Mortgage statistics 2026

+1 more

Rather than buying a home outright with cash, the average American gradually finances their home purchase by taking out a home loan, which is commonly called a mortgage. Nearly 62% of owner-occupied households in the U.S. are currently paying down mortgages, according to the U.S. Census Bureau.

While most Americans will take out a mortgage at some point in their life, mortgagors can have vastly different borrowing experiences depending on where they live, the generation they belong to and the type of mortgage they take out, among many other factors. Understanding the current mortgage market’s intricacies is pivotal to a homebuyer selecting the best mortgage option for their unique situation.

80% of homebuyers take out mortgages to finance their home.

Jump to insightThe vast majority (92%) of homebuyers choose fixed-rate or hybrid adjustable-rate loans, and about 90% of homebuyers choose a 30-year loan term.

Jump to insightCumulative U.S. mortgage debt rose to $12.9 trillion by the third quarter (Q3) of 2023, a 0.6% increase over the previous quarter.

Jump to insightMortgage debt makes up nearly 70% of total consumer debt. Millennials hold more mortgage debt, on average, than other age groups.

Jump to insightThe mortgage delinquency rate is about 3.6%, and the seriously delinquent home loan rate is about 1.5%.

Jump to insightGeneral mortgage statistics

There are a number of key factors to consider when selecting the best mortgage options, including the loan’s term, type, interest rate and rate type.

Types of mortgages

Among homebuyers who finance their homes, approximately 62% use conventional loans, while approximately 29% use loans backed by the Federal Housing Administration (FHA loans) or the Department of Veterans Affairs (VA loans).

Loan term

A loan term is the time frame a borrower has to repay a loan. Home loan terms typically range from 15 to 30 years. About 90% of mortgages are 30-year loans, and 6% are 15-year loans.

Interest rates

Mortgage rates can be fixed, adjustable or a hybrid of both. About 92% of homebuyers opt for fixed-rate loans. Another 3% choose hybrid adjustable-rate loans, which start with fixed rates and later switch to adjustable rates Only about 1% of homebuyers select purely adjustable-rate loans.

Size of the residential mortgage market

The total value of the single-family housing market in the U.S. was $45.5 trillion in Q3 2023, while housing equity was $32.6 trillion.

- Total U.S. mortgage balances amounted to $12.25 trillion at the end of 2023, spread out across 84.2 million mortgages.

- Mortgage origination volume, which includes both refinance and purchase originations, stood at nearly $394 billion at the end of 2023.

- Mortgages are used to finance 80% of homes in the U.S.

Average sale price of homes

The average sale price of a new home in the U.S. was $534,300 in January 2024; the median sale price was $420,700.

Average homeownership rates by region

The Midwest has the highest average percentage of homeownership, more than 4 percentage points higher than the average across the U.S.

| Region | Average |

|---|---|

| U.S. | 65.7% |

| Midwest: Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Wisconsin | 69.8% |

| Northeast: Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, Vermont | 61.5% |

| South: Alabama, Arkansas, Delaware, Florida, Georgia, Kentucky, Louisiana, Maryland, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, Virginia, Washington, D.C., West Virginia | 67.8% |

| West Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada, New Mexico, Oregon, Utah, Washington, Wyoming | 61.4% |

Homebuyer demographics

Of all homebuyers in 2023, 32% were buying a home for the first time, while 68% were repeat buyers.

- The vast majority (87%) of homes purchased were previously owned, while 13% were new properties.

- The typical age of a first-time homebuyer is 35, and 70% of homebuyers between the ages of 24 and 32 are first-time homebuyers.

- Most homebuyers (39%) are baby boomers.

- Veterans and active-duty military personnel made up about 18% of all homebuyers between July 2022 and June 2023.

