The most (and least) expensive states for health care

+1 more

Health spending in the U.S. has reached an all-time high of $4.5 trillion per year. That means about $1 out of every $5 spent in the U.S. is going toward health care, and consumers across the country are feeling the pinch in their pocketbooks. According to recent polling from the health policy research organization KFF, about half of U.S. adults say it's difficult to afford health care costs, and 1 in 4 say they or a family member in their household had problems paying for health care in the past 12 months.

However, not all Americans face the same burden when it comes to the cost of health care. Health insurance plans come with a much higher price tag in some states. For example, the average annual premium for a silver-tier Affordable Care Act marketplace plan is $320 in New Hampshire but $1,275 in neighboring Vermont. Approximately 1 in 10 Americans skipped seeing a doctor in the past 12 months due to cost, but the rate is nearly three times higher in Texas than it is in Hawaii.

To make sense of the data and compare costs side by side, the ConsumerAffairs Research Team ranked all 50 states and Washington, D.C., by health care costs, considering average annual premiums and deductibles, the percentage of residents forgoing care due to cost and the percentage of children whose families have difficulty paying medical bills.

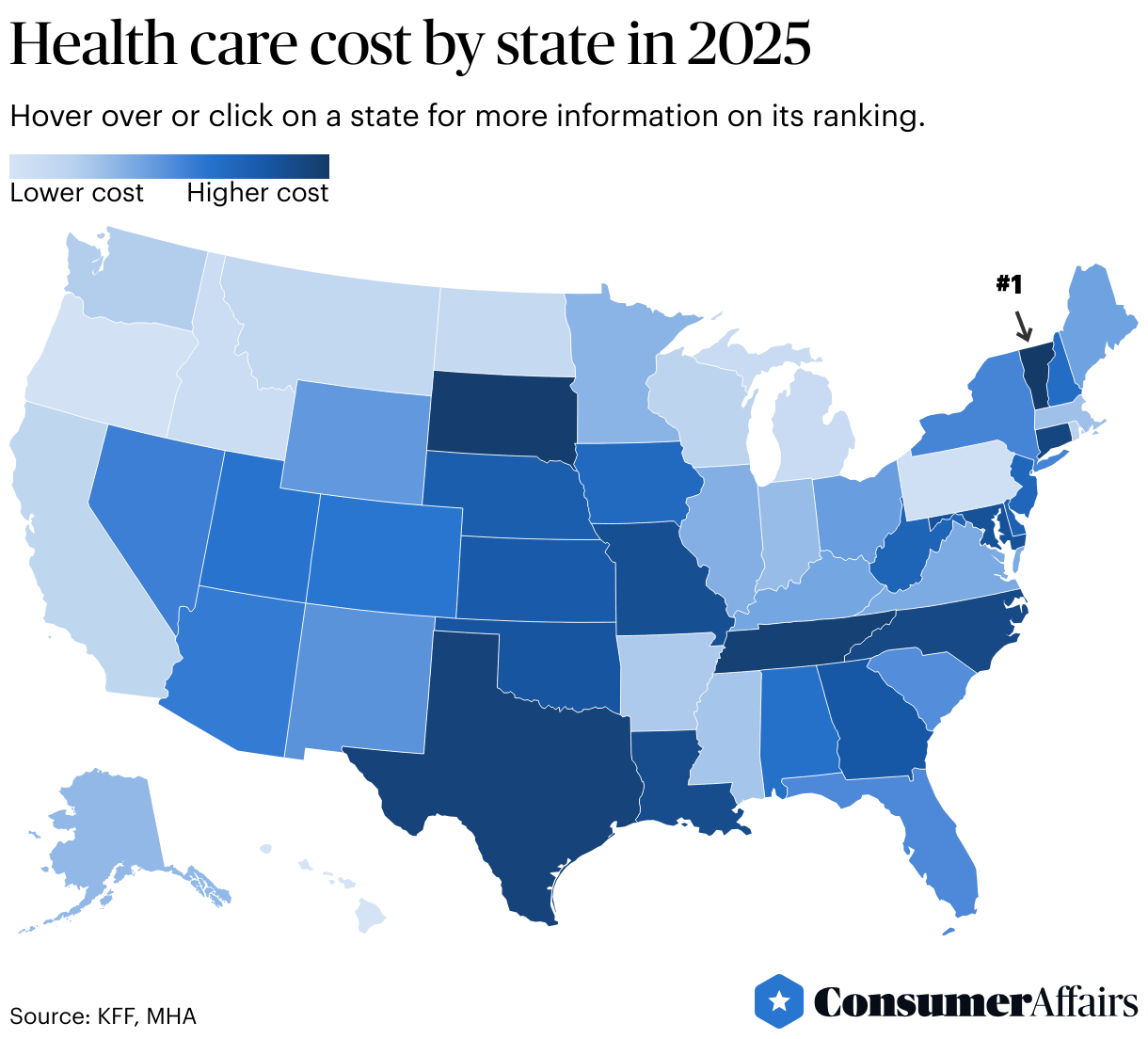

Vermont is the most expensive state for health care, while Hawaii is the most affordable.

Jump to insightSix of the 10 most expensive states for health care are in the South: Tennessee, Texas, North Carolina, Louisiana, Maryland and Oklahoma.

Jump to insightFive out of the 10 most affordable states for health care are in the West: Hawaii, Oregon, Idaho, Montana and California.

Jump to insightAbout 1 in 6 Texas residents skipped seeing a doctor in the past year due to costs, the highest rate in the nation.

