Average Credit Card Debt by Age (2026 Data)

+1 more

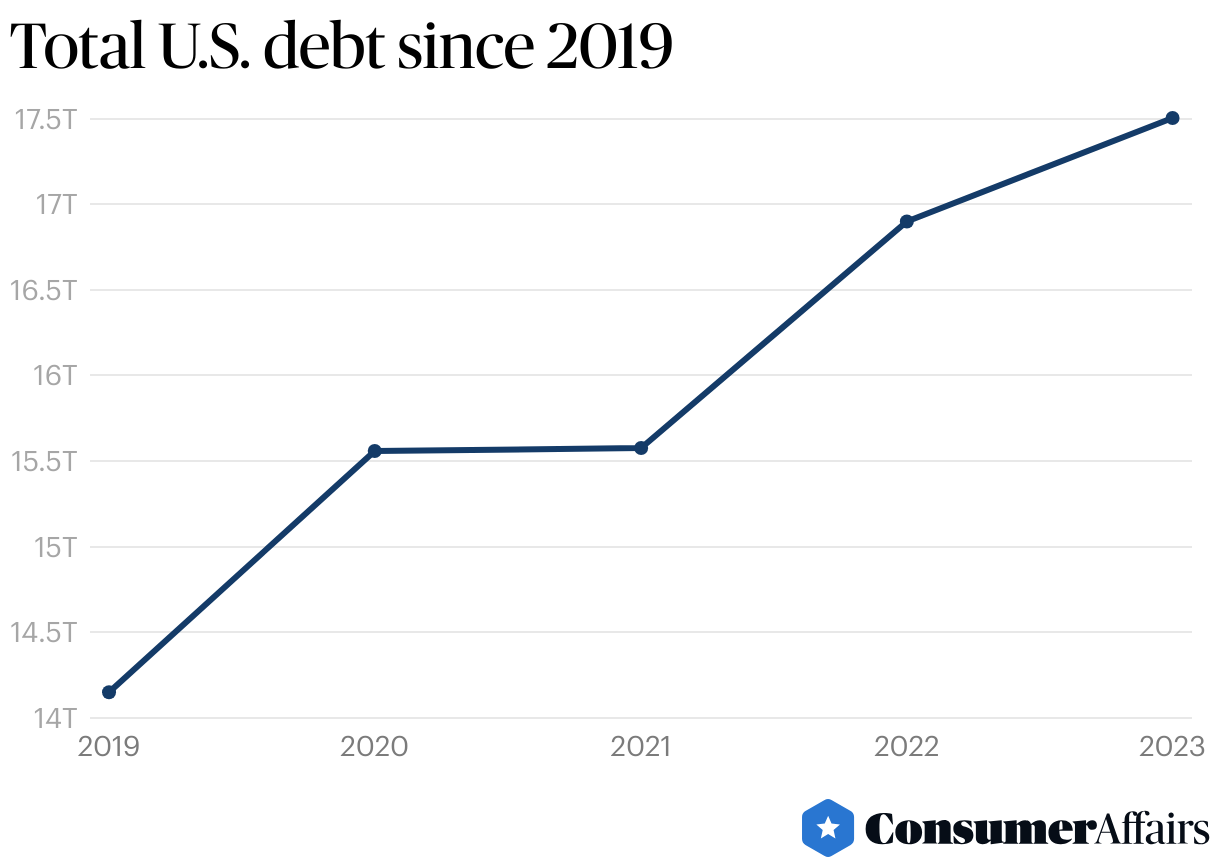

Debt for citizens in the U.S. is rising, with a roughly $600 billion increase in 2023. Of the total $17.5 trillion in debt, about $1.13 trillion comes from credit cards alone. While many commonly attribute credit card debt to younger generations, Gen Z has the lowest amount of debt overall. Gen X and millennials aged 30 or older account for the largest portion of debt, including credit card debt.

Credit card debt is the U.S.’s fourth highest debt category.

Jump to insightThose between the ages of 40 and 49 have the highest amount of credit card debt, making up for about 23% of the total debt in that category.

