Student Loans: Reentering Repayment (2026 Data)

+1 more

With the final emergency forbearance on federal student loan debt drawing to a close on Apr. 30, 2022, tens of millions of Americans are about to reenter the repayment experience after over two years of reprieve. But exactly how is this massive group of people preparing for this eventuality — are they ready? We spoke to 1,020 people within the demographic to find out.

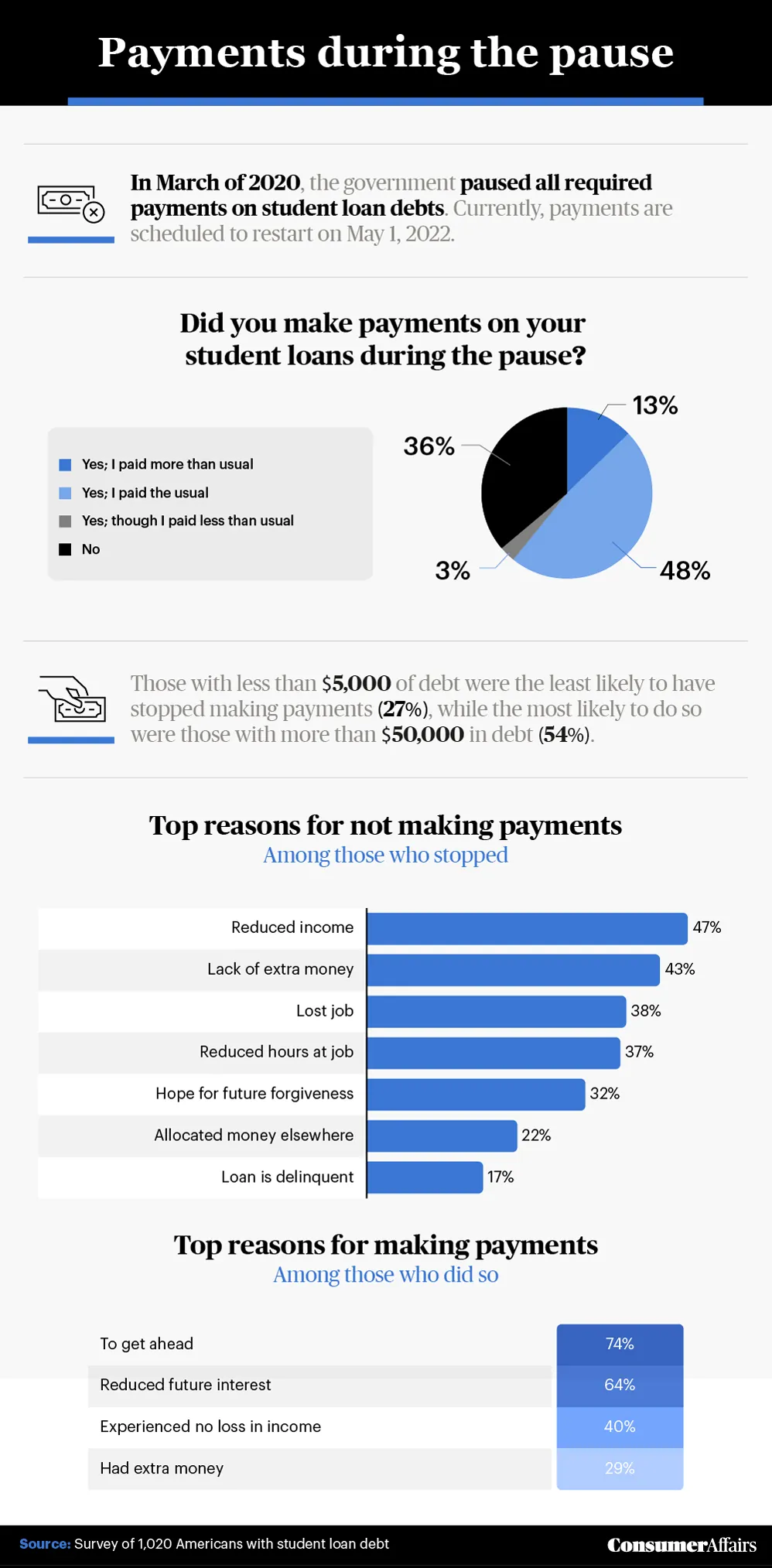

Nearly half of respondents have continued making their usual student loan payments during the pause.

