How many car insurance claims are filed each year? 2026

+1 more

Auto insurance helps protect drivers from unexpected costs, and providers help hedge their bet by charging cheaper premiums for “low-risk” drivers and higher premiums for “high-risk” drivers.

U.S. car insurance rates increased more than 20% over the course of 2023, which has also spurred a spike in rate comparison shopping. Between the increased cost of labor and inflationary increases in vehicle parts, extreme weather damaging vehicles and crash fatalities increasing, insurance providers are trying to recoup losses from the past few years by increasing insurance premiums.

The average annual cost of full coverage auto insurance in the U.S. was $2,019 in 2023, with costs estimated to rise to $2,160 in 2024.

Jump to insightFlorida is the most expensive state to have auto insurance, costing drivers $233 per month on average. Ohio is the cheapest state, with an average monthly insurance cost of $84.

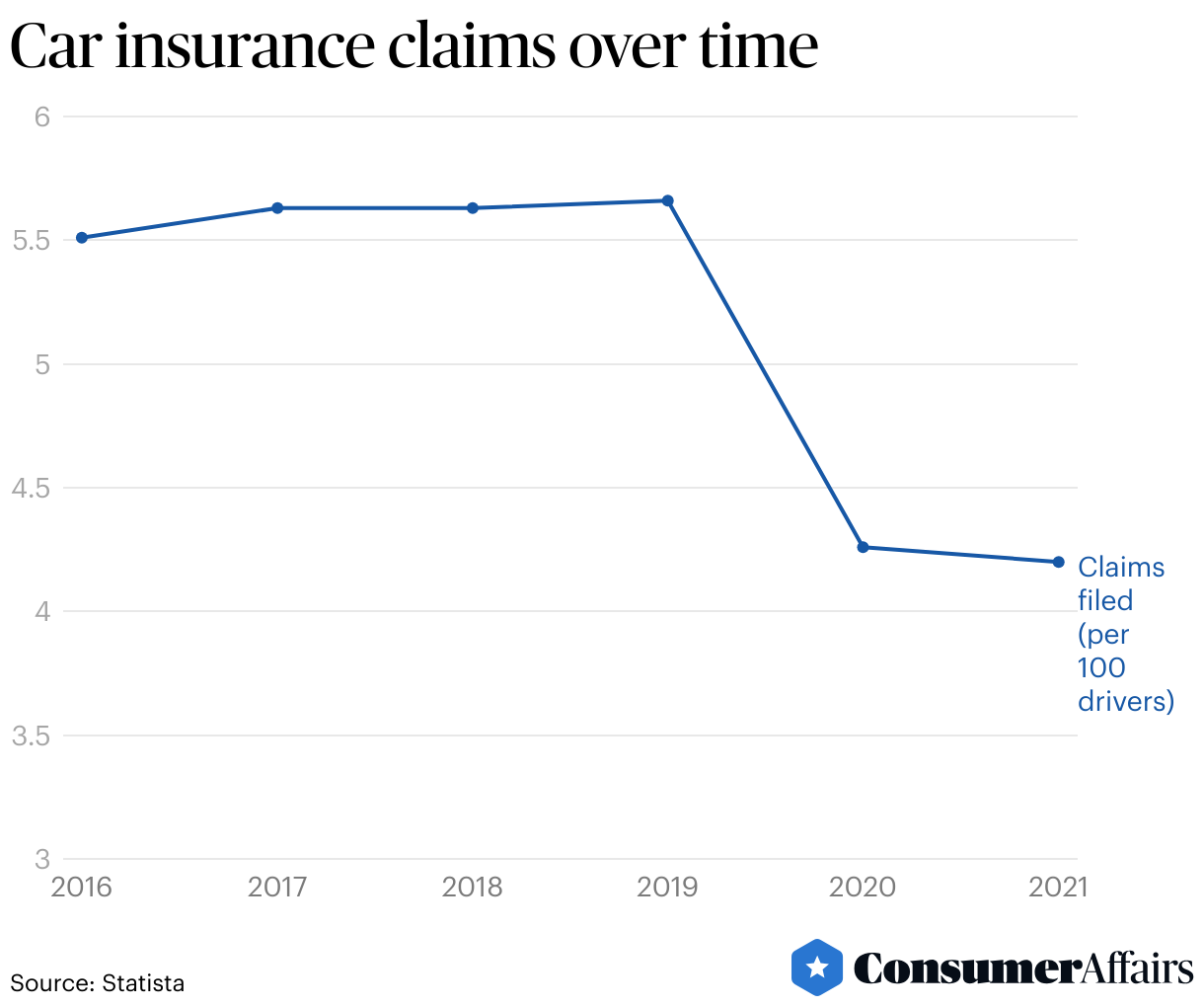

Jump to insightThere were 4.2 private passenger auto collision insurance claims filed for every 100 drivers in 2021.

