Homeownership Statistics by State (2026 Data)

+1 more

According to a 2004 United States Department of Housing and Urban Development analysis, homeownership is an important factor for building wealth in the U.S., especially for groups with lower incomes and people of color. Homeownership rates in the U.S. vary by geography and demographics, meaning that this source of wealth is not evenly distributed across the country. After the shocks of the 2004 foreclosure crisis and the 2008 Great Recession sent homeownership on a multi-year downturn, the national rate has recovered some of that loss since 2016.

Homeownership rates vary across geography and demographics, including age, race/ethnicity, and sex.

Jump to insightAt the end of 2023, it is estimated the U.S. had nearly 146 million housing units, 131 million of which were occupied.

Jump to insightHomeowners accounted for 59.1% of occupants, while renters accounted for 30.8%.

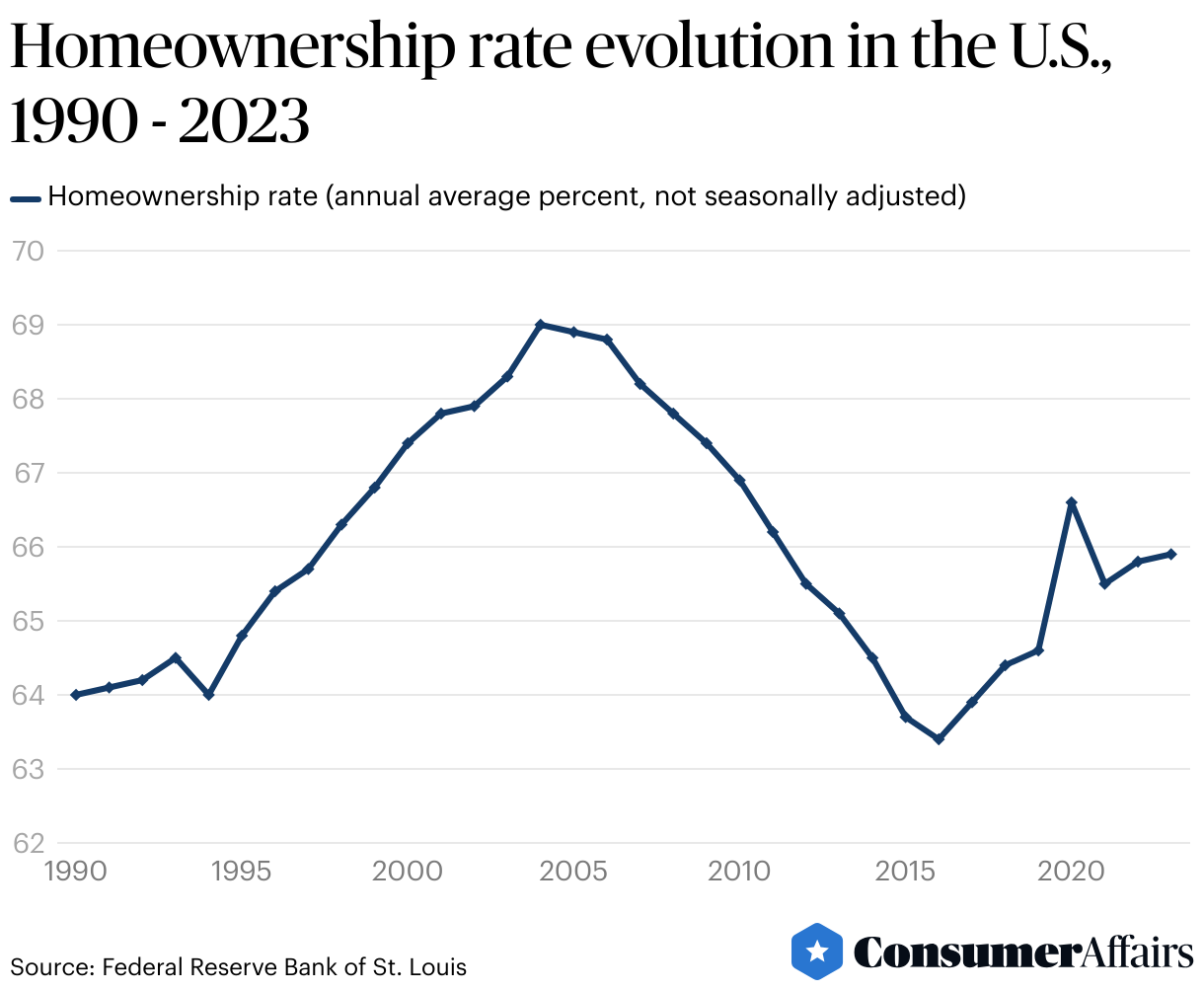

Jump to insightBetween 2004 and 2016, the national homeownership rate in the U.S. dropped from 69% to 63.4%, driven by the 2004 foreclosure crisis and the 2008 Great Recession.

Jump to insightBetween 2016 and 2023, the rate rose to 65.9%.

Jump to insightHome ownership statistics in the U.S. over time

Homeownership rates in the U.S. have fluctuated over time. In the 30 years between 1993 and 2023, the annual, average, non-seasonally-adjusted homeownership rate rose from 64.5% in 1993 to a high of 65.9% in 2023. The rate peaked in 2004 at 69%. After the 2004 foreclosure crisis, followed by the 2008 Great Recession, the rate tumbled to a low of 63.4% in 2016.

While it is difficult to estimate the homeownership rates in 2020 and 2021 due to the COVID-19 pandemic’s impact on census data collection, the homeownership rate rose by 1.2 points between 2019 and 2022 — an indication that the national rate weathered the storm.

In Q4 of 2023, the homeowner vacancy rate was 0.9%, and the median asking price for vacant units up on the market was $310,900. The rental vacancy rate was 6.6%, with a median monthly rent for vacant units of $1,465.

By the end of 2023, there were estimated to be nearly 146 million housing units in the U.S.; around 131 million were occupied, with homeowners occupying 59.1% and renters occupying 30.8%.

