This website utilizes technologies such as cookies to enable essential site functionality, as well as for analytics, personalization, and targeted advertising. To learn more, view the following link:

Where a $100K Salary Stretches the Furthest — After Taxes 2026

A six-figure salary is often viewed as a major financial milestone. But in many cities, it no longer guarantees that you can live comfortably. In fact, a sizable share of six-figure earners — nearly two-thirds — say that a $100,000-plus salary is just enough for survival mode, not a sign of wealth, according to a recent survey by The Harris Poll.

Even if you do arrive at that $100,000 salary, it doesn’t all make it to your net paycheck. Take-home pay varies dramatically by location, in part due to the wide variance in state and local tax rates across the U.S. But taxes are only part of the equation; housing and everyday costs can erode take-home pay just as quickly.

So, where does a six-figure income deliver the most real value?

To find out, ConsumerAffairs analyzed the tax rates of the 100 largest U.S. cities, leveraging that data to estimate the take-home pay of a $100,000 salary. To compare how far that income goes across cities, we adjusted the post-tax amount using regional price parities, which account for differences in local price levels.

Whether you’re looking for ways to reduce taxes or simply feeling motivated to think critically about your money as tax season rolls around, keep reading to see where a $100,000 salary stretches the furthest — and where your city lands in the rankings.