Jump to insight31% of respondents lacked confidence that they would be able to resume making payments.

Jump to insight93% of respondents believed they would need to make some budget cuts when payments resumed.

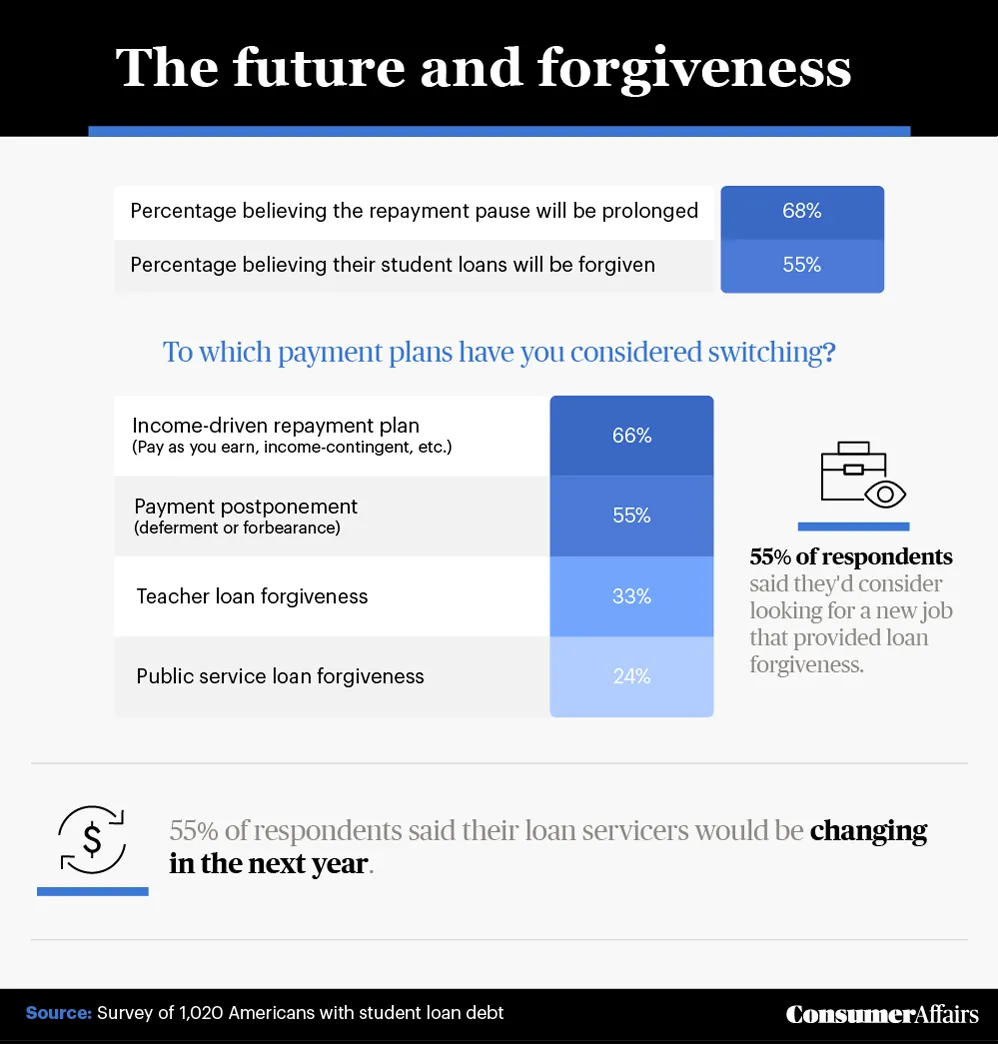

Jump to insight68% of respondents thought the pause would be extended again.

Jump to insightAmericans prepare to resume student loan payments after a pause of nearly two years.

From emotional readiness to specific financial plans, we now have data-backed information as to how the end of the payment pause may take shape for many Americans. Respondents shared the sacrifices they’re likely to make to start paying again, as well as how they’ve been handling the pause in the first place. Read on to see what we uncovered with regards to the fast-approaching Apr. 30 date.

