How Long Does It Take to Go Broke? (2026 Data)

+1 more

We wanted to learn more about the financial well-being of the average American and how long their savings would last in different parts of the country if they lost their job today — so we surveyed over 1,000 Americans and gathered data about their average monthly expenses. Read on to find out how far a typical American’s savings would last across the U.S.

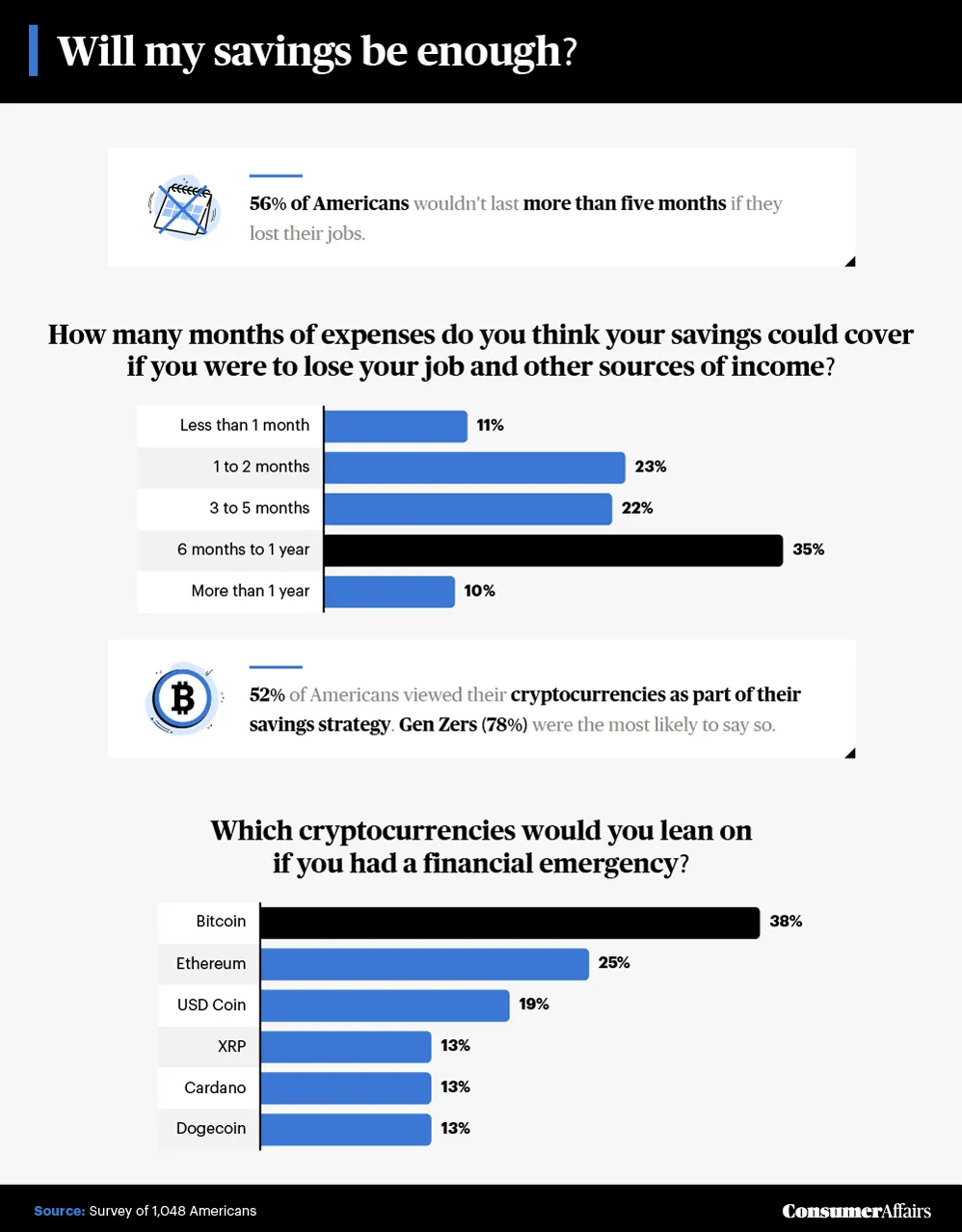

Fifty-six percent of Americans wouldn’t last more than five months if they lost their jobs.