Jump to insightWhile credit card debt is high, mortgage and student loan debt are more prevalent, making up about $12.25 trillion and $1.6 trillion of total U.S. debt, respectively.

Jump to insightIn 2022, Americans identifying as white had the most credit card debt — an average of $6,930.

Jump to insightDebt in the U.S. has risen approximately $3.35 trillion in the past four years.

Jump to insightCredit card debt statistics

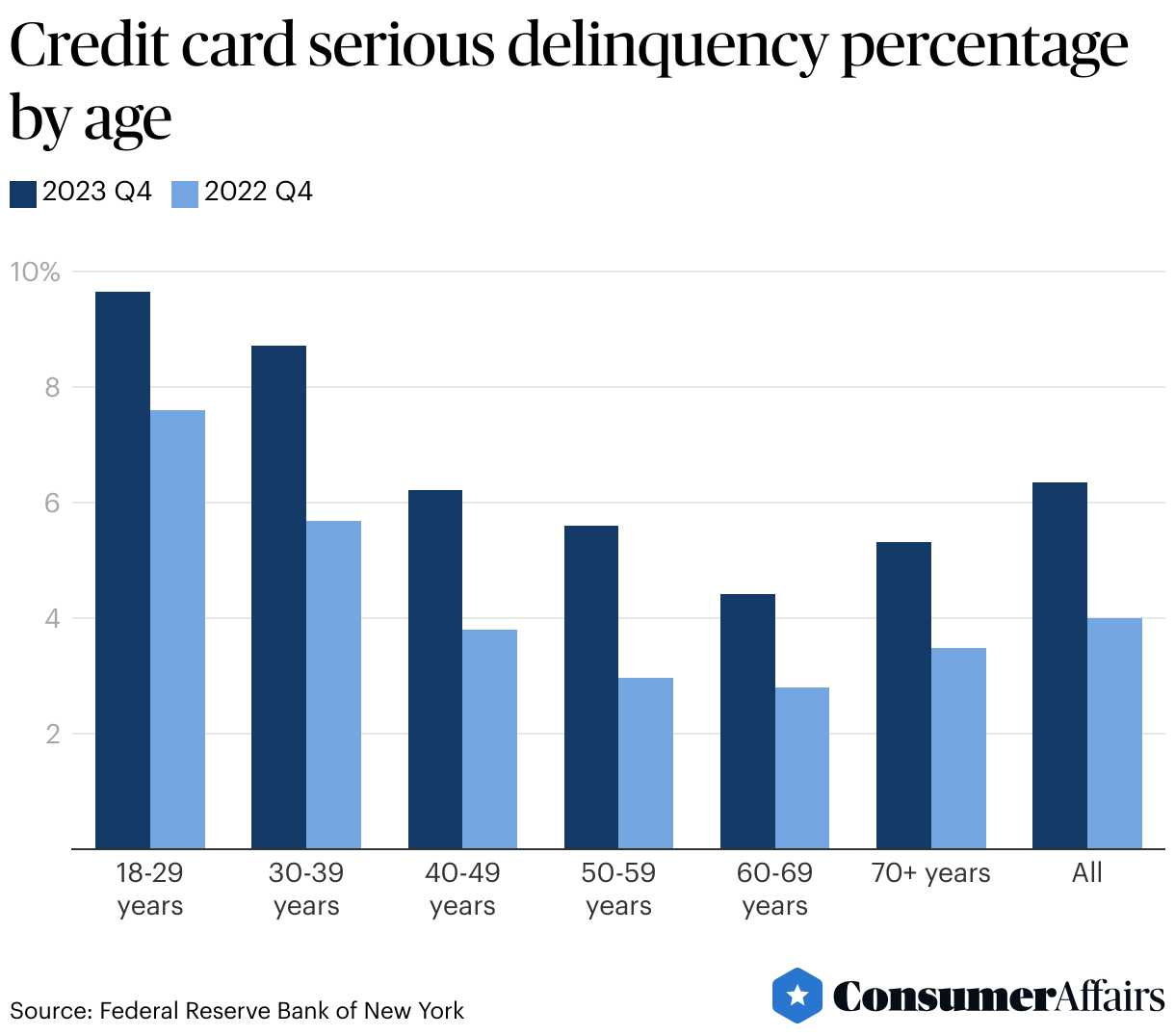

Credit card debt is the fourth highest debt category in the U.S., according to the Federal Reserve Bank of New York’s 2023 report on household debt and credit. As debt in the U.S. has increased, so has serious delinquency on credit card debt. Between 2022 and 2023, serious delinquencies across age groups as a whole increased by nearly 59%. Delinquency was most prevalent in those aged 18 to 29, at 9.65% as of 2023.

