Medicare Statistics (2026 Data)

+1 more

Medicare for all? The contemporary debate, along with the current structure of Medicare, is rooted in the early 20th century. Pressure from various stakeholders and the subsequent growth of employer-based health coverage ended the effort to enact a national health insurance program, transforming it into one providing health coverage for the elderly.

In August of 1960, on the 25th anniversary of the signing of the Social Security Act, Senator John F. Kennedy, then seeking the U.S. presidency, made a pitch for a national program of senior health care. It was needed, he said, in “every city and town, every hospital and clinic, every neighborhood and rest home in America — wherever our older citizens live out their lives in want and despair under the shadow of illness.” Kennedy expounded upon the following:

- A population of 16 million Americans past the age of 65

- Three-fifths of that population — 9.5 million seniors — with an income of less than $1,000 a year

- Skyrocketing medical costs consuming from 25% to 50% of the annual income of almost 20% of Social Security recipients

- A senior population experiencing chronic diseases at almost twice the rate of younger people and who needed to see a doctor twice as often

Kennedy did not see his program realized during the abbreviated term of his office. That achievement fell to Lyndon Johnson, who took up the slain president’s Medicare agenda and, in July of 1965, signed the bill that led to today’s Medicare and Medicaid programs. Coverage was offered to those ages 65 and older without health insurance. The original Medicare program included hospital insurance (Part A) and medical insurance (Part B). Together, these two parts are now termed “Original Medicare.”

Congress has since expanded Medicare by extending eligibility and covering additional medical conditions. In 1972, people receiving Social Security disability benefits were added, as well as people with end-stage renal disease requiring dialysis or kidney transplant. In 1982, legislation added hospice coverage for the terminally ill. Medigap, also called Medicare supplement insurance, has been available since Medicare’s inception, to cover out-of-pocket costs that Original Medicare does not include. Legislation in 1990 standardized the structure of Medigap plans. There is no cap on Original Medicare out-of-pocket costs, hence the need for supplemental coverage.

The Medicare Prescription Drug Improvement and Modernization Act (MMA) of 20036 made two big changes to Medicare. It added the option to join a private health plan — called a Part C Medicare Advantage (MA) Plan — approved by and offered in partnership with Medicare. The legislation also added an optional outpatient prescription drug benefit that went into effect in 2006 and is referred to as Part D.

Medicare is paid for through two dedicated U.S. Treasury trust fund accounts: the Hospital Insurance (HI) Trust Fund and the Supplementary Medical Insurance (SMI) Trust Fund. The governing board that oversees these trusts reports annually to Congress regarding HI and SMI financial health.

Medicare’s four parts are financed as follows:

- Part A: through payroll taxes on current workers and their employers, credited to the HI trust fund

- Part B: through current enrollees’ monthly premiums plus general revenues, credited to the SMI trust fund

- Part C: through current enrollees’ monthly premiums plus payments made to the participating private plans drawn from the Medicare HI and SMI trust funds

- Part D: through a separate account in the SMI trust fund financed through general revenues, state contributions and beneficiary premiums

The HI trust fund has faced a projected shortfall almost from its inception. The insolvency date has been frequently postponed, most recently to 2031, one year after the program itself matures into older adulthood.