Jump to insightMore than half of Americans see cryptocurrency as part of their savings strategy.

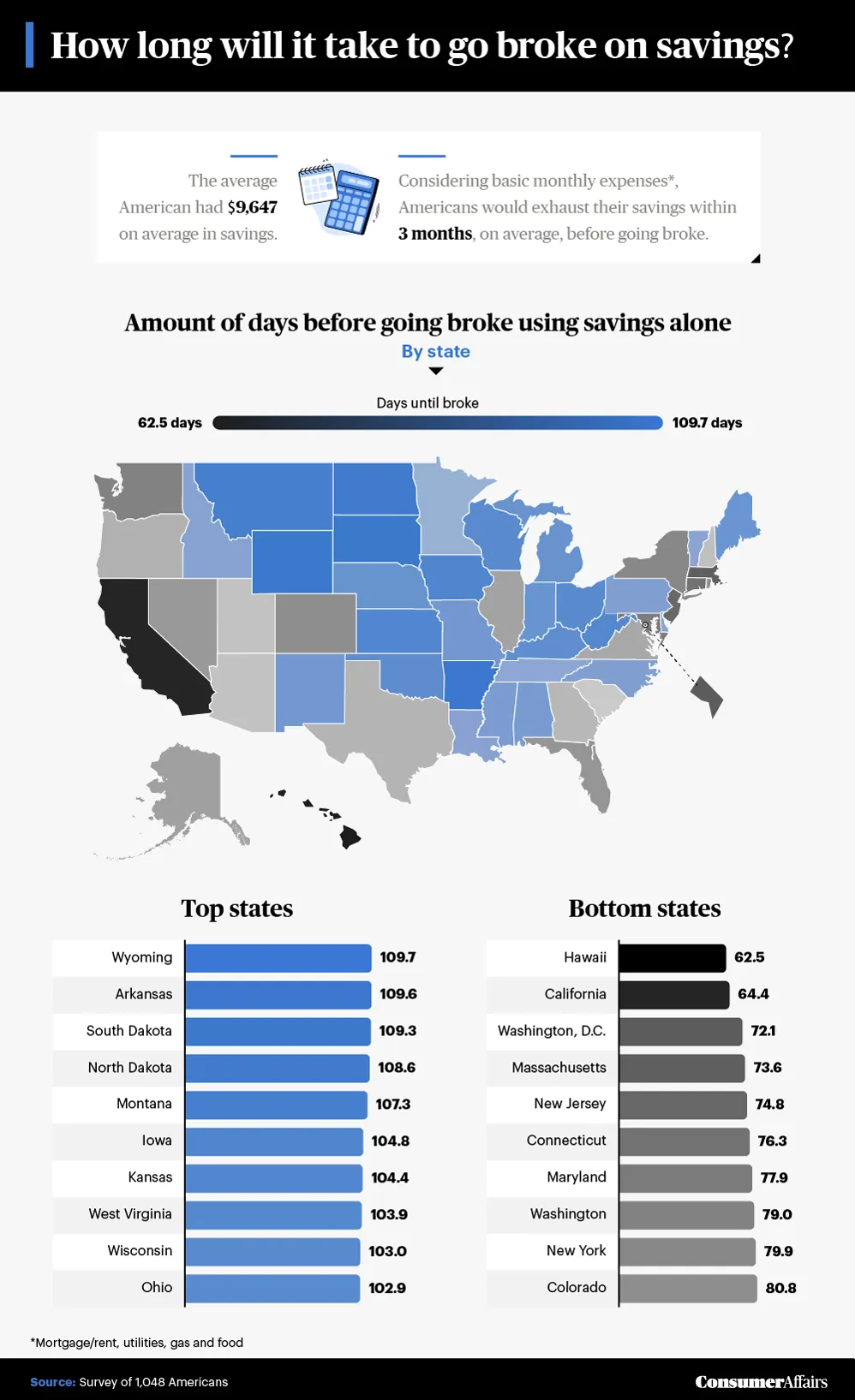

Jump to insightAmericans' savings would run out fastest in Hawaii (63 days) and last longest in Wyoming (110 days).

Jump to insightHow long can we live without an income?