Jump to insight

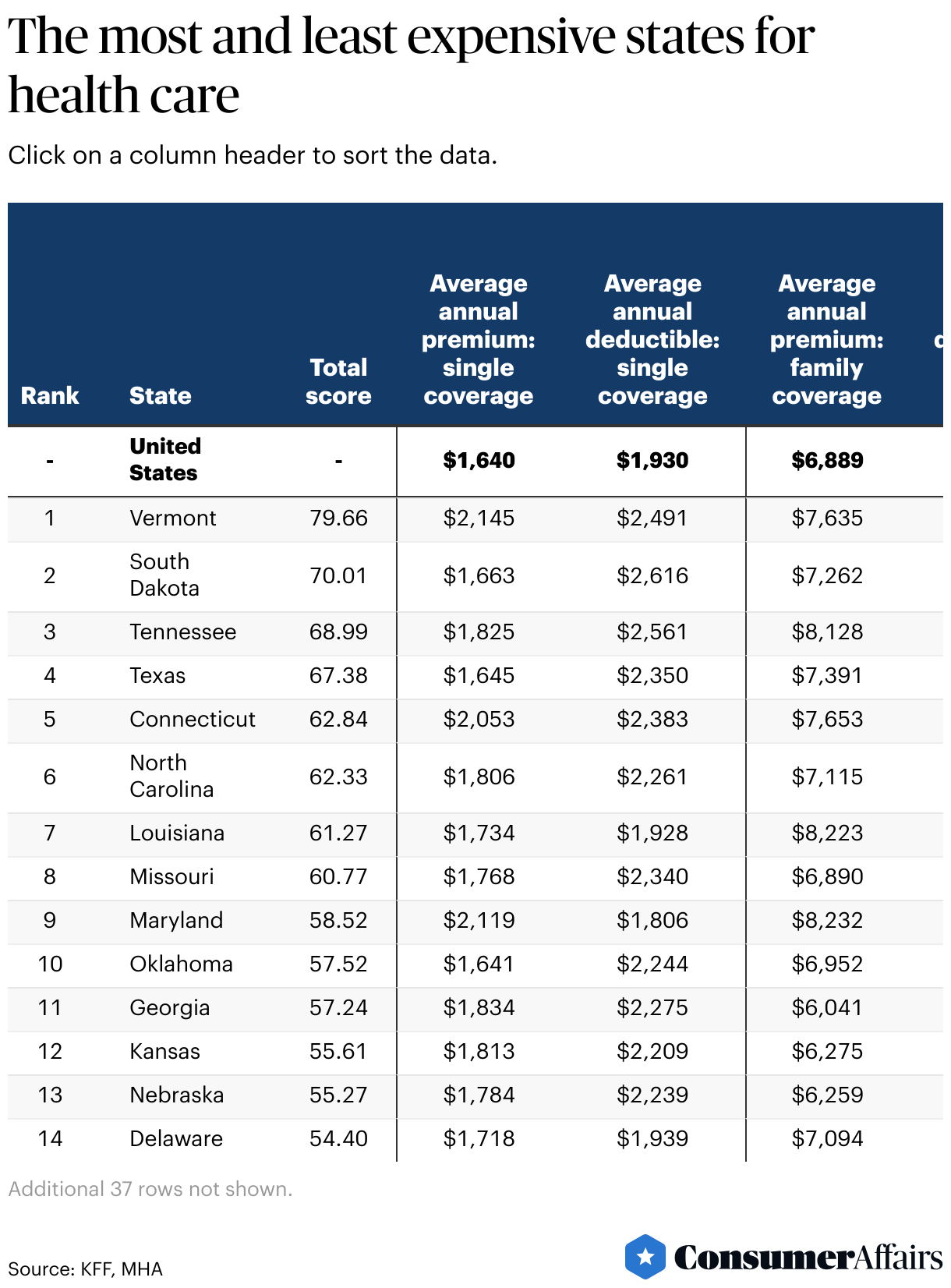

The five most expensive states for health care

High health insurance costs drove five states to the top of our list. On average, residents in these states pay $4,346 each year in annual premiums and deductibles for coverage for a single person, nearly 22% higher than the national average. However, not all of the most expensive states reported high rates of skipping health care services due to cost.

1. Vermont

79.66 out of 100 points

With some of the highest premiums and deductibles in the country, Vermont tops our list as the most expensive state for health care in 2025. This may not come as a surprise to some: Our cost of living study found that Vermont is among the most expensive states to live in.

Despite high health insurance costs, Vermont residents aren’t as cost-burdened by health care expenses as those in other states — just 6.1% of Vermonters skipped a doctor’s appointment due to cost, the second-lowest rate in the country. Other key findings:

- Highest overall costs for single insurance coverage: $4,636 average annual cost

- Average annual premium: $2,145, the highest of all states

- Average annual deductible: $2,491

- Most expensive average premium for a silver-tier health plan: $1,275 per year, almost triple the national average

2. South Dakota

70.01 out of 100 points

Deductibles and premiums are high in South Dakota, especially for family coverage. The average annual cost of family health insurance coverage (annual premiums plus deductible) in the Mount Rushmore State is the second highest in the U.S.

However, South Dakota dispels — or at least complicates — the notion that a high cost of living and high health care costs are innately intertwined. South Dakota’s cost of living is among the lowest in the country. Noteworthy stats include the following:

