VA Loan Statistics (2026 Data)

+1 more

VA loans are mortgage loans guaranteed by the U.S. Department of Veterans Affairs (VA). These loans are intended to make it easier for veterans and service members to obtain mortgages. The loans themselves are provided by private lenders, such as banks and mortgage companies, but the backing of the VA means that borrowers can obtain more favorable terms. Among the primary benefits of VA loans are no down payments, competitive interest rates and lower closing costs.

In 2022, VA loans made up 10.2% of all purchase loans for owner-occupied properties.

Jump to insightVA loan volume was down 46% between 2022 and 2023, primarily due to a significant decrease in refinance loans.

Jump to insightTexas had more VA loan recipients than any other state in 2023. Loans to Texas citizens made up more than 10% of total VA loans for the year.

Jump to insightIn the fourth quarter of 2020, serious delinquency rates on VA loans reached nearly 6%. By the same time in 2023, delinquency rates were down to pre-pandemic levels, around 2%.

Jump to insightVA loan statistics

VA loans are only available to a subset of borrowers, including veterans, active service members and eligible surviving spouses. The VA loan program includes both purchase loans and refinance loans.

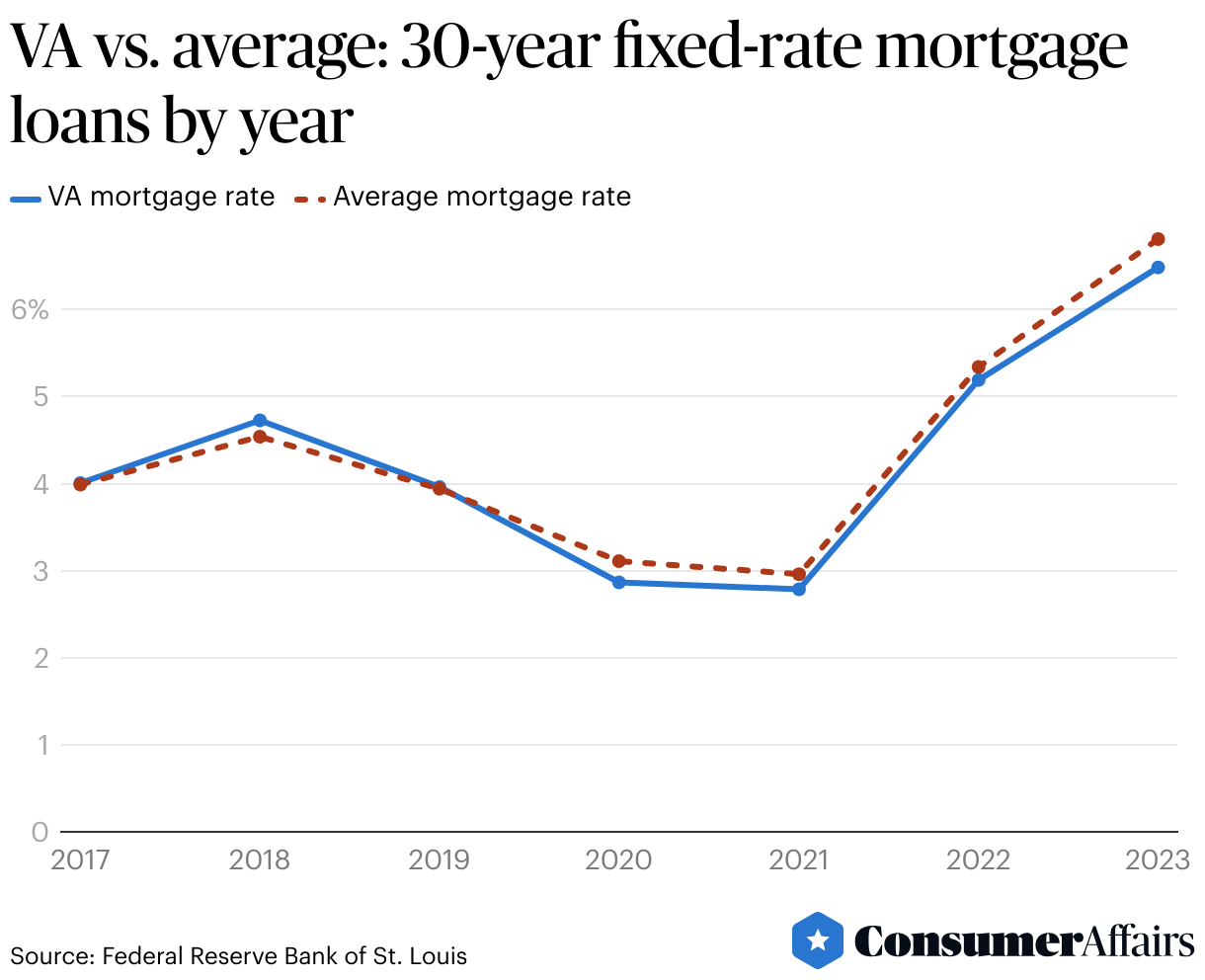

Mortgage rates on VA loans are generally (although not always) lower than the overall average mortgage rate. Of course, an individual borrower’s mortgage rates will vary depending on their particular circumstances.

