Student Loan Statistics (2026 Data)

+1 more

In 2023, the total U.S. student loan debt surpassed $1.7 trillion, predominantly comprised of federal student loans, which make up over 92% of the total. This significant increase in educational expenses has made student loans an indispensable component of financing higher education for the majority of Americans. Despite the availability of payment plans and refinancing alternatives, they are proving inadequate, as evidenced by the fact that 10% of Americans have defaulted on their student loans.

U.S. student loan debt reached over $1.7 trillion in 2023.

Jump to insightAmericans aged 35-49 have the highest student loan balances, while Black women have the highest share of student loan debt of all demographics.

Jump to insight10% of Americans have defaulted on a student loan, and 5% of all student loan debt is currently in default.

Jump to insightThe average student loan debt for graduate degrees is nearly triple the $28,400 balance for bachelor’s degree holders.

Jump to insightFrom 2003-2023, the cost of tuition at private universities jumped 40%, and the cost of in-state tuition at public universities skyrocketed 56% when adjusted for inflation.

Jump to insightAverage student loan debt and general student loan statistics

Over the past 10 years, the national student loan balance in the U.S. increased by about 53%, totaling over $1.7 trillion in Q3 2023. In the 2020-2021 academic school year, 54% of bachelor’s degree earners from public and private schools graduated with student loan debt, with an average balance of $29,100.

Student loan debt by gender and race

Black women carry the biggest burden of student loans, both in terms of debt balances and share of those with loans. Black women have higher loan debts than their white and Hispanic/Latino counterparts and are the most likely to have student loan debt of all demographics with a share of 53%.

Fifty-seven percent of black borrowers and 52% of Asian borrowers have outstanding student loan balances of at least $25,000. Only 45% of white borrowers and 39% of Hispanic/Latino borrowers noted the same.