- Highest average annual deductible for family coverage: $5,004 per year

- Highest average deductible for single coverage: $2,616 per year

- Third-most expensive annual premium for plus-one coverage: $5,278 per year

3. Tennessee

68.99 out of 100 points

Tennessee contains some of the most affordable cities in the U.S., but health care costs in the state are far from cheap. In fact, Tennessee is the most expensive state for family health insurance coverage, based on the combined costs of annual premiums and deductibles for a family health plan.

Health care costs are a challenge for insured and uninsured Tennesseans alike. In a 2021 survey of adults in the state by Altarum, nearly half (48%) of uninsured adults in Tennessee said the high cost of premiums was the major reason they lacked coverage, far surpassing other reasons like not needing coverage or not knowing how to acquire it. The following metrics stood out:

- Highest overall costs for family insurance coverage: $12,362 average annual cost ($8,128 average annual premium plus $4,234 average annual deductible)

- Second-highest average deductible for single coverage: $2,561 per year

- Third-highest average premium for family coverage: $8,128 per year

4. Texas

67.38 out of 100 points

The saying “everything’s bigger in Texas” appears to hold true when it comes to health care costs. Texas residents are among the most cost-burdened by health care expenses; the state has the highest percentage of adults who have forgone health care services because of cost. Texas also has the largest uninsured population in the country, with 16.6% of the population lacking public or private coverage.