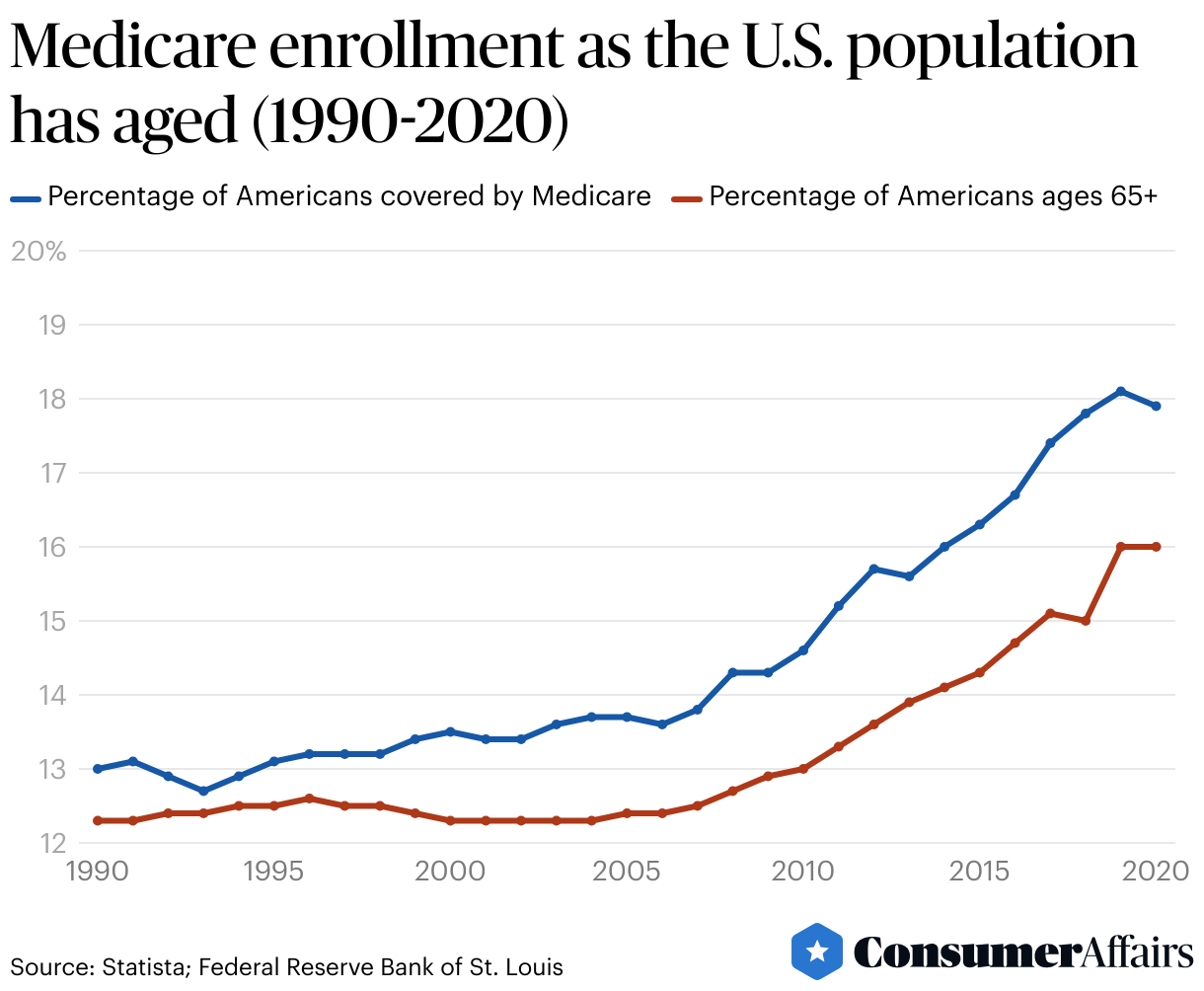

Medicare began in 1966 with coverage for just under 19.1 million adults ages 65 and older, or roughly 9.6% of the U.S. population. In the years since its inception, the program has grown to cover 66.4 million people, 7.4 million of whom are younger than 65 and qualify because of disability.

Jump to insightThe oldest of the baby boom generation, those born from 1946 through 1964, turned 65 in 2011. Medicare enrollment began climbing that year, and the number of Americans ages 65-plus is projected to reach 82 million by 2050.

Jump to insightMedicare enrollees have two primary choices: coverage under Parts A and B of Original Medicare or coverage with a government-approved MA plan issued by a private insurer in conjunction with the Centers for Medicare & Medicaid Services (CMS). Those listed as having MA and other plan enrollment have increased over time and, as of March 2024, account for 48.49% of all enrollees.

Jump to insightOut-of-pocket costs are not capped in Original Medicare, and coverage for prescription drugs is not included. Most Original Medicare enrollees purchase separate policies to cover these costs, but over 3 million people (10% of those covered by Original Medicare) did not have this coverage in 2021. MA plans are required to provide an out-of-pocket cap.

Jump to insightAs of 2024, there are 3,959 MA plans generally available for individual enrollment. The number of plans from which to choose varies by location. Fewer choices are available in rural areas, for example, while there are some locations where MA plans are not at all available.

Jump to insightPrivate insurance companies offer MA plans, and 10 companies nationwide dominate the marketplace. Many Medicare-eligible people find the selection and enrollment process complicated.

Jump to insightAs the eligible population grows and health care costs increase, Medicare expenditures are forecast to reach 18% of the U.S. budget by 2032. Sustaining the program into the future will demand much thought and deliberation among all stakeholders.

