage loan, as nonexistent credit makes homebuying almost impossible. Because purchasing a home is the most significant single investment many make in their lifetime, banks and lenders want to know that those on the title have the capability to make consistent payments over an extended period.

To better understand the financial challenges many Americans encounter, we asked 1,037 people about their financial knowledge and what barriers keep them from achieving their dreams. The results may surprise — and inspire — you.

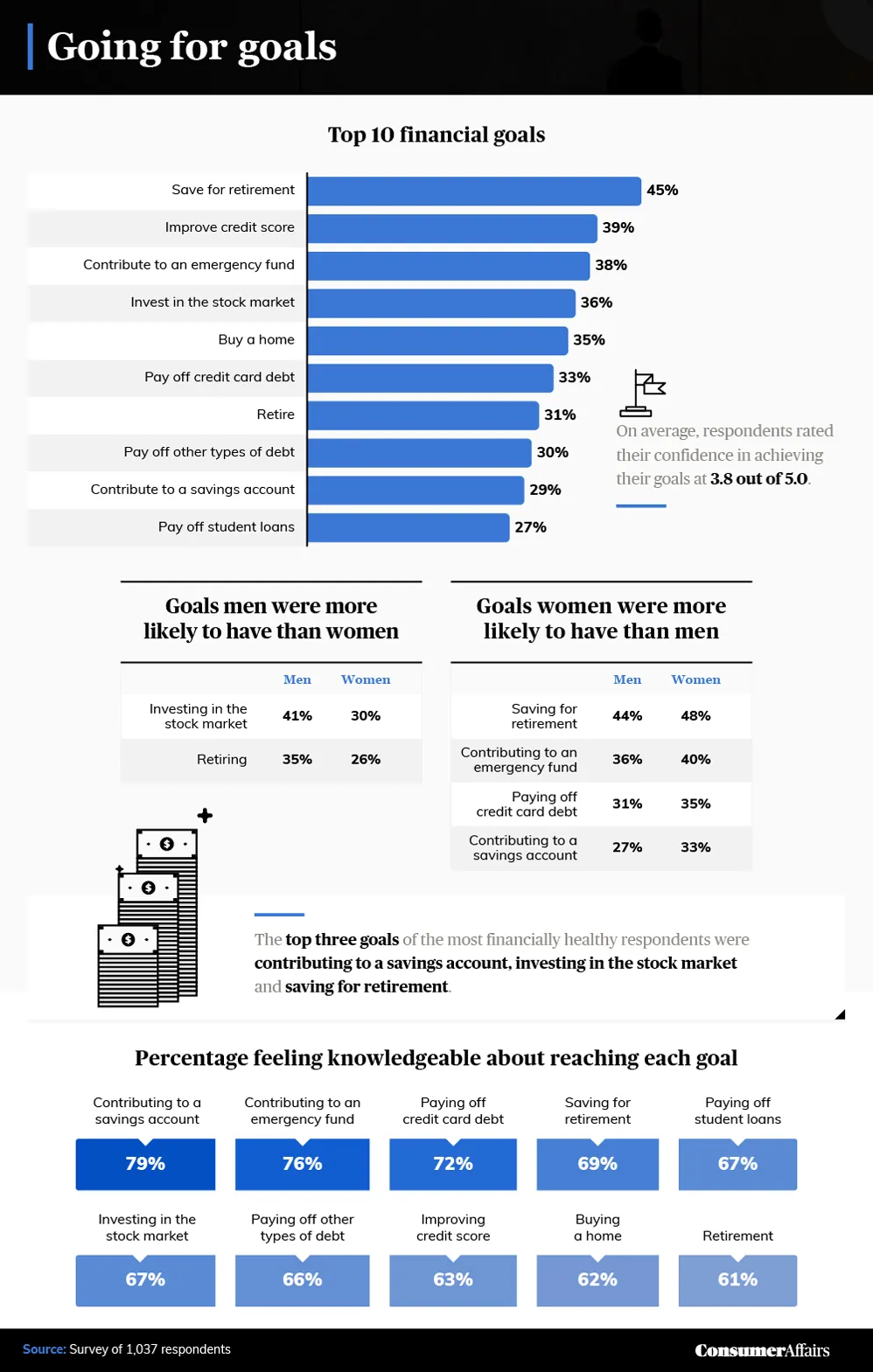

The top three goals of the financially healthiest respondents were to contribute to a savings account, invest in the stock market and save for retirement.