Data from the Home Mortgage Disclosure Act shows that when compared to other types of mortgage loans (e.g., FHA, conventional loans), VA loans have the largest share of loans with mortgage rates below 3% and the smallest share of loans with interest rates above 7%.

According to the Consumer Financial Protection Bureau, in 2022, VA loans made up 10.2% of new purchase loans for one- to four-family owner-occupied homes. This represented a slight increase from 2021, when VA loans comprised 9.7% of such loans.

VA loan data by state

In 2023, residents of Texas obtained more VA mortgage loans than residents of any other state. With over 43,000 loans, individuals in Texas made up more than 10% of all VA loan recipients in the U.S. Notably, 98% of VA loans in Texas were purchase loans. In 2023, Florida was the state with the second most VA loans and the only other state with more than 40,000 loan recipients that year.

Not surprisingly, states with smaller populations made up the other end of the spectrum. There were three states with fewer than 1,000 loan recipients in 2023: North Dakota, Rhode Island and Vermont.

VA loan totals by year

The chart below details VA loan totals since 2015. The total number of loans is relatively steady from year to year, outside of 2020 to 2021 and 2023. Inflated numbers from 2020 to 2021 are primarily due to increases in refinance loans. Mortgage rates in the U.S. were at all-time lows during 2020 and 2021, making it an attractive time to refinance. The total number of refinance loans was down sharply in 2023 as interest rates on mortgage loans continued to rise.