| Demographic | Average student debt | Share with student debt |

|---|---|---|

| White men | $7,700 | 41% |

| White women | $9,600 | 46% |

| Black men | $7,900 | 44% |

| Black women | $11,000 | 53% |

| Hispanic/Latino men | $7,400 | 35% |

| Hispanic/Latino women | $6,700 | 39% |

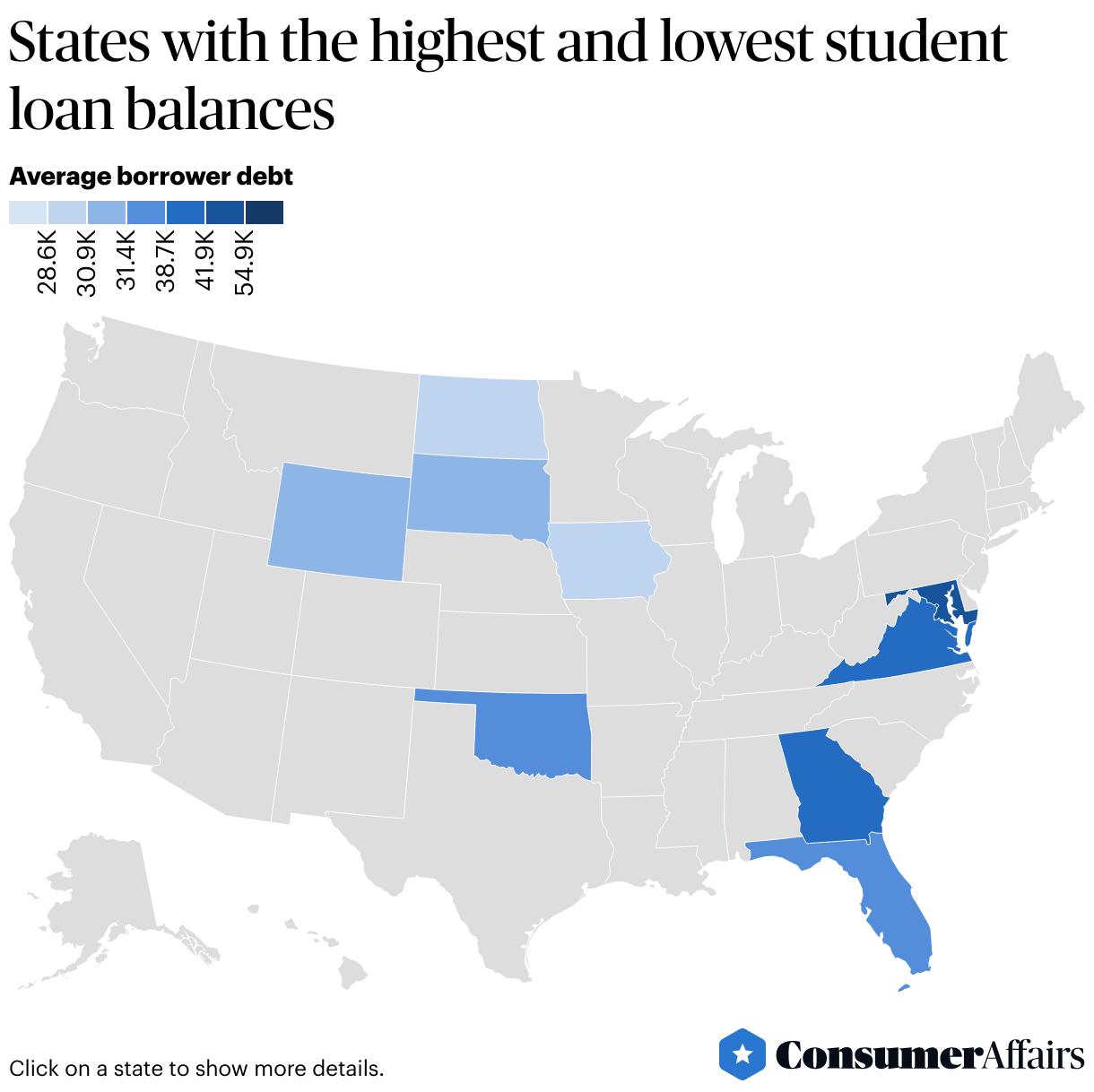

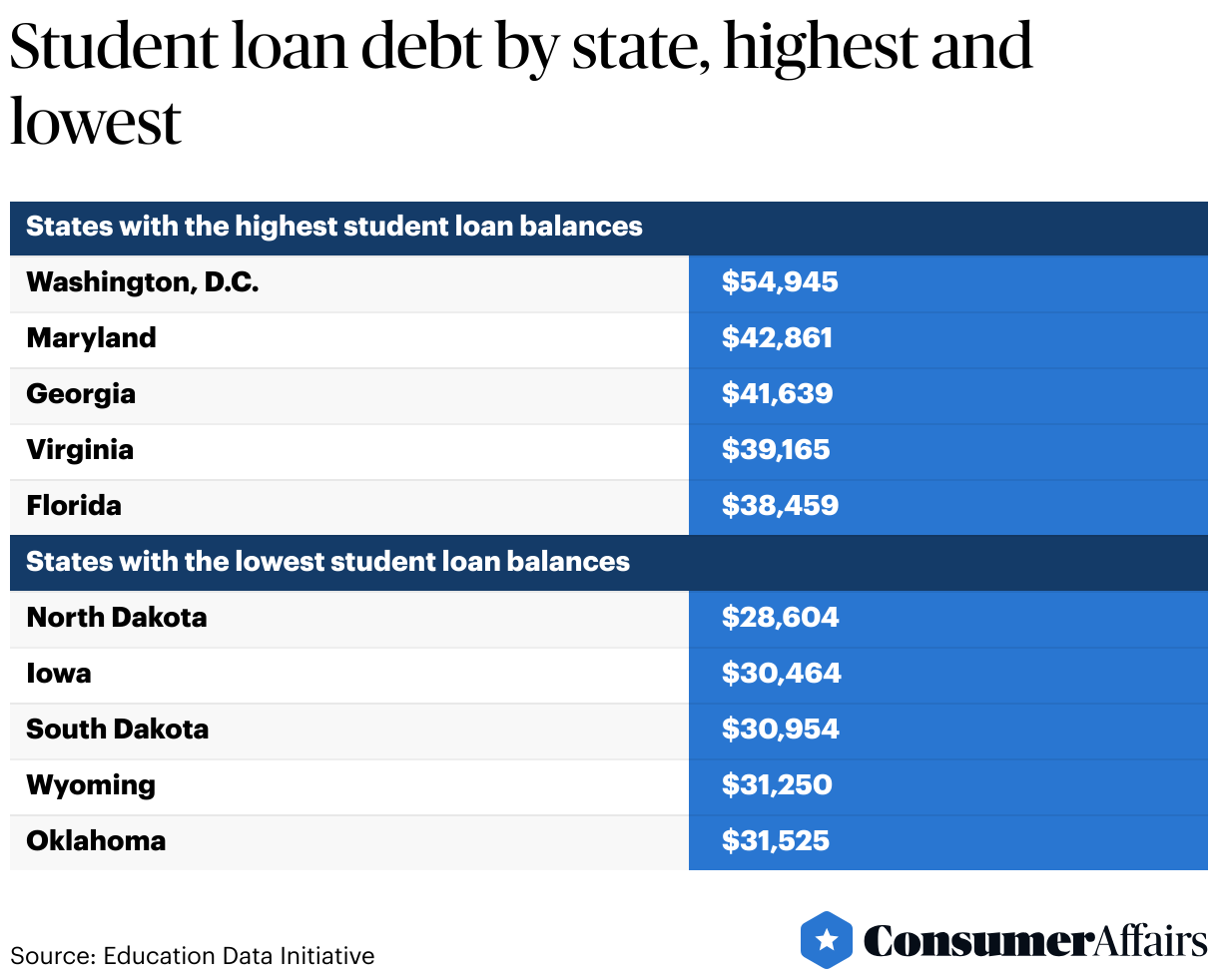

Student loan debt by state

The average student loan debt balance in Washington, D.C., is nearly double the $28,000 of North Dakota. It’s also over $12,000 more than Maryland, the state with the second highest debt balance. This is likely attributed to the high concentration of specialized government jobs requiring graduate-level education and, therefore, more student loans.

States with the lowest student loan balances tend to correlate with agrarian economies, which don’t necessarily require college education and student loan debt.