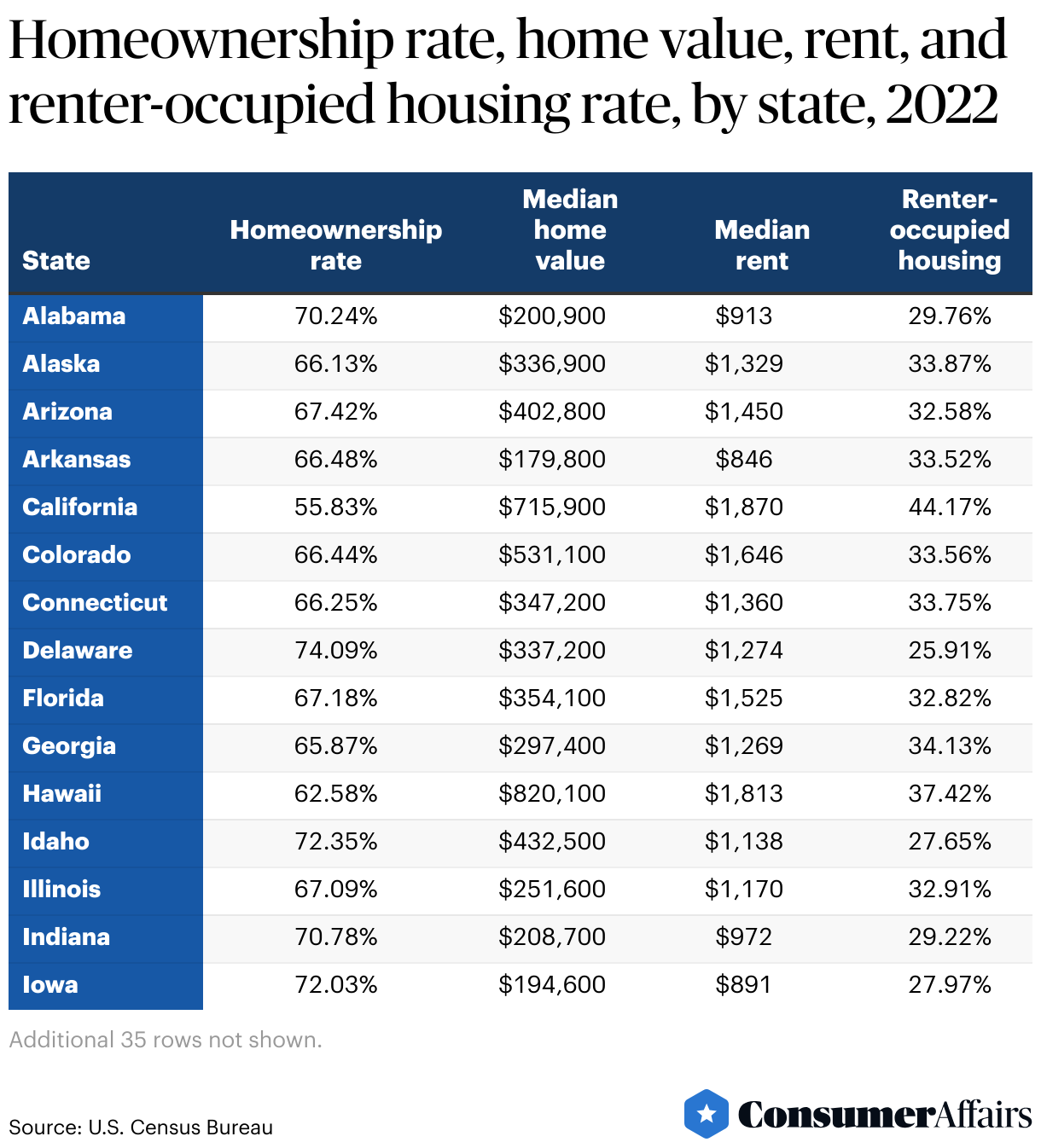

Homeownership by state statistics

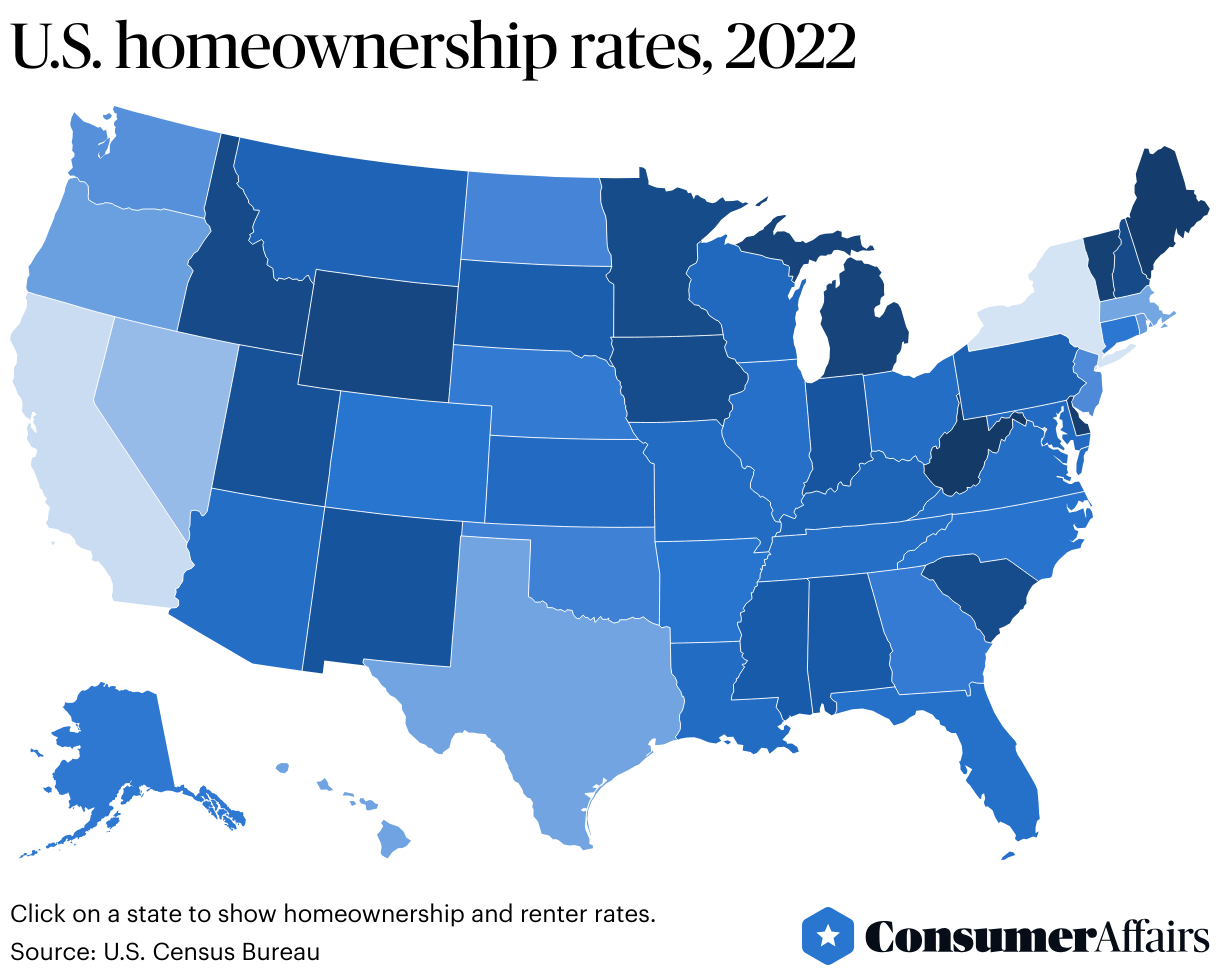

Homeownership rates in the U.S. vary across states. The “state” with the lowest homeownership in 2021 was New York, where residents owned 54.1% of occupied housing units. West Virginia had the highest state homeownership rate at 74.5%.

Rates of home vacancies also varied by state, with Maryland having the lowest rate of owner-vacant homes at 0.1% and South Dakota having the highest rate at 1.8%.9 Many factors impact homeownership rates, including the state of the economy, housing prices, opportunities for employment, and generational preferences.

The average sales price of U.S. homes sold in the fourth quarter of 2023 was $492,300.

