40% of Americans need a loan right now, nationwide survey finds

+2 more

Citing challenges with inflation, surprise expenses and less money for household bills, a staggering 4 in 10 American consumers say they need a loan to make ends meet today, according to a nationwide survey.

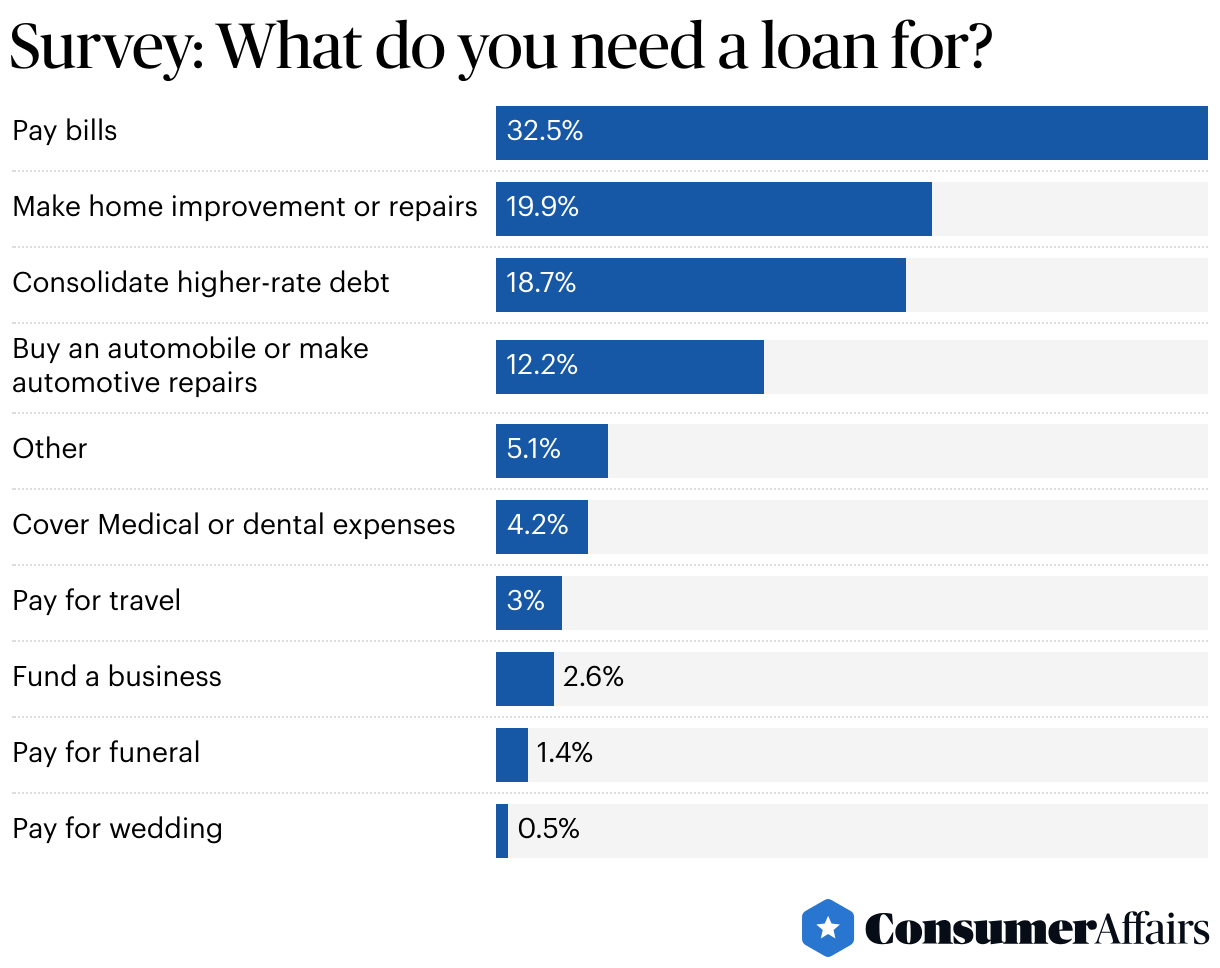

Among those who were looking to borrow funds, about one-third (32.5%) said they’d use the funds simply to cover bills, underlining the ongoing economic challenges still impacting households three years after the onset of the pandemic. Nearly 60% of the people surveyed said they found it more difficult or were unable to pay all monthly bills in the past year.

The survey was conducted by ConsumerAffairs via SurveyMonkey between Jan. 18 and Jan. 19, 2023, and included 1,070 respondents. The margin of error is three percentage points.

We dig into all of these statistics and more in this report.

Two in five people need a personal loan — many to pay their bills. Over 40% said they need a personal loan, and 32.5% of those respondents said they need one to pay their bills.

Jump to insightRising interest costs and inflation have made it harder for people to pay their bills. Just over 50% have had a harder time paying all their monthly bills, and 9.4% can’t pay them.

Jump to insightIncreases in household income haven’t kept pace with rising living costs. About 67% said their household income has decreased or stayed the same in the last year.