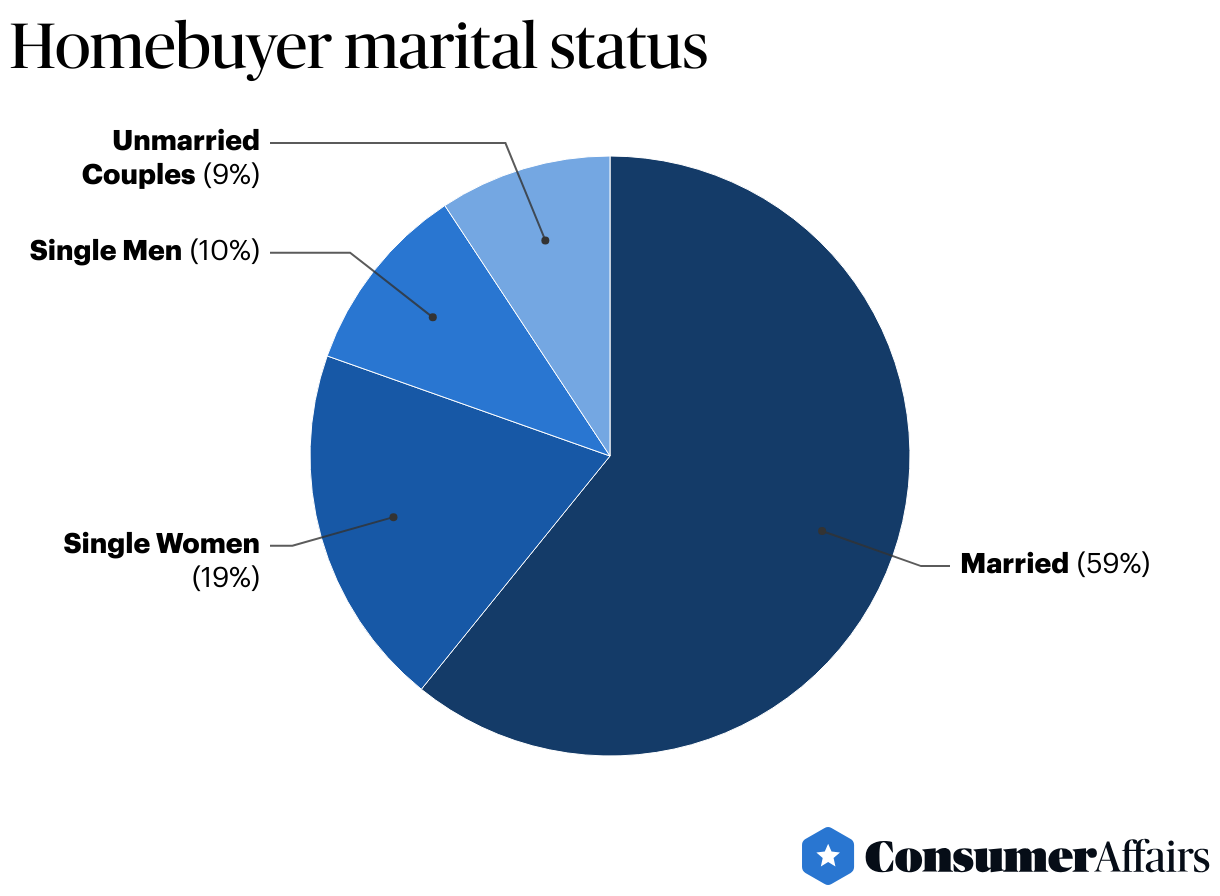

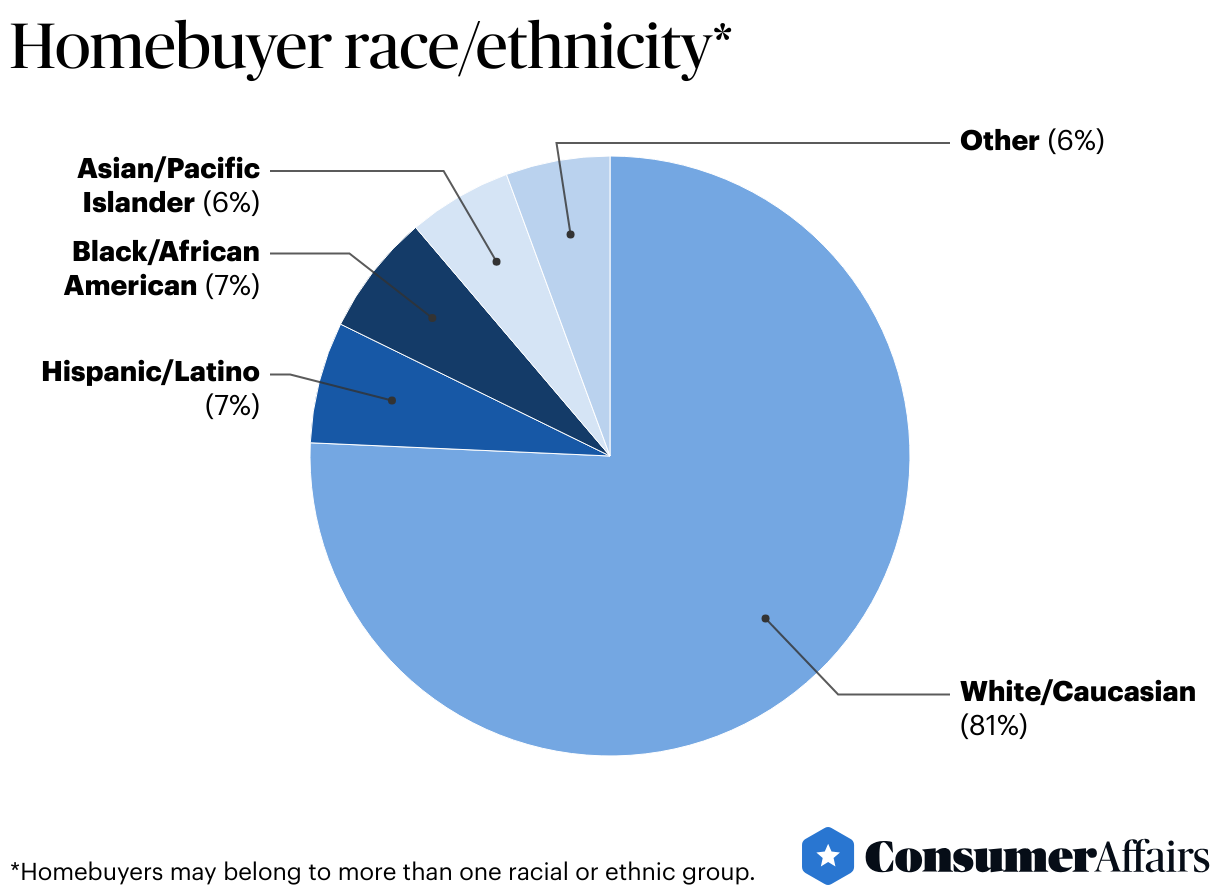

Marital status and race/ethnicity

Single women currently make up the second largest group of first-time homebuyers after married couples. The share of homebuyers who are married is the lowest it’s been since 2010.

Racial and ethnic minorities make up a growing share of homebuyers in the U.S. Individuals identifying as white/Caucasian made up only 81% of homebuyers from July 2022 to June 2023, down from 88% during the year prior.

