How Long Does It Take to Save for a Home in Each State? 2026

+1 more

Do you dream of owning a home but struggle with the financial realities of bringing that dream to life? Before you’re ready to talk with a mortgage lender and start seeing what’s within reach, it’s important to save a significant amount for a down payment.

But in today’s market, how big a down payment do you really need? And how long will it take to get there?

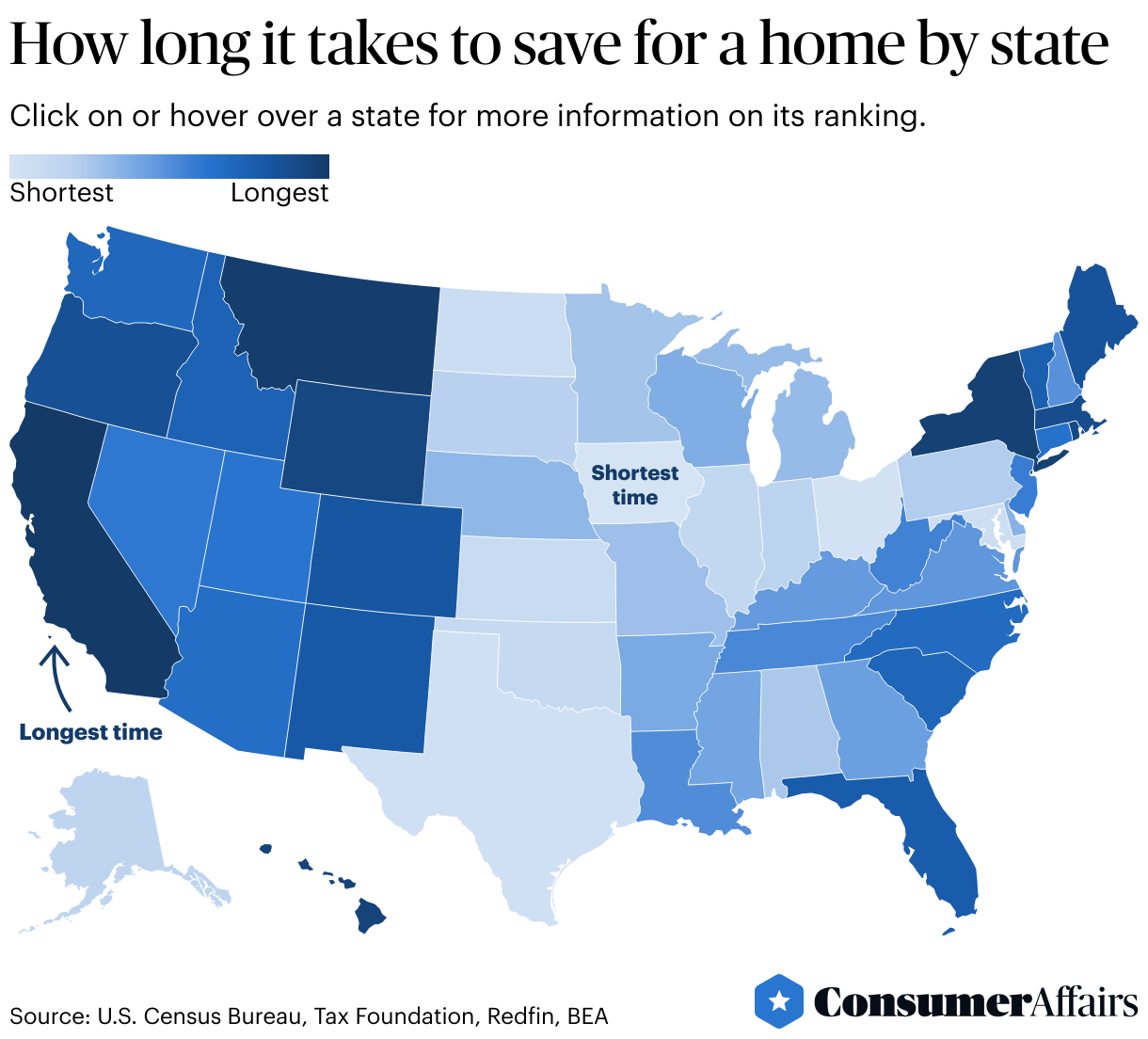

This report ranks all 50 states by how long it would take the typical household to save for a 10% down payment on a median-priced home — based on real data around income, taxes and cost of living. By calculating “fractional savings” (setting aside 10% of remaining income after taxes and essentials), ConsumerAffairs reveals where homeownership is most — and least — attainable.

Saving for a home is quickest in the Midwest, which has six states in the top 10 and no states below the top 20.

Jump to insightIowa offers prospective buyers the quickest path to saving for a down payment — just eight years and nine months.

Jump to insightCalifornians face the slowest path to homeownership. It would take more than 25 years of fractional saving to have enough for a 10% down payment.

Jump to insightIt takes nearly three times longer to save for a down payment in bottom-ranked California than in top-ranked Iowa.

Jump to insightTop 10 states where it’s fastest to save for a home

Nine of the top states are in the Midwest or the South, where home prices and living expenses tend to be more manageable. But those regions represent a wide and diverse swath of the country. What else do these top-ranked places have in common?

For most states in the top 10, it’s a balance of moderate incomes, low cost of living and relatively affordable home prices. There are a few intriguing exceptions, however, and they appear at the geographical extremes. Maryland, the only East Coast state, and Alaska, the sole Western state, face much higher expenses and home prices, but high household incomes expedite the journey to a down payment.

Below the map, we take a closer look at the states with the shortest paths to homeownership. Read on to dig deeper.