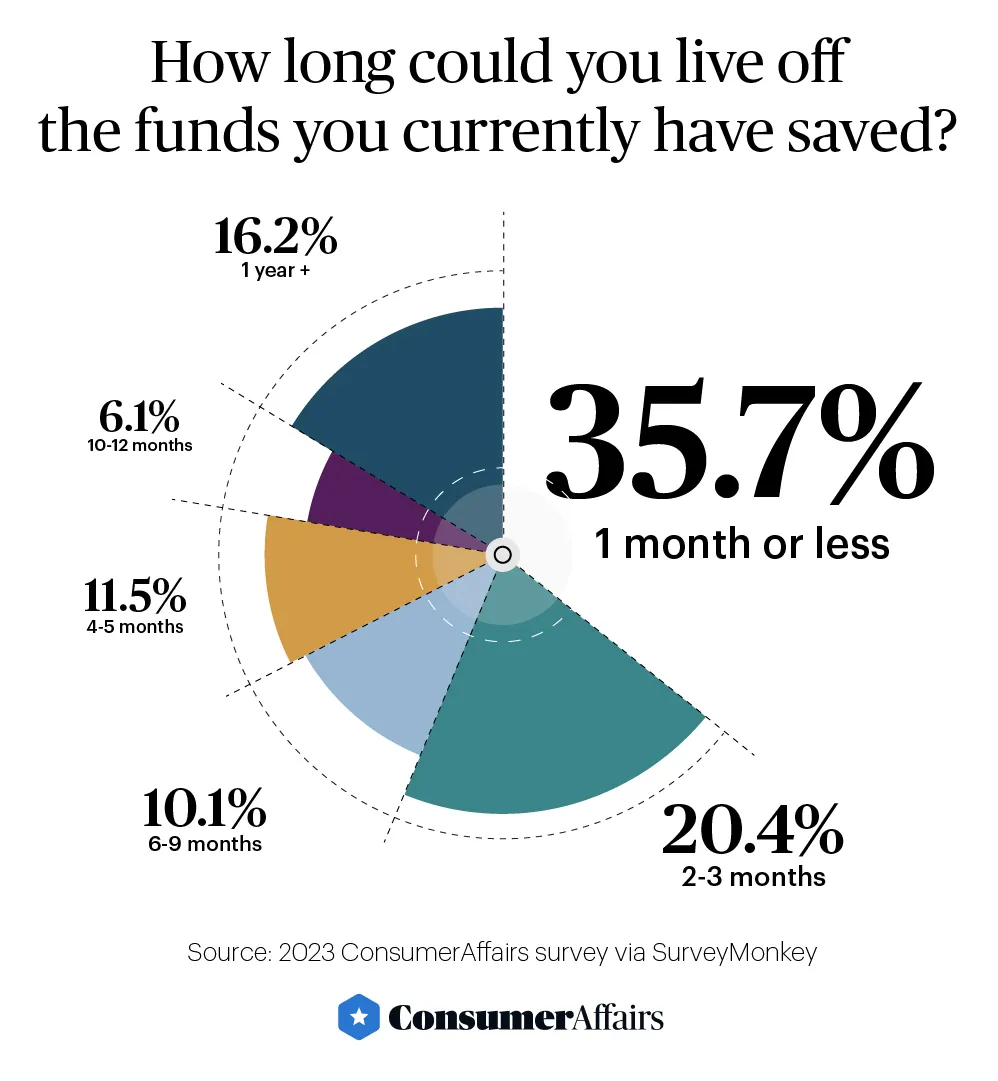

Jump to insightSavings are being drained. About 42% of people said their savings rates have declined in the last 12 months. About 36% of people could only live off their savings for a month or less.

Jump to insightA third of those who need a personal loan need it to pay bills

The survey asked, “Do you need a personal loan right now?” More than 40% of the survey participants said yes, and 31.3% said they have looked into one in the last 12 months.

Besides the 32.5% who said they would use the funds to pay bills, 18.7% said they needed a personal loan to consolidate higher-rate debt. Most respondents who said they needed a loan said they would seek $5,000 or less. A plurality said they would seek between $1,000 and $2,500, but over 3 in 10 said they needed $10,000 or more. The median answer was $2,500 to $4,999.