However, even with higher delinquency in younger age groups, Federal Reserve data shows a consistent trend of the burden of debt, including credit card debt, falling more heavily on those in the middle generations.

Total debt by age group

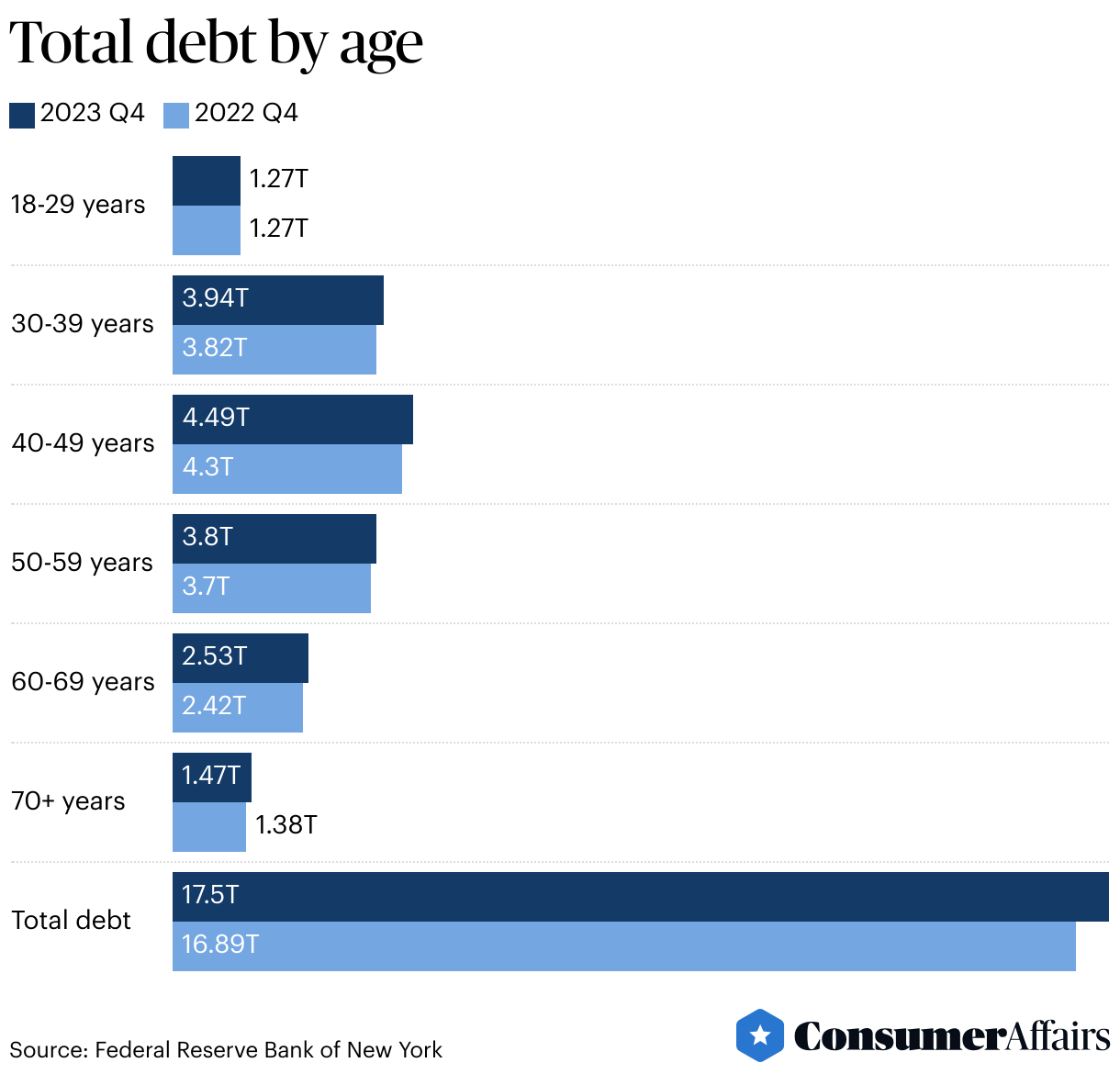

Debt of all types is a problem in America. Those between the ages of 40 and 49 have the highest amount of debt than any other age group.