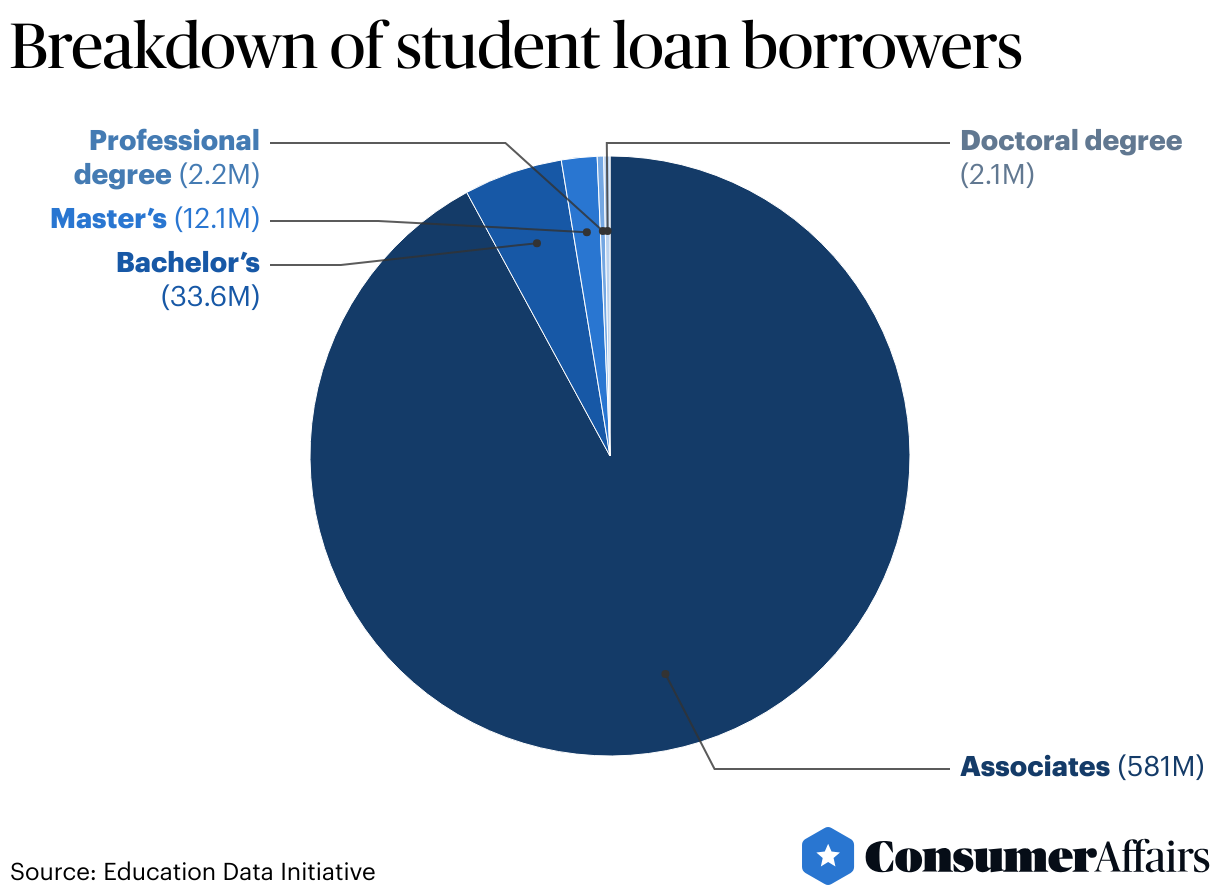

Student loan debt by education level

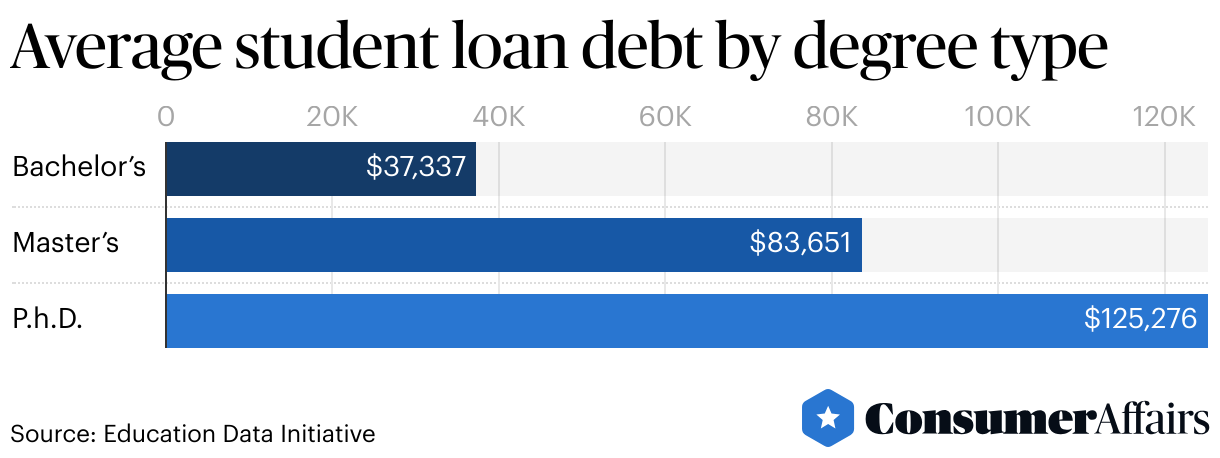

The average student loan debt for graduate degree holders is more than double the $37,337 balance for bachelor’s degree holders. However, 14.3% of graduate borrowers’ debt is from their undergraduate study.