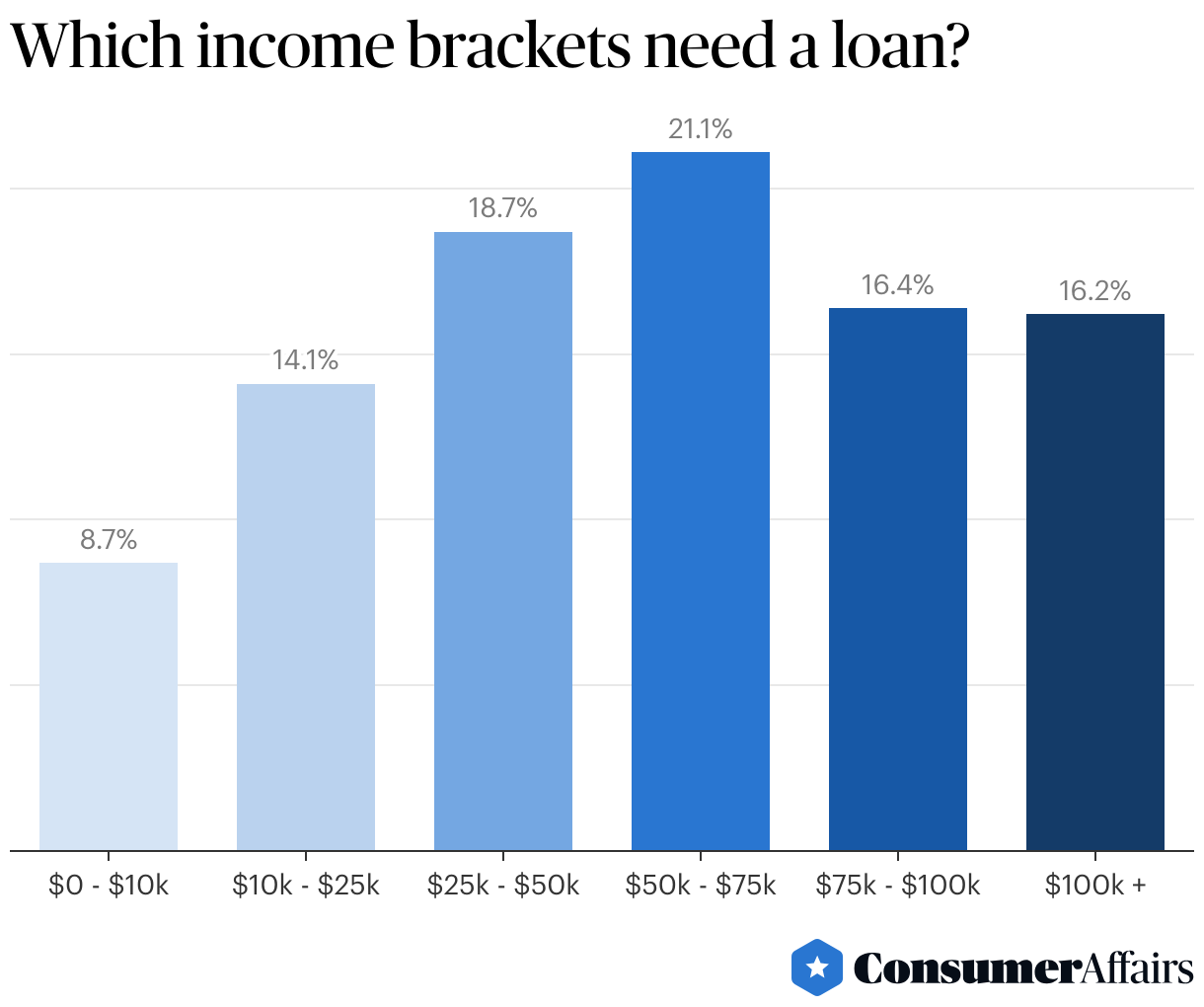

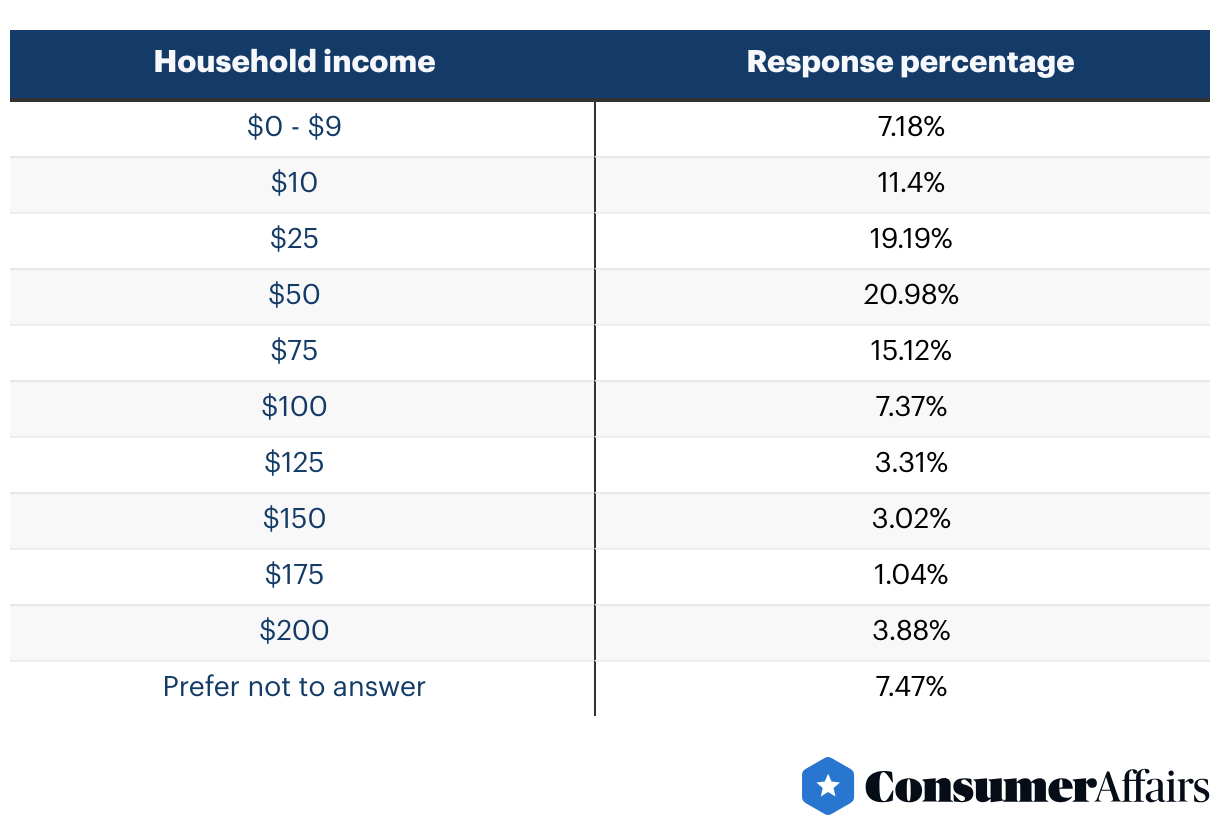

The need to take on debt crossed all income brackets. About 54% of those who said they need a personal loan earn $50,000 or more a year. Nearly one-third earn $75,000 or above.