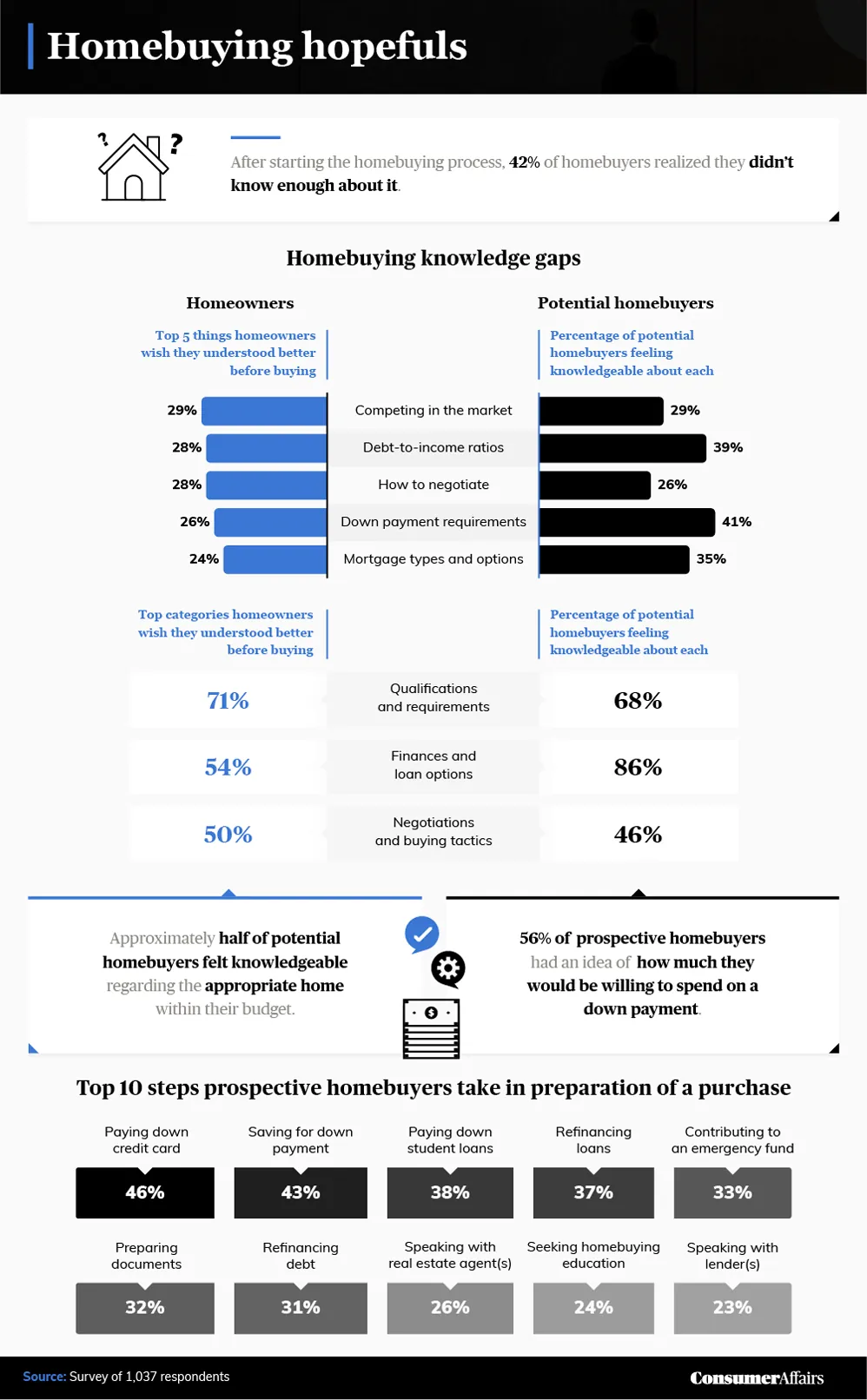

Jump to insightAfter starting the homebuying process, almost half of homebuyers (42%) realized they didn’t know enough about it.

Jump to insightThe top three things homeowners wish they had known more about before buying were qualifications and requirements, financing and loan options and negotiation and buying tactics.

Jump to insightBuilding a financial foundation

An often overlooked tenet of sound money management is to pay yourself first. This could mean creating or adding to a savings account or opening or adding to retirement or investment accounts. On payday, you might want to go shopping or buy concert or sports tickets, but paying yourself first by setting aside money for a rainy day fund can be a wiser option in the long term, increasing the chances of meeting your goals.

Younger workers sometimes defer saving for retirement, thinking they have ample time. Getting in the habit of saving money pays more significant dividends when you consider the power of compound interest, meaning accruing interest over time. Saving for retirement was the top financial goal for respondents, coming in at 45%.

Overall, women were more likely than men to prioritize their retirement savings. They also found contributing to emergency funds, paying off credit card debt and building savings accounts more important than men did. Just under a third of respondents prioritized retiring, and one-third said they’re determined to pay off credit card balances.

Improving credit score was an objective for 39% of survey participants, followed closely by building an emergency fund, investing in the stock market and buying a home. This makes sense — if you have too much outstanding debt versus your annual income (also called a high debt-to-income ratio), lenders may hesitate to extend additional credit, especially for major purchases.

Almost 80% of respondents indicated feeling knowledgeable about savings accounts, another crucial element of solid money management. A nearly equal percentage of men and women claimed to understand the importance of building an emergency fund for unexpected expenses, such as a job loss or significant repair bills.