In the analysis that follows, we use the term discretionary income to describe the money remaining after typical tax burdens and essential expenses. We also refer to fractional saving, which represents saving 10% of that discretionary income to put toward a down payment. For more, check out the full explanation of our methodology.

1. Iowa

Is this heaven? No, it’s Iowa — the fastest place to save for a home. A typical household in the Hawkeye State can save enough to afford a typical down payment with less than nine years of fractional saving.

The reason for this short timeline to homeownership isn’t high household incomes or low tax burdens; Iowa ranks near the middle of the pack for both. It’s the combination of a relatively low cost of living and low home prices. (The median home sale price in Iowa is just $247,400 — the second lowest of all states.)

After taxes and essential expenses, a typical Iowan household is left with more than $28,000 of annual discretionary income. If a family saves just a tenth of that each year ($2,830), they’ll have enough for a 10% down payment ($24,740) on that median-price home in about eight years and nine months.

What makes Iowa the fastest place to save for a home:

- Median household income: $75,501

- Typical tax burden: $18,072

- Essential expenditures: $29,129 (seventh lowest)

- Discretionary income: $28,300

- Median home sale price: $247,400 (second lowest)

- Time to save for 10% down payment: 8 years, 9 months

2. Ohio

Flyover country? Not if you want to fast-track the road to homeownership. In Ohio, a typical household can save enough for a 10% down payment in just under 10 years. That makes the Buckeye State the second-fastest place to save for a home. (However, it’s worth noting that this is more than a year slower than top-ranked Iowa — the largest gap among the top 10 ranks.)

Ohio ranks in the bottom quarter of states for median household income, but the typical tax burden and the cost of living are on the lower side, too. And so are home prices: The median sale price is just $261,700 — the fifth-lowest price tag in the country.

After taxes and essential expenses, a typical Ohio household has more than $26,000 remaining each year. But it's not reasonable to save every penny and put it toward a future home. If a typical Ohio family set aside just 10% of that each year ($2,639), they’d have enough for a 10% down payment on a median home ($26,170) in about nine years and 11 months.