Interestingly, an increasing demand for GLP-1 medications like Ozempic is one factor contributing to rising costs for employer-provided health coverage, according to the Texas Association of Health Plans.

Some notable metrics from our source data:

- Highest percentage of adults who didn’t see a doctor due to cost: 16.4%

- Second-highest percentage of adults who skipped mental health due to cost: 34.4%

- Fourth-highest percentage of children whose families struggled to pay for their children’s medical bills: 12.4%

5. Connecticut

62.84 out of 100 points

Connecticut’s high average costs for premiums and deductibles rank it the fifth-most expensive state for health care. Connecticut residents may not find this surprising: Our 2023 cost of living analysis identified Connecticut’s cost of living as the fourth highest in the nation.

Like Vermonters, Connecticuters are actually less cost-burdened by health care expenses than many other states. Cost prohibited only 8.1% of adults in Connecticut from seeing a doctor in the past 12 months (about 2 points below the national average) and 18.3% from getting mental health care (more than 6 points below the national average). However, Connecticut ranks as one of the most expensive states for other key stats:

- Second-highest overall costs for single insurance coverage: $4,436 average annual cost ($2,053 average annual premium and $2,383 average annual deductible)

- Fourth-highest annual premium for single coverage: $2,053 per year

The five most affordable states for health care

Lower health insurance premiums and deductibles help give these five states — including three in the West — the cheapest health care costs in the country.

1. Hawaii

17.94 out of 100 points

Hawaii ranks as the least expensive state for health care. Despite its reputation for high cost of living (and topping our list of most expensive states to live), it has some of the lowest health insurance premiums and deductibles in the nation. It also has the lowest rates in the country of adults forgoing doctor’s visits and mental health care due to cost.

Some experts have identified Hawaii’s Prepaid Health Care Act as a key factor in keeping health care costs low. According to a report from the UC Berkeley Labor Center, this legislation helps keep insurance costs low by capping premiums by income and creating a large risk pool with many young, low-risk participants. Ultimately, Hawaii boasts the following stats:

- Lowest average premium and deductible for single insurance coverage: $1,060 premium and $1,059 deductible per year

- Lowest rate of children from families struggling to pay medical bills: 6.1%

2. Oregon

18.11 out of 100 points

In the Beaver State, cost of living doesn’t always correspond with health care costs. We ranked Oregon’s cost of living among the highest in the U.S., but the state falls among the least expensive for health care across several key metrics, including the lowest average annual costs for family insurance coverage (premium plus deductible). Notable figures include:

- Lowest average premium for family coverage: $4,142 per year, 40% less than the national average

- Second-lowest average premium for single coverage: $1,082 per year

- Lowest average premium for plus-one coverage: $3,222 per year

3. Pennsylvania

26.26 out of 100 points

Pennsylvania is the third-most affordable state for health care overall and the only Northeastern state to rank within the top 10 most affordable states. The state’s average combined annual costs for family coverage (premium plus deductible) are the fourth lowest in the nation, and the state is the most affordable in other metrics:

- Lowest average deductible for family coverage: $2,665 per year

- Fourth-lowest average premium for plus-one coverage: $3,729 per year

4. Washington, D.C.

31.51 out of 100 points

Low average deductibles for single and family coverage helped land Washington, D.C., among the most affordable places for health care in the U.S. The capital also has one of the lowest rates of children whose families are struggling to pay for their medical bills.

Washington’s strong metrics may be supported in part by the DC Department of Insurance, Securities and Banking (DISB), which reviews insurers’ rates to make sure premiums are priced fairly. In 2024, DISB required rate decreases that will save residents almost $1.5 million in 2025. Check out these key stats:

- Third-lowest average deductible for family coverage: $2,830 per year

- Second-lowest average deductible for single coverage: $1,328 per year

- Seventh-lowest percentage of children whose families are struggling to pay their child’s medical bills: 7.1%

5. Idaho

31.59 out of 100 points

Idaho, the only landlocked state to rank in the top five for affordability, has some of the lowest annual premiums across coverage types. However, it lands closer to the middle of the pack for metrics that measure how much health care cost is a barrier to access — the percentages of Idaho adults that didn’t see a doctor or obtain mental health care due to cost, 10.6% and 26%, respectively, are both slightly higher than the national average.