Homeownership demographics

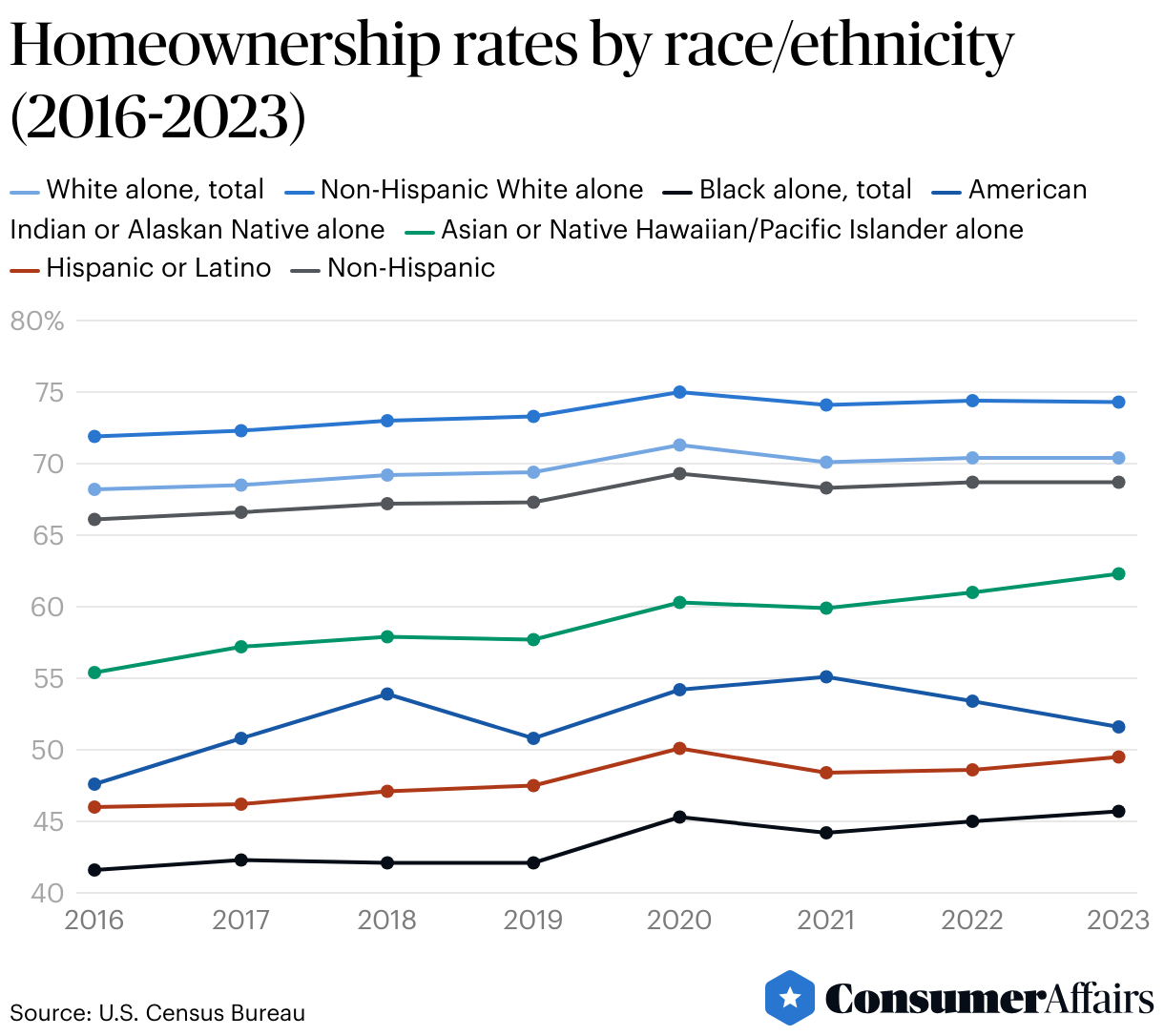

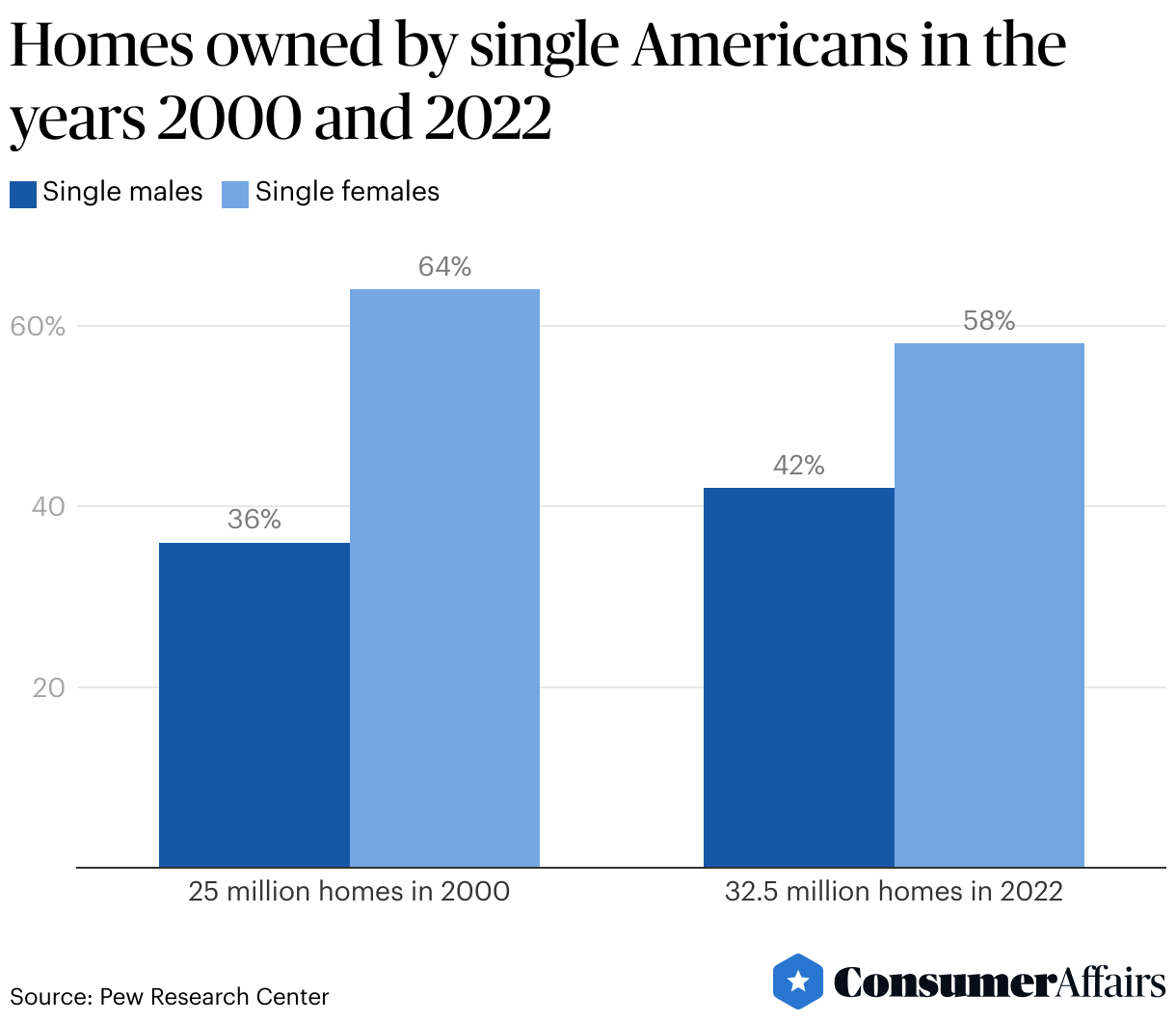

Homeownership rates in the U.S. vary significantly by demographics like race, age, and gender. While 74.3% of non-Hispanic White Americans owned homes in 2023, the rate was only 45.7% for Black Americans. Homeownership increases with age, from 38.6% for those under 35 to 79% for those 65 and older. There are more single female homeowners than single males, potentially due to females' longer life expectancy putting more of them in the older age brackets with higher homeownership rates.

Race and ethnicity

In addition to geography, homeownership rates also vary by demographics, such as race and ethnicity. In 2023, 74.3% of Americans identifying as non-Hispanic White were homeowners. By contrast, Black Americans had a homeownership rate of 45.7%.

Between 2016 and 2023, homeownership rates increased for all racial and ethnic groups captured in the U.S. Census. However, certain groups saw greater increases than others. Homeownership rates rose by less than five percentage points for those identifying as Black, Hispanic or Latino, American Indian or Alaskan Native, or White. The rate for those identifying as Asian or Native Hawaiian/Pacific Islander rose by 6.9% during that same period.