Jump to insightMedicare statistics

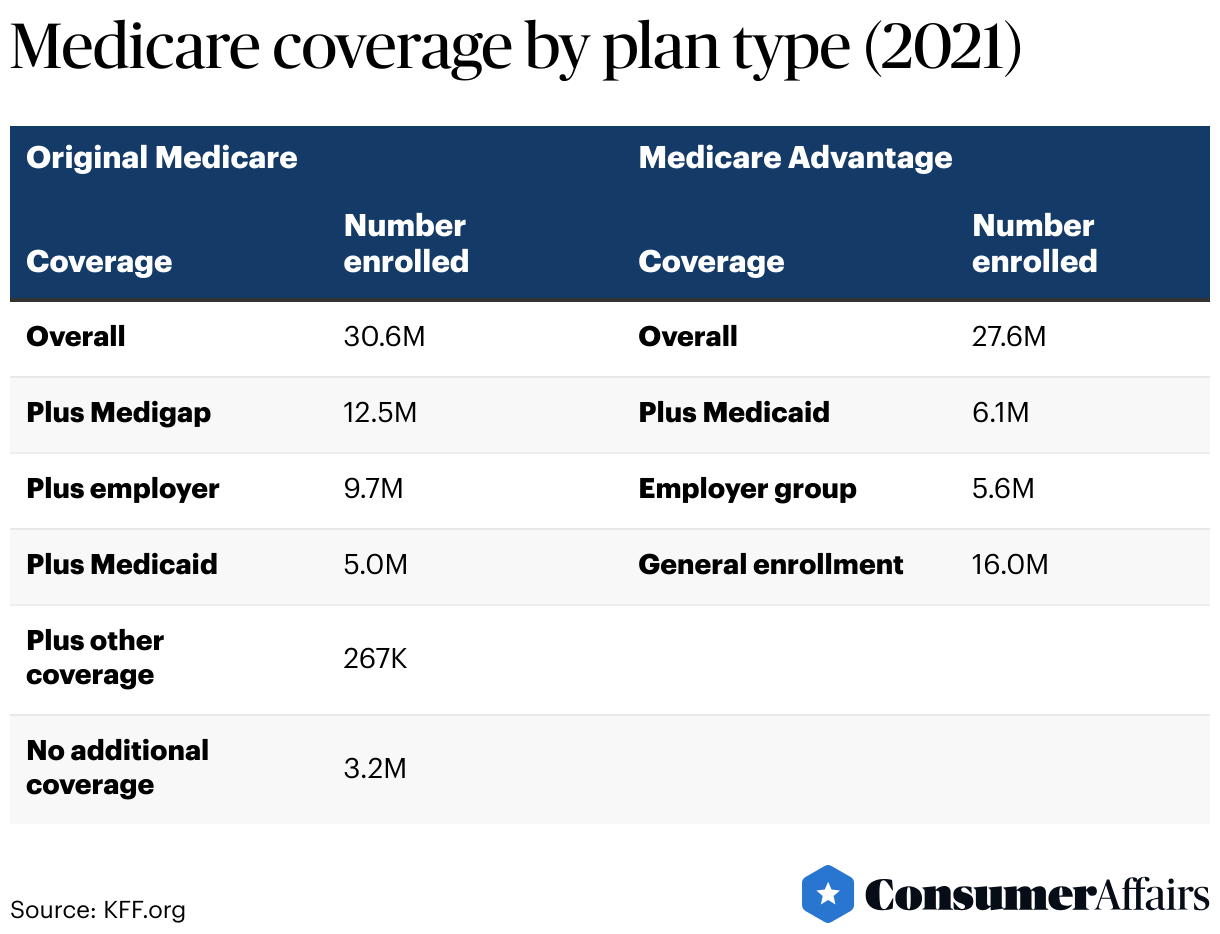

According to the most recent data published by the CMS, 66.4 million people, or about 19.7%10 of the U.S. population, are covered by Medicare Parts A and/or B. Of those, 34.2 million are enrolled in Original Medicare, and 32.2 million, or 48.49% of total enrollees, are listed among those with MA and other plan enrollment.

How many Americans are covered by Medicare?

At its inception in 1966, Medicare covered just under 19.1 million individuals ages 65 and older, and roughly 9.6% of the country’s population fell into that age group. Those figures have generally increased quite steadily with time, program changes and the general aging of the population.

Born in 1946, the oldest of the baby boomer generation turned 65 in 2011. The Medicare enrollment trend line begins a generally steeper ascent at that point. The census showed nearly 16% of the U.S. population (55.8 million people) were 65 and older in 2020 and, thus, eligible for Medicare. This figure is projected to rise to 82 million by 2050 and the group’s population share to reach 23%.

Original Medicare coverage types

In 2021, most people enrolled in Original Medicare had some form of additional coverage — Medicaid, retiree health benefits and Medigap are examples — but over 3 million Medicare beneficiaries (nearly 5.5% of all beneficiaries and 10.5% of those with Original Medicare) had no additional coverage.

Enrollees in Original Medicare without additional coverage are fully responsible for Medicare’s cost-sharing requirements. In 2024, those requirements are as follows:

- Inpatient hospital deductible: $1,632

- Daily hospital stay coinsurance for days 61 through 90: $408

- Daily hospital stay coinsurance for lifetime reserve days up to day 150: $816

- Daily hospital stay beyond 150 days: full cost

- Daily coinsurance at a skilled nursing facility for days 21 through 100: $20440

- Monthly premium for Part B services: $174.70

- Physician visits and other outpatient services: $240 deductible plus 20% coinsurance after the deductible is paid

Original Medicare enrollees have no cap on their out-of-pocket spending for Parts A and B services.