What makes Ohio the No. 2 place to save for a home:

- Median household income: $72,212

- Typical tax burden: $15,318

- Essential expenditures: $30,504

- Discretionary income: $26,390

- Median home sale price: $261,700 (fifth lowest)

- Time to save for 10% down payment: 9 years, 11 months

3. Texas

Roadrunners aren’t the only speedy thing about the Lone Star State. When it comes to saving for a home, Texas is the third-fastest state — and the fastest state outside the Midwest. A typical Texan household needs just over a decade to stack enough cash for a 10% down payment.

At nearly $340,000, median-priced homes in Texas are significantly more expensive than in top-ranked Iowa or Ohio, but they’re still cheaper than in most of the country. (That’s due in no small part to the recent influx of new home construction across the state: Greater housing supply is proven to help keep costs low.)

Fortunately for prospective homebuyers, discretionary income is a bit higher in Texas, too. After taxes and essential expenses, the typical Texas household has almost $33,000 to play with each year. Saving just a tenth of those remaining funds will add up to enough for a 10% down payment ($33,940) in about 10 years and three months.

What makes Texas the No. 3 place to save for a home:

- Median household income: $79,721

- Typical tax burden: $15,898

- Essential expenditures: $30,848

- Discretionary income: $32,975

- Median home sale price: $339,400

- Time to save for 10% down payment: 10 years, 3 months

4. Maryland

Maryland ranks the fourth-fastest place to save for a home, and it’s the only state on the East Coast to be represented in the top 10. The typical Maryland households need 10 years and change to save enough for a 10% down payment.

Marylanders face significant tax burdens (fifth highest in the country) and a moderate cost of living. But many families in the Old Line State bring home more than enough bacon — er, crab? — to make progress on their home savings goals.

The typical Maryland household earns almost $103,000 a year. Essential expenses take up just 32% of that, the second-lowest share in the nation. After paying for those essentials, a typical household in Maryland has around $43,000 leftover — more than any other state.

Under these conditions, it takes about 10 years and four months of fractional saving ($4,258 each year) to have the $43,930 needed for a 10% down payment on a typical home.

What makes Maryland the No. 4 place to save for a home:

- Median household income: $102,905 (third highest)

- Typical tax burden: $27,311 (fifth highest)

- Essential expenditures: $33,018

- Discretionary income: $42,576 (highest)

- Median home sale price: $439,300

- Time to save for 10% down payment: 10 years, 4 months

5. North Dakota

For the next fastest state to save for a home, we return to America’s heartland. North Dakota ranks fifth, with typical households needing about 10.5 years to sock away enough cash for a down payment.

Interestingly, essential expenses in North Dakota are on the higher side. Households spend almost $34,000 each year on necessities, ranking in the top 20 states. In particular, high health care costs ($11,667, seventh highest) outweigh lower typical costs on groceries and gas.

The quick path to homeownership in the Peace Garden State comes down to a supply of relatively affordable homes. The median home sale price in North Dakota is under $300,000. With the fractional saving method (setting aside $2,823 each year), you’d have enough for a 10% down payment ($29,820) on that median-price home in about 10 years and seven months.

What makes North Dakota the No. 5 place to save for a home:

- Median household income: $77,871

- Typical tax burden: $15,848

- Essential expenditures: $33,795

- Discretionary income: $28,228

- Median home sale price: $298,200

- Time to save for 10% down payment: 10 years, 7 months

6. Kansas

Homebuying hopefuls in Kansas have to wait just a smidge longer than those in fifth-ranked North Dakota to save enough for a down payment. With fractional saving, households are looking at a timeline of less than 11 years.

Like some other states in the top 10, Kansas lands near the middle of the pack for household income and tax burden. But families in the Sunflower State get a leg up, thanks to the state’s overall affordability. The typical household spends under $30,000 a year on essentials, the ninth lowest of all states. One significant boon is the low cost of housing and utilities: Families spend just $7,974 a year on these expenses, the sixth-lowest amount in the country.

After essential expenses and taxes, a typical Ohio household has about $27,600 left over each year. By saving a tenth of that ($2,762), a Kansas household would have enough for a 10% down payment on a median-priced home ($29,260) in about 10 years and seven months.

