Cities Where It’s Cheaper To Buy a Home Than Rent 2026

+1 more

Summer is just around the corner — and with it, peak moving season. Are you weighing whether to re-sign your lease or start looking to buy a home? There’s a litany of factors to consider, from your personal budget, savings and other financial goals to the temperature of the local housing market and macroeconomic conditions. But in the recent environment of rising home sales prices, mortgage rates and home insurance costs, it’s become increasingly difficult for first-time buyers to enter the housing market.

Over the past decade, the typical monthly costs of owning a home have increased by nearly 140%, pushing prospective buyers to defer their homeownership dreams or abandon them altogether. According to Lawrence Yun, chief economist at the National Association of Realtors, the impacts of tariffs and “trade wars,” including China's possible sale of mortgage-backed securities and U.S. government bonds, could lead to even higher mortgage rates and increased construction costs, pushing home prices even further out of reach.

However, you might be surprised to learn that in some cities, owning a home is actually a better deal than renting — and not just in the long term. The ConsumerAffairs Research Team compared median rents and monthly home payment data from 384 metro areas between 2015 and 2025 to find where it’s more affordable to own a home than rent. Read on for our principal findings.

Nationally, owning a home is 45% more expensive than renting in 2025 — a sharp increase from 2015, when the monthly costs of homeownership and renting were almost exactly the same.