Jump to insightAbout 1 out of every 7 drivers in the U.S. are uninsured.

Jump to insightCar insurance statistics

Car insurance rates are determined by a number of factors, including age, gender, driving record, location, credit history and type of vehicle. The average cost to own and operate a new car in 2023 was $12,182, while the annual cost of full coverage auto insurance was $2,019 in 2023.

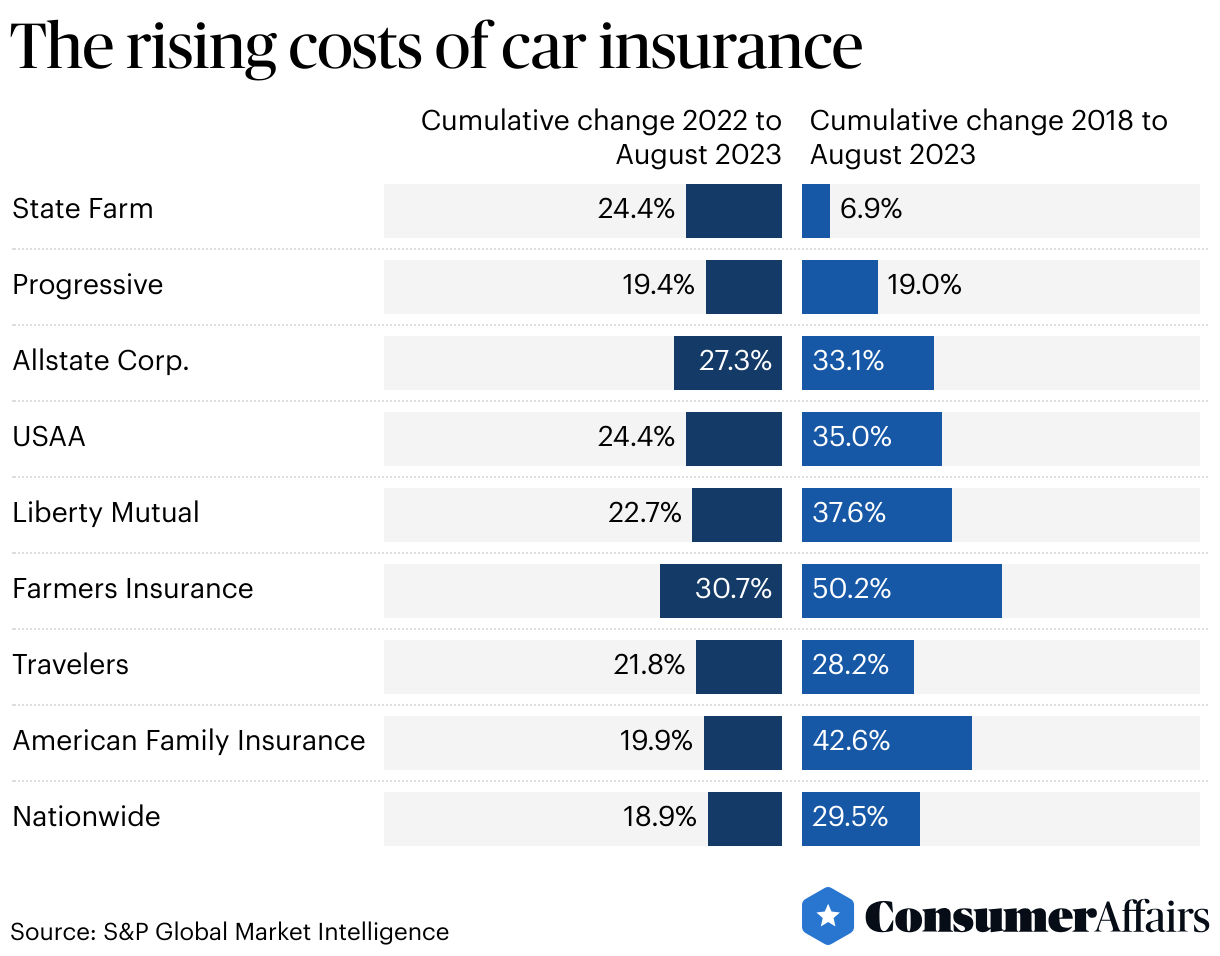

Private car insurance rates have steadily risen to offset the rising costs of insuring drivers and reduce losses incurred by insurers. Smaller insurers, like American Family Insurance and Farmers Insurance, have increased rates between more than 42% and 50%, respectively, from 2018 and 2023. Larger insurers such as State Farm and Progressive are likely more insulated from losses due to company size and therefore only raised rates about 7% to 19% over the same period.

Claims per year and cars registered

As of 2022, there were 282,174,766 motor vehicles in the U.S., and in 2021, there were 4.2 auto collision insurance claims filed per 100 drivers. Claims filed increased from 2016 to 2019, before dropping dramatically in 2020 and 2021, likely due to decreased auto travel from COVID-19 restrictions.

Types of car insurance and requirements

There are ten types of auto insurance, the most common being liability, collision, personal injury and comprehensive. Each policy has its own term limits and requirements.

- Liability insurance: covers you in an accident if you’ve been determined to be at fault. It covers car repairs to damaged property and medical bills due for the other vehicle’s driver and its passengers. Liability insurance is generally considered the bare minimum for auto coverage and is what most states mandate.

- Collision coverage: provides coverage for auto repairs, regardless of whether you are at fault. If you’re in an accident and your car is deemed a total loss, collision coverage usually pays the value of your car.

- Comprehensive coverage: covers damage to your vehicle outside of accidents, such as that due to theft and weather damage.

- Personal injury protection: covers the missed work expenses and all medical bills for the driver and all passengers. It is incredibly useful for all drivers but can also be fairly expensive due to the broad coverage.

- Uninsured motorist coverage: provides payment if you are in an accident with a driver who is at fault and doesn’t have insurance or if you’re in a hit-and-run accident.

- Rental car insurance: usually offered as an add-on to your insurance policy, rental car insurance provides payment if your vehicle is undergoing long-term repairs due to damage from an accident, and you’re in need of a rental car.