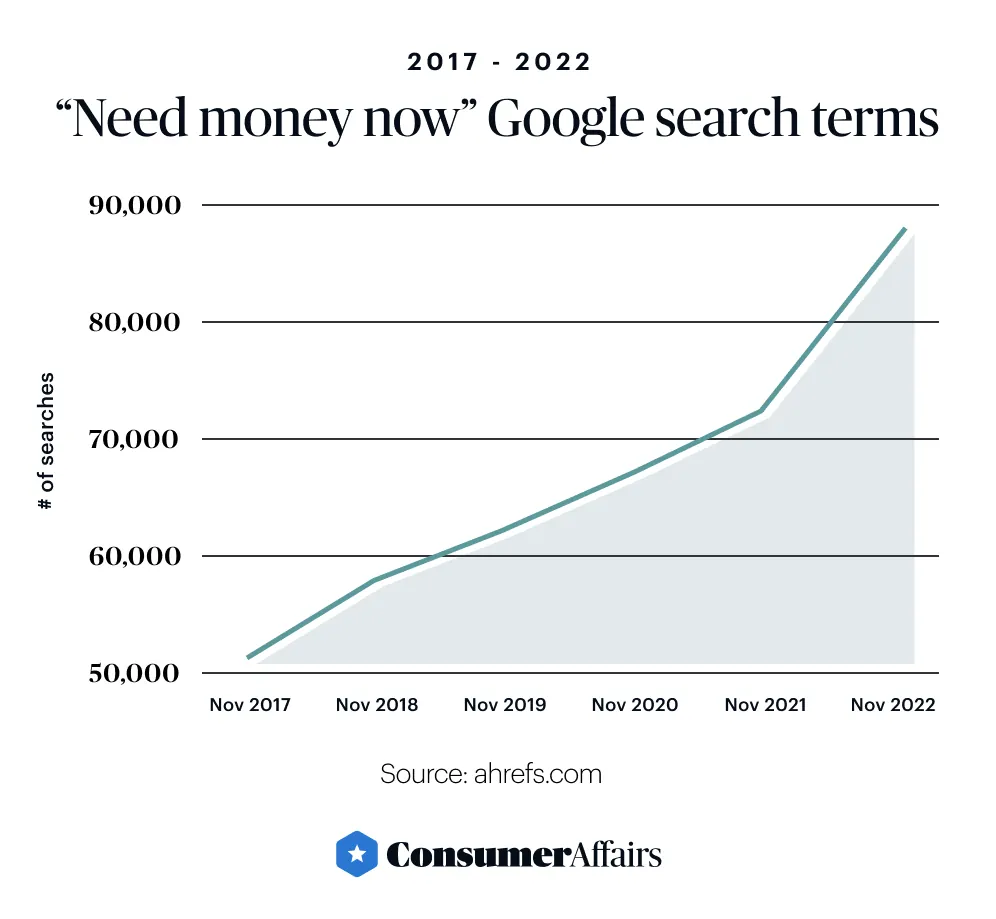

Google search trends confirm the growing number of Americans leaning into debt to make ends meet. More than 88,100 consumers searched in November 2022 for “I need a personal loan now,” “need money now” and similar terms.

These searches rose 18% over 12 months and have risen 41% since November 2019, when 62,512 people typed in those keywords.

Inflation’s rise in 2022 is a big reason people need a loan in 2023

The survey found vivid evidence that scores of Americans have spent recent months feeling the troubling effects of inflation on their bank accounts and credit cards.

Consumer prices for all items increased by 6.4% from January 2022 to January 2023, and the prices of food, shelter and energy rose even higher, according to the U.S. Bureau of Labor Statistics. Fuel oil prices, for example, increased by 27.7%.

As a result, the national ConsumerAffairs survey showed that about 60% of Americans found it more difficult or were unable to pay all monthly bills in the past year. Among those who said they needed a personal loan, that figure rose to over 75%.