Paused payment behaviors

While student loan payment pauses were certainly a welcome relief for many, they weren’t a requirement, and not everyone chose to delay repayment. The first part of our study looks at how student loan debtors approached the option and what reasoning drove their respective behaviors.

The majority of former students who responded chose not to take advantage of the student loan payment pause. In fact, more than 1 in 10 actually started paying more each month than they previously had been. Nearly half (48%) continued paying as usual. Seventy-four percent said they did so to “get ahead,” while 40% explained that they had not suffered any loss in income and didn’t feel pressured to stop paying. Job losses did in fact impact lower-income, nongraduate employees the hardest, so student loan debtors may have been more protected from mass layoffs than their less educated counterparts.

For those who did stop making payments (36% of former students), the driving factor was typically a loss of income (47%), employment (38%) or hours (37%). Nearly a third, however, admitted to procrastinating over payments in the hope of being granted student loan forgiveness in the future. At the time of writing this article, Congress was still undecided as to whether student loans should be forgiven and, if so, to what extent.

» MORE: Best student loan companies

Student loan repayment readiness

The next section of our study asked student loan debt holders to take a look at their current financial situation and estimate their readiness and confidence for the approaching repayment date.

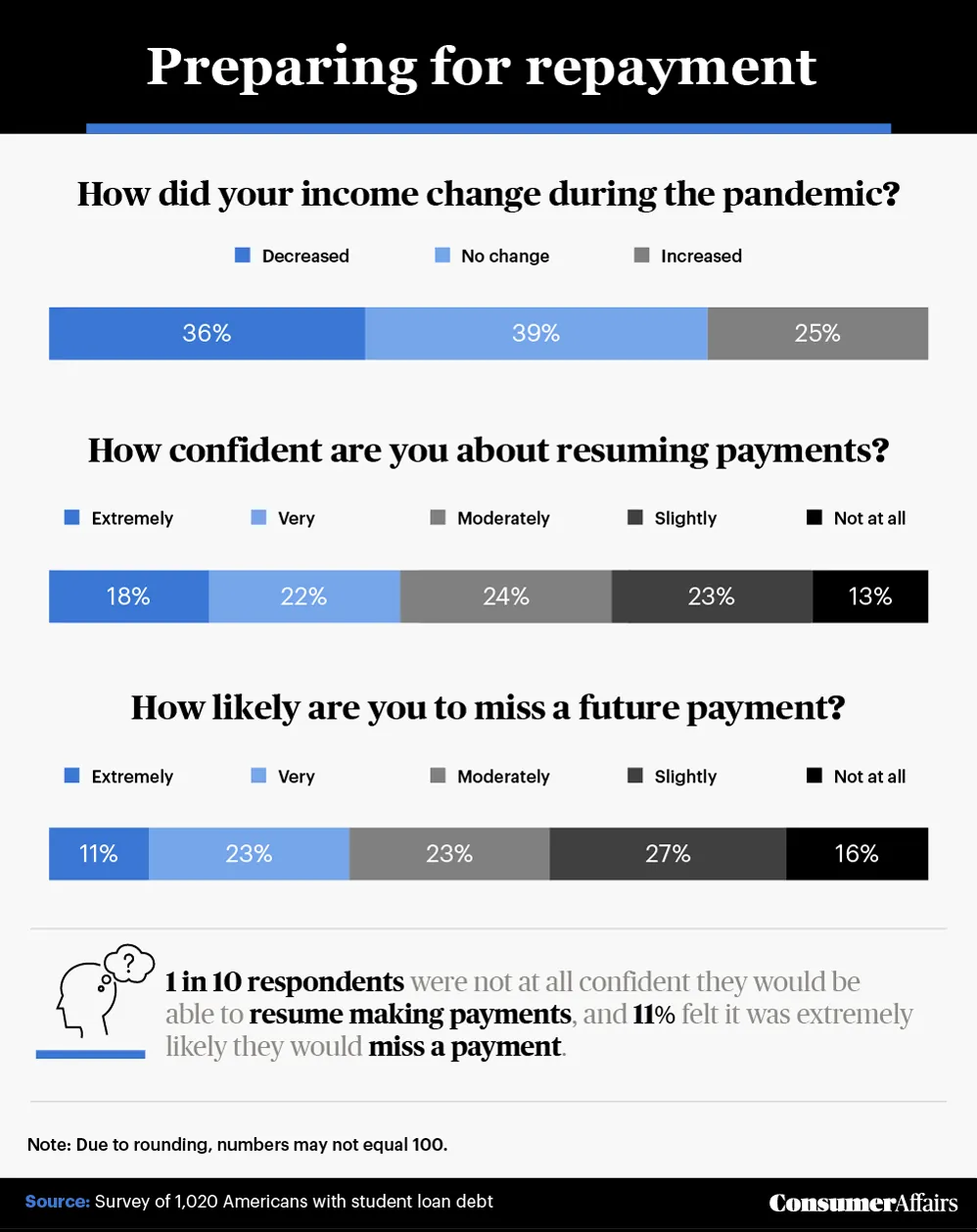

While many respondents did not suffer a change of income during the pandemic, it was definitely more likely for income to decrease than increase, which took a noticeable toll on confidence. Just 18% considered themselves extremely confident about being able to resume payments in May. One in 10 were not at all confident, while 23% had only a limited amount of faith in their repayment ability.

This lack of confidence, of course, relates to the probability of missing future payments. A whopping 84% admitted that there was at least some likelihood of not being able to afford a future payment and therefore missing it altogether. In fact, 34% agreed that there was a very high or extremely high likelihood of missing a future payment.