What makes Kansas the No. 6 place to save for a home:

- Median household income: $75,514

- Typical tax burden: $18,101

- Essential expenditures: $29,796 (ninth lowest)

- Discretionary income: $27,617

- Median home sale price: $292,600

- Time to save for 10% down payment: 10 years, 7 months

7. Oklahoma

Lower household incomes don’t need to deter Oklahomans from pursuing homeownership. While the median household income is among the lowest in the nation, at just over $66,000, typical taxes and essential expenses are also among the cheapest in the U.S.

Because household incomes provide a low starting point, Oklahomans are left with less than $24,000 each year. (That puts Oklahoma in the bottom quarter of states for discretionary income.)

But don’t despair, Sooners: Homes are selling for a median of just over $250,000, the third-lowest in the country. If a family can set aside a tenth of its discretionary income each year ($2,371), it will be on track for a 10% down payment in 10 years and eight months.

What makes Oklahoma the No. 7 place to save for a home:

- Median household income: $66,148 (sixth lowest)

- Typical tax burden: $14,567 (seventh lowest)

- Essential expenditures: $27,867 (fourth lowest)

- Discretionary income: $23,714

- Median home sale price: $252,900 (third lowest)

- Time to save for 10% down payment: 10 years, 8 months

8. Illinois

We’re back in the Midwest for the eighth fastest state for saving for a down payment. In Illinois, the typical timeline is less than 11 years.

Prospective homeowners in the Prairie State face higher expenses and tax burdens than in more than half the states, including most states that rank in the top 10 for fastest timelines to save. However, this is balanced by the fact that Illinoisans tend to have more cash flow to begin with: The Land of Lincoln ranks in the top 20 states for median household income, at over $83,000.

The bottom line? With fractional saving ($2,831 each year), Illinois households can put away enough for a 10% down payment ($30,330) in about 10 years and nine months.

What makes Illinois the No. 8 place to save for a home:

- Median household income: $83,211

- Typical tax burden: $20,934

- Essential expenditures: $33,971

- Discretionary income: $28,306

- Median home sale price: $303,300

- Time to save for 10% down payment: 10 years, 9 months

9. Alaska

It may be known as the Last Frontier, but it’s not the last place in America where you can afford to buy a home. Saving for a down payment is ninth fastest in Alaska, with a typical timeline of just under 11 years.

With typical homes selling for about $403,000, it’s not cheap real estate that earned Alaska a position in the top 10. It’s the right kind of balance between income, expenses and home prices — though each of those metrics is higher than in many other states on the top 10 list.

At the state level, Alaskans have some of the lowest expenditures on a few essentials, like gasoline, which costs the typical resident just $972 a year (the fifth lowest in the country). But these relative savings are canceled out by high costs for groceries ($4,811 a year, 10th highest) and health care costs ($14,044, the highest in America).

But thanks to a median household income of almost $96,000 a year, many Alaskans can make steady progress toward homeownership. By saving a tenth of their discretionary income each year ($3,699), residents can stash away enough for a typical 10% down payment ($40,280) in 10 years and 11 months.

What makes Alaska the No. 9 place to save for a home:

- Median household income: $95,665

- Typical tax burden: $20,625

- Essential expenditures: $38,054 (seventh highest)

- Discretionary income: $36,986 (sixth highest)

- Median home sale price: $402,800

- Time to save for 10% down payment: 10 years, 11 months

10. Indiana

A final Midwestern state rounds out our top 10 fastest places for saving for a home. Indiana joins its neighbors Ohio and Illinois on the leaderboard. With the fractional savings approach, the journey to a down payment takes just over 11 years.

After paying taxes and covering essential expenses, a typical Indiana household has about $25,000 left over. Compared with the country as a whole, that’s not a lot: The figure puts Indiana in the bottom third of all states for that metric. But thanks to the state’s relatively affordable real estate market, it’s enough for a Hoosier household to chart a path to homeownership.