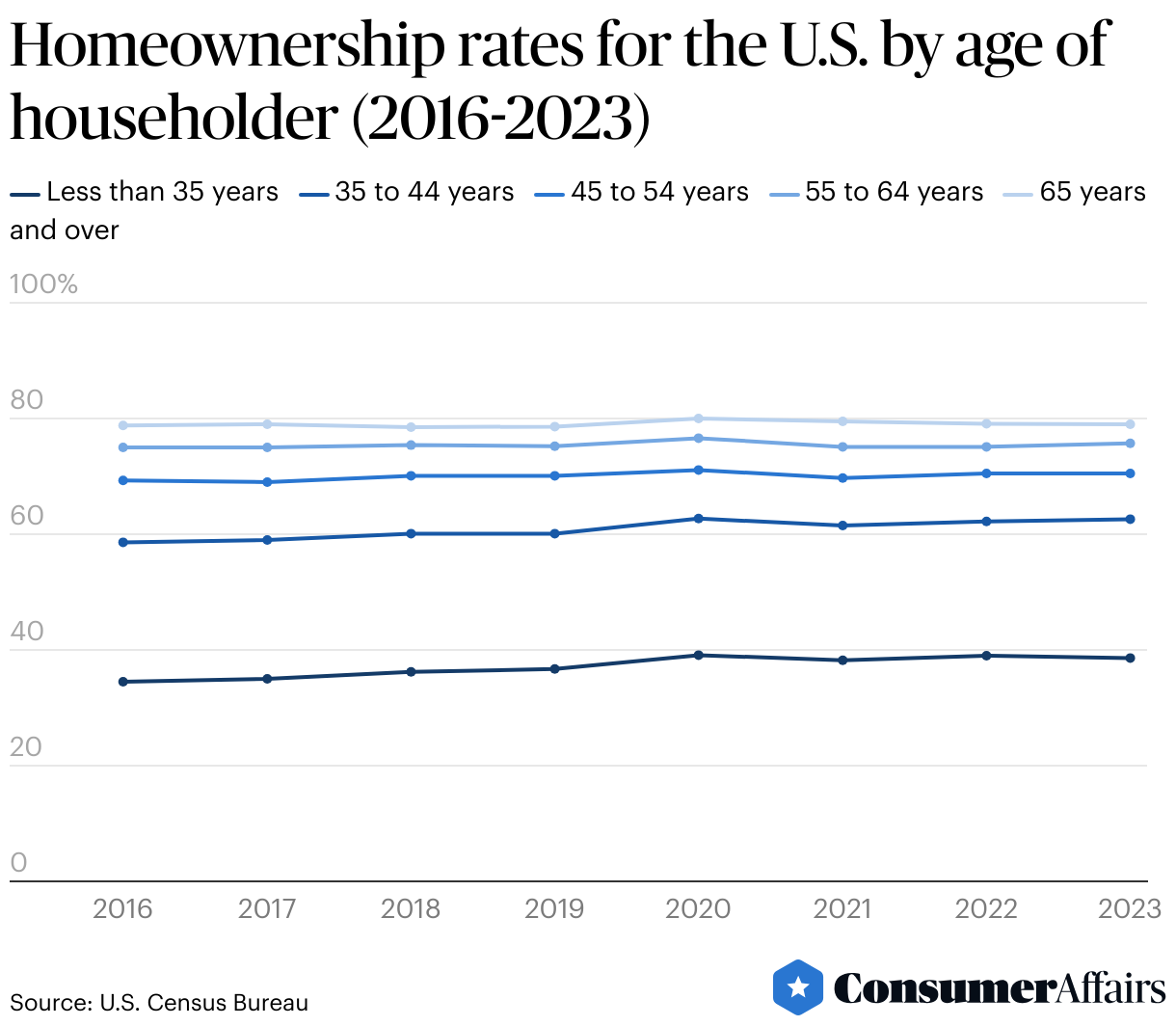

Age

Different age groups also experience different rates of homeownership. Rates are higher among older age groups. In 2023, 38.6% of people in the U.S. who were younger than 35 years old were homeowners. By contrast, 79% of those aged 65 and older were homeowners.

People below the age of 44 account for most of the recovery in homeownership rates after 2016. Between 2016 and 2023, homeownership rates among those younger than 35 rose by 4.1 percentage points; a similar increase occurred among those aged 35 to 44. During that same period, the increase in homeownership rates was more modest for those aged 45 to 54 (1.2 points), 55 to 64 (0.7), and those aged 65 and older (0.2 points). Between 2020 and 2021, amid the COVID-19 pandemic, all of these age groups saw a drop in homeownership rates.