Making it work

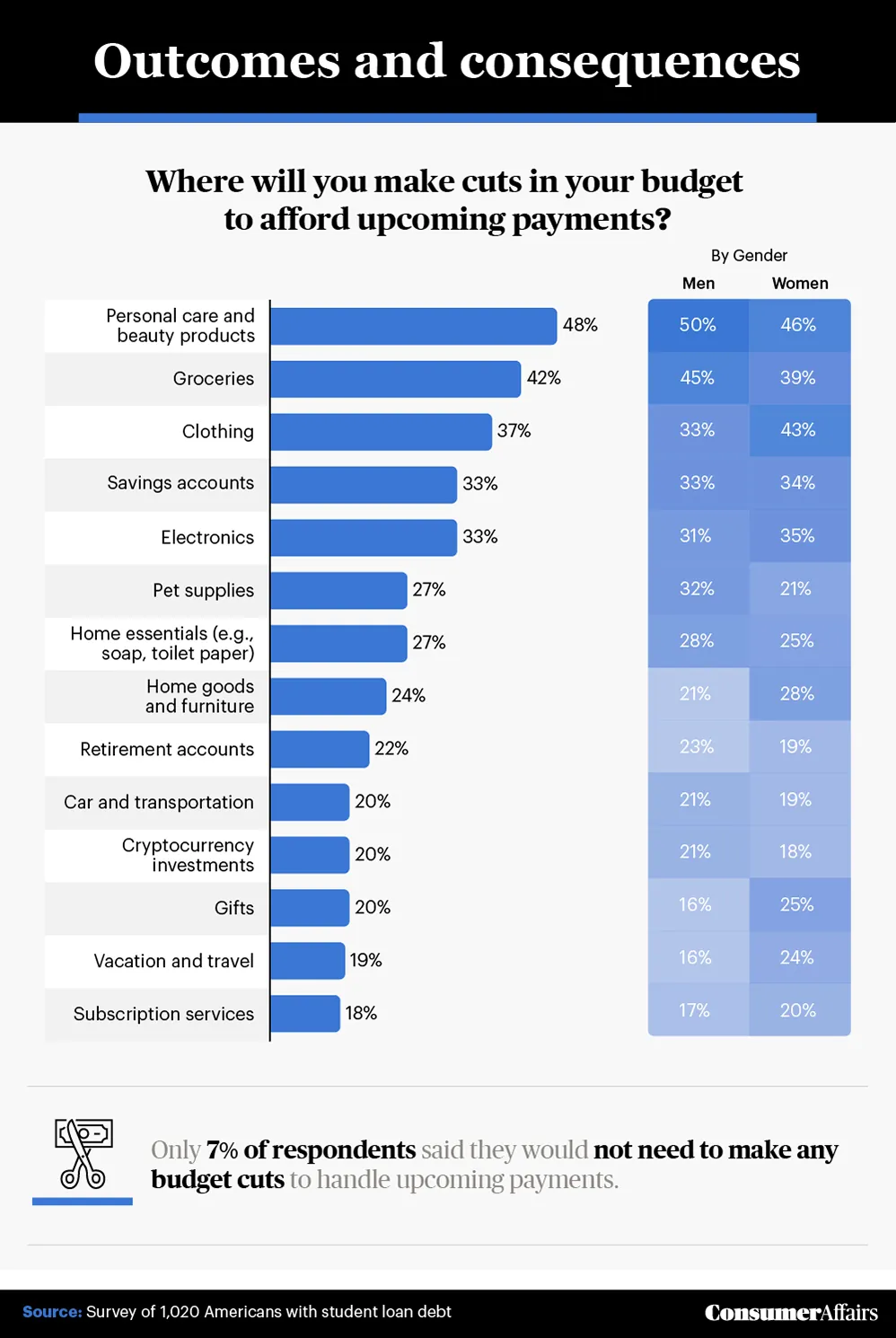

Repaying student loan debt wasn’t easy for many prior to the pause. With the relief end date quickly approaching, these people are faced with the question of how they’ll make their finances work and what exactly they’ll have to sacrifice.

Personal care and beauty products were voted as the first things to go in an attempt to afford repayments. Fifty percent of men and 46% of women planned on sacrificing these purchases when the time comes. While products like these may seem superfluous and perhaps an added luxury, they often relate to important components of self-care and health that can seriously impact mood and a person’s ability to avoid burnout. The next most commonly anticipated sacrifice was groceries — an obviously vital component of survival. Forty-two percent of participants actively planned to reduce their grocery spending in order to come up with money for their student loans.

Farther down the list, but still common, was a sacrifice in cryptocurrency investments (20%). Again, this may seem unnecessary to survival, but it could have significant impacts on the investors’ ultimate financial condition.

Ultimately, only 7% of respondents were lucky enough to feel they won’t have to make any sacrifices at all.

» MORE: Good debt vs. bad debt

Unexpected consequences

Beyond the financial realities of student loan repayments, the emotional toll can be just as tangible. This part of our study looks into the specific emotions former students feel when thinking about their repayments.