How much do you have saved for a rainy day? Is it enough to get by until you land your next job? Our study found most Americans have enough savings to last them just a few months, whether they held traditional savings accounts or cryptocurrency. And, depending on where they lived, they could have even less time.

Current and future look at Americans’ finances

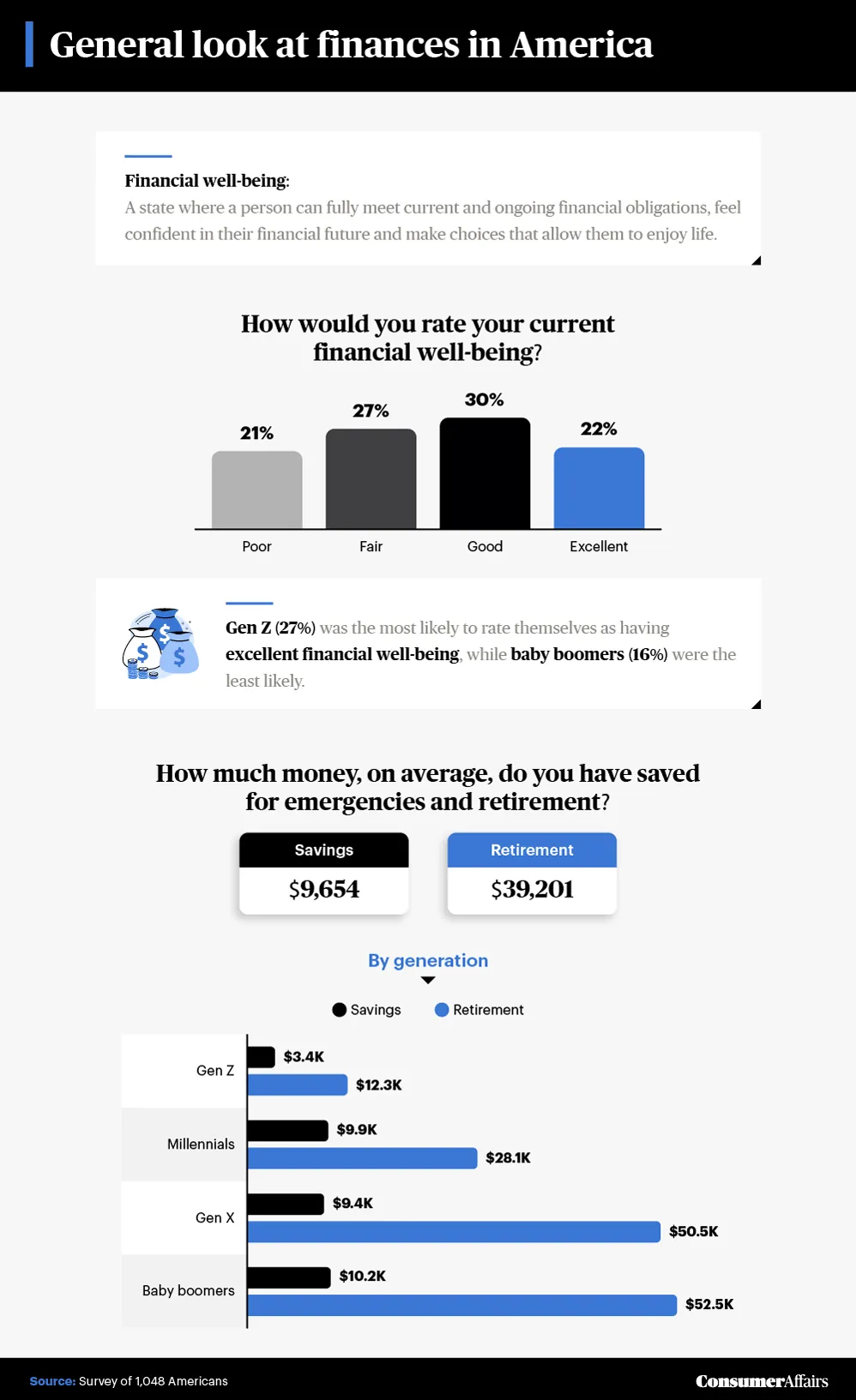

Our study used a validated scale from the Consumer Financial Protection Bureau to determine how Americans feel about their financial health. Respondents with the highest scores have higher financial well-being, while those with low scores have poorer economic health. Based on questions related to their ability to pay bills, meet lifestyle needs and contribute to savings, just over half of those we surveyed were in good or excellent financial standing.