Those surveyed that were the most financially healthy prioritized establishing a solid savings account, investing in the markets and saving for retirement above other objectives. However, across all respondents, retirement was at the bottom of the financial goals list for which people felt sufficiently knowledgeable.

Achieving the dream

For generations, part of the American dream has involved homeownership — but purchasing a home involves more than being able to make monthly payments. Acquainting yourself with the homebuying process from start to finish is also vital.

Different types of mortgages have their own additional requirements (e.g., lower debt-to-income ratio; decent credit history). Conventional mortgage loans may require a 20% down payment, while other loans might ask for less money down but require a higher credit score. Understanding these various mortgage guidelines can make purchasing a home much more manageable.

Before they finalize a home purchase, buyers need to consider many factors. Market conditions are a significant component and are subject to the basic principles of supply and demand. The higher the demand, the lower the supply and the higher the price. Nearly 30% of current homeowners who responded said they wished they understood market conditions better prior to buying.

Some current homeowners also wanted to know their debt-to-income ratio calculations, though a higher percentage (39%) of potential homebuyers felt they were sufficiently knowledgeable in this area.

Bankers, credit card companies and mortgage lenders routinely use debt-to-income ratios to determine borrowing limits or monthly payments. When a borrower’s debt total exceeds a certain percentage of their income, lenders start to question the borrower’s ability to pay off the debt promptly. To avoid the potential of repossessing a home, car or other large purchase, lenders carefully consider a borrower’s ability to meet their outstanding obligations.

Generally, mortgage lenders don’t want to see debt-to-income ratios above 41%, and they tend to prefer 28% or lower. To illustrate, suppose a borrower’s gross monthly income is $6,500, and their recurring monthly debt and expenses equal $2,000. In this case, their debt-to-income ratio is 31%.