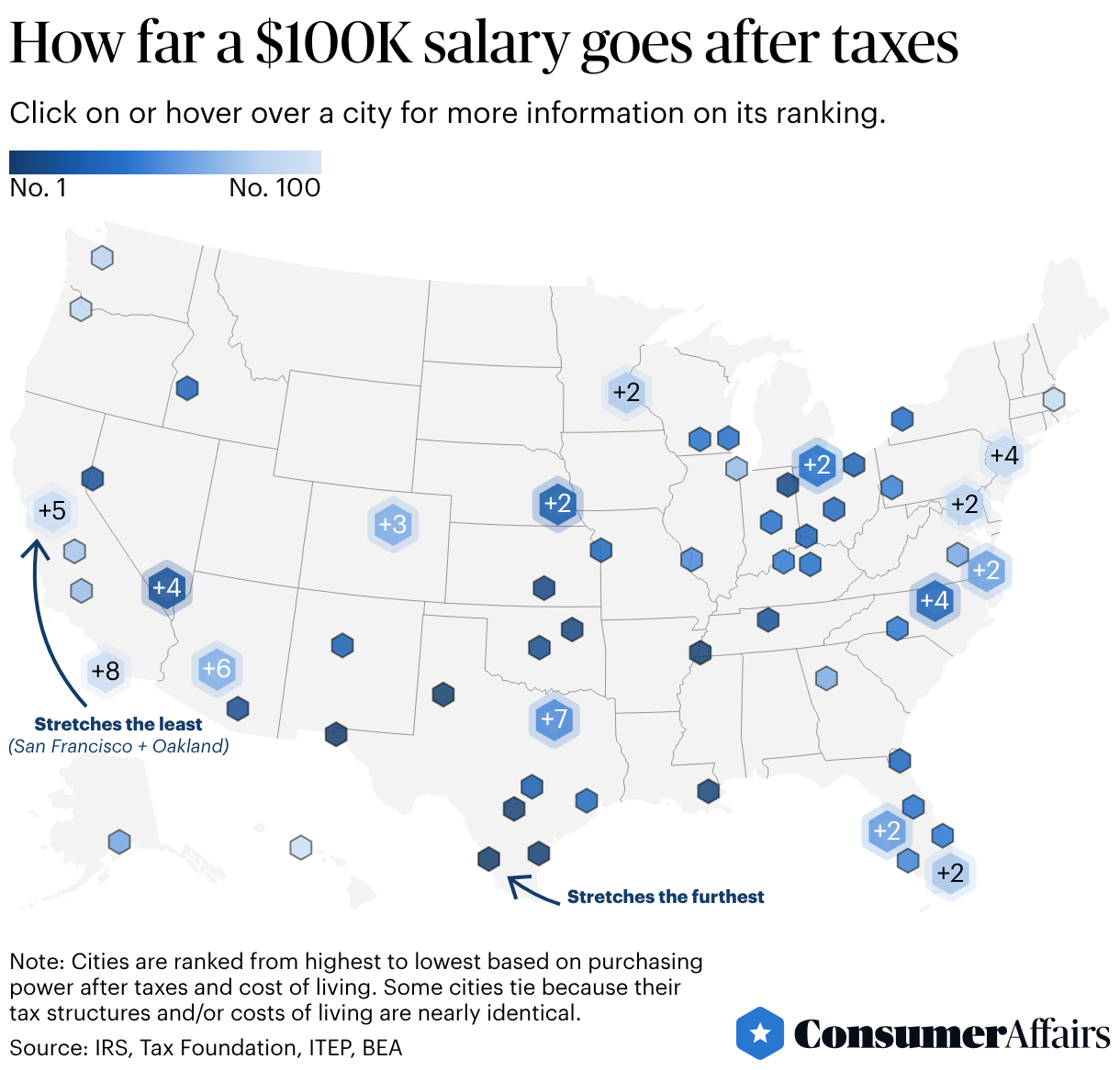

Key insights

A $100,000 salary goes the furthest in Laredo, Texas. With no state or local income taxes and a low cost of living, $100,000 adjusts to $89,864 in purchasing power at national-average prices.

Two Bay Area cities, San Francisco and Oakland, rank at the bottom. In these high-cost, high-tax cities, a $100,000 salary adjusts to only $62,371 in purchasing power.

Some cities tie in the rankings due to shared tax rates or metro areas. For example, five California cities tied for 93rd are all in the Los Angeles metro area and share the same tax rates and costs of living.

Earning $100,000 a year is no small achievement, but it doesn’t guarantee that you can live large in many of America’s major cities. When adjusted for taxes and regional price parity (RPP) — a measure that compares the local costs of goods and services with the national average — the effective "buying power" of that $100K shifts dramatically.

The good news? In some cities, residents benefit from a combination of lower housing costs, below-average prices for goods and cheaper utilities.

“Gross salary is what most people focus on but what really matters is purchasing power — what’s left after taxes plus local prices,” said Sebastian Fidilio, an accountant in New York and the founder of sebCFO, which provides financial services to small businesses. “It's not what you make — it's what you keep that matters.”

The following cities offer the highest adjusted post-tax salary, effectively making a $100,000 income feel like over $80,000 at national-average prices:

Laredo, Texas

El Paso, Texas

Lubbock, Texas

Corpus Christi, Texas

Memphis, Tennessee

San Antonio, Texas

New Orleans, Louisiana

Tulsa, Oklahoma

Wichita, Kansas

Fort Wayne, Indiana

Our analysis found that a $100,000 salary goes the furthest in several Texas cities, thanks to affordable local cost of living and no state and local taxes. Laredo leads the list, with an adjusted purchasing power of $89,864.

Texas cities are among the best in the nation in homebuilding and housing supply as of publishing, which helps bring (and keep) down housing costs — a critical metric in regional price data. Beyond five cities in the Lone Star State, three other Southern cities and two Midwest metros made the top 10.

Cities where your income doesn’t stretch as far

In some cities, high costs of living and taxes can shrink a six-figure salary to feel more like peanuts. Combined, these costs can leave a stark contrast between a resident’s gross pay and their actual purchasing power.

Most cities have low or minimal local taxes; only one city in the bottom 10 faces the double whammy of both state and local taxes (New York). The other nine cities have relatively high state taxes but no local income tax.

However, all the lowest-ranked cities face staggering costs of living. The RPP, which considers costs of goods and services such as housing and utilities, in each of these cities is much higher than the national average. For example, the RPP for San Francisco’s housing is 200.2, meaning housing there costs double the national average. Many of the cities at the bottom of the list are among the most expensive cities in America.

The following cities rank the lowest for how far a six-figure income will go:

San Francisco, California

Oakland, California

New York, New York

Irvine, California

Anaheim, California

Santa Ana, California

Long Beach, California

Los Angeles, California

Honolulu, Hawaii

San Jose, California

In all of the above cities, a $100,000 salary translates to less than $66,000 in adjusted post-tax purchasing power — more than $20,000 less than in cities where purchasing power is highest.

One reason several cities are tied in the rankings is that they belong to the same metro area.

For example, the five California cities tied for fourth worst are all in the Long Angeles-Long Beach-Anaheim metro statistical area.

These five cities tie because they share the same taxes (5.18% state, 0% local), as well as the same RPP index score (115.50, or 15.5% higher than the national average).

How far does a $100K salary go in your city?

You may have a sense of how much of your own pay goes toward taxes each month. But the raw tax rate doesn’t tell the full story.

When it comes to true post-tax purchasing power, where does your city fall in the rankings? And zooming out even further, how does your state stack up against the rest of the nation?

Check out the full data table below to see which factors contribute to whether you keep — or lose — more of your paycheck in the place you call home.

Why your income stretches more in some cities

Many people assume that having no state income tax is the be-all and end-all of cheaper living — but the data suggests otherwise.

“No-income-tax states aren’t always ‘better,’” said Fidilio. “Lower income tax can be offset by higher housing costs, property taxes, insurance and sales taxes. The best outcome is usually (a combination of) low total cost and a reasonable tax burden, not just no state tax,” he explained.