Generally, advanced post-graduate degrees tend to be the most expensive degree but have the lowest concentration of borrowers, likely due to the specialization required. Seventy-one percent of those with graduate degrees and 50% of those with bachelor’s degrees have at least $25,000 in outstanding loan debt.

Student loan debt by age

Student loan borrowers 62 and over have the lowest debt balance, likely offset by older generations not needing college degrees or having more time to pay off their loan balances.

Perhaps somewhat surprisingly, the highest average remaining student loan balance belongs to those ages 35-49, which encompasses both older millennials and Gen Xers.

| Age group | Dollars outstanding (in billions) | Number of borrowers (in millions) |

|---|---|---|

| 24 and younger | $100.1 | 7.1 |

| 25-34 | $491.4 | 15.0 |

| 35-49 | $624.4 | 14.6 |

| 50-61 | $278.5 | 6.3 |

| 62 and older | $109.8 | 2.7 |

Student loan debt by loan type

The most common type of student loans are direct loans — both subsidized and unsubsidized. Direct student loans are typically the most accessible, straightforward, and low-interest option. However, federal direct loans max out at $7,500 per year for undergraduates ($5,500 for freshmen), which often doesn’t cover private university tuition.

| Loan type | Amount outstanding (in billions) | Number of borrowers (in millions) |

|---|---|---|

| Direct subsidized loans (stafford) | $295.6 | 30.6 |

| Direct unsubsidized loans (stafford) | $588.5 | 31.1 |

| Grad PLUS loans | $104.0 | 1.8 |

| Parent PLUS loans | $112.2 | 3.8 |

| Perkins loans | $3.6 | 1.2 |

| Direct consolidation loans | $498.3 | 9.8 |

Student loan repayment status statistics

The average student loan borrower takes 20 years to repay their loan balance, while it may take some professional graduates 45 years or longer to repay their debts. Most borrowers opt to defer loan payments until after they’ve graduated, but there is often an option to pay a nominal amount per month while in school to secure a lower interest rate.

| Quarter/year | Dollars outstanding (in billions) | Recipients (in millions) |

|---|---|---|

| Q1 2023 | $93.1 | 2.68 |

| Q2 2023 | $109.5 | 2.95 |

| Q3 2023 | $95.4 | 2.63 |

| Q4 2023 | $94.8 | 2.67 |

| Q1 2023 | $4.8 | 0.12 |

| Q2 2023 | $4.3 | 0.11 |

| Q3 2023 | $6.9 | 0.14 |

| Q4 2023 | $14.6 | 0.28 |

Student loan debt repayment options

Payment plans reduce the monthly cost to a percentage of the borrower’s discretionary income but can extend the loan term by up to 20 years. The most common payment plans are income-contingent, income-based and pay as you earn. Student loan refinancing options through private lenders pay off student loans with a new private loan with a lower interest rate.

- Income-contingent repayment (ICR): Payments are 20% of a borrower’s discretionary income with forgiveness after 25 years.

- Income-based repayment (IBR): For loans taken out starting July 1, 2014, payments are 10% of a borrower’s discretionary income with forgiveness after 20 years. For loans taken out before July 1, 2014, payments are 15% of a borrower’s discretionary income with forgiveness after 25 years.

- Pay As You Earn (PAYE): Loan payments are 10% of a borrower’s discretionary income with loan forgiveness after 20 years.