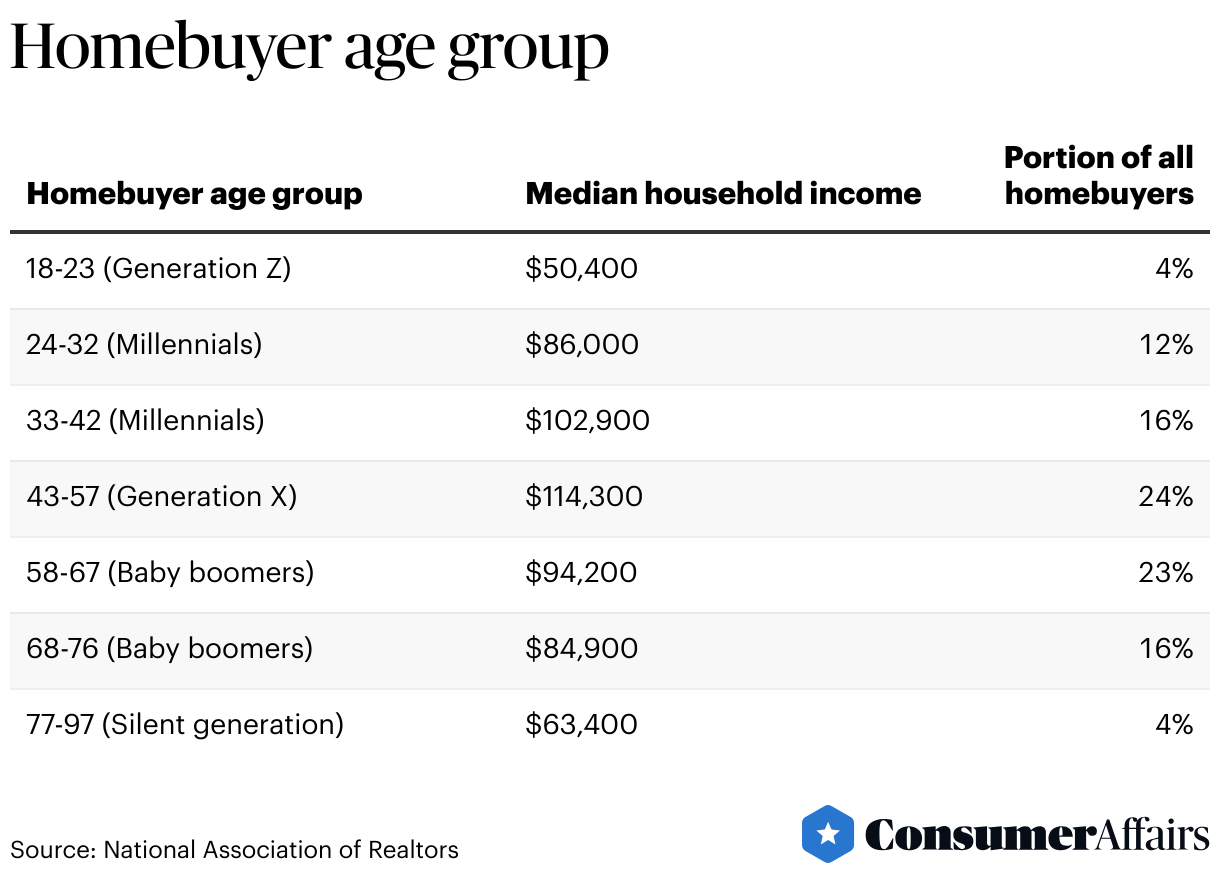

Age and income

Baby boomers, aged 58 to 76, make up the largest homebuying age group.

Home purchase vs. refinance loans by race/ethnicity

While borrowers who are white still account for a majority of both home purchase and refinance loans taken out in the U.S., their shares of both have decreased since 2018.

| Race/ethnicity | Purchase loan portion | Refinance loan portion |

|---|---|---|

| White | 54.4% | 57.3% |

| Black/African American | 8.1% | 8.1% |

| Hispanic/Latino | 9.1% | 7.1% |

| Asian/Pacific Islander | 7.6% | 3.6% |

Mortgage origination statistics

Mortgage originations in 2022 increased by 2.8% from 2021.

Applications vs. closings

- In 2022, approximately 14.3 million applications and 8.4 million mortgages were originated in the U.S.

- In January 2024, 661,000 new single-family homes were sold in the U.S.

Mortgage origination by loan type

Government-sponsored loans saw a near 5 percentage point decrease in their share of U.S. mortgage originations from Q3 2022 to Q3 2023, while the share of FHA/VA loan types increased by nearly 5 percentage points during the same period.

| Loan type | Percentage |

|---|---|

| Government-sponsored | 45.1% |

| Portfolio | 26.1% |

| FHA and VA | 26.4% |

| Private-label securities | 2.5% |

Credit scores and mortgages

The U.S. mortgage market is largely dominated by borrowers with very good to excellent credit scores. The average FICO score for mortgages in 2022 was 757.

| Borrower credit score | Mortgage origination volume |

|---|---|

| <620 | $14.87 billion |

| 620-659 | $14.05 billion |

| 660-719 | $53.19 billion |

| 720-759 | $63.76 billion |

| 760+ | $247.9 billion |

Percentage of loan delinquencies and foreclosures

According to the most recent National Delinquency Survey, the mortgage delinquency rate was about 3.6% at the end of Q3 2023, an increase over the 3.4% approximate delinquency rate from Q2 2023. However, the seriously delinquent loan rate was about 1.5% at the end of Q3 2023, a slight decrease from the approximate 1.6% seriously delinquent rate during the previous quarter.

Across the U.S., 1 in 752 homes (0.13%) had a foreclosure filing in the first half of 2023, amounting to about 74,500 individuals who experienced a new foreclosure during that time.