The number of Medicare beneficiaries without supplemental coverage declined from 5.6 million enrollees in 2018 to 3.2 million in 2021, possibly due to the steady increase in people choosing MA plans. That said, those still covered by Original Medicare but without additional coverage remain particularly vulnerable because they are more likely to:

- Self-report fair or poor health that may need more frequent or costly medical services (23% compared to 19% of all of those covered by Original Medicare)

- Be under the age of 65 and therefore covered by Medicare as a result of disability

- Have annual incomes between $10,000 and $40,000, limiting their ability to afford Medigap premiums but with income and assets too high to be Medicaid-eligible

Medicare demographics statistics

According to the most recent statistics available, demographics among Original Medicare enrollees vary somewhat when grouped by supplemental coverage sources.

Medigap

Of all people enrolled in Original Medicare in 2021, nearly 12.5 million, or 41%, had Medicare supplemental insurance (Medigap) policies.

These policies are sold by private insurance companies. Ten types, designated by the letters A-D, F, G and K-N, are available in most states (in Massachusetts, Minnesota and Wisconsin, the plans are standardized differently). Benefits are the same among all plans of a specific type. Monthly premiums, however, vary widely: A person’s age at the time of plan purchase, health status (preexisting medical conditions), tobacco use, geographic location and the insurance company issuing the coverage may all be determinants. Consumers are urged to compare specifics before selecting a plan.

Among 2021 Medicare beneficiaries, 91% of those with a Medigap policy were white, compared to 82% overall. Medigap policyholders were also more likely to:

- Have annual incomes $20,000 or above per person (85% compared to 74% overall)

- Self-report good to excellent health (87% compared to 81% overall)

- Hold a bachelor’s degree or higher (42% compared to 36% overall)

Employer

Employer- or union-sponsored health insurance plans are another way some Original Medicare beneficiaries can mitigate out-of-pocket health care costs.

Of the 30.6 million people with Original Medicare in 2021, nearly 9.7 million, or 31.7%, had employer- or union-sponsored coverage in addition to traditional Medicare. Compared to all of those with Original Medicare, this group was similar in ethnicity but more likely to:

- Have annual incomes $40,000 or over per person (62% compared to 43% overall)

- Self-report good to excellent health (87% compared to 81% overall)

- Hold a bachelor’s degree or higher (47% compared to 36% overall)

Medicaid

Medicaid is a joint federal and state program that helps pay medical costs for people with limited income and resources. It may provide for services that are not covered or only partially covered by Medicare. Rules vary from state to state. People who qualify under both programs are termed “dual-eligibles.”

In 2021, about 5 million people enrolled in Original Medicare received additional benefits through Medicaid. Compared to the entire cohort of 2021 Original Medicare enrollees, dual-eligible individuals were more likely to:

- Be under the age of 65 (45% compared to 12% overall)

- Have incomes less than $20,000 (84% compared to 26% overall)

- Have no more than a high school or GED diploma (65% compared to 33% overall)

- Identify as Black or Hispanic (34% compared to 13% overall)

Medicare Advantage plans

Medicare Advantage (MA) is a private plan alternative to traditional Medicare that has become increasingly popular over the last quarter century. It provides that private health insurance companies receive federal monies to furnish Medicare-covered services for Medicare enrollees who select an MA plan. The CMS has reported a steady increase in those listed as having MA and other plan enrollment since 2004, from 5.3 million people, or 12.8% of the 41.4 million enrollees, to 32.2 million, or 48.49% of Medicare participants enrolled in Parts A and/or B, as of March 2024.

MA enrollment is projected to reach 60% of all Medicare participants by the end of the decade. Among the factors contributing to this growth are the following:

- Simplicity and convenience: Coverage is provided in a single plan — there is no need for supplemental (Medigap) or separate prescription (Part D) drug coverage.

- Attractive benefits: Insurers receive higher payments relative to those in Original Medicare, allowing them to offer enrollees such items as dental coverage, gym memberships, debit cards for over-the-counter medical supplies and other health-related benefits that are not covered by traditional Medicare.

- Financial security: MA plans require a cap on annual out-of-pocket costs, so enrollees know the upper limit of their out-of-pocket responsibilities.

- Employer interest: Shifting to MA retiree benefit plans may simplify employee benefits administration and reduce overall employer costs.

- Industry incentives: The higher gross margins — a rough measure of profitability — and broker commissions associated with MA have resulted in intensive marketing efforts.

MA plans are of several types. The vast majority are open to general enrollment and fall under one of the following:

- Health Maintenance Organizations (HMOs), offering care by in-network doctors, hospitals and other providers

- Preferred Provider Organizations (PPOs), offering care by in-network providers or via out-of-network providers at a higher cost. The network may be local (restricted to a small service area like a single county) or regional (serving a much larger government-defined geographic area).

- Private Fee-for-Service plans (PFFs), not commonly offered, wherein the insurer agrees to pay a set amount for each type of medical treatment. Providers may be in-network or outside the network. Those outside must agree to provide care at the set rate.