Other noteworthy metrics:

- Low costs for average single-coverage premium: $1,186 per year, fourth-lowest overall

- Low average premium for single plus-one coverage: $3,866 per year, ninth-lowest in the country

How do your state’s health care costs compare?

Researchers have identified that differences in cost of living, market competition and share of the population enrolled in Medicare or Medicaid can contribute to the differences in health care costs between states. If you're curious about how your state compares, explore the full cost breakdown in the table below.

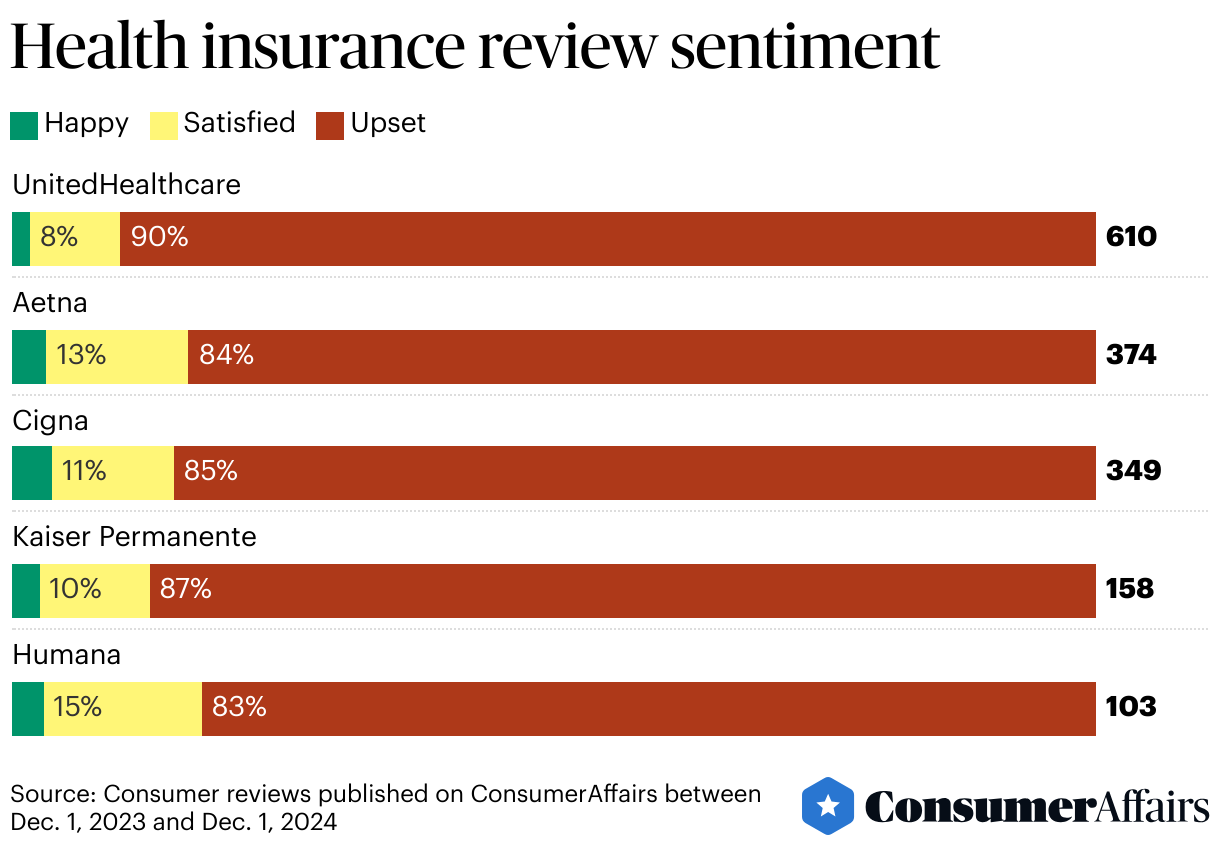

Public perception of health insurance companies in America

More than 305 million people (approximately 92% of the population) have some form of health insurance, but just 4% of adults have a great deal of trust in health insurance companies to improve the health care system. Nearly 6 in 10 insured adults report having experienced a problem with their health insurance in the past 12 months, and more than two-thirds of Americans feel that health insurance companies provide only fair or poor services.