| Dollars outstanding (in billions) | Recipients (in millions) | |

|---|---|---|

| Q1 2018 | $27.7 | 0.63 |

| Q1 2019 | $30.9 | 0.68 |

| Q1 2020 | $34.5 | 0.72 |

| Q1 2021 | $36.3 | 0.75 |

| Q1 2022 | $37.8 | 0.78 |

| Q1 2023 | $39.4 | 0.82 |

| Q1 2018 | $169.0 | 2.91 |

| Q1 2019 | $169.8 | 2.82 |

| Q1 2020 | $171.9 | 2.76 |

| Q1 2021 | $173.2 | 2.77 |

| Q1 2022 | $171.8 | 2.75 |

| Q1 2023 | $165.6 | 2.65 |

| Q1 2018 | $68.3 | 1.19 |

| Q1 2019 | $85.3 | 1.31 |

| Q1 2020 | $103.5 | 1.44 |

| Q1 2021 | $109.8 | 1.5 |

| Q1 2022 | $112.5 | 1.52 |

| Q1 2023 | $113.1 | 1.52 |

Student loan debt delinquencies and defaults

If a borrower is unable to make a loan payment, there is a 30- to 90-day grace period before the loan becomes delinquent, or past due. After 270 days of delinquent payments, student loans go into default, after which the loan is due in its entirety.

Ten percent of Americans have defaulted on a student loan, and 5% of all student loan debt is currently in default. Defaulted loans have detrimental long-term effects, including destroyed credit scores and withheld wages, tax refunds and Social Security benefits and could prevent borrowers from receiving loan aid in the future.

From Q3-2020 to Q3 2023, there were not any delinquent public student loans in the U.S. due to changes to the CARES Act in March 2020, which moved borrowers’ balance into forbearance. During Q2 2020, $31.6 billion in loans were 31-90 days delinquent. Due to the federal student loan freeze ending September 1, 2023, Q1 2024 may likely see a drastic uptick in loan delinquencies.

When student loan payments resumed as of September 1, 2023, only 60% of borrowers had made the necessary loan payments by mid-November 2023. However, less than 1% of aggregate student loan debt was at least 90 days delinquent or in default, and default rates are expected to remain low through Q4 2024, which is when defaulted loans will next be reported to U.S. credit bureaus.

The majority of those in loan default are Pell Grant recipients (67%) and those who hadn’t completed their degree or program (62%). Graduate students only accounted for 3.5% of those in loan default as of September 2021.

FAQ

What is the average debt for a 4-year degree?

The average student loan debt balance for a 4-year degree is $34,700.

Who has the most student loan debt?

Borrowers between 35-49 have the most debt, totaling nearly $636 billion.

How can federal student loans be forgiven?

The Public Service Loan Forgiveness Program forgives all student loans not paid off after 120 payments (10 years) have been made while working for federal, state or local government agencies.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Federal Reserve Board, “Consumer Credit Outstanding (Levels).” Accessed Jan. 24, 2024.

- The College Board, “Trends in College Pricing and Student Aid 2022.” Accessed Jan. 24, 2024.

- Federal Reserve Bank of St. Louis, “Gender and Racial Disparities in Student Loan Debt.” Accessed Jan. 25, 2024.

- Education Data Initiative, “Student Loan Debt by State.” Accessed Jan. 25, 2024.

- Education Data Initiative, “Indebted Student Loan Borrowers by Education Level.” Accessed Jan. 25, 2024.

- Education Data Initiative, “Average Graduate Student Loan Debt.” Accessed Feb. 1, 2024.

- Education Data Initiative, “Student Loan Age by Age.” Accessed Jan. 25, 2024.

- Federal Student Aid, “Federal Student Loan Portfolio.” Accessed Jan. 28, 2024.

- CNBC, “What happens when you default on a loan? These tips will help you avoid finding out.” Accessed Jan. 28, 2024.

- CNBC, “Only 60% of student loan borrowers made payments when bills restarted.” Accessed Jan. 28, 2024.

- Consumer Financial Protection Bureau, “Choosing a loan that’s right for you.” Accessed Jan. 28, 2024.

- New York Federal Reserve Bank, “Center for Microeconomic Data.” Accessed Jan. 31, 2024.

- Education Data Initiative, “Student Loan Default Rate.” Accessed Jan. 29, 2024.

- Education Data Initiative, “Average Time to Repay Student Loans.” Accessed Jan. 29, 2024.

- Federal Reserve Board, “Report on the Economic Well-Being of U.S. Households in 2022 - May 2023.” Accessed Jan. 29, 2024.

Figures