Other plans have restricted enrollment. Among them are the following:

- Employer Group Waiver Plans (EGWPs), offered by employers to retirees

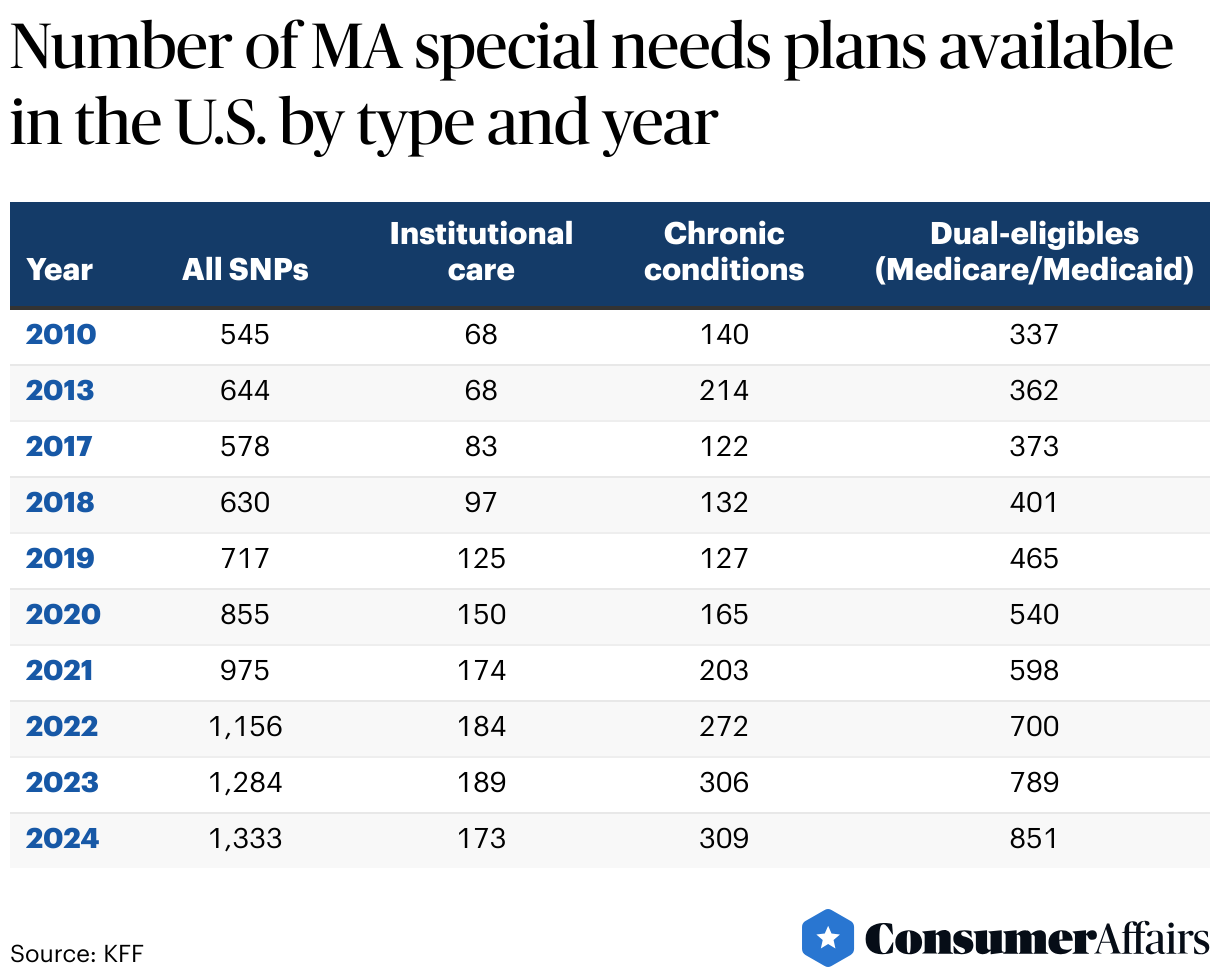

- Special Needs Plans (SNPs), designed for people with high health care needs, including Medicare/Medicaid dual-eligibles, people with specific chronic conditions or those requiring institutional care

How many Medicare companies are there?

The annual Medicare open enrollment period runs from October 14 to December 7, with advertising permitted beginning October 1. During this period, Medicare beneficiaries can compare and switch their coverage choices. Enrollees can find the process confusing with the annual advertising blitz compounding the difficulty.

A review of 2022 Medicare enrollment advertising counted over 1,200 unique television ads that aired more than 643,000 times. More than 85% of the ads were for MA plans. Most of the remaining ads pertained to prescription drug plans and Medigap supplements. Few mentioned the availability of Original Medicare or referred to government resources. The majority of telephone hotline numbers provided promoted private industry sources rather than official Medicare helplines or impartial state government insurance counseling. Participants often sought assistance from brokers and ignored potential financial incentives to enroll them in particular plans.