Factors like savings and retirement accounts can play a significant role in financial health, and our study showed that savings across both these areas were higher among older generations.

While logic would indicate that the longer you’ve saved and contributed to retirement, the larger your savings, millennial and Gen X respondents reported comparable savings to those of baby boomers. Gen X also had comparable retirement savings.

So far Gen Z has struggled to save as much as the older generations, having just around a third of the average savings for all the people we studied. However, this number could be trending in a positive direction. Though Gen Z was hit hard by the COVID-19 pandemic, they’re still keen on saving — and confident about it. Gen Z was also the most likely to report excellent financial health among our respondents.

Cryptocurrency’s role in savings

Designating a portion of income to savings per paycheck or investing in cryptocurrency with expendable income may help during an emergency or job loss. However, our study found that most Americans don’t have much money to spare; many would have just a little more than a few months of savings to live on should they lose their primary source of income.

Making ends meet without an income would likely require a healthy savings account and no unexpected expenses to get through the first few months. According to a recent study, more than half of Americans can’t afford an unexpected $1,000 emergency, highlighting that job loss in the current economy would be tough to navigate for most Americans.

But innovation in the finance industry might provide new ways for generations to save and build on their money. Interestingly, younger respondents, especially Gen Z, saw cryptocurrency as a key aspect of their savings portfolio, and more than half of Americans see it as part of their long-term investment strategy. It’s clear that many Americans are starting to view crypto investments as a way forward in financially troubling times.

Where savings last the longest

In the unfortunate event of income loss, financial instability looks different from state to state due to considerable disparities in living costs. On average, most Americans would exhaust their savings within three months. But in states with lower costs of living, like Wyoming and Arkansas, recently unemployed workers could stretch their savings much longer than those in states like Hawaii or California.

Despite job loss, many strategies can help forecast your budget depending on where you live. Making a spending plan, outlining an honest budget and reviewing credit options are top recommendations from financial advisors.

With a 47-day difference between the state with the highest average time until residents go broke (Wyoming) and the state with the lowest (Hawaii), those in higher-cost areas may need to set more money aside in case of emergency. With the prevalence of remote jobs these days, relocating to areas where housing, taxes and the general cost of living is lower comes with benefits beyond emergency savings.