“No-income-tax states aren’t always ‘better.’ Lower income tax can be offset by higher housing costs, property taxes, insurance and sales taxes.”

— Sebastian Fidilio, accountant and founder of sebCFO

Consider Toledo, Ohio. Residents of the Glass City have to pay both state (1.97%) and local (2.5%) income tax. However, a worker earning $100,000 a year in Toledo has greater purchasing power than a worker with the same wage in Austin, Texas, even though Austin has no state or local income tax. Both cities have costs of living that are below the national average, but the RPP is seven percentage points lower in Toledo.

States that lack an income tax may have other drawbacks for their residents' finances. In a state like Florida, the thousands of dollars you may save on state or local income taxes might get offset by property insurance costs (Florida’s are the highest in the nation for homes with a mortgage).

How state and local taxes affect your income

State and local taxes vary widely. For the 100 cities we compared, state taxes on a $100,000 salary range from $0 to $7,954, and local taxes range from $0 to $3,740.

In cities where residents pay both state and local income taxes, workers earning six figures can owe upward of $6,000 total. (That is, of course, in addition to the federal income tax — $13,449 for an individual filer with a $100,000 salary.)

If you make six figures, you’d face the steepest tax burden in New York City. With a 4.95% state tax rate and 3.44% local rate, living in the Big Apple takes a significant bite out of workers’ paychecks: $8,393 out of a $100,000 salary.

Not far behind is Portland, Oregon. If you make $100,000 here, you’ll pay a combined $7,989 in state and local taxes. Portland’s city income tax is just 0.04% — the lowest non-zero tax rate of the cities we compared — but Oregon’s state income taxes are the highest in the country, at 7.95%.

Tax season tips to keep more of your paycheck

Tax Day isn’t until April, but as soon as the calendar turns to the new year, some start celebrating tax season — or dreading it. Whichever camp you fall into, check out these tips for hanging on to more of each paycheck and making your salary go the furthest.

Take advantage of deductions and credits. Make sure you’re not overlooking anything you can claim — from above-the-line adjustments like student loan interest or individual retirement account contributions to itemized deductions like mortgage interest.

… Especially those that may be new or expanded. The One Big Beautiful Bill Act means significant changes for the 2026 tax season, including tax-free treatment of tips and overtime, car loan interest deduction and expanded charitable contributions.

“All of these new tax deductions come with a set of eligibility requirements and new reporting requirements,” said Laurie Smith, a tax partner with the accounting firm Wiss. “It’s important to understand these new deductions so that if you qualify, you can properly claim them on your 2025 tax return.”

Maximize your contributions. Putting money toward retirement or health care savings each month might mean a slightly smaller paycheck, but it lowers your taxable income — and therefore, your tax burden.

“Maximize contributions to tax-advantaged accounts like a 401(k), IRA or HSA to lower your adjusted gross income (AGI) and manage your tax bracket,” said Smith. “Taxpayers who contribute early in the year give investments more time to grow tax-deferred (or tax-free in the case of Roth/HSA).”

Keep your withholdings current. To prevent surprises, taxpayers should review their withholding or estimated tax payments to smooth out the tax burden over the year.

“Update your W-4 for life changes — like a raise, new side job or change in marital status,” said Smith.

Track deductible expenses. Maximizing the appropriate deductions and credits is a lot easier if you stay on top of your recordkeeping year-round.

“Keeping records from the beginning of the year will provide you with more accurate records versus trying to re-create and remember expenses that were incurred throughout the year, eight to 10 months later,” Smith said.

Explore options for tax relief. Maximizing deductions can help lower your next tax bill, but if you’re struggling to settle an old one, you may need to pursue other actions. Tax relief programs may be able to help you settle up on back taxes and keep more of your paycheck — no matter which city you call home.

Methodology

To determine where a $100,000 salary goes the furthest, ConsumerAffairs analyzed the 100 largest U.S. cities. For each city, we started with a flat $100,000 annual salary and estimated take-home pay by subtracting federal income tax (using the standard deduction for a single filer), as well as applicable state and local taxes. We also deducted payroll taxes for Social Security and Medicare.

We then adjusted each city’s post-tax income using regional price parity (RPP) data to account for differences in local price levels. This resulting figure represents the purchasing power of a $100,000 salary in national-average prices, or, put another way, the value of everything a $100,000 salary can buy, repriced using average U.S. prices. Cities were ranked from highest to lowest based on this adjusted take-home pay, with ties assigned to cities that produced the same result.

Reference policy

We love it when people share our findings! If you do, please link back to our original article to credit our research.

Questions?

For questions about the data or if you'd like to set up an interview, please contact dedens@consumeraffairs.com.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include: