What percent of student loans are in default? 2026

+1 more

Student loan debt makes up more than 9% of total consumer debt in the U.S., more than any other type of debt outside of mortgages. The total amount of debt owed on student loans now exceeds $1.7 trillion, an amount that has doubled since 2010. Perhaps not surprisingly, as the total amount of student debt has increased, so has the number of borrowers struggling to pay back their loans. Defaults and delinquencies on student loans impact millions of Americans.

Education Department data shows that, as of 2023, a total of 6.8 million federal student loan borrowers had loans in default. This represents 15% of the total number of borrowers.

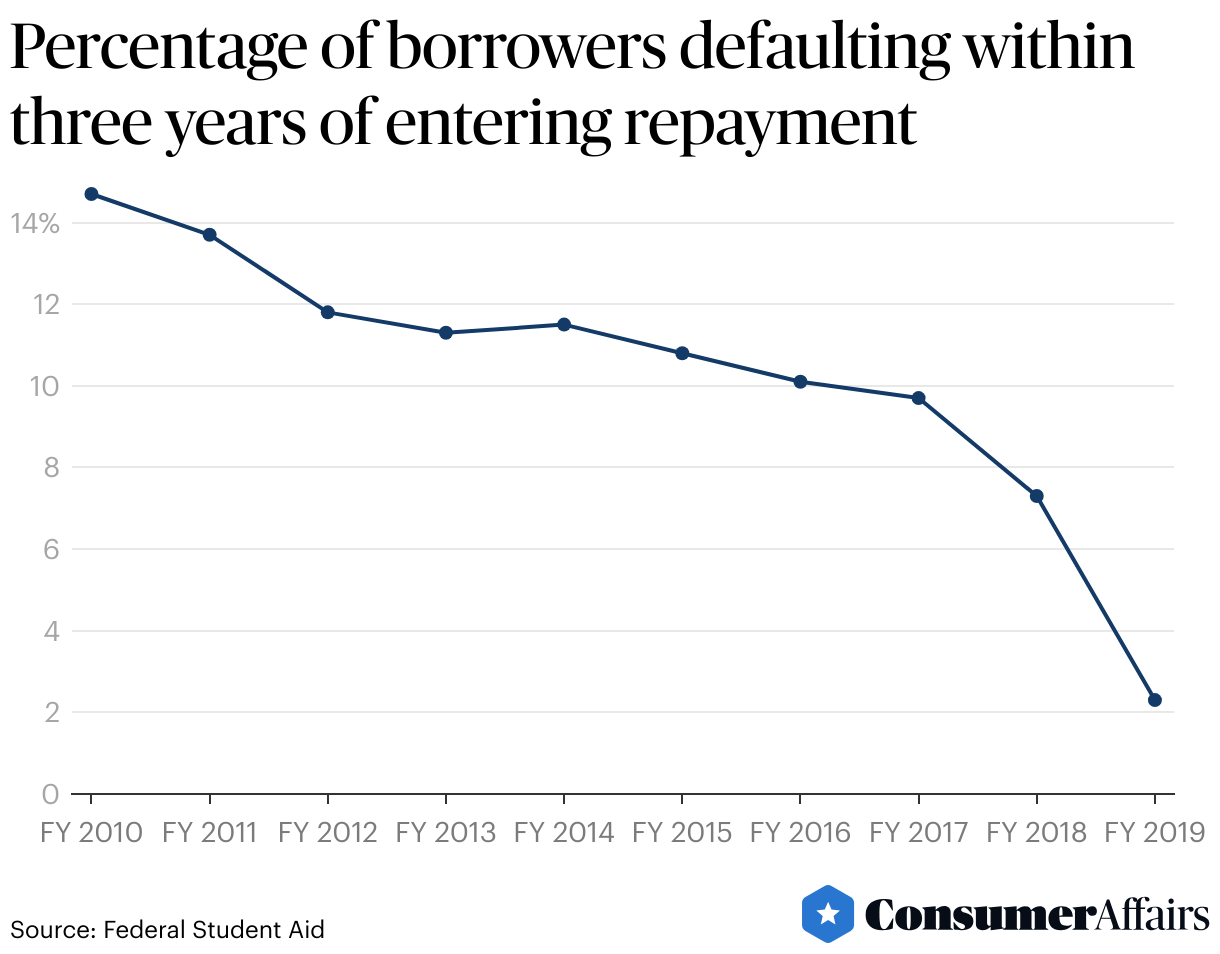

Jump to insightStudent loan forbearance policies have caused a significant drop in student loan default rates, from 14.7% for students who began repaying loans in 2010 to 2.3% for students who began repaying loans in 2019.