Credit card debt affects Gen Z the least, with only about $90 billion for 2023. Baby boomers and those born in the Silent Generation have the second-most credit card debt, with about $330 billion combined.

However, for Gen X and millennials 30 and older, credit card debt is a different story. These generations account for approximately $720 billion of total credit card debt, making them the most greatly affected. Within the millennial and Gen X generations, those between 40 and 49 hold the highest amount, accounting for about 23% of total credit card debt.

In addition to facing the highest credit card debt, these generations also have the highest debt overall. Gen X and millennials 30-plus account for a combined total of approximately $12.23 trillion in debt. Meanwhile, the younger generation, between ages 18 and 29, accounts for the least amount at $1.27 trillion.

Debt by age and type

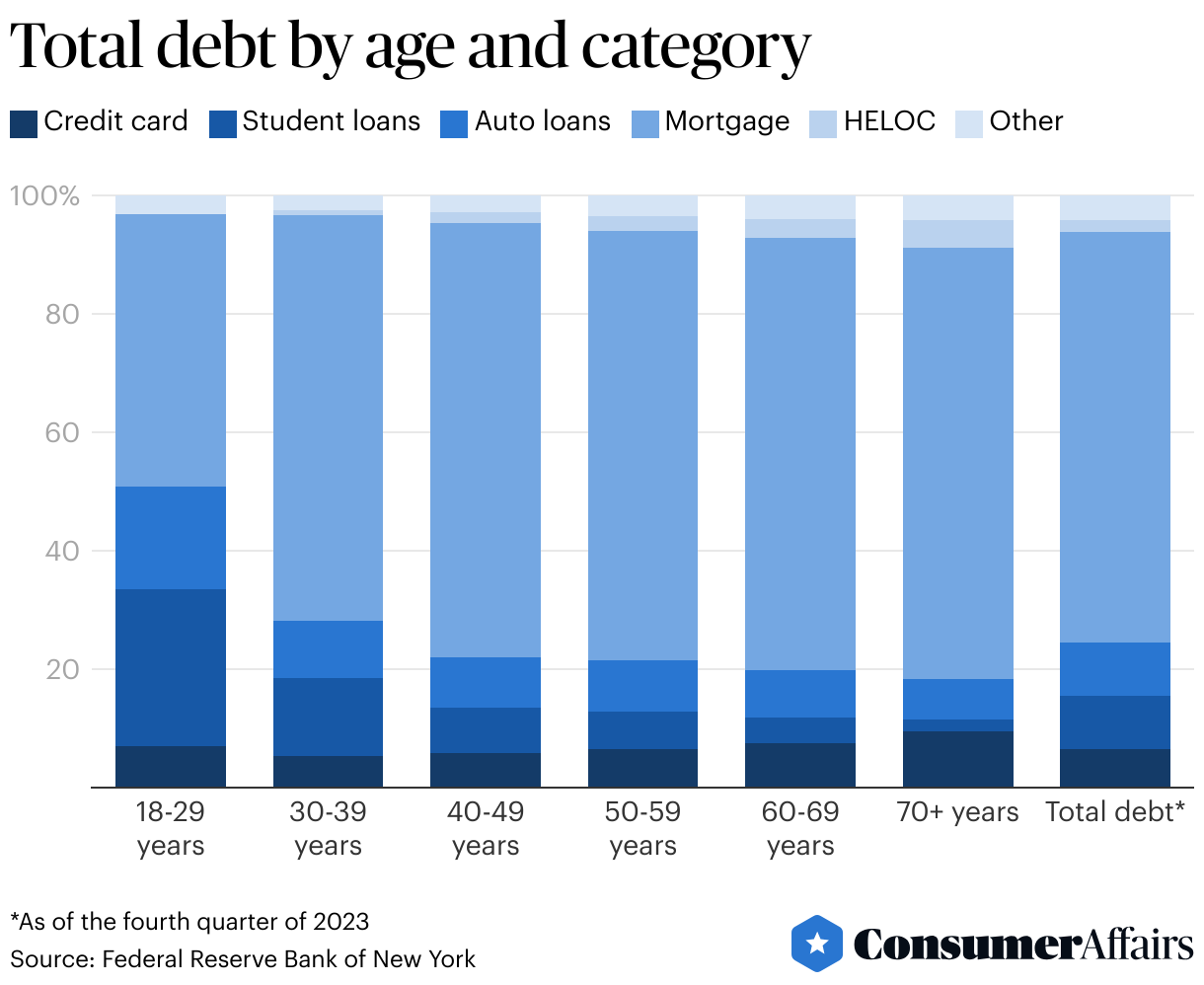

While credit cards make up a significant portion of U.S. debt overall, mortgage and student loan debt are significantly higher. Mortgage debt accounts for about $12.25 trillion, while student loans sit at approximately $1.6 trillion. Auto loans also make up a significant portion of U.S. debt, at just over $1.6 trillion.

As with all other debt categories, those between the ages of 30 and 59 hold the most debt. The major difference here is that Gen Z has higher auto and student loan debt but lower mortgage debt than baby boomers and those from the Silent Generation. This suggests that older generations are spending more money on homes, while the younger generations are directing their funds toward higher education and transportation.