There are 3,959 MA plans available nationwide for individual enrollment in 2024. That number excludes plans like employer and special needs groups with specific enrollment requirements. This is a 1% decrease from the number of plans offered in 2023 but still larger than any other year since 2010.

The number of available plans varies geographically. In 2024, the following holds true:

- The average person has 43 MA plans from which to choose.

- A third of Medicare beneficiaries have more than 50 MA plan choices.

- MA plan choices for those living in urban areas average 47.

- Choices for those living in rural areas average 27 MA plans.

- The roughly 94,000 Medicare beneficiaries living anywhere in Alaska have no access to an MA plan option. Some counties in states like Colorado, Idaho, Montana, Nebraska, Nevada, Oregon, South Dakota and all U.S. territories other than Puerto Rico are similarly unserved by the MA marketplace.

Nationwide, 56% of all 2024 MA plans are HMOs, but that share of the market has declined from 71% in 2017 in favor of local PPOs, which had only 24% of the MA plan market in that year and now constitute 42% of MA plans.

Among plans with restricted enrollment, MA plans are an increasingly popular choice among the small percentage of employers with 200 or more workers who offer health benefits to retirees. In 2023, 52% of these employers provided benefits through MA, up from 26% in 2017.

As seen in the table below, the number of MA special needs plans has also been rising steadily in recent years.

The number of Medicare Advantage SNPs has increased every year since 2017, with the largest increase in those plans for dual-eligible beneficiaries. The total number of SNPs in 2024 more than doubled from six years prior.