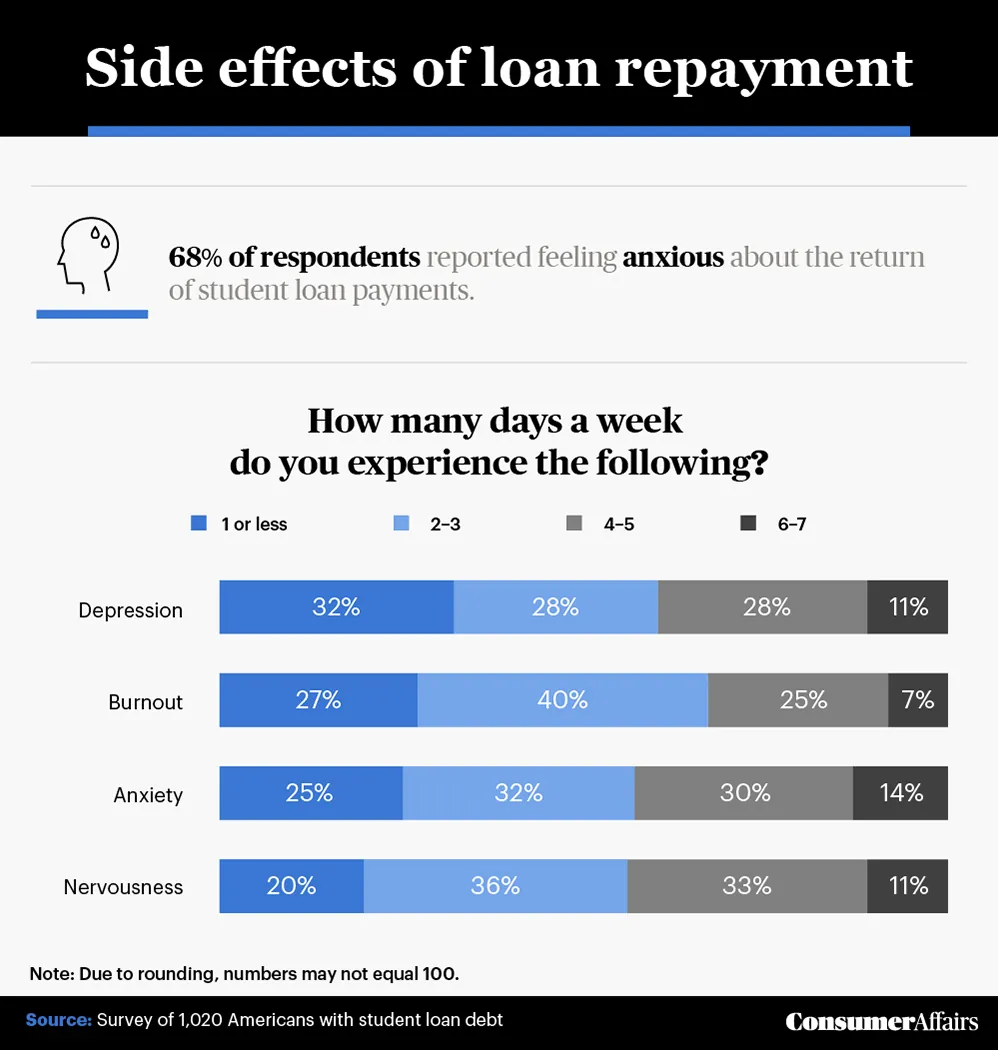

Student loan payments were already daunting before the pandemic, but returning to them after the pause had 68% of respondents feeling anxious. Unfortunately, signs of anxiety and depression come with the territory of debt and student loans. Among our survey group (all of whom have student loan debt), more than 1 in 10 experience depression every single day of the week; depression, burnout, anxiety and nervousness were often common for participants at least once a week.

Future hopes among student loan debtors

Though the future is still uncertain with regards to student loan forgiveness, we wanted to give those with debt the chance to share their thoughts. Our study wraps up with a look at how respondents believe student loan pauses and forgiveness will unfold for them in the coming months and years.

In spite of their fears and anxieties, respondents largely remained hopeful that their student loan payments would one day be forgiven (55%) or at least be extended again (68%). And while this topic has, of course, been politicized, we found Republicans and Democrats to be relatively in agreement. Fifty-nine percent of Republicans and 58% of Democrats believed their student loans would ultimately be forgiven.

Lastly, we asked respondents which specific payment plans they would consider in the nearer future. Most (66%) wanted to follow an income-driven repayment plan, where you pay as you earn. Fifty-five percent wanted to pursue a payment postponement or deferment plan, while the same number would consider looking for a job that offers student loan forgiveness options.

Facing the future of loans