Jump to insightStudent loan default can have long-lasting consequences. 13% of borrowers who defaulted on loans have been in default for 20 years or longer.

Jump to insightStudent loan defaults are more common than average among certain demographic groups, including borrowers who are Black or Hispanic, female borrowers, and people who have been widowed, divorced, or separated.

Jump to insightCollege loan default statistics

The federal government considers a student loan delinquent when a payment isn’t made by the due date. That account will remain in delinquency until the borrower repays the past due amount or makes other arrangements, such as a deferment. If a loan is in delinquency for 90 days, the loan servicer reports the borrower to the three national consumer reporting agencies.

Generally, a federal student loan that has been delinquent for at least 270 days is considered to be in default. Some specific loans, such as Perkins Loans, have stricter stipulations—a lender can declare a Perkins loan to be in default as soon as the borrower misses a payment.

The most recent data released by the Education Department showed that, as of 2023, a total of 6.8 million federal student aid borrowers had defaulted loans. This represents 15% of the total number of borrowers.

How common is student loan defaulting?

The student loan default rate is currently on the decline. This decline is due at least in part to student loan forbearance policies enacted during the Covid-19 pandemic. According to the Department of Education, the student loan default rate for students in the FY 2019 cohort is just 2.3%, down from 14.7% for students who were part of the FY 2010 cohort.

Despite these falling numbers, roughly one of every 10 Americans has defaulted on a student loan. Just over 10% of all borrowers default on their loans during the first year of repayment, and one in four borrowers default within the first five years of repayment.

Consequences of a student loan default

Once a loan is in default, the financial consequences can be devastating. The entire amount of the loan becomes due immediately, your income and tax refunds can be garnished, and it can take a significant amount of time to reestablish a positive credit record.

Plenty of borrowers never fully recover from a default. More than 13% of student loan borrowers whose loans are in default have been defaulted for 20 or more years.

| Number of borrowers | % of defaulted borrowers | |

|---|---|---|

| Up to 5 years | 2,507,600 | 34% |

| Between 5 and 9 years | 2,486,100 | 33.7% |

| Between 10 and 19 years | 1,410,000 | 19.1% |

| 20 years or more | 964,900 | 13.1% |

The longer a borrower’s loans have been in default, the more they tend to owe compared to their original student loan balance. For example, borrowers who have been in default for 20 years or more had an average original loan balance of $6,470. The average current balance among these borrowers is $13,695.

| Original loan balance (average) | Current loan balance (average) | Percentage increase | |

|---|---|---|---|

| Up to 5 years | $20,188 | $24,694 | 22% |

| Between 5 and 9 years | $15,468 | $20,734 | 34% |

| Between 10 and 19 years | $14,949 | $21,553 | 44% |

| 20 years or more | $6,470 | $13,695 | 112% |

Student loan default demographics

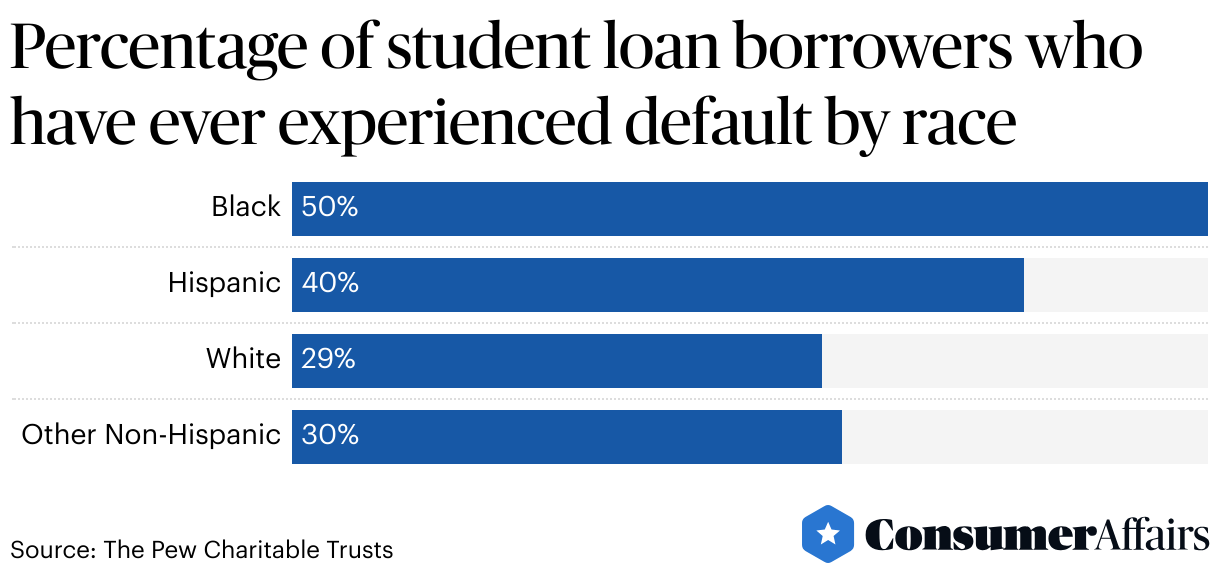

Student loan default rates vary among different demographic groups. A survey conducted by The Pew Charitable Trusts found that defaults were more likely among Black and Hispanic borrowers, female borrowers, those between the ages of 45 and 59, and people who have been widowed, divorced, or separated.