Medicare spending

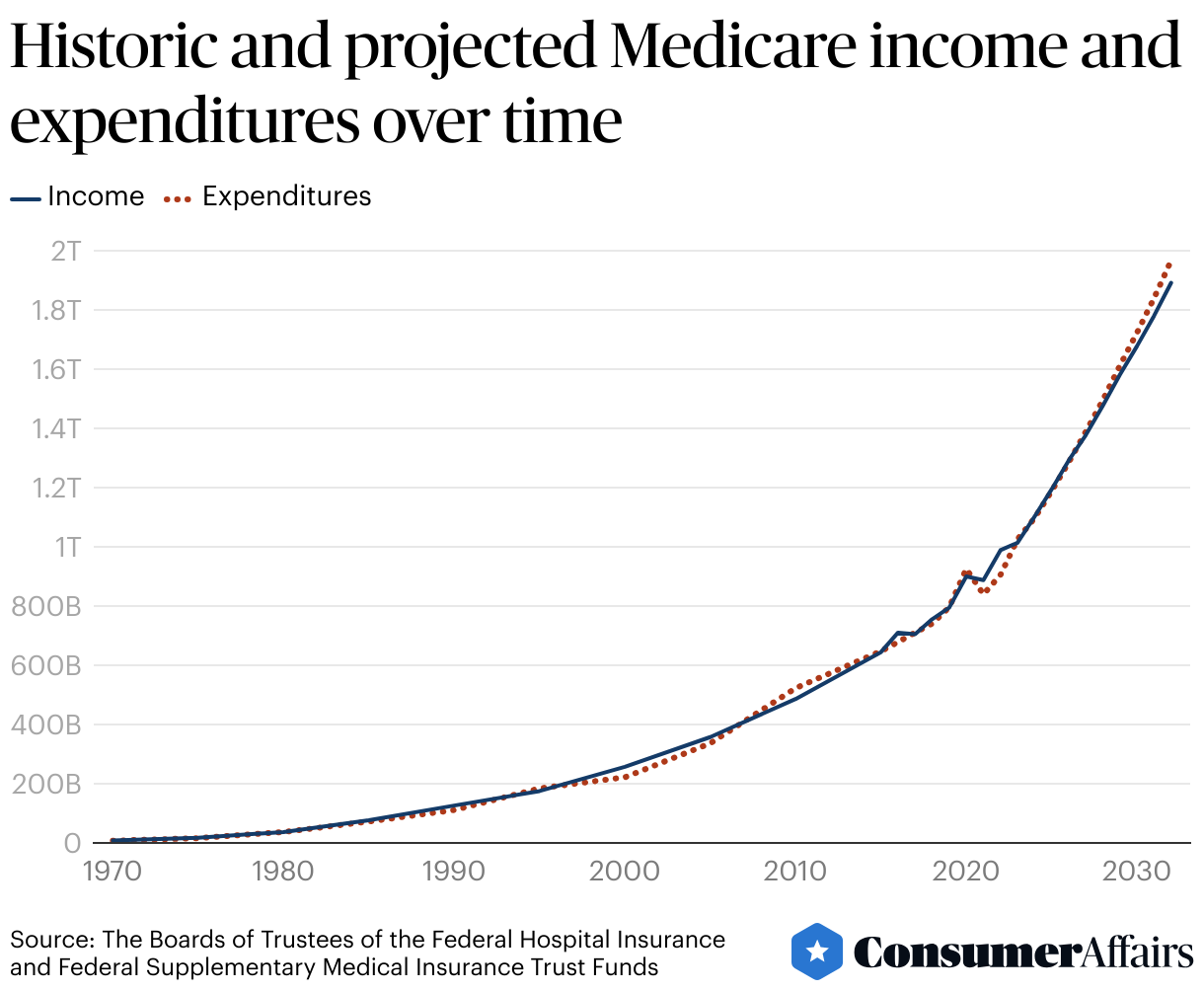

Data provided by the Medicare Boards of Trustees in their latest annual report show how much Medicare spending has increased since 1970 and projects the extent of the spending rise through 2032.

Medicare cost the country some $7.5 billion in 1970. The Medicare price tag stood at $905.1 billion in 2022. A portion of this huge increase can be attributed to inflation: a single 1970 dollar had the purchasing power of $7.44 in 2022. Allowing for inflation, $905.1 billion represents spending 16 times greater than that spent for Medicare 22 years earlier.

Various reasons for the huge increase in Medicare costs have been suggested, including the following:

- Aging of the U.S. population and the consequent growth of Medicare enrollment

- Increased use of services and intensity of care needed

- Rising health care costs

- Higher costs of care for conditions, like Alzheimer’s disease, which are more prevalent among older adults

- The increased popularity of the MA alternative and higher per-person spending in MA than in Original Medicare

Future projections

Medicare spending amounted to 10% of all federal spending in 2021. According to the U.S. Treasury, that percentage stands at 12% in 2024. For the sake of comparison, national defense spending represents 13% of the 2024 U.S. budget.

Medicare expenditures are expected to continue to increase and are forecast to reach 18% of the U.S. budget by 2032. The Boards of Trustees overseeing the Medicare trust funds project the insolvency of the Hospital Insurance (HI) Trust Fund in 2031, coming up rapidly even if three years subsequent to the year previously forecast. At the same time, discussion continues around the improvement of existing Medicare benefits as well as the possibility of structuring some form of universal health coverage.

In a Gallup Poll published in January 2023, 57% of those surveyed felt that the U.S. government should ensure universal health coverage. However, 53% of respondents favored a private-insurer health care system as opposed to the 43% who preferred a government-run system. There were clear political differences regarding program structure, with 72% of Democrats — but only 13% of Republicans — expressing preference for government-run health care.

There is no shortage of ideas that have been proposed in recent years to address Medicare’s fiscal issues, among them:

- Raising the age of eligibility from 65 to 67 for some or all beneficiaries

- Increasing or modifying cost-sharing measures among participants, either for deductibles or for specific services

- Increasing the amount of Part B or Part D premiums paid by beneficiaries

- Raising the Medicare payroll tax or imposing new taxes dedicated to Medicare funding

The passage in 2022 of the Inflation Reduction Act was an attempt to lower prescription drug costs paid by Medicare recipients as well as lower federal government costs for prescription drugs.

Consideration of possible changes and their effects on the federal budget, Medicare sustainability, program beneficiaries, health care providers and the American taxpayer will require much thought and deliberation among all stakeholders.

FAQ

What percentage of the population has Medicare?

As of February 2024, 19.7% of the total population, or about 66.4 million people, were enrolled in Medicare.

How satisfied are Medicare beneficiaries with the care they receive?

According to the 2023 CMS publication, “Medicare Beneficiaries at a Glance,” in 2021:

- Of all participants, 95% were satisfied with the general care they received.

- Concerning their ease of access to a doctor, 96% were satisfied.

- Out-of-pocket costs were reported satisfactory by 87%.

- Forty-two percent reported having to wait less than a week before seeing a physician for a doctor's appointment.

- People with disabilities who are under age 65 and covered by Medicare report poorer access to care, greater cost concerns and less satisfaction than those who are 65 and older.

Who benefits most from Medicare?

Medicare provides health care coverage for individuals who meet one the following qualifications:

- Are age 65 or older

- Are younger than 65, disabled and meet other specific criteria

- Have end-stage renal disease (permanent kidney failure requiring dialysis or a transplant, sometimes called ESRD)

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- American Journal of Public Health, “Lessons From the Long and Winding Road to Medicare for All.” Accessed Apr. 2, 2024.

- John F. Kennedy Presidential Library and Museum, “Remarks of Senator John F. Kennedy at the Memorial Program Honoring the 25th Anniversary of the Signing of the Social Security Act, Hyde Park, New York, August 14, 1960.” Accessed Apr. 2, 2024.

- National Archives, “Medicare and Medicaid Act (1965).” Accessed Apr. 2, 2024.

- Social Security, “1972 Social Security Amendments.” Accessed Apr. 2, 2024.

- Health Care Financing Review, “Medigap Reform Legislation of 1990: A 10-Year Review.” Accessed Apr. 2, 2024.

- Congress.gov, “H.R.1 - Medicare Prescription Drug, Improvement, and Modernization Act of 2003. 108th Congress (2003-2004).” Accessed Apr. 2, 2024.

- KFF.org, “FAQs on Medicare Financing and Trust Fund Solvency.” Accessed Apr. 2, 2024.

- The Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds, “2023 Annual Report.” Accessed Apr. 3, 2024.

- Centers for Medicare & Medicaid Services, “Fast Facts March 2024 Version.” Accessed Apr. 3, 2024.

- U.S. Census Bureau, “U.S. and World Population Clock, March 1, 2024.” Accessed Apr. 3, 2024.

- Centers for Medicare & Medicaid Services, “Medicare Current Beneficiary Survey (MCBS).” Accessed Apr. 4, 2024.

- KFF.org, “A Snapshot of Sources of Coverage Among Medicare Beneficiaries.” Accessed Apr. 4, 2024.

- Medicare.gov, “What Does Medicare Cost?” Accessed Apr. 4, 2024.

- Medicare.gov, “2024 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” Accessed Apr. 7, 2024.

- KFF.org, “Medicare Advantage 2024 Spotlight: First Look.” Accessed Apr. 7, 2024.

- Statista, “Total Medicare Advantage enrollment from 2004 to 2023 in the United States.” Accessed Apr. 7, 2024.

- U.S. Census Bureau. “Medicare Enrollment - National Trends 1966-2013.” Accessed Apr. 7, 2024.

- KFF.org, “10 Reasons Why Medicare Advantage Enrollment is Growing and Why It Matters.” Accessed Apr. 7, 2024.

- FRED, Federal Reserve Bank of St. Louis, “Population ages 65 and above for the United States [SPPOP65UPTOZSUSA].” Accessed Apr. 7, 2024.

- Statista, “Percentage of people covered by Medicare in the United States from 1990 to 2022.” Accessed Apr. 7, 2024.

- U.S. Census Bureau, “2020 Census: 1 in 6 People in the United States Were 65 and Over; U.S. Older Population Grew From 2010 to 2020 at Fastest Rate Since 1880 to 1890.” Accessed Apr. 7, 2024.

- Population Reference Bureau, “Fact Sheet: Aging in the United States.” Accessed Apr. 7, 2024.

- U.S. Department of Justice and the Federal Trade Commission, “2023 Merger Guidelines.” Accessed Apr. 8, 2024.

- American Medical Association, “AMA identifies market leaders in health insurance.” Accessed Apr. 8, 2024.

- KFF.org, “KFF Research Shows that Medicare Open Enrollment TV Ads Are Dominated by Medicare Advantage Plans Featuring Celebrities, Active and Fit Seniors, and Promises of Savings and Extra Benefits Without Fundamental Plan Information.” Accessed Apr. 8, 2024.

- State Health Insurance Assistance Program, “Local Medicare Help.” Accessed Apr. 9, 2024.

- KFF.org, “Medicare Advantage Has Become More Popular Among the Shrinking Share of Employers That Offer Retiree Health Benefits.” Accessed Apr. 9, 2024.

- KFF.org, “The Facts About Medicare Spending.” Accessed Apr. 9, 2024.

- KFF.org, “What to Know about Medicare Spending and Financing.” Accessed Apr. 9, 2024.

- U.S. Treasury, “How much has the U.S. government spent this year?” Accessed Apr. 9, 2024.

- Gallup, “Majority in U.S. Still Say Gov't Should Ensure Healthcare.” Accessed Apr. 9, 2024.

- KFF.org, “Explaining the Prescription Drug Provisions in the Inflation Reduction Act.” Accessed Apr. 9, 2024.

- KFF.org, “Policy Options to Sustain Medicare for the Future.” Accessed Apr. 9, 2024.

- Congress.gov, “H.R.5376 - Inflation Reduction Act of 2022.” Accessed Apr. 9, 2024.

- Centers for Medicare and Medicaid Services, “Monthly Enrollment by State 2024 02.” Accessed Apr. 9, 2024.

- Centers for Medicare and Medicaid Services, “Medicare Beneficiaries at a Glance.” Accessed Apr. 9, 2024.

- Center for Medicare Advocacy, “Medicare Coverage for People with Disabilities.” Accessed Apr. 9, 2024.

- KFF.org, “Overall Satisfaction with Medicare is High, But Beneficiaries Under Age 65 With Disabilities Experience More Insurance Problems Than Older Beneficiaries.” Accessed Apr. 30, 2024.

- U.S. Bureau of Labor Statistics, “CPI Inflation Calculator.” Accessed Apr. 30, 2024.

- Medicare.gov, “Costs ❘ Medicare.” Accessed May 1, 2024.

Figures