The impact of emergency expenses

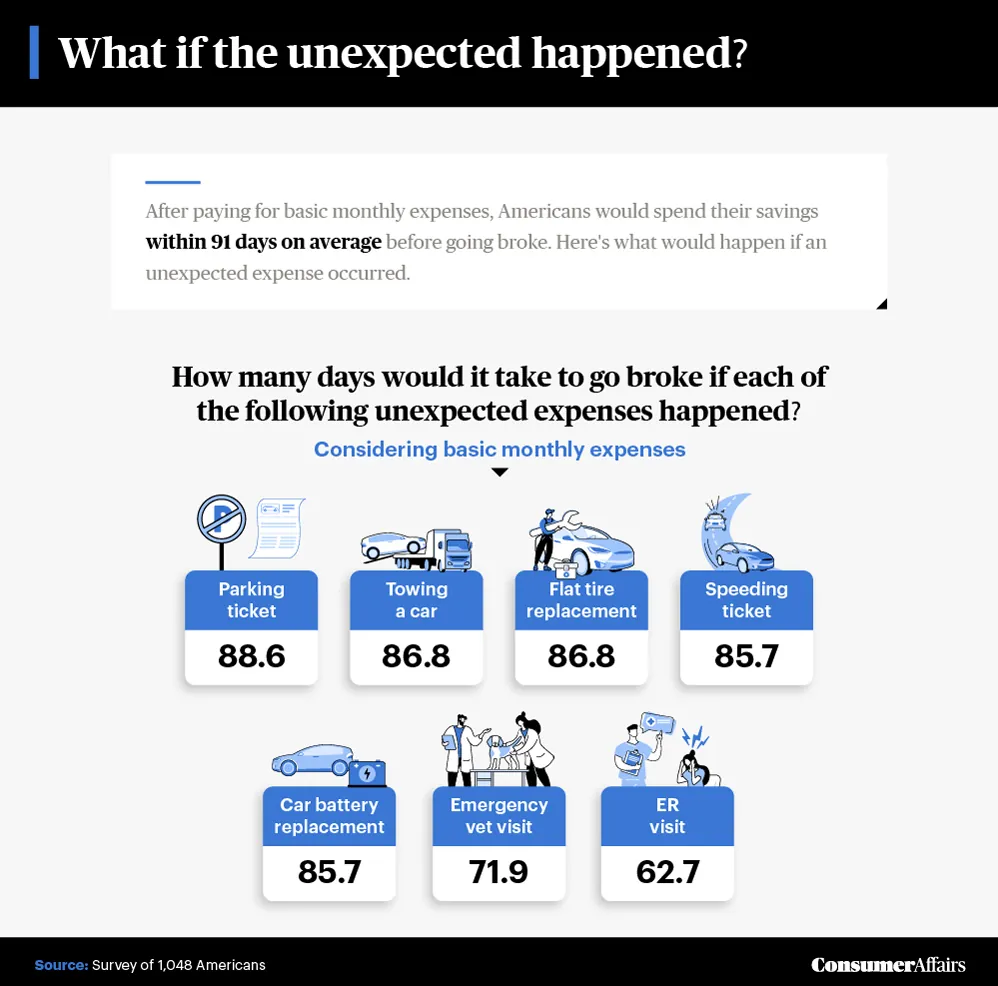

Americans facing an unexpected loss of income might encounter other challenges, like a medical emergency or a necessary vehicle repair, simultaneously. Our study found that unplanned expenses could considerably shorten the time an individual’s savings would last.

It’s probably no wonder that emergency medical expenses were the most negatively impactful event for our surveyees. Small, unexpected instances like a flat tire or a speeding ticket didn’t have a huge impact on financial stability, but with nearly two-thirds of Americans living paycheck to paycheck, our study revealed that Americans might be increasingly unprepared to manage unexpected costs amid a shrinking pool of savings.

How long will your savings last?

If you’re interested in seeing how your savings would hold up against your expenses in the event of income loss, check out our calculator below. Enter your ZIP code, monthly expenses and total savings to calculate how long your savings will last.

Summary

Our research indicates that most Americans with an average savings account would need to find new employment within one to two months of losing their job. Otherwise, they might have to go into credit card debt or make early withdrawals from a retirement account to afford their expenses while out of work. While savings strategies varied, our study found that many are banking on cryptocurrency to supplement traditional savings methods and build a safety net.

Parts of the country with lower costs of living may be particularly attractive to those looking for new opportunities and willing to relocate. Saving as much as possible and living in a low-cost area are the most effective ways to hedge against a sudden loss of income due to job turnover or a recession. These strategies can help Americans bridge the gap between jobs and avoid going broke during an emergency.

Methodology

For this campaign, we pulled data from the following sources to explore the average monthly expenses for Americans:

- World Population Review: Utilities by State

- AAA: Gas Prices

- BEA: Consumer Spending by State

- Insure.com: Cost of Living by State

- Business Insider: Average Mortgage Payment by State

- Zumper: Average Rent by State

We used the Consumer Financial Protection Bureau scale of financial well-being to determine how Americans currently feel about their financial wellness.

We also surveyed 1,048 Americans to learn about their financial well-being, the average money they have in savings and retirement funds and how prepared they’d be if they had to live solely on savings. Among them, 53% were women, 46% were men and 1% were nonbinary. The generational breakdown: 12% Gen Z, 46% millennials, 28% Gen X and 14% baby boomers.

For short, open-ended questions, outliers were removed. To help ensure all respondents took our survey seriously, they were required to identify and correctly answer an attention-check question.

Survey data has certain limitations related to self-reporting. The margin of error is plus or minus 3% with a 95% confidence interval.

About ConsumerAffairs

ConsumerAffairs.com is a comprehensive source for various investment strategies and buying decisions. We provide the information you need to increase your financial literacy and help you make educated purchases.

Fair use statement

If you enjoyed our study on American saving habits and how long savings can last after an income stoppage, please feel free to share the study for noncommercial use. Just be sure to link back to this page so our research team can receive credit for their work.