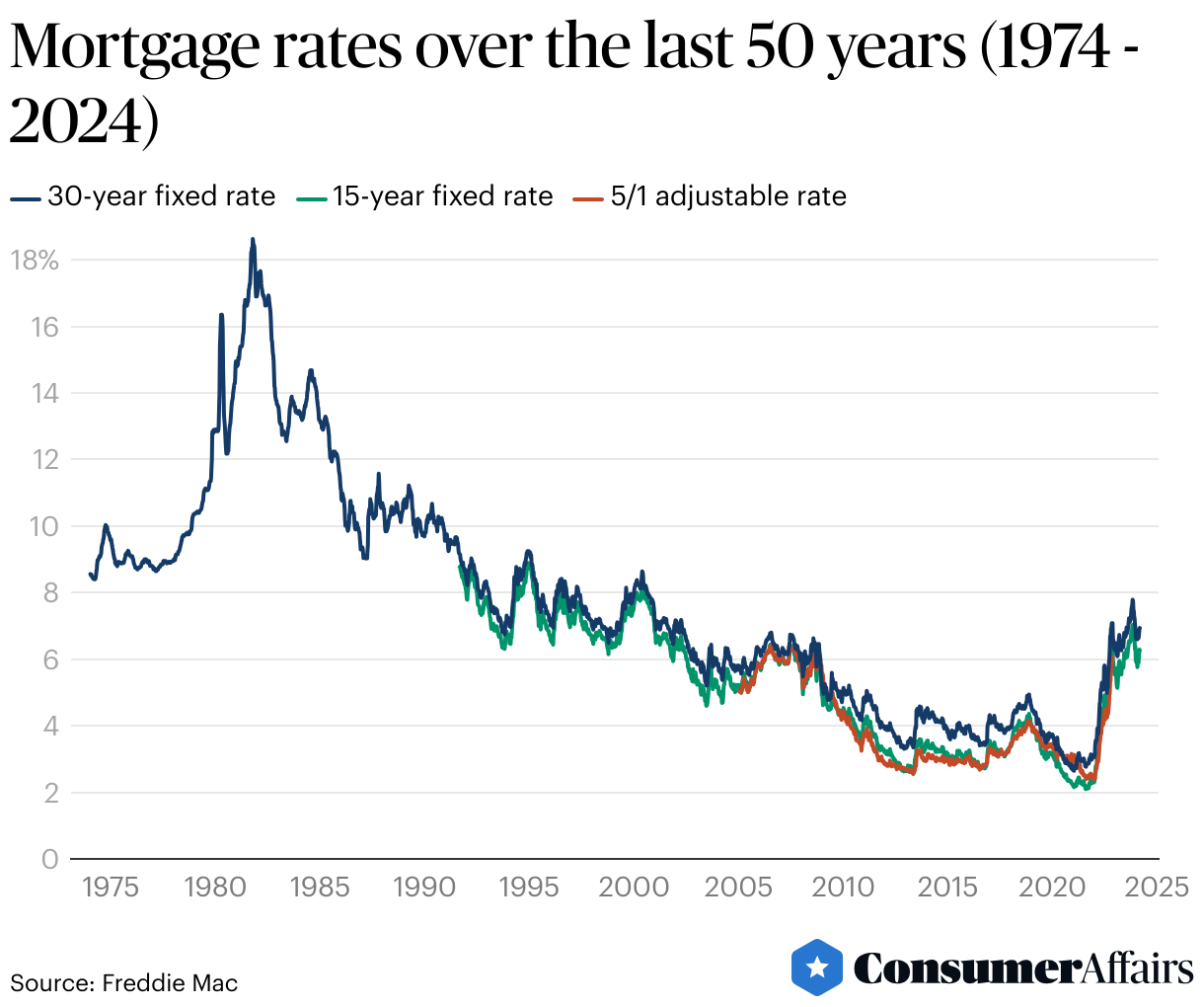

Mortgage rates over time

As of Feb. 22, 2024, the average rate for a 30-year fixed-rate mortgage stands at 6.9%, while the average rate for a 15-year fixed-rate mortgage is 6.29%.

Multiple factors, including inflation and a strong job market, are contributing to high mortgage rates.

Impact of COVID-19 on mortgages

During the COVID-19 pandemic, Congress moved to protect consumers' finances by expanding forbearance options for borrowers. During the same period, the Federal Reserve reduced the federal funds rate’s target range, leading mortgage interest rates to drop to their lowest averages in at least 50 years. More remote work options motivated many individuals living in cities with high costs of living to find lower-cost living options in other areas.