- Gap insurance: covers the difference between what you owe on a new car and what the car is worth. Typically used when a vehicle is stolen or totaled.

- Stacked coverage: enables a driver with multiple policies to cash out on overlapping coverage to maximize their payout.

- Pet injury coverage: covers vet bills for your pet if they are injured in an accident.

- New car replacement: covers the cost of a new car of the same make and model in the event that it is stolen or totaled. It typically isn’t included in standard policy coverage and must be purchased as an add-on.

How many drivers do not have auto insurance?

Roughly 1 out of 7 drivers in the U.S. were uninsured12 in 2022, despite auto insurance being required in most states. Auto liability insurance is mandatory in 49 states and Washington, D.C., but the degree of coverage needed varies from state to state. New Hampshire is the only state in the U.S. that does not require compulsory auto insurance coverage, but it does enforce financial responsibility laws that require drivers who have been financially irresponsible in previous accidents to have auto insurance coverage.

Uninsured motorist coverage

Twenty U.S. states and Washington, D.C., require uninsured motorist coverage, which can include car repairs outside of standard coverage, rental car coverage, medical bills for the driver and passengers, lost wages, extended medical care, damages resulting from pain and suffering and vehicle loss of value. Uninsured motorist coverage is most likely to come in handy in states with a high share of uninsured drivers. For example, 29.4% of drivers in Mississippi are uninsured — the highest in the nation — versus the 3.1% of uninsured New Jersey drivers.

States generally fall into two buckets regarding insurance claim payouts: At-fault states and no-fault states. At-fault states require the insurer of the driver who caused the accident to pay the damages to both cars and any bodily injury to both parties. No-fault states require that the at-fault driver’s insurance provider pay for their damages, and the insurance provider for the driver not at fault will pay for their own damages.

How do I file a car insurance claim?

Filing an auto insurance claim is a multistep process involving contacting your insurance provider and supplying all pertinent documents in a timely, expedited manner.

- Call your insurance provider as soon as possible, regardless of which party is “at fault.” This will jump-start the claims process and will let you know if your policy covers your accident.