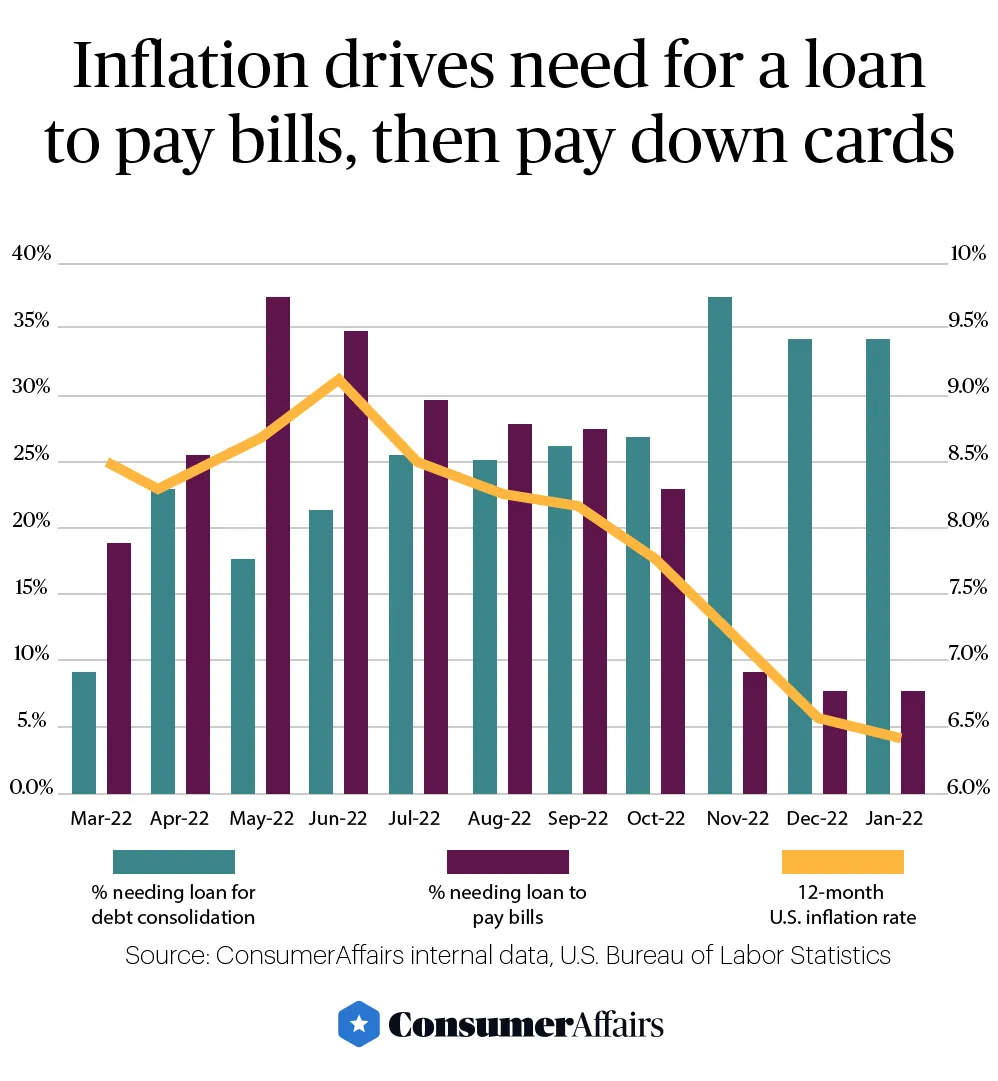

This picture of loan seekers mirrors the one created from March 2022 to January 2023 by 247,700 consumers who have used a ConsumerAffairs online tool to get information about potential personal loan providers.

On the tool, 21.5% of loan seekers said they would use a loan simply to pay bills, while 28.5% needed it to consolidate their higher-interest debt.

As inflation rose in the first six months of 2022, peaking in May and June, as many as 35% of loan seekers using the ConsumerAffairs tool needed the funds to pay higher bills. By year’s end, inflation may have eased, but more loan seekers (up to 37%) needed funds to consolidate higher-interest credit card debt.

To this point, 2022 data published by the Federal Reserve Bank of New York shows consumer credit card balances increased from $887 billion in the second quarter to $925 billion in the third quarter to $986 billion in the fourth quarter. Meanwhile, delinquencies of 30 or more days on credit card payments increased from 4.76% in the second quarter to 5.24% and 5.87% in the third and fourth quarters.

Many consumers who need a personal loan in 2023, it appears, need it to pay down credit card debt run up last year.