If an Indiana household uses the fractional savings approach, putting aside $2,504 a year, it can save enough for a 10% down payment ($27,600) in 11 years.

What makes Indiana the No. 10 place to save for a home:

- Median household income: $71,959 (10th lowest)

- Typical tax burden: $15,888

- Essential expenditures: $31,032

- Discretionary income: $25,039

- Median home sale price: $276,000 (ninth lowest)

- Time to save for 10% down payment: 11 years

The 10 states where it takes the longest to save for a home

In many states, high home prices, taxes and overall living costs drive longer savings timelines — even for households with above-average income.

In the following states, saving for a down payment is the slowest:

- California

- Montana

- New York

- Hawaii

- Wyoming

- Rhode Island

- Massachusetts

- Oregon

- Maine

- Colorado

These states are all located in the West or the Northeast — the same regions that Americans are most interested in leaving, according to our analysis of the latest domestic migration trends. In contrast with the heartland-heavy top 10 ranks, most of the states above are coastal, where higher costs of living and a housing supply crunch tend to push home prices higher.

It’s worth noting that median household income varies widely among the bottom-ranked states, reinforcing our finding that wages and cost of living aren’t the primary predictors of savings timelines; home prices are.

Compare Iowa, our top-ranked state, with Wyoming, which is in the bottom 10. Only $31 separates the median income in each state. But the median home sale price in Wyoming is 81% more expensive than in Iowa.

In three of the bottom 10 states, the median household income exceeds six figures: Massachusetts ($104,828) has the highest income in the nation, and Hawaii ($100,745) and California ($100,149) aren’t far behind. But those high wages aren’t enough to fast-track saving because typical home prices are astronomically high. Of these 10 states with the slowest paths to homeownership, seven states have median home prices in the top 10, and the other three rank in the top half.

California, the state with the highest median home price ($832,400), is also the state with the longest savings timeline. In the Golden State, it would take more than 25 years of fractional saving to afford a 10% down payment on today’s median-priced home.

How saving for a home compares across the U.S.

The median length of time it takes to save for a down payment across all 50 states is 13 years and seven months. But in some states — including the entire Midwest — savers can achieve this milestone much faster.

In fact, the Midwest is the fastest region for saving for a home. The Midwest doesn’t just dominate the very top of the list, occupying six of the top 10 places — it dominates the whole top half of the list. (All 12 Midwestern states rank in the top 20, with no state exceeding 13 years of saving.)

There’s a sizable gap between the fastest and slowest states. It takes households in California 16 years and four months longer than those in Iowa to save enough for 10% down; Iowans can save for a home almost three times faster than Californians.

On the road toward affording a down payment, does your state feel like the fast lane, or more like a standstill? Check out the full data table to see how your state compares.

Why we used a 10% down payment instead of 20%

If you’ve dipped your toes into the housing market, chances are you’ve heard advice about putting 20% down. “A 20% down payment has been the social norm and the financial wisdom passed down in the real estate world for almost a century,” said Nick Booth, a real estate agent in Salt Lake City, Utah.

But as home prices have risen, so has the barrier to entry — and renters are often just treading water as they watch their homeowning dreams drift out of reach. “With inflation, rising living costs and growing consumer debt, many first-time buyers are struggling to save even a fraction of what’s needed for a large down payment,” Booth said.

Jeff Lichtenstein, the founder of Echo Fine Properties, a real estate brokerage in South Florida, said, “20% should be (realistic), but I think it’s why people are more house poor with less savings.”

In our analysis, we chose to use a benchmark of 10% down because it reflects what many buyers are already doing in today’s market. It also offers a more realistic target to help measure the affordability and accessibility of homeownership.

“I see every week how unrealistic the 20% rule has become,” said Shawn Zar, a real estate investor and co-founder of Sell-My-House-Fast.com. “With rent up 30% since 2019, and wages lagging, most buyers now do 6% to 10% down — not by choice, (but) by survival.”