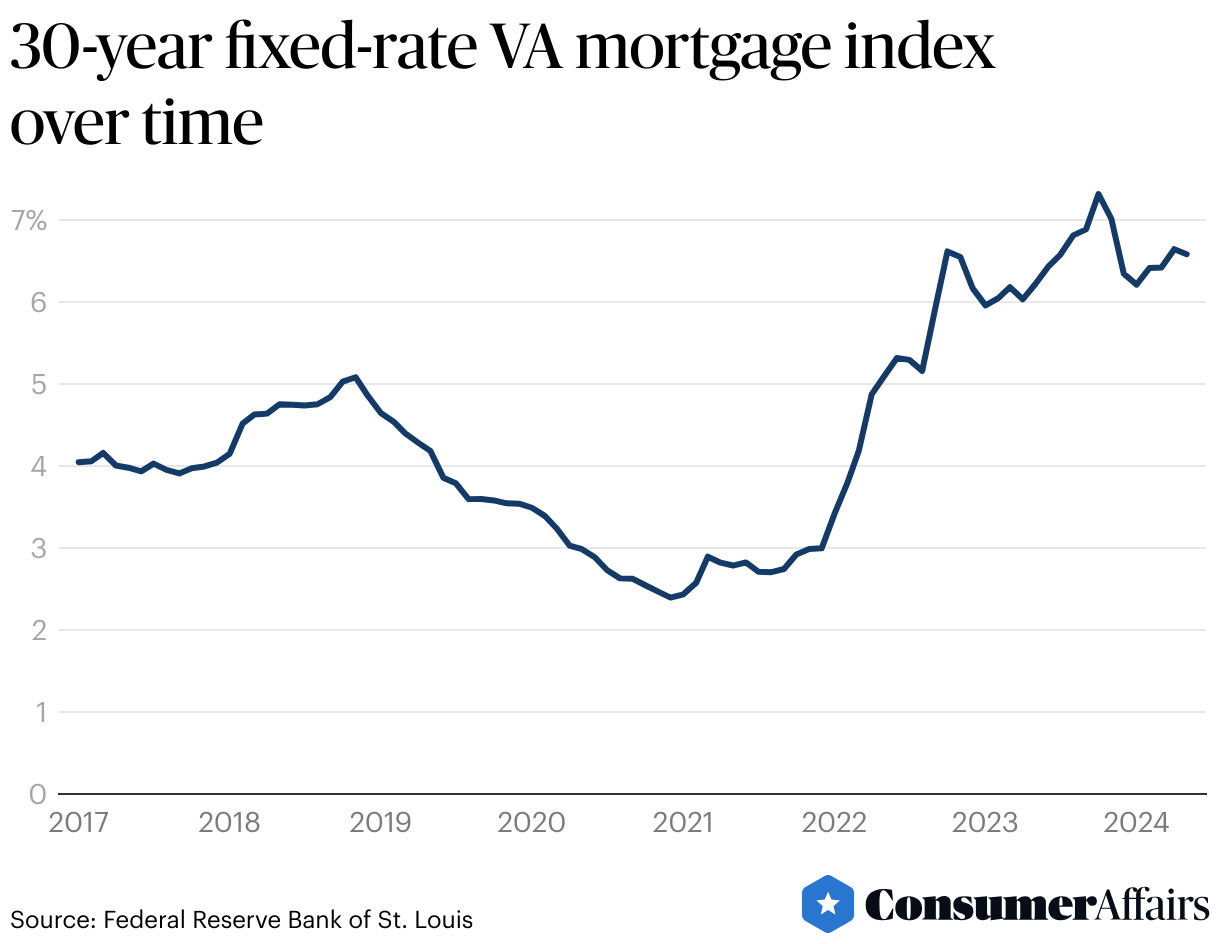

VA mortgage index by year

The VA mortgage index tracks the average interest rate on 30-year fixed mortgage loans from the U.S. Department of Veterans Affairs. As noted above, these interest rates generally tend to be competitive with rates on other mortgage loans, including FHA and conventional mortgage loans.

VA mortgage index rates reached a record low of 2.395% in December 2020 but have increased significantly since then.

Mortgage delinquency rates for VA loans

Despite rising interest rates, the percentage of VA mortgage loans in serious delinquency has been falling since a spike during the COVID-19 pandemic. As of the end of 2023, delinquency rates on VA loans had returned to pre-pandemic levels. A serious delinquency is defined as a mortgage that is 90 or more days past due or one that has entered the foreclosure process.

VA loan delinquency rates fall in between the delinquency rates of other mortgage loan types. The delinquency rate on FHA loans is generally higher than the corresponding VA rate. Serious delinquency rates for conventional mortgage loans are lower than the VA rate. For example, in December of 2023, the serious delinquency rate on FHA loans was 3.97%. In the same month, delinquency rates on conventional mortgages from Fannie Mae and Freddie Mac were 0.53% and 0.54%, respectively.

How do I apply for a VA loan?

In order to apply for a VA home loan, you must obtain a Certificate of Eligibility (COE) from the Department of Veterans Affairs.

Requirements for obtaining a COE are detailed in the table below. Note that some service members only need to meet one of the applicable requirements.

In some situations, spouses of veterans are also eligible, as are service members whose discharges meet specific criteria.

Once you have obtained a COE, you must present it to your mortgage lender. In order to receive financing, you’ll still need to meet that lender’s income and credit requirements.

FAQ

What percentage of mortgages are VA loans?

In 2022, VA loans comprised 10.2% of mortgages for one- to four-family owner-occupied properties.

Who is the largest VA lender?

Veterans United Home Loans was the largest VA lender in 2023, providing nearly double the number of VA loans (58K) as the next largest lender.

What is the average 30-year VA mortgage rate?

The average 30-year fixed VA mortgage rate was 6.58% in May of 2024. The majority of VA borrowers (56.8%) have interest rates of 5% or less.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Veterans United Home Loans, “VA Loan Statistics.” Accessed May 22, 2024.

- U.S. Department of Veterans Affairs, “VA Home Loans - Lender Statistics.” Accessed May 22, 2024.

- Federal Reserve Bank of St. Louis, “30-Year Fixed Rate Veterans Affairs Mortgage Index.” Accessed May 29, 2024.

- Urban Institute, “Housing Finance: At a Glance Monthly Chartbook, April 2024.” Accessed May 28, 2024.

- U.S. Department of Veterans Affairs, “Eligibility for VA Home Loan Programs.” Accessed May 28, 2024.

- U.S. Department of Veterans Affairs, “VA Home Loans.” Accessed May 28, 2024.

- Federal Reserve Bank of St. Louis, “30-Year Fixed Rate Mortgage Average in the United States.” Accessed May 29, 2024.

- Urban Institute, “VA Home Loans Have Several Advantages but Could Do More to Support Military Members Facing Financial Hardship.” Accessed May 29, 2024.

- Consumer Financial Protection Bureau, “Summary of 2022 Data on Mortgage Lending.” Accessed May 29, 2024.

- Consumer Financial Protection Bureau, “Summary of 2021 Data on Mortgage Lending.” Accessed May 29, 2024.

Figures