- Formally file your insurance claim. Most providers now offer a digital claims process through their mobile app. This will provide updates on the status of the claim and allow you to upload photos, schedule an appraisal and check your deductible.

- Identify which documents are needed to complete the claim. A “proof of claim” form and a copy of the police report (if filed) will be required by all providers to resolve the claim.

- Understand the important filing deadlines. A delay in supplying accurate information will delay the claims payout process. If your provider has a time limit for filing claims and submitting bills, it could disqualify your case. There may also be time limits for resolving claim disputes, so it is pivotal to keep all deadlines in mind.

- Keep all pertinent information regarding the accident and claim on hand, including names and phone numbers of people you speak with regarding your insurance and all auto bills related to the accident.

Car insurance costs

The Motor Vehicle Consumer Price Index — which tracks auto insurance premiums — has steadily increased since early 2021, but it began to truly skyrocket at the beginning of 2022. The price index increased from $574.04 in January 2022 to $780.28 by December 2023 — nearly eight times the amount of 1982 to 1984 prices.

By age

Car insurance costs are significantly higher for younger, less experienced drivers than their older counterparts, due in part to the fact that 15- to 34-year-olds are historically responsible for nearly 40% of all crashes in the U.S.

| Age | Average monthly insurance cost | Average annual insurance cost |

|---|---|---|

| 16 | $565 | $6,779 |

| 17 | $489 | $5,862 |

| 18 | $411 | $4,931 |

| 19 | $319 | $3,822 |

| 21 | $226 | $2,708 |

| 25 | $161 | $1,929 |

| 30 | $142 | $1,705 |

| 35 | $138 | $1,654 |

| 45 | $132 | $1,582 |

| 55 | $122 | $1,462 |

| 60 | $121 | $1,449 |

| 65 | $125 | $1,494 |

| 70 | $132 | $1,585 |

By state

Florida is the most expensive state for drivers to have auto insurance coverage, with rates roughly 71% higher than the national average of about $136 per month. Ohio is the cheapest state for drivers to have auto insurance; however, states with lower insurance costs often have less stringent coverage requirements.

| State | Average monthly insurance cost | Average annual insurance cost |

|---|---|---|

| Florida | $233 | $2,796 |

| Louisiana | $211 | $2,532 |

| Michigan | $202 | $2,424 |

| New Jersey | $185 | $2,220 |

| Nevada | $183 | $2,196 |

| Ohio | $84 | $1,008 |

| Vermont | $87 | $1,044 |

| North Carolina | $90 | $1,080 |

| Idaho | $91 | $1,092 |

| Maine | $91 | $1,092 |

FAQ

How much does car insurance cost?

Car insurance costs an average of $2,019 in the U.S. However, age, gender, location and insurance provider will all impact the final cost.

Does every driver need car insurance?

While it is a good idea for all drivers to have auto insurance coverage, it is not mandatory in every state. As of 2024, New Hampshire is the only state in the U.S. that does not require auto insurance for all drivers.

What does car insurance cover?

Car insurance can cover medical bills, missed work expenses, vehicle repairs and more depending on if you opt for full coverage or minimum coverage.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- U.S. Bureau of Labor Statistics, “Economic News Release, Consumer Price Index Summary.” Accessed Feb. 14, 2024.

- S&P Global Market Intelligence, “US private auto insurance rates see double-digit jump in 2023.” Accessed Feb. 3, 2024.

- U.S. Department of Transportation, “Highway Statistics Usage 2022.” Accessed Feb. 3, 2024.

- Statista, “Frequency of private passenger auto collision insurance claims for physical damage in the United States from 2007-2021.” Accessed Feb. 3, 2024.

- NAIC, “Uninsured Motorists.” Accessed Feb. 4, 2024.

- Insurance Information Institute, “How to file an auto insurance claim.” Accessed Feb. 2, 2024.

- Bureau of Labor Statistics, “Consumer Price Index for All Urban Consumers.” Accessed Feb. 7, 2024.

- Policygenius, “Average car insurance rates by age and gender.” Accessed Feb. 8, 2024.

- Policygenius, “Average Car Insurance Rates (2024).” Accessed Feb. 8, 2024.

- Insurance Research Council, “14 Percent of U.S. Drivers Were Uninsured in 2022, IRC Estimates.” Accessed Feb. 15, 2024.

Figures