Default rates by ethnicity

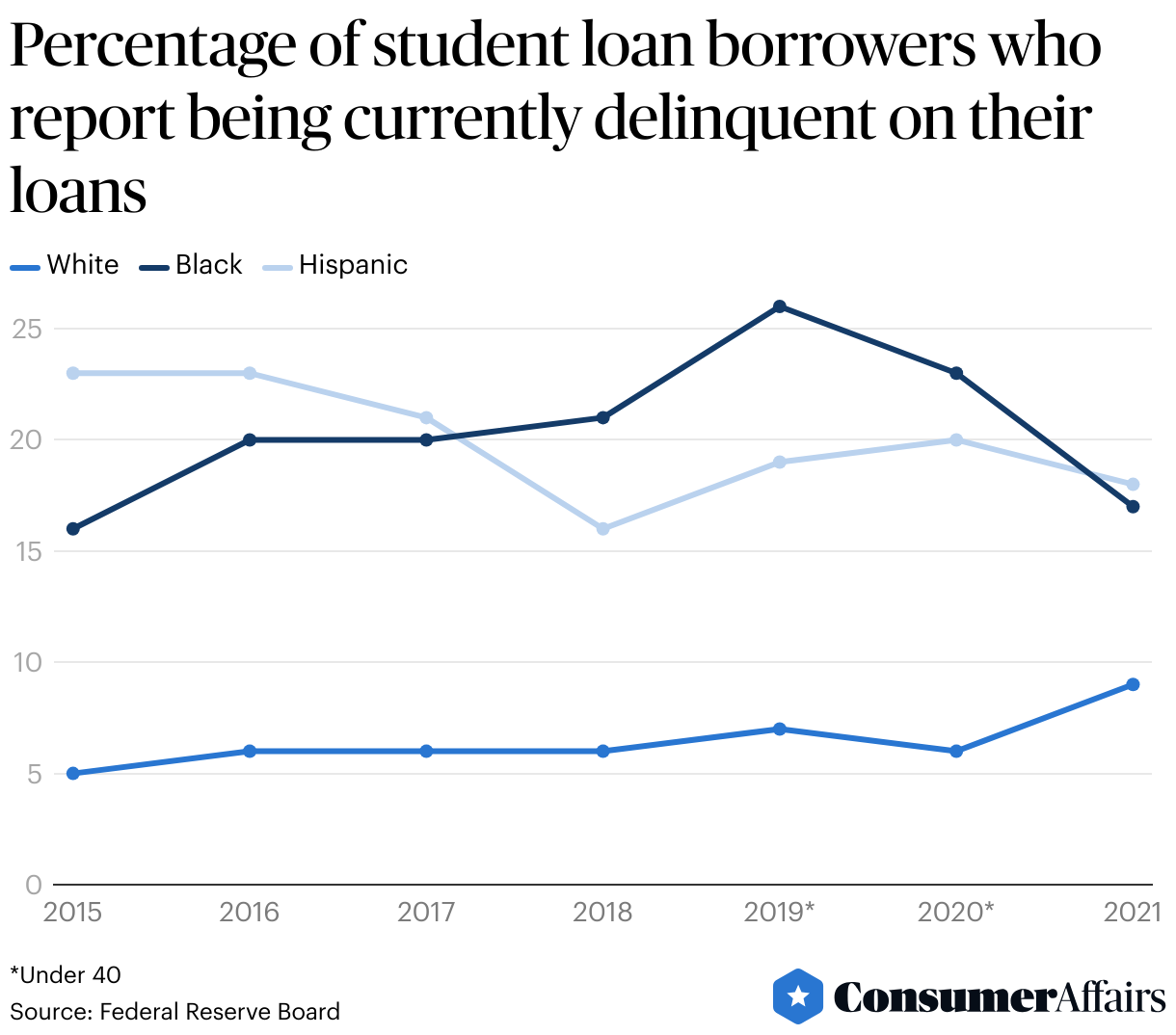

Both default and delinquency rates are higher among Black and Hispanic student loan borrowers than among white borrowers.

In 2021, 9% of white borrowers reported being delinquent on their student loans. While black and Hispanic borrowers reported a delinquency rate nearly double that.