Unexpected or major expenses also take a toll

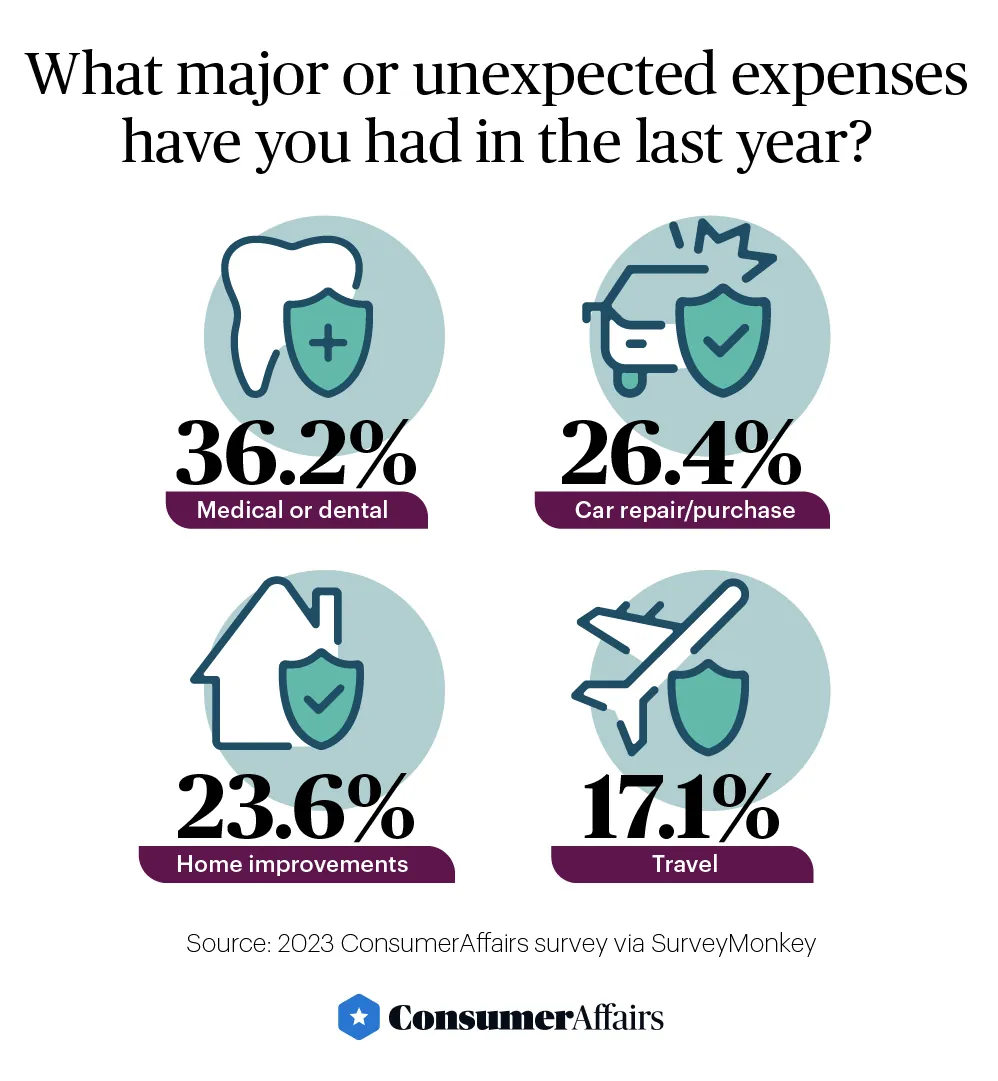

According to our national survey, another factor, unexpected expenses, caused 60% of Americans to draw down a checking or savings account or take on more credit card debt last year.

Unexpected or major medical or dental expenses landed on 36.2% of Americans. Automobile purchases or repairs impacted 26.4% of respondents; home improvements, 23.6%; and pet medical or dental bills, 17.9%.

Among those who said they had major or unexpected expenses, 28.4% of Americans took on credit card debt, 27% drew down cash or checking accounts and 18.6% dipped into savings simply to pay for unexpected or major expenses.

All told, 81.2% of Americans had to pay for an unexpected or major expense during the past 12 months.

The result: More than a third of Americans have only a month or less of cash in the bank to live off

Personal finance experts who’ve studied the financial ups and downs of Americans suggest that households need three to six months of savings in case of an unexpected expense. But half of respondents reported that their cushion isn’t remotely sufficient.

Nearly 42% of those surveyed said their savings rates declined last year. Most worrisome, about 36% said they only have enough savings to live off for a month or less.

Among those who needed a personal loan and made less than $100,000 a year, a staggering 47.2% said they could only live for a month or less off their savings.

The median duration of how long Americans can live off their savings, the ConsumerAffairs survey found, is two to three months.

Behind the need for a “personal loan”

About 11% of households in 2021 carried a personal loan, according to research by the Federal Deposit Insurance Corporation. Personal loans generally carry lower interest rates than credit cards and, with repayment schedules of 24 or 36 months or longer, can be an option for consumer debt that doesn’t have to be paid off right away.

But “personal loan” also can be a colloquial term with other meanings, the survey confirmed.

Of those who said they needed a personal loan, 16.4% said they meant a debt consolidation loan, while 11.2% specified a credit card advance, 10.3% meant a loan from family and friends, and 6.8% indicated needing a home equity line of credit or home equity loan.

About 54% of loan seekers responded that they specifically needed a personal loan; 61.4% said they actually had looked into one in the past 12 months.

Most of those who said they needed a personal loan hadn’t taken one out. Only 6.5% of respondents who said they needed a personal loan used one to pay for unexpected or major expenses in the past 12 months, the survey found. About 1 in 3 used credit cards; 71.5% of American households used credit cards in 2021, according to the FDIC.

Based on results of the national ConsumerAffairs survey, personal loans look to many Americans like an emerging alternative to taking on yet more credit card debt.

Examples: getting behind the numbers

When asked via the ConsumerAffairs tool to detail a more specific reason why they needed a personal loan, respondents' answers ranged from extraordinary to everyday. Most common were those who cited automotive repair. “My transmission and motor need to be replaced or rebuilt,” said one person.

Another major need was to cover moving expenses, with one person sharing that they had to rent a moving truck to move to another town. And many planned to use the funds for their business.

One entrepreneur said, “Just got a contract and need 200 garbage toters.” Another said, “I need money to start an Amazon FBA business and to cover expenses while it goes up and running.” Several shared that they planned to use the funds to buy tools for their businesses. One needed funds to open a furniture restoration business to produce epoxy coffee tables.

Medical expenses was another common prompt, with one person explaining that they needed funds “to buy much-needed medications insurance isn’t willing to pay at this time.” Another cited an emergency, sharing, “My fiance was in an explosion and is critically injured.” Stories of funds needed to care for the health of loved ones were plentiful.

Many caregivers said they planned to use the funds to buy school supplies, with one saying: “My grandkids start school next week. Need clothes and shoes, at least for the first week of school.”

Essential debt payoff tips for Americans

With so many borrowing options out there, it’s all too easy for debt to spiral out of control, said ConsumerAffairs public advocate and personal finance expert Mandi Woodruff-Santos.

“We’re seeing how many Americans are lucky enough if they can pay their bills on time, let alone have additional income they can be setting aside and saving,” she said. “Sometimes these golden rules of thumb about having a cushion of three months just don’t match up to reality.”