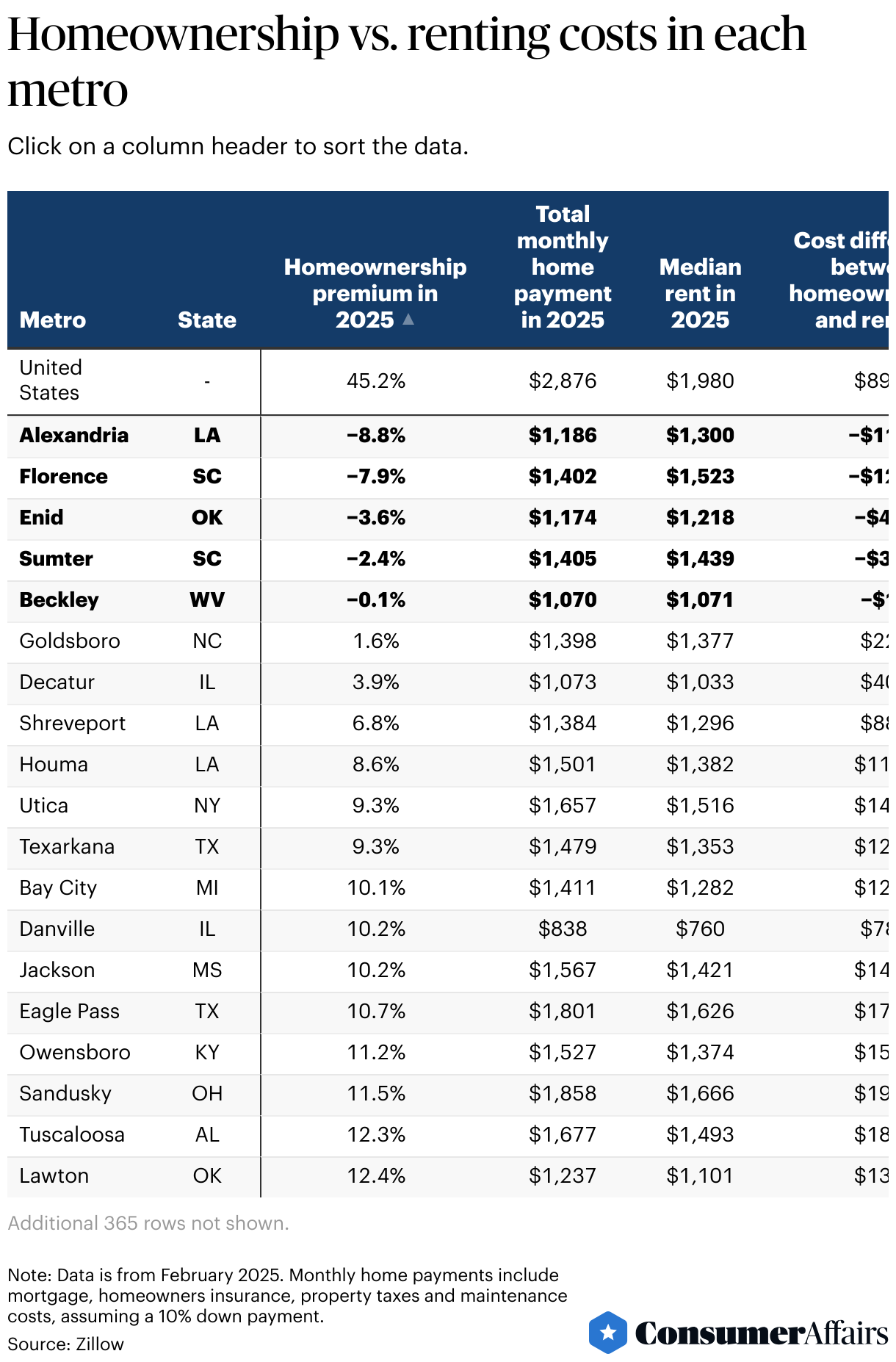

Jump to insightOnly five U.S. metro areas offer more affordable homeownership than renting in 2025. Alexandria, Louisiana, leads the list, where owning a home costs 8.8% less than renting.

Jump to insightAll five cities where owning a home costs less than renting are located in the South.

Jump to insightSan Jose, California, has the biggest cost gap in the nation — owning a home is 285.9% more expensive than renting. It also has the highest monthly home payment at $12,627.

Jump to insightHow rents and homeownership costs have shifted

Newcomers to the housing market may be surprised to learn that 10 years ago, the costs of renting and homeownership in the U.S. were almost the same. In 2015, the typical monthly home payment and the median rent price were each just over $1,200. Then, it cost just 84 cents more a month to own a home than to rent, on average.

Over the past decade, median rents have increased by almost 65%, mortgage rates have nearly doubled and home prices have soared to historic highs. However, a dramatic gap has widened between the costs of renting and homeownership. As of February 2025, the national median rent approaches $2,000 a month, but typical monthly home payments have risen to nearly $2,900. That creates a difference (or “homeownership premium”) of more than 45%.

Note the sharp spike in the monthly home payment cost from 2021 onward. The timing is no coincidence — home prices have increased by approximately 45% since 2020, which translates to larger mortgage payments. An analysis from the National Bureau of Economic Research estimates that at least half of the increase in national house prices from 2019 to 2022 was caused by the shift to remote work amid the pandemic.

Rising home values and increasingly frequent severe weather events like hurricanes, tornadoes and wildfires have driven up home insurance premiums, too, compounding the financial burden for current homeowners — and the financial barrier for prospective buyers.

Cities where owning a home costs less than renting

In most places, homeownership has become even harder to afford, especially for first-time buyers looking to escape the rental cycle. And homeowners aren’t the only ones feeling the squeeze — since 2020, median rents have risen by 32% nationwide.

Of the nearly 400 metro areas we compared, it’s cheaper to own a home than to rent in just a handful of cities, all in the South. Dive deeper into the data with our ranking of the cities where homeownership is a better deal.

1. Alexandria, Louisiana

In Alexandria, Louisiana, it’s nearly 9% cheaper each month to own a home than to rent — the most significant “homeownership discount” in the nation. Affordable home prices and low property taxes play a role: Home values in Alexandria average about $130,000, or just over a third of the national average of $361,263, and Louisiana has some of the lowest property taxes in the nation, with a 0.55% effective rate.

Median monthly rent: $1,300

Typical monthly home payment: $1,186

Difference between homeownership costs and renting: -8.8%

2. Florence, South Carolina

Homeowners in Florence, South Carolina, pay nearly 8% less each month than renters do. A hot rental market plays a significant role in making homeownership a better deal. Florence has the highest median rent of the five cities where it’s cheaper to own.