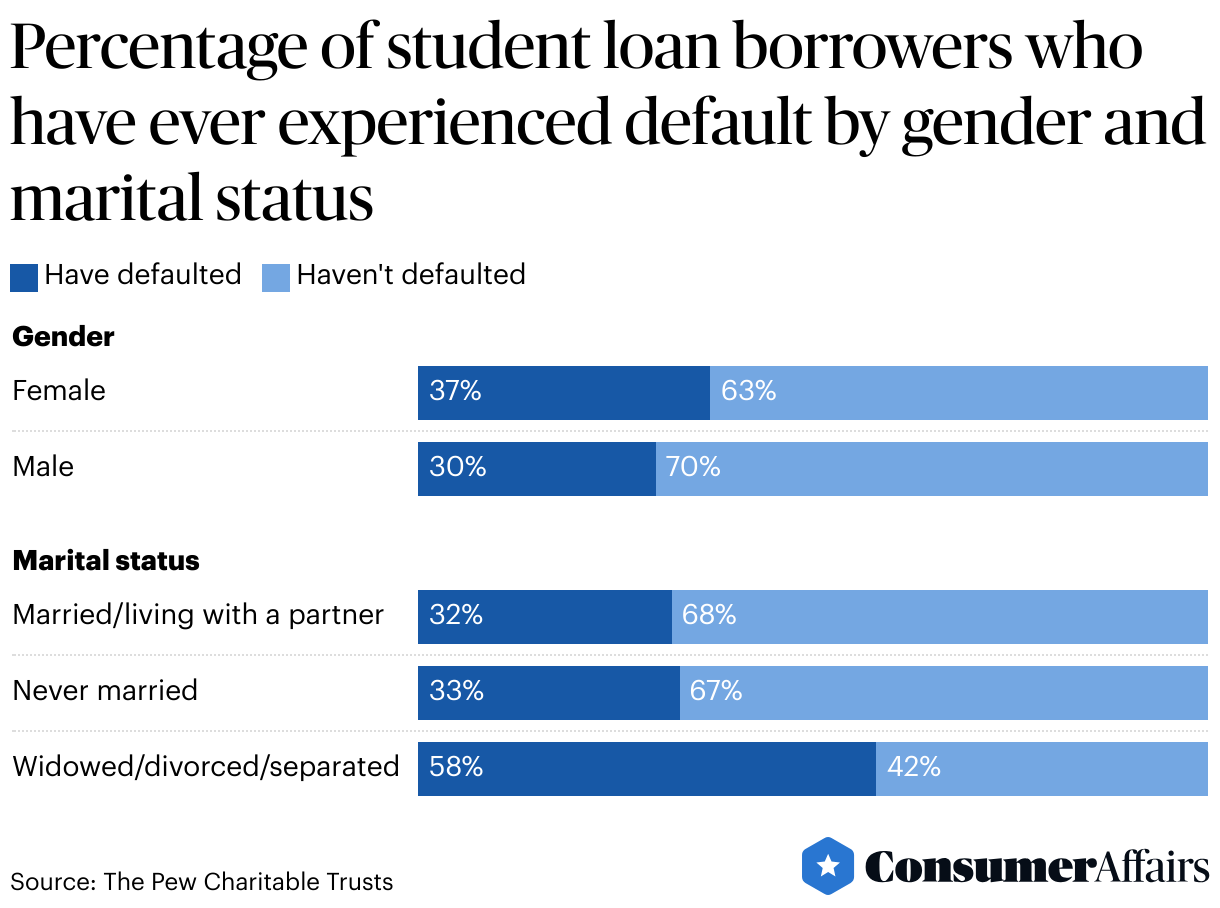

Default rates by gender and marital status

Women hold a disproportionate amount of the total student loan debt, at 66%. They are also more likely than men to have reported defaulting on their loans. Default rates are also higher among individuals who are widowed, divorced, or separated than among people who are currently married, living with a partner, or who have never been married.

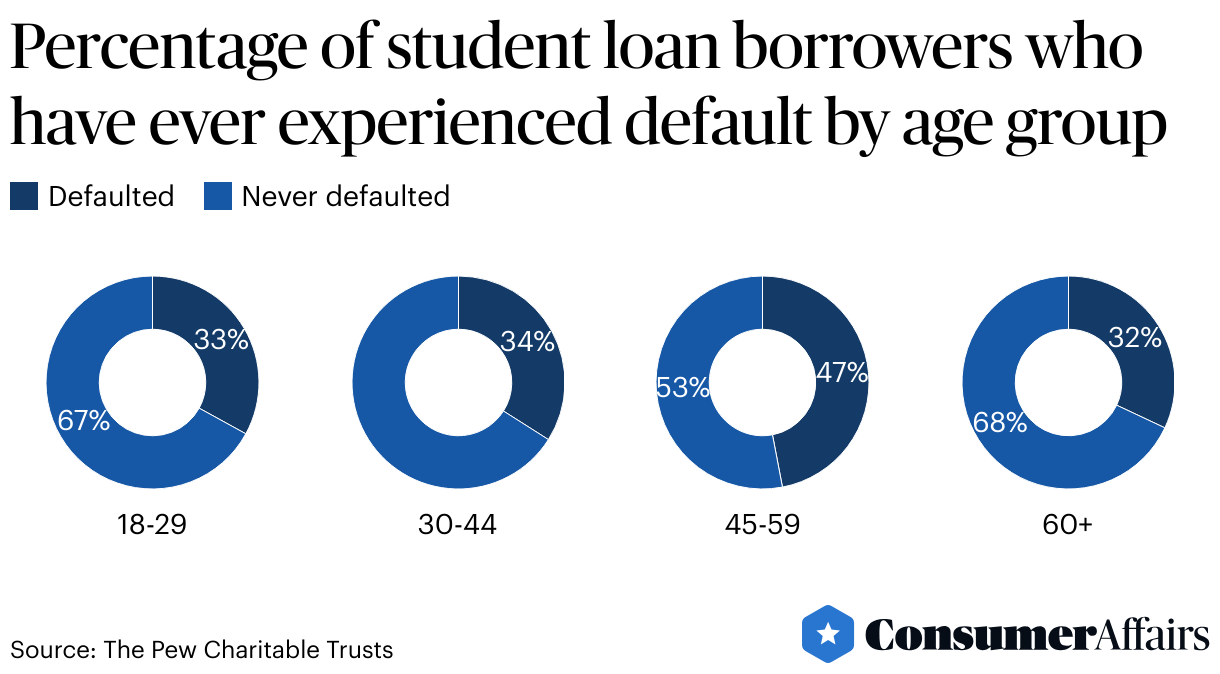

Default rates by age

In terms of raw numbers, there are more student loan borrowers under the age of 30 than in any other age group. However, individuals between the ages of 30 and 39 have higher cumulative student loan balances than other cohorts.

| Number of borrowers (2022) | Cumulative student loan balance | % of total student loan balance | |

|---|---|---|---|

| Under 30 | 14,775,000 | 351,570,000,000 | 22% |

| 30-39 | 12,316,000 | 517,450,000,000 | 32% |

| 40-49 | 7,833.000 | 350,900,000,000 | 22% |

| 50-59 | 5,304,000 | 239,350,000,000 | 15% |

| 60+ | 3,626,000 | 135,470,000,000 | 8% |

Meanwhile, those aged 45 - 59 are most likely to have reported ever defaulting on their loans.