Debt by demographics

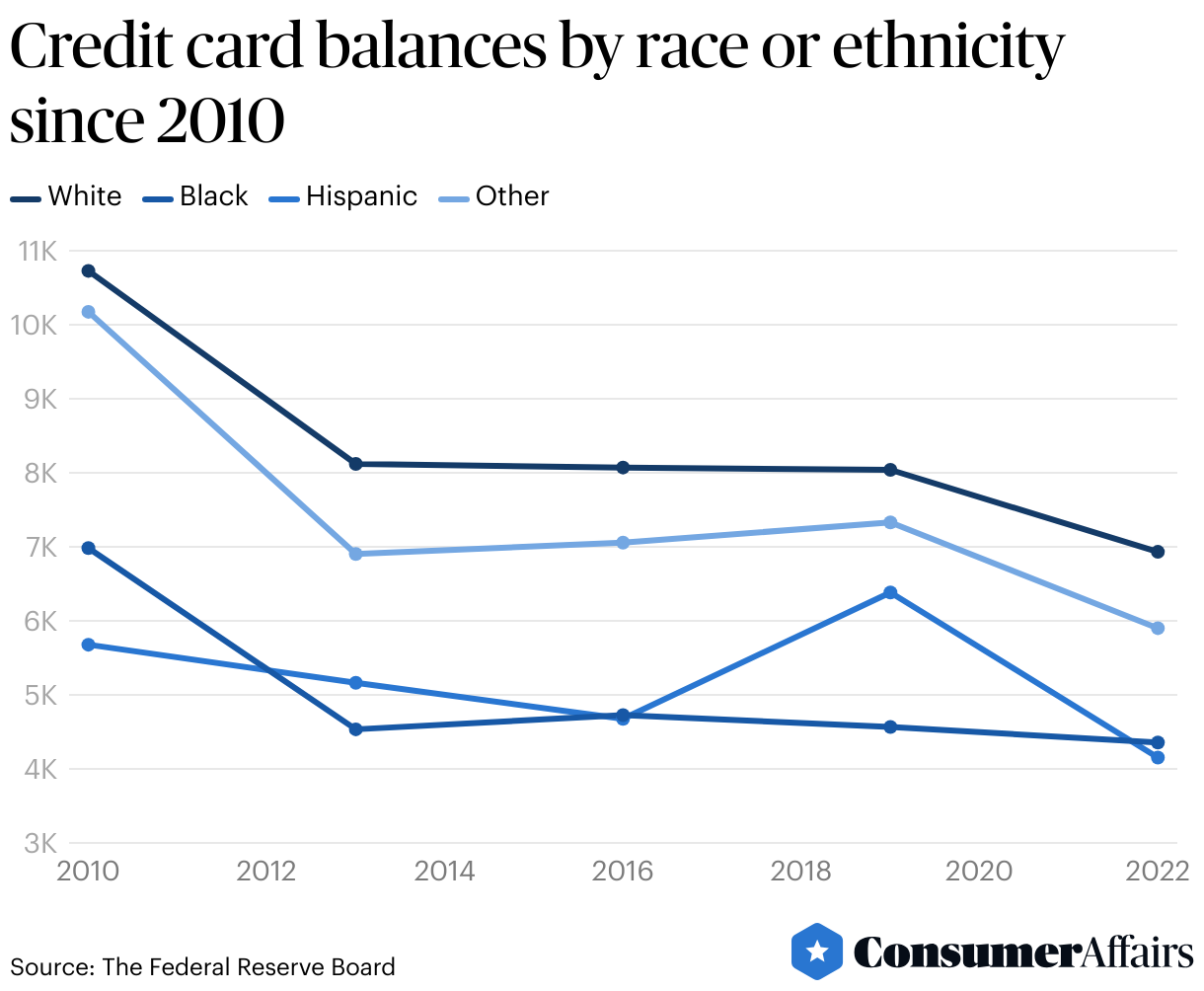

Beyond age, credit card debt varies by demographic. According to the 1989 to 2022 Survey of Consumer Finances, Americans identifying as white had the highest credit card debt, averaging $6,930 in 2022. Americans identifying as Hispanic or Black reported the least amount of credit card debt, though it varies by year. As of 2022, Hispanic Americans had the lowest debt at an average of $4,150, compared to Black Americans at $4,360. Those who identify as another ethnicity held the second highest credit card debt, at an average of $5,910 for 2022.

The higher credit card debt of white Americans indicates that they are either borrowing higher amounts on credit cards, struggling more to pay back existing credit debt or a combination of the two.

Gender also seems to play a role in credit card debt. The Federal Reserve Board and the Financial Industry Regulatory Authority found that, while men and women often have similar credit balances, women are much more likely to engage in credit card behaviors that lead to higher debt. This includes only making minimum monthly payments, carrying credit balances and accruing late fees.

How much total debt exists in the U.S.?

Overall, U.S. debt continues to rise. Over the past four years, it has increased by more than $3.35 trillion and totals $17.5 trillion as of 2023. At this time, the burden of debt has fallen heavily on the middle generations — Generation X and millennials ages 30 and older. While credit card debt is significant, mortgage debt remains the highest and more greatly impacts the older generations. Regardless, debt continues to rise across the board for all generations, demographics and debt categories.

FAQ

How much credit card debt does the average American have?

With a population of 336.33 million and a total credit card debt of about $1.13 trillion in 2023, if spread evenly among the population, the average American would have about $3,360 in credit card debt.

How much debt does the average 30 year old have?

In 2023, 30- to 39-year-olds held a total of $210 billion in credit card debt. Since there are about 45.58 million people in the U.S. between those ages, each individual in that age group would have a little over $4,607 in debt.

Which age group holds the most credit card debt?

Those between the ages of 40 and 49 had the most credit card debt in 2023, totaling $260 billion.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Federal Reserve Bank of New York, “Household Debt and Credit Report (Q4 2023).” Accessed Apr. 23, 2024.

- United States Census Bureau, “U.S. and World Population Clock.” Accessed Apr. 23, 2024.

- Board of Governors of the Federal Reserve System, “Board Survey of Consumer Finances, 1989 - 2022.” Accessed Apr. 23, 2024.

- Board of Governors of the Federal Reserve System, “Gender-Related Differences in Credit Use and Credit Scores.” Accessed Apr. 23, 2024.

- Financial Industry Regulatory Authority, “In Our Best Interest: Women, Financial Literacy, and Credit Card Behavior.” Accessed Apr. 23, 2024.

Figures