Median monthly rent: $1,523

Typical monthly home payment: $1,402

Difference between homeownership costs and renting: -7.9%

3. Enid, Oklahoma

Within a couple hours’ drive of both Tulsa and Oklahoma City is Enid, where residents can save more than 3.5% on housing costs by owning a home instead of renting. Enid has the eighth-lowest typical monthly home payment among all of the metro areas we compared, and Oklahoma’s low cost of living can help new homeowners decrease their spending on other essentials.

Median monthly rent: $1,218

Typical monthly home payment: $1,174

Difference between homeownership costs and renting: -3.6%

4. Sumter, South Carolina

Sumter, South Carolina, joins nearby Florence on our list, giving the Palmetto State not one but two metro areas where homeownership is more affordable than renting. In Sumter, residents typically save about $35 a month by owning a home, a difference of almost 2.5%.

Median monthly rent: $1,439

Typical monthly home payment: $1,405

Difference between homeownership costs and renting: -2.4%

5. Beckley, West Virginia

Beckley, West Virginia, offers the smallest cost gap between owning and renting of all the cities we compared. Just 50 cents separates the typical monthly cost of owning a home from the median monthly rent, a razor-thin margin of 0.05%. Among the cities where it’s more affordable to own than rent a home, Beckley also has the lowest typical monthly home payment: about 63% lower than the national average of $2,876.

Median monthly rent: $1,070.67

Typical monthly home payment: $1,070.17

Difference between homeownership costs and renting: -0.05%

Homeownership vs. renting costs in each metro

Unfortunately, the five cities listed above are exceptions to the rule: In 379 of the 384 metro areas we investigated, it costs more each month to own a home than to rent. The peak example: San Jose, California, where a typical home payment exceeds the median rent by $9,354 a month. However, several cities boast “homeownership premiums” of less than 10% — like Goldsboro, North Carolina, where the typical monthly home payment is just $22 higher than the median rent.

Check out the full dataset below to see how the costs of homeownership and renting compare in your city — or to explore which cities could offer you a more affordable path to homeownership.

Rent or buy? How to decide what’s right for you

If you’re considering whether to rent or buy, chances are you’ve already begun crunching the numbers on your monthly budget and done some initial searching — or scrolling — of available homes in your area.

Are you ready to dig deeper into whether to rent or buy? Read on for some key factors to consider when determining whether renting or buying is the right choice for your current situation, plus perspectives from housing market experts and current renters with a variety of views on homeownership.

Buying a home

Watching homeownership costs climb in recent years has been discouraging for aspiring homeowners, but if your city has a steep homeownership premium or ranks low on our list of best cities for first-time homebuyers, don’t despair. A single data point doesn’t need to be a death sentence to your dreams of owning a home.

"Historically, homeowners have seen financial gains over time, regardless of specific rent-to-own calculations at any given moment,” said Yun, the chief economist at NAR. “The key is to stay within budget and avoid overextending financially, allowing time to build wealth steadily.”

Researching the typical rents and home prices in your chosen area is a good place to start. Tools like mortgage calculators can help you figure out how much “house” you can afford based on your income, amount saved for a down payment and other fixed monthly expenses. There’s a wealth of resources for first-time homebuyers, including loans and other programs to help you navigate the complex homebuying process.

One key tip for affording your first home: Explore your options for down payments. A survey by the nonprofit research organization Urban Institute found that 68% of renters said that saving for a down payment was an obstacle to homeownership, and nearly 2 in 5 renters believed that they’d need a down payment of at least 20% to buy a home. However, a 20% down payment is not necessary for most borrowers. For example, a first-time homebuyer loan from the Federal Housing Administration (FHA) can have a down payment requirement as low as 3.5%.

Renting long-term

For some Americans, renting feels like the best fit, and not just in the short term. Take Caleb H., a 30-year-old financial consultant and comedy show producer in Atlanta. Despite an upwardly mobile career and minimal debt, he has no plans to pursue buying a home.

“I really feel like I missed the boat on anything that resembles a good deal on a house,” Caleb said. It’s not just a feeling: In Atlanta, homeownership is currently 64% more expensive than renting, with a typical monthly home payment of almost $3,100. Compare that with 2015, when there was only a 6% premium on homeownership — a difference of just $62 a month.

Caleb is especially concerned that home prices could “fall out of the bottom,” like they did in the financial crisis of 2007 to 2009. “The possibility that homes are not a stable investment is very real,” he said. “It’s happened in my lifetime.”