Interestingly, over 7 in 10 homeowners wished they had more knowledge before starting the house-hunting exercise, and roughly the same number of potential homebuyers said they felt knowledgeable about this topic. One factor in homebuying that can be a challenge is price negotiation — half of homeowners surveyed wished they had mastered better negotiation tactics, with 54% wanting more understanding about financing options.

When looking to fortify your finances in order to buy a house, obtaining an excellent debt-to-income ratio usually means you need to pay down credit card and student loan balances. Forty-six percent of respondents said they reduced or paid off credit card balances, with another 43% stashing more down payment cash away.

Sometimes, lenders recommend refinancing other significant loans, such as auto loans, to improve the chances of securing the right mortgage.

One of the best ways to understand the process is to speak with real estate agents and mortgage lenders, who are knowledgeable about the ins and outs of the homebuying process. Both can help educate potential buyers, especially when it comes to the mortgage application.

Trusted financial sources

Making a major financial decision takes time and research. If you want to buy a house but still feel you have a lot to learn, it can be smart to reach out to more informed sources, like trusted advisors, attorneys, tax professionals, family members and online publications.

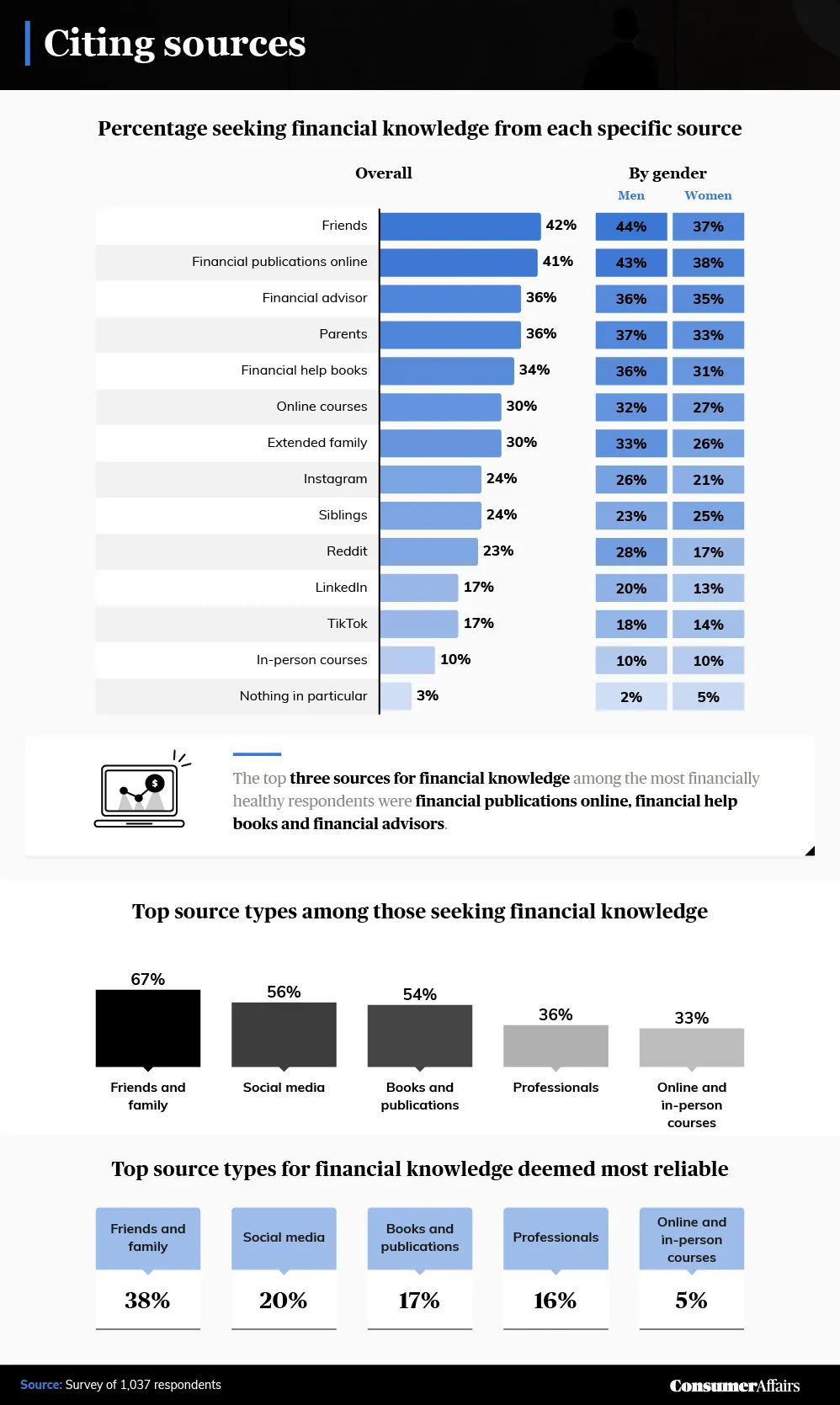

There are plenty of online resources out there to turn to for info on mortgage qualification and savings strategies. Among our respondents, 41% depended on financial websites for this kind of guidance. A slightly higher percentage said they leaned on friends for advice related to spending and saving money (though more men than women confided in friends). According to 36% of respondents, insights from parents and financial advisors were crucial.

Siblings were reported as a source of guidance by 25% of women and 23% of men. Social media platforms, such as Instagram, Reddit, LinkedIn and TikTok, also appealed to a significant percentage of those surveyed.

When it comes to reliability, friends and family ranked highly, with slightly over two-thirds looking to them for money-based knowledge. Social media outlets also ranked well at 20%, with books and financial publications following in popularity.

Finding trusted online sources works well for many. Make sure any financial advice you take relates to your own personal situation, however. For example, you could live in a state with an income tax and work in a neighboring state with a different tax structure. Knowing how income and property are taxed is important — not understanding federal, state and local tax implications can cost extra down the road.

Staying financially focused

Learning financial strategies is important; however, implementing those strategies can be challenging.