Here are some tips to consider to help get debt under control:

Shop around and compare the cost of each borrowing option. Shop for loans the same way you’d shop and compare prices on a new appliance. If you’re borrowing a large amount of money, the costs are even more crucial to understand because they can seriously compound over time, Woodruff-Santos said. “For example, a personal loan offered by a credit union or online lender may have a much lower rate than the credit card in your wallet,” she added.

You can shop and compare rates on personal loan options through the ConsumerAffairs online tool.

Understand fixed- versus variable-rate loans. One of the key benefits of personal loans to pay down debt is that they offer fixed loan amounts, fixed borrowing terms and a fixed interest rate. That means borrowers will know exactly how much they owe each month and exactly when the loan will be paid off — without worrying about the lender changing the rate.

“I’m actually pleasantly surprised that people surveyed who need a personal loan actually specified that they need a debt consolidation loan, because that’s one of the best use cases for a fixed-rate personal loan,” Woodruff-Santos said. “So you not only will save money by getting rid of your higher-rate debt, but you’re also protected from interest rate changes.”

Don’t be afraid to seek outside help. If you’re severely burdened by debt, seek help from a certified credit counselor who can help you wade through your options. A good starting place is the National Foundation for Credit Counseling or this list of agencies approved by the U.S. Department of Justice.

Keep some cash in reserves if possible. Even if you have debts to pay down, prioritize maintaining some liquid cash savings for essentials like housing and utilities. “It may not feel great knowing you have debt to pay down, but if something were to happen, you at least could have peace of mind that you're able to care for yourself and your family and keep yourself healthy and safe, because you’ve protected your liquid cash savings for family expenses,” Woodruff-Santos said.

Facts about personal loans and credit cards

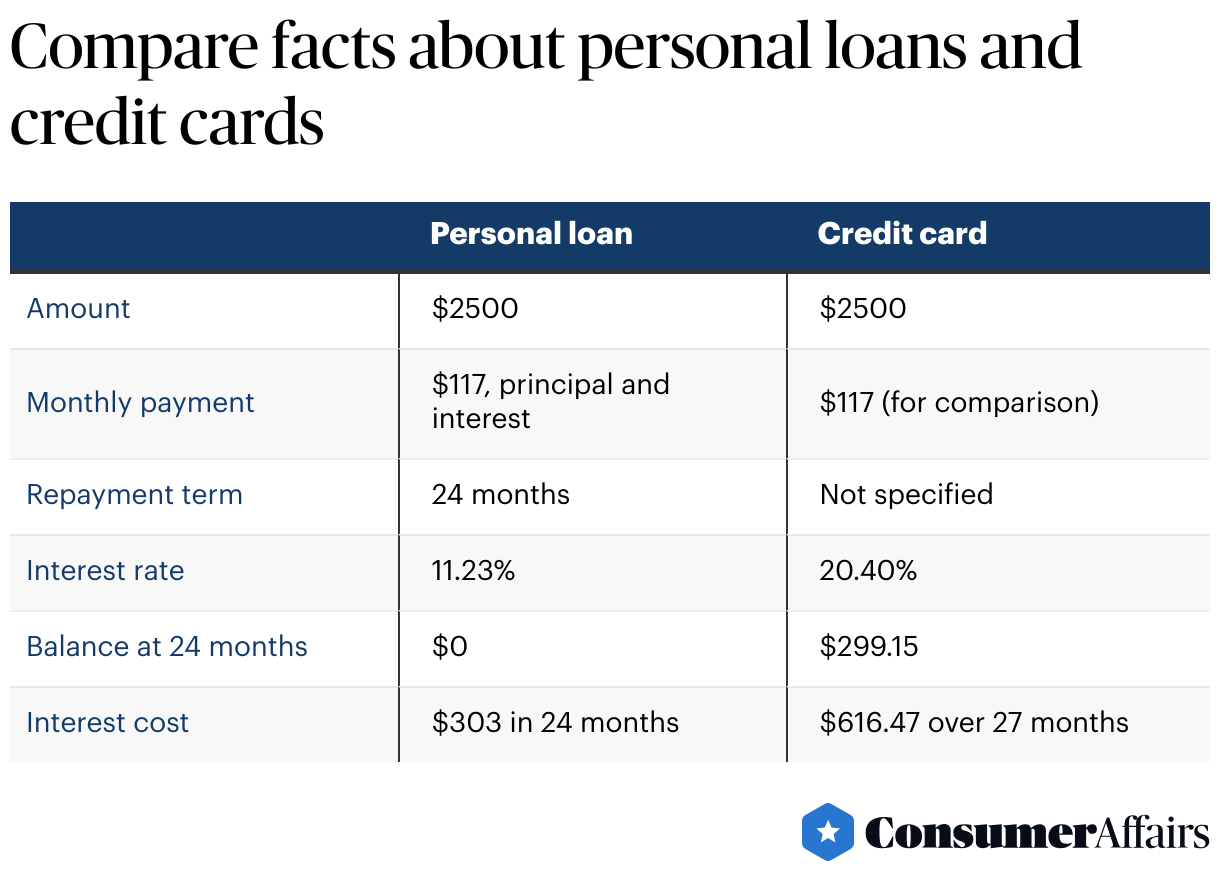

According to the latest data from the Federal Reserve (as of the publication date), the average rate on outstanding interest-bearing credit cards is 20.40%, versus 11.23% on 24-month personal loans. Other differences are:

- Credit cards carry variable rates that can increase interest payments in a rising interest rate environment, while personal loan rates are usually locked.