These developments allowed individuals to take advantage of lower mortgage rates, which spiked mortgage origination and drove housing costs up due to a lack of inventory to meet demand. Existing homeowners were also able to refinance their mortgages to lower the burden of monthly loan payments. As the economy rapidly recovered following the peak of the pandemic, inflation rose quickly. To combat that rise in inflation, the Federal Reserve began to raise interest rates again, and with this, mortgage rates also increased.

Purchasing costs

About 1 in 5 homebuyers (22%) finance between 80% and 89% of their home purchase with a mortgage. Only 14% of homebuyers finance less than 50% of their home purchase.

| Purchase price financed | Homebuyer portion |

|---|---|

| <50% | 14% |

| 50%-59% | 4% |

| 60%-69% | 6% |

| 70%-79% | 12% |

| 80%-89% | 22% |

| 90%-94% | 12% |

| 95%-99% | 16% |

| 100% | 14% |

Down payments

Though conventional wisdom suggests that homebuyers should make at least a 20% down payment on a home, the average median down payment is only 14%. Homebuyers who are 58 years of age or older are more likely to put at least 20% down.

| Age group | Median down payment |

|---|---|

| All buyers | 14% |

| 24-32 | 8% |

| 33-42 | 11% |

| 43-57 | 10% |

| 58-67 | 20% |

| 68-76 | 21% |

| 77-97 | 27% |

Closing costs

According to data from Assurance, the national average for mortgage closing costs as of January 2024 is about $4,243. The states with the highest average closing costs are as follows:

- New York: $8,039

- California: $8,028

- New Jersey: $7,702

- Washington: $6,966

- Massachusetts: $6,223

The states with the lowest average closing costs include the following:

- West Virginia: $2,124

- Alabama: $2,400

- South Carolina: $2,473

- Arkansas: $2,518

- Mississippi: $2,622

Mortgage debt

Mortgage debt makes up about 70% of total consumer debt in the U.S. Millennials hold more mortgage debt, on average, than other age groups.

Between 2018 and 2022, average mortgage debt grew from $199,990 to $236,443. This represents an increase of 18.2%.

The average homeowner in the Western U.S. has about $280,923 in mortgage debt, while the average Midwestern homeowner holds around $165,492 in mortgage debt. Average mortgage debt and median home purchase loan amounts also vary substantially by age and race/ethnicity.