The cost of health insurance may be one key factor driving negative sentiment. Fewer than 1 in 5 Americans are satisfied with health care costs, and more than 1 in 10 adults (both insured and uninsured) in the U.S. didn’t see a doctor in the past 12 months because of cost. Among adults without insurance, the rate is about five times higher.

To better understand current public sentiment toward health insurance companies in the U.S., we analyzed ConsumerAffairs review data for five major providers: UnitedHealthcare, Kaiser Permanente, Humana, Aetna and Cigna Healthcare. Each verified reviewer is classified as happy, satisfied or upset based on the information and experiences they report.

UnitedHealthcare, the nation’s largest health insurance company, with 29 million members, received the highest number of poor reviews among the five major insurance providers on ConsumerAffairs. Over the past year, 90% of UnitedHealthcare reviews on our site expressed dissatisfaction. Some takeaways:

- Customers commonly reported issues such as unauthorized changes to primary care physicians, claim denials, poor customer service, difficulty finding in-network providers and high deductibles.

- Many reviewers accuse the company of denying necessary treatments and medications and feel that UnitedHealthcare prioritizes profits over patient care.

Aetna, Cigna, Kaiser Permanente and Humana, four of the largest health insurance companies, also received largely negative reviews, with an average 85% dissatisfaction rate on our site. Some recurring themes in these reviews include difficulties finding in-network providers, denials or delays of necessary treatments and medications, and poor customer service.

6 tips for minimizing health care costs

Whichever health insurance provider you choose — and no matter which state you call home — there are some steps you can take to help manage the costs of coverage and care.

- Choose the right insurance plan for your needs.

Take stock of what your health care needs have been in the past year and what you anticipate they will be in the year to come. If you’re not anticipating frequent doctor's visits or costly treatments, a high deductible plan with low monthly premiums can help keep more money in your pocket. - Get an FSA or HSA.

Opt for a plan that offers a health savings account (HSA) or a flexible spending account (FSA). According to the National Library of Medicine, you can save several hundred dollars each year by contributing pretax money from each paycheck to these accounts and putting those funds toward eligible expenses, like prescriptions, dental care, vision-related needs and other treatments. - Use in-network providers.

Prices are almost always lower when you go to doctors, clinics and hospitals that are “in-network” for your health care plan. Your health insurance provider should have an online tool or list to help you find in-network health care providers in your area. - Optimize prescription costs.

Whether you’re already taking prescription medication or preparing to start a new one, ask your doctor if you can switch to a generic medicine. You may also have lower prescription copays if you order a 90-day supply or order by mail. Search websites like GoodRx, NeedyMeds and RxAssist for coupons or rebates. - Know your options for urgent and emergency care.

Some illnesses and injuries are too severe to wait for an appointment with your primary care provider, but not all issues warrant a trip to the hospital. The National Library of Medicine offers the following guidelines to determine whether you should go to urgent care or head to the ER: “If a person or unborn baby could die or have permanent harm, it is an emergency. Examples include chest pain, trouble breathing, or severe pain or bleeding. If you need care that cannot wait until the next day to see your provider, you need urgent care. Examples of urgent care include strep throat, bladder infection, or a dog bite.” - Take care of your body and your health.

While it might not put extra dollars in your pocket in the short term, taking care of your health can set you up to have fewer health care costs in the future. Maintaining healthy habits with diet, exercise and sleep can help reduce your risk of chronic conditions like diabetes or heart disease.

Methodology

To rank the most and least expensive states for health care, we compared all 50 states and Washington, D.C., across nine key metrics. For each metric, the state with the highest cost or percentage was given the maximum score, with others scoring relative to that state. Each metric contributes to an overall score out of 100. Higher scores are associated with more expensive health care costs.