However, a smaller down payment offers buyers some genuine benefits, too. “Smaller down payments keep cash flow flexible for repairs or rate hikes. It’s not a bad strategy anymore — it’s modern risk management,” Zar said.

So if a lower down payment is more relevant to today’s homebuyers, why does that 20% number still feel so prevalent?

“The biggest drawbacks to putting less than 20% down are higher monthly payments and private mortgage insurance (PMI) added to the loan,” Booth said. “Once you put down at least 20%, PMI goes away.”

How to save for a down payment

While saving timelines vary by state, there are still practical ways to make homeownership more attainable. Check out these tips to shorten your journey:

- Set specific goals. Use a tool like our “How much house can I afford?” mortgage calculator to start determining how much you might need for a down payment, closing costs and an emergency cushion.

- Try fractional saving. Ready to start saving for a home but not sure where you can flex your budget? Start by putting aside just 10% of your discretionary income. It gets the ball rolling without requiring a total upheaval of your financial routines.

- Use your banking tools to your advantage. Set a portion of your paycheck to be automatically deposited into a high-yield savings account to accrue risk-free interest on your money. Every little bit can help make homeownership closer to a reality.

- Explore down payment assistance programs. Many states and cities offer grants or forgivable loans for first-time buyers. “Your agent and lender can walk you through the options and get you on the right path,” said Booth, the Utah-based real estate agent.

- Boost your savings rate gradually. Each time you get a raise or have some other increase in income, increase your savings percentage before you adjust your budget for “wants” and “nice-to-haves.” This can help fend off “lifestyle creep.”

- Shop around for mortgage options. Even a small difference in mortgage rates can save thousands and make your goal more achievable.

- Consider compromising for a more affordable home. Expanding your search to nearby suburbs or smaller cities can dramatically shorten the time it takes to buy. So can expanding your search to include homes that need a little TLC. “(Consider) getting a fixer-upper that you can do projects on slowly,” said Lichtenstein, the Florida-based broker. “It’s fun and fulfilling to do things each year. You don't need a turnkey, perfect house on day one.”

However you approach the journey to homeownership, many experts encourage prospective buyers to get started saving for a down payment sooner rather than later, even when the market is overwhelming.

“(It’s) smarter to buy earlier and build equity than wait for prices to ‘cool,’” said Zar, the real estate investor.

“Lower (down payments) are becoming more prevalent because speed trumps perfection,” said Matt Schwartz, co-founder of VA Loan Network, which matches veterans with lenders. “Liquidity reigns.”

Methodology

The ConsumerAffairs Research Team analyzed data from all 50 U.S. states to determine how long it would take the typical person to save for a 10% down payment on a median-priced home.

To calculate the rankings, we combined data on median household income; federal, state and payroll taxes; and average annual living expenses — including food and beverages, clothing, gasoline, housing and utilities, health care, transportation, and insurance. These were used to estimate remaining discretionary income in each state after taxes and essential costs.

Using the median home sale price in each state, we then calculated how many years it would take to save a 10% down payment by setting aside 10% of that remaining discretionary income each year — a method we refer to as fractional saving. States were ranked from shortest to longest time frame based on the number of years and months required to reach this goal.

All monetary values were rounded to the nearest dollar, and all calculations were based on the most recent publicly available data as of 2025.

Reference policy

We love it when people share our findings! If you do, please link back to our original article to credit our research.

Questions?

For questions about the data or if you'd like to set up an interview, please contact rsowell@consumeraffairs.com.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- Zillow, “Housing Data.” Accessed Oct. 27, 2025.

- Bureau of Economic Analysis, “Regional Data: GDP and Personal Income.” Accessed Oct. 27, 2025.

- U.S. Census Bureau, “American Community Survey Data.” Accessed Oct. 27, 2025.

- Redfin, “Data Center.” Accessed Oct. 27, 2025.

- Tax Foundation, “Facts & Figures 2025: How Does Your State Compare?” Accessed Oct. 27, 2025.

Figures