| Age | Average mortgage debt |

|---|---|

| 18-25 (Generation Z) | $217,613 |

| 26-41 (Millennials) | $287,489 |

| 42-57 (Generation X) | $275,368 |

| 58-76 (Baby boomers) | $189,570 |

| 77+ (Silent generation) | $140,251 |

| Race/ethnicity | Median home purchase loan |

|---|---|

| White | $295,000 |

| Black/African American | $297,000 |

| Hispanic/Latino | $300,000 |

| Asian/Pacific Islander | $449,000 |

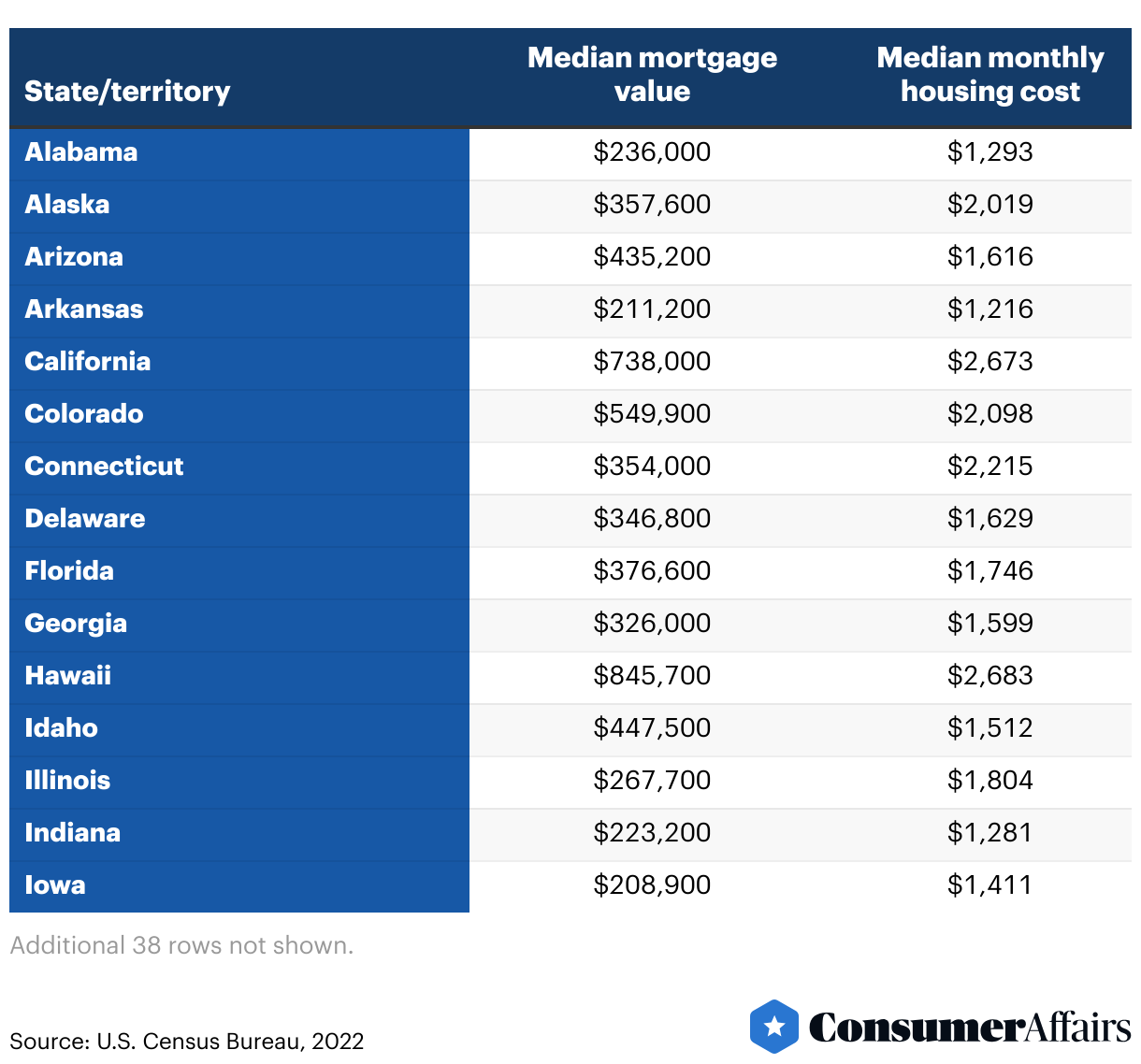

Owner-occupied housing units with mortgages

The median value and monthly housing cost of a mortgaged, owner-occupied housing unit vary widely from state to state.

FAQ

What are the current mortgage rates?

The average rate for a 30-year fixed-rate mortgage is 6.9% as of Feb. 22, 2024. The average rate for a 15-year fixed-rate mortgage is 6.29%.

What is the average price of a home purchase?

As of January 2024, the average sale price of a new home in the U.S. was $456,000. The median sale price was $420,700.

What are the average mortgage closing costs?

According to data from Assurance, the national average for mortgage closing costs is about $4,243.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Urban Institute, “Housing Finance: At A Glance Monthly Chartbook, January 2024.” Accessed Feb. 25, 2024.

- Federal Reserve Bank of New York, “Quarterly Report on Household Debt and Credit: 2023 Q4.” Accessed Feb. 25, 2024.

- U.S. Census Bureau, “Quarterly Residential Vacancies and Homeownership, Fourth Quarter 2023.” Accessed Feb. 25, 2024.

- U.S. Census Bureau, “Monthly New Residential Sales, December 2023.” Accessed Feb. 25, 2024.

- National Association of Realtors, “2023 Highlights From the Profile of Home Buyers and Sellers.” Accessed Feb. 25, 2024.

- Freddie Mac, “Mortgage Rates Continue to Rise, Nearing Seven Percent.” Accessed Feb. 25, 2024.

- Mortgage Bankers Association, “Mortgage Delinquencies Increase in the Third Quarter of 2023.” Accessed Feb. 26, 2024.

- Assurance, “Mapping Out Average Closing Costs Across the U.S.” Accessed Feb. 26, 2024.

- U.S. Census Bureau, “Housing Costs for Owners.” Accessed Feb. 26, 2024.

Figures