Employer-based health insurance premiums

- Single-coverage average annual premium per employee (14.5 points) (KFF, 2023)

- Plus-one coverage average annual premium per employee (14.5 points) (KFF, 2023)

- Family coverage average annual premium per employee (14.5 points) (KFF, 2023)

Employer-provided health insurance deductibles

- Single-coverage average annual deductible per employee (14 points) (KFF, 2023)

- Family coverage average annual deductible per employee (14 points) (KFF, 2023)

Affordable Care Act marketplace health insurance premium

- Silver-tier health plan average annual premium (14 points) (KFF, 2025)

Affordability barriers

- Percentage of adults who skipped doctor's visits due to cost in past 12 months (6.5 points (KFF, 2022-2023)

- Percentage of adults reporting 14-plus mentally unhealthy days per month who could not see a doctor due to cost (4 points) (Mental Health America, 2024)

- Percentage of children whose families struggled to pay child’s medical bills in past 12 months (4 points) (KFF, 2023)

For questions about the data or if you'd like to set up an interview, please contact acurls@consumeraffairs.com.

Reference policy

We love it when people share our findings! If you do, please link back to our original article to credit our research.

Article Sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- KFF, “Average Annual Single Premium per Enrolled Employee For Employer-Based Health Insurance.” Accessed Jan. 1, 2025.

- KFF, “Average Annual Employee-Plus-One Premium per Enrolled Employee For Employer-Based Health Insurance.” Accessed Jan. 1, 2025.

- KFF, “Average Annual Family Premium per Enrolled Employee For Employer-Based Health Insurance.” Accessed Jan. 1, 2025.

- KFF, “Average Annual Deductible per Enrolled Employee in Employer-Based Health Insurance for Single and Family Coverage.” Accessed Jan. 1, 2025.

- KFF, “Average Marketplace Premiums by Metal Tier, 2018-2025.” Accessed Jan. 1, 2025.

- KFF, “Adults Who Report Not Seeing a Doctor in the Past 12 Months Because of Cost by Race/Ethnicity.” Accessed Jan. 1, 2025.

- KFF, “Percent of Children Whose Families Had Trouble Paying Bills for Child’s Medical or Health Care Bills in Past 12 Months.” Accessed Jan. 1, 2025.

- Mental Health America, “Access to Care Ranking 2024.” Accessed Jan. 1, 2025.

- KFF, “Health Care Costs and Affordability.” Accessed Jan. 1, 2025.

- KFF, “Americans’ Challenges with Health Care Costs.” Accessed Jan. 1, 2025.

- Altarum, “Tennessee Residents Struggle to Afford High Healthcare Costs; COVID Fears Add to Support for a Range of Government Solutions Across Party Lines.” Accessed Jan. 1, 2025.

- United Health Foundation, “Uninsured in Texas.” Accessed Jan. 1, 2025.

- Texas Association of Health Plans, “Texas Employers Absorb Rising Health Premiums Amid Surging GLP-1 Costs.” Accessed Jan. 1, 2025.

- UC Berkeley Labor Center, “Hawaii’s Prepaid Health Care Act.” Accessed Jan. 1, 2025.

- District of Columbia “DC Announces 2025 Health Insurance Rates, with Rate Increases Smallest in Recent Years.” Accessed Jan. 1, 2025.

- U.S. Census Bureau, “Health Insurance Coverage in the United States: 2023.” Accessed Jan. 1, 2025.

- Harvard T.H. Chan School of Public Health, “AMERICANS’ VALUES AND BELIEFS ABOUT NATIONAL HEALTH INSURANCE REFORM.” Accessed Jan. 1, 2025.

- KFF, “KFF Survey of Consumer Experiences with Health Insurance.” Accessed Jan. 1, 2025.

- Gallup, “Healthcare System.” Accessed Jan. 1, 2025.

- Gallup, “View of U.S. Healthcare Quality Declines to 24-Year Low.” Accessed Jan. 1, 2025.

- National Library of Medicine, “Eight ways to cut your health care costs.” Accessed Jan. 1, 2025.

Figures