As the end of the student loan repayment pause draws nearer, debt holders have begun to face some harsh realities. Most felt a lack of confidence in their ability to make repayments, while others anticipated delinquent loans in their near future. Even those who could pay experienced weekly feelings of depression and anxiety.

Many of life’s important purchases, such as a college education, come with a lot of uncertainty and anxiety, especially if you’re doing it alone. Fortunately, there are experts who are ready and willing to help. Our site provides information for all of life’s major purchases — from loans to cars to houses and more. If you could use trustworthy information on financial matters like these, visit ConsumerAffairs.com today.

Methodology and limitations

We surveyed 1,020 respondents ranging in age from 18 to 80 years old in order to explore their plans for resuming student loan repayments this year. For gender breakdowns, 596 respondents were men, 421 respondents were women and three were nonconforming or nonbinary. Those that identified as nonconforming or nonbinary were removed from gender breakdowns due to the small sample size. In terms of political party, 492 respondents were Democrats, 353 were Republicans and 175 were independent. The independent group was removed from political party breakdowns due to the smaller sample size.

For the free-response section regarding respondent debt, outliers were removed. To help ensure that all respondents took our survey seriously, they were required to identify and correctly answer an attention-check question. Survey data have certain limitations related to self-reporting; these limitations include telescoping, exaggeration and selective memory.

Fair use statement

Student loan debt affects nearly 45 million Americans. If you think this data would be helpful to your audience, please feel free to share. Just be sure your purposes are noncommercial and that you link back to this page.