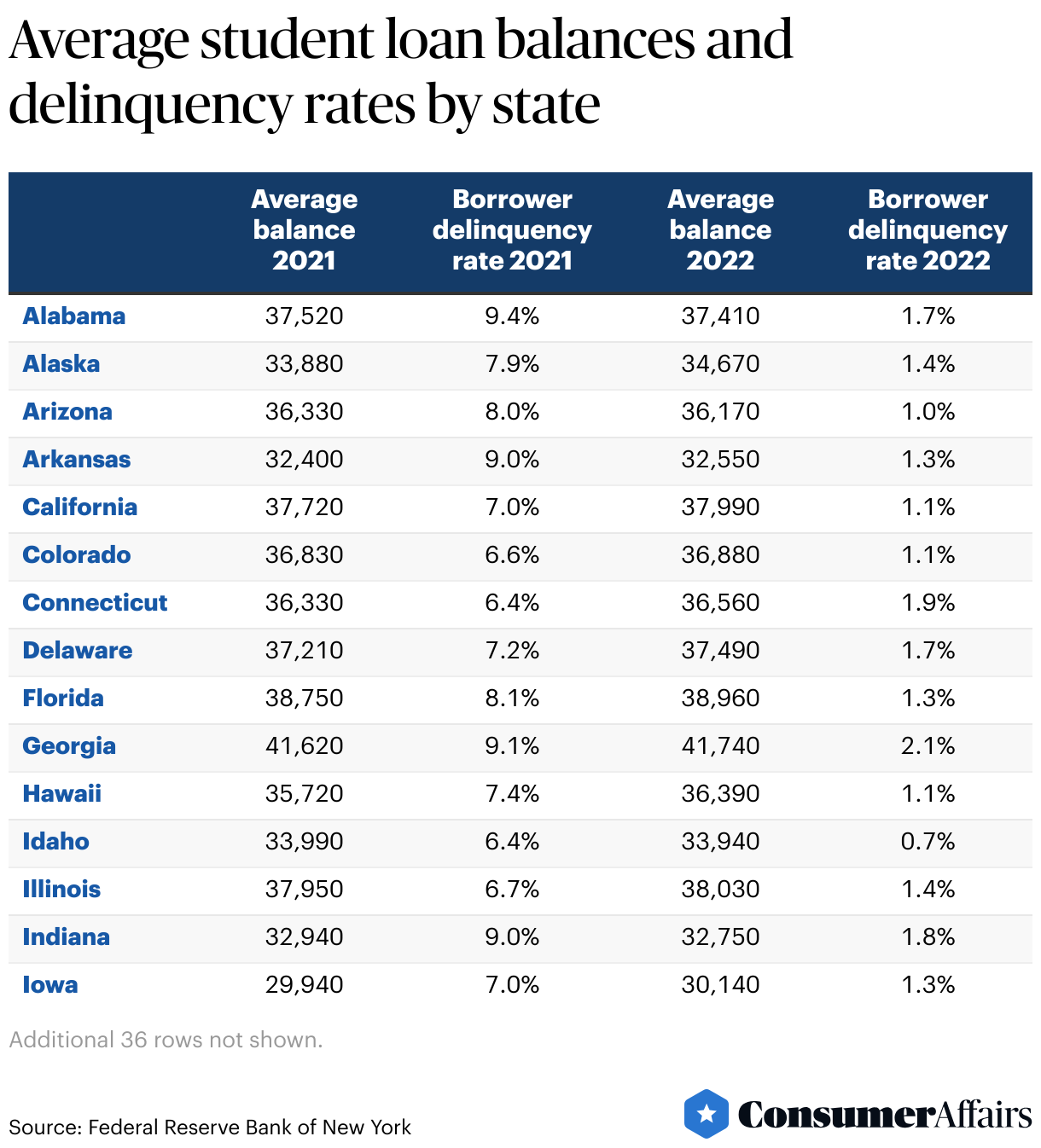

Student loan delinquency rates by state

Student loan delinquency and default rates vary from state to state. At the end of 2021, approximately 10.8% of borrowers in Mississippi were delinquent, while the same was true for only 4.8% of borrowers in New York. Delinquency rates in all states plunged in 2022, likely due to Covid forbearance policies. The graphic below shows average student balances and borrower delinquency rates in each state for 2021 and 2022.