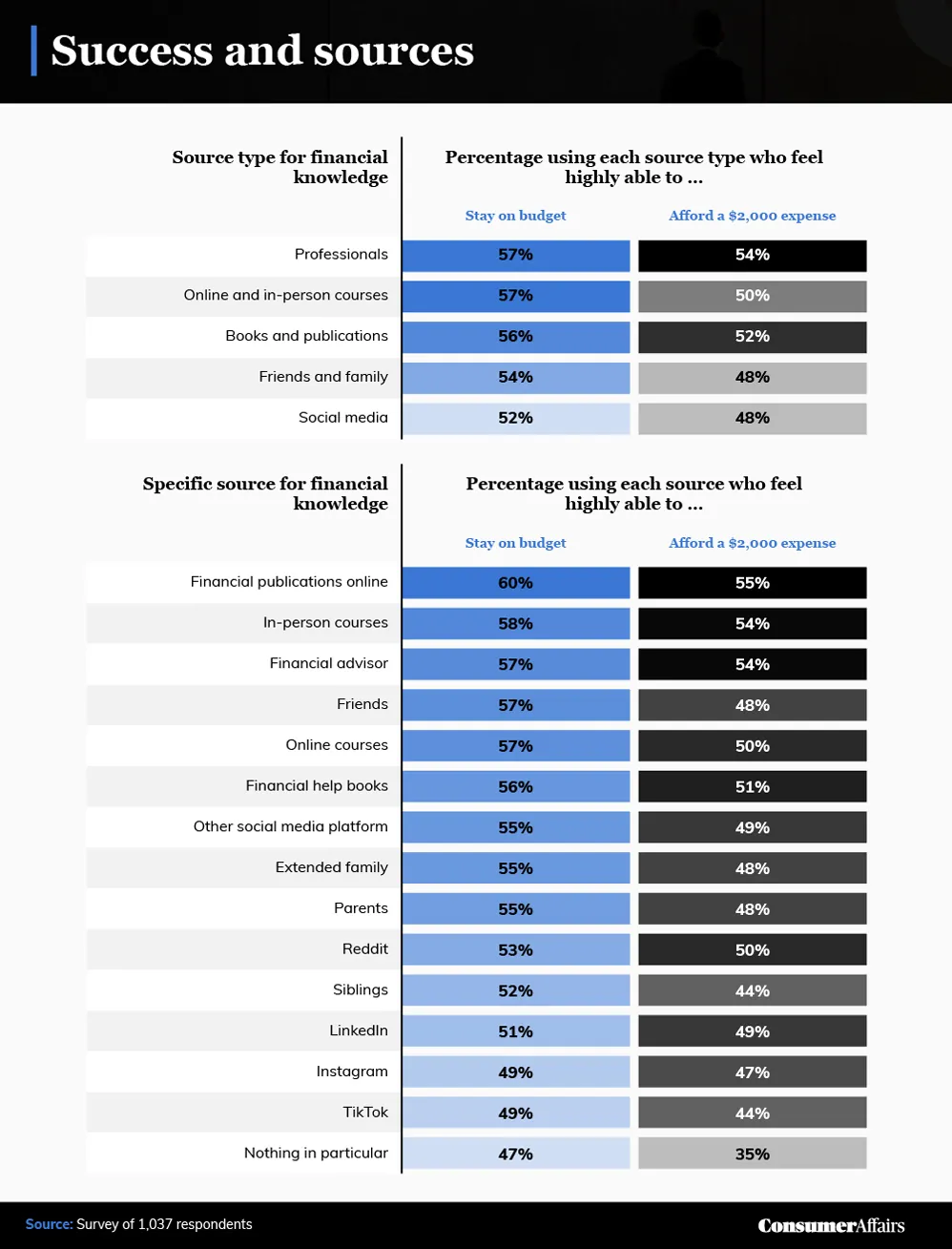

Making and staying on a budget requires discipline and consistency, so how can you stick to one over the long term? According to our data, 6 out of 10 respondents who gained insight from financial publications expressed confidence that they can adhere to a monthly budget, and 55% of the same group felt able to handle a $2,000 expense.

Though many people rely on social media platforms for the latest information, LinkedIn, Instagram and TikTok were the least successful in helping respondents keep within their budgetary confines to meet emergency needs. That’s not to say that Reddit hasn’t played an integral role in the investment landscape over the past 12 months — individuals interested in stock market trends, especially cryptocurrencies, often frequent the online board.

Respondents who relied on professionals (online or elsewhere) were the most likely to stay on budget and be able to meet a $2,000 expense. Respondents who used financial courses and books also seemed to garner confidence in their financial ability.

Financial help is here

Everyone needs financial help at some point. Don’t let the numbers and percentages wear you down, especially if you’re trying to buy a home. One point respondents reinforced in this survey was the need to better understand the homebuying process. Before engaging a real estate agent (or certainly before getting to the closing table), set aside time to study and get to know the real estate market in your area so you have an idea of your best options.

Methodology and limitations

For this analysis, we surveyed 1,037 respondents using the Amazon Mechanical Turk platform. Among those respondents, 623 were men, 410 were women, two were nonbinary and two preferred not to identify their gender. Our respondents ranged in age from 18 to 80 years old, with an average age of 39.

In some cases, questions and answers were rephrased for clarity. To help ensure accurate responses, all respondents were required to identify and answer a decoyed attention-check question.

These results rely on self-reported data. Potential issues with self-reported data include but are not limited to selective memory, telescoping, exaggeration and other attribution errors of respondents.

Fair use statement

Learning financial basics is important to everyone. If you agree and would like to share this info for noncommercial purposes, please be our guest — one simple request is that you link back to the original article to give credit where it’s due.