- Credit cards don’t have a set repayment term, and many issuers require low minimum payments (e.g., $25). So it can take consumers longer to pay off a credit card balance versus the same size personal loan.

As shown in the example below, consumers pay $303 in total interest costs on a $2,500 personal loan with a 24-month term and an interest rate of 11.23%. The loan balance is $0 at the end of the term. In contrast, making a monthly payment of that same $117 on a credit card at a 20.40% rate with the same balance takes three additional months to pay off and incurs over twice as much interest cost: $616.47.

Methodology

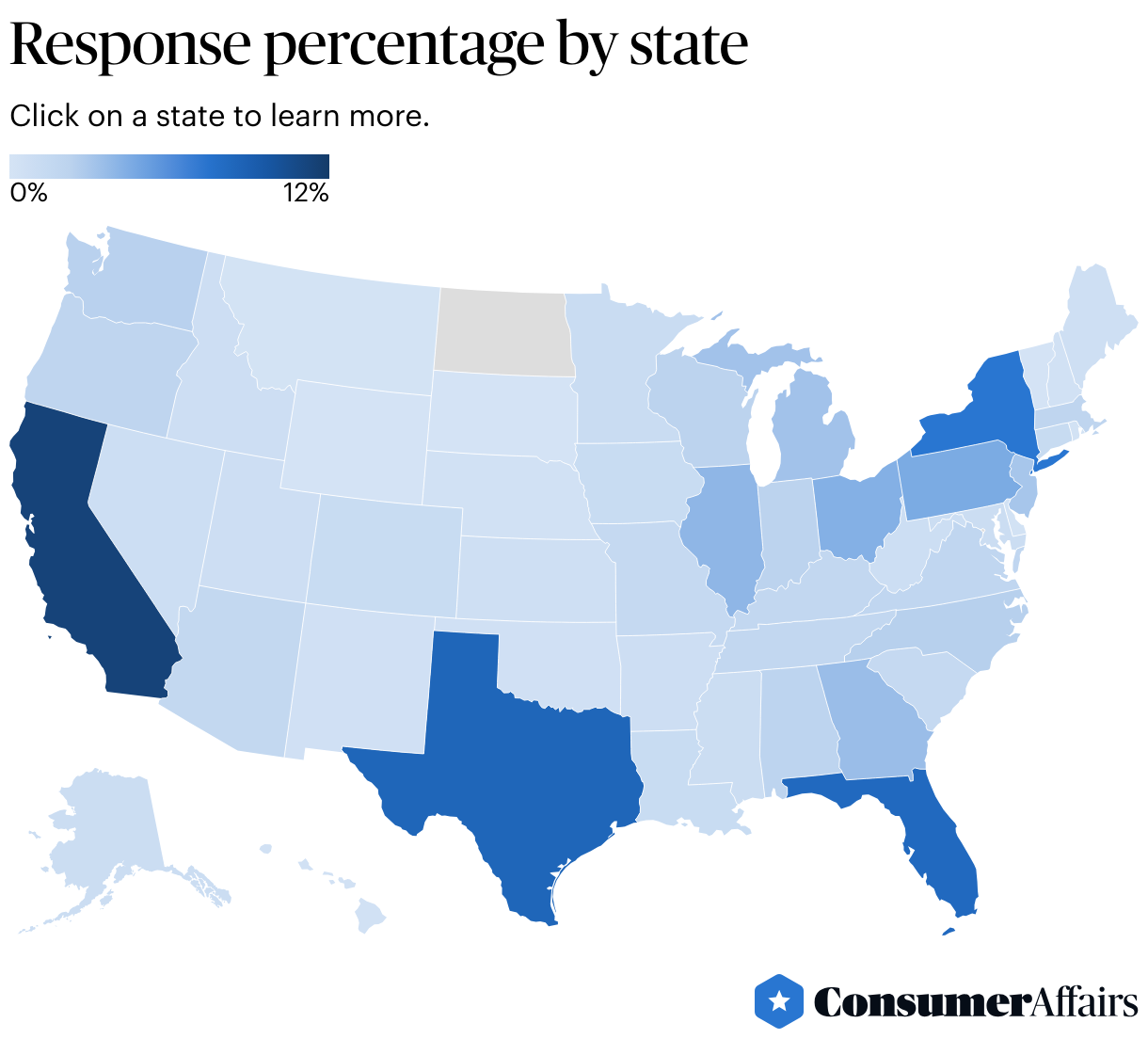

ConsumerAffairs polled 1,070 people across the United States to gather the data used in this survey. The results included responses from 49 states and Washington, D.C. All of the respondents were over 18 years old, with 47.5% of the responses provided by males and 52.5% of the responses provided by females. More survey statistics are provided below.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Federal Reserve, “Consumer Credit - G.19.” Accessed Feb. 8, 2023.

- Federal Reserve Bank of New York, “Household Debt and Credit.” Accessed Feb. 22, 2023.

- Federal Deposit Insurance Corporation, "2021 FDIC National Survey of Unbanked and Underbanked Households." Accessed Feb. 15, 2023.

- U.S. Bureau of Labor Statistics, "Consumer Price Index." Accessed Feb. 15, 2023.

Figures