Student loan rates info

The vast majority (91.8%) of student loans are federally funded. Congress sets federal student loan interest rates each year, based chiefly on the yield of the 10-year Treasury note. Interest rates are fixed, meaning that they do not change over the life of the loan.

Interest rates for loans with initial disbursement dates of July 1, 2023, through June 30, 2024, are as follows.

| Type of loan | Interest rate |

|---|---|

| Undergraduate Direct Subsidized and Unsubsidized Loans | 5.50% |

| Graduate Direct Unsubsidized Loans | 7.05% |

| Direct PLUS Loans (parents and graduate or professional students) | 8.05% |

Because student loan interest rates are tied to the value of Treasury notes, these rates change from year to year. Historical rates for undergraduate loans are as follows:

| Disbursement dates | Interest rate |

|---|---|

| 7/1/22 - 6/30/23 | 4.99% |

| 7/1/21 - 6/30/22 | 3.73% |

| 7/1/20 - 6/30/21 | 2.75% |

| 7/1/19 - 6/30/20 | 4.53% |

| 7/1/18 - 6/30/19 | 5.05% |

| 7/1/17 - 6/30/18 | 4.45% |

| 7/1/16 - 6/30/17 | 3.76% |

| 7/1/15 - 6/30/16 | 4.29% |

| 7/1/14 - 6/30/15 | 4.66% |

| 7/1/13 - 6/30/14 | 3.86% |

FAQ

How many people have student loan debt?

Nearly 45 million people in the United States are carrying some federal student loan debt, according to statistics from the Office of Federal Student Aid. Federal student loan debt accounts for nearly 93% of all student loan debt.

How many borrowers are behind on student loan payments?

According to the Federal Reserve’s report on the Economic Well-Being of U.S. Households, 15% of borrowers report being behind on their student loan payments as of 2022.

What happens if you default on a student loan?

For most types of federal student loans, you default if you fail to make payments for 270 days. Defaulting on your student loan has several negative consequences. Your entire loan balance will be due immediately, your default will be reported to credit agencies, negatively affecting your credit score, and you will no longer be eligible for benefits like payment plans or deferments.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Federal Reserve Bank of New York, “Quarterly Report on Household Debt and Credit, 2023: Q4.” Accessed Mar. 20, 2024.

- Federal Reserve Board, “Consumer Credit Outstanding (Levels).” Accessed Mar. 20, 2024.

- Department of Education, “Federal Student Aid Posts New Quarterly Reports to FSA Data Center.” Accessed Mar. 20, 2024.

- Department of Education, “National Default Rate Briefing for FY2020 Official Cohort.” Accessed Mar. 20, 2024.

- US Department of Education, “Data on Borrowers in Default.” Accessed Mar. 20, 2024.

- US Department of Education, “Student Loan Delinquency and Default.” Accessed Mar. 20, 2024.

- Education Data Initiative, “Student Loan Default Rate.” Accessed Mar. 20, 2024.

- The Pew Charitable Trusts, “Student Loan Borrowers With Certain Demographic Characteristics More Likely to Experience Default.” Accessed Mar. 20, 2024.

- Federal Reserve Board, “Report on the Economic Wellbeing of Households, 2015 - 2021.” Accessed Mar. 20, 2024.

- Education Data Initiative, “Student Loan Debt by Gender.” Accessed Mar. 20, 2024.

- Federal Reserve Bank of New York, “2022 Student Loan Debt Statistics (pgs 2 & 3).” Accessed Mar. 20, 2024.

- Federal Reserve Bank of New York, “2022 Student Loan Debt Statistics (pgs 11 & 12).” Accessed Mar. 20, 2024.

- Department of Education, “Interest Rates and Fees for Federal Student Loans.” Accessed Mar. 20, 2024.

- Federal Reserve Board, “Report on the Economic Wellbeing of Households in 2022.” Accessed Mar. 20, 2024.

- Education Data Initiative, “Student Loan Debt Statistics.” Accessed Mar. 20, 2024.

- Department of Education, “Federal Student Aid Portfolio Summary.” Accessed Mar. 20, 2024.

Figures