He also cited the cost of maintaining a home and intentions to eventually move out of state as a few other reasons he’s not looking to pursue homebuying any time soon. “There’s a lot of money that goes into keeping the house alive,” he said. “Why would I put myself at financial risk now, for a period where I’m already liking the flexibility of renting?”

Buying, selling, then renting again

Whatever variables you’re weighing, know that a path to homeownership isn’t necessarily linear. Consider LJ, who recently bought and sold her first home in Mississippi and now rents in Massachusetts.

In 2025, the typical monthly home payment in Jackson, Mississippi, is about 10% higher than the median monthly rent. But in 2021, when LJ purchased her home there, the typical monthly home payment was almost 17% less expensive than renting.

“I ended up buying because renting would have been way more expensive at the time,” she said. “Not having a huge salary, it just made more sense (to buy).”

When a dream job opportunity arose in the Bay State in early 2025, LJ took the leap. She quickly sold her house in Jackson and moved to Massachusetts, where she’s now renting and taking a “wait-and-see” approach to buying her next home. In the nearby Pittsfield, Massachusetts, area, homeownership costs outpace median rents by 78%. LJ anticipates that the housing market may fluctuate amid economic uncertainty — hopefully, in her favor.

The bottom line

Only you can decide if you’re ready and willing to pursue homeownership.

- Renting has its upsides: Compared with homeownership, it’s more flexible, it involves less responsibility for upkeep, and it’s more affordable in the vast majority of metropolitan areas in the U.S.

- Buying a home comes with maintenance and repair costs that renters don’t have to worry about, but it’s also a key way to grow your wealth by building home equity. (According to a recent report by the Aspen Institute, renters in the U.S. have just 3% of the wealth of homeowners. Said another way, the average homeowner has more than 30 times the wealth of an average renter.) Getting a home warranty and homeowners insurance can also help you handle the cost of home repairs.

If you’re daunted by all the variables of the housing market — or by the task of saving for a down payment — take a step back to remember the big picture. Homeownership is a big investment, but it can offer significant stability, especially if you’re in a market with rapidly climbing rents.

“The cost of your monthly mortgage is fixed, (whereas) rent rises regularly,” said Jennifer Murphy, vice president at Homeownership Council of America. “Any purchase (of a home) would give you long-term fixed housing costs that are eventually paid off. Rent is never paid off.”

Methodology

The research team at ConsumerAffairs analyzed data from 384 metropolitan areas to identify the U.S. cities where it’s cheaper to own a home than rent.

We used Zillow data from February of each year between 2015 and 2025 to find the total monthly cost of homeownership, assuming a 10% down payment. This includes the mortgage payment, homeowners insurance, property taxes and maintenance costs. The payment estimates are based on the typical home value in each metro, as defined by the Zillow Home Value Index. We compared that with the median monthly rent in each metro area, also sourced from Zillow during the same period.

To determine whether owning or renting is more affordable, we calculated the “homeownership premium” by finding the difference between the typical monthly home payment and the median rent. A negative value indicates it’s cheaper to own than rent.

For questions about the data or if you'd like to set up an interview, please contact acurls@consumeraffairs.com.

Reference policy

We love it when people share our findings! If you do, please link back to our original article to credit our research.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Zillow, “Housing Data.” Accessed April 18, 2025.

- Freddie Mac, “Mortgage Rates.” Accessed April 18, 2025.

- Reuters, “US existing home sales rise in December; house prices hit record high in 2024.” Accessed April 18, 2025.

- Axios, “How the pandemic transformed the housing market in 5 years.” Accessed April 18, 2025.

- National Bureau of Economic Research, “Housing Demand and Remote Work.” Accessed April 18, 2025.

- Tax Foundation, “Property Taxes by State and County, 2025.” Accessed April 18, 2025.

- Urban Institute, “Barriers to Accessing Homeownership Down Payment, Credit, and Affordability.” Accessed April 18, 2025.

- The Aspen Institute, “From Rent to Riches? A Profile on the Wealth and Financial Well-Being of Renter Households.” Accessed April 18, 2025.

Figures