Gender

In the U.S., there are more single female homeowners than single male homeowners; however, this gap has narrowed over time. In 2000, around 25 million homes were owned by single Americans. Of these homes, 64% were owned by females, and 36% were owned by males. By 2022, there were around 35.2 million homes owned by single Americans, with 58% owned by females and 42% owned by males. While the percentage of homes owned by single females decreased by six points over that period, the rate for single males increased by six percentage points.

This difference is not due to females having greater financial resources. In fact, single female household heads were less likely to own their home than male household heads across most age groups in 2023. Females also typically have lower incomes than males. In 2019, the incomes of single females who were heads of households were 88% that of their male counterparts. The median household wealth of these females was also around 10% lower than that of males.

So, what explains this counterintuitive sex discrepancy in homeownership? One explanation may be the longevity differences between females and males. Females typically have a longer life expectancy than males, leading to more single female household heads, especially among older Americans. While life expectancy for both females and males in the U.S. has risen over time, male lifespans have lengthened at a faster rate, narrowing the life expectancy gap between the sexes.

As a possible result, female household heads skew older than their male counterparts. In 2022, one-third of single female household heads were aged 65 or older, while only 22% of single male household heads were in that age group. Older single household heads are more likely to own their homes. Among single household heads of both sexes aged 65 and up, 70% were homeowners, while only 44% of single household heads between the ages of 35 and 44 owned their home. Putting this all together, females make up a larger proportion of the age group that is most likely to own their home.

FAQ

What is the U.S. homeownership rate?

In 2023, the annual, average, non-seasonally-adjusted homeownership rate in the U.S. was 65.0%.

Did the COVID-19 pandemic impact the homeownership rate in the U.S.?

While it is difficult to determine the homeownership rates in 2020 and 2021, the rate increased by 1.2 percentage points between 2019 and 2022, indicating that the U.S. rebounded from any pandemic impacts.

What is the impact of race and gender on homeownership rates?

Homeownership rates are impacted by several factors, including race, sex, and age. In 2023, non-Hispanic White people had the highest homeownership rate across all other census-defined racial and ethnic groups. Most homeowners were female, and homeownership rates were highest among older people.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Property Shark, “2024 Homeownership Rates in the U.S. by State and City.” Accessed Mar. 11, 2024.

- Pew Research Center, “Single women own more homes than single men in the U.S., but that edge is narrowing.” Accessed Mar. 12, 2024.

- United States Census Bureau, “Quarterly Residential Vacancies And Homeownership, Fourth Quarter 2023.” Accessed Mar. 12, 2024.

- United States Census Bureau, “Housing Vacancies and Homeownership (CPS/HVS).” Accessed Mar. 12, 2024.

- United States Census Bureau, “Table 3. Homeownership Rates by State: 2005 to 2023.” Accessed Mar. 22, 2024.

- United States Census Bureau, “Table 2. Homeowner Vacancy Rates by State: 2005 to 2023.” Accessed Mar. 22, 2024.

- Federal Reserve Bank of St. Louis, “Homeownership Rate in the United States.” Accessed Mar. 22, 2024.

- United States Census Bureau. “Table 22. Homeownership Rates by Race and Ethnicity of Householder.” Accessed Mar. 22, 2024.

- United States Census Bureau, “Table 17. Homeownership Rates by Age of Householder and Family Status for the United States.” Accessed Mar. 22, 2024.

- Centers for Disease Control and Prevention, “Life expectancy at birth, age 65, and age 75, by sex, race, and Hispanic origin: United States, selected years 1900–2019.” Accessed Mar. 22, 2024.

- United States Census Bureau, “Younger Householders Drove Rebound in U.S. Homeownership.” Accessed Mar. 22, 2024.

- Federal Reserve Bank of St. Louis, “Average Sales Price of Houses Sold for the United States.” Evaluated Mar. 31, 2024.

- United States Census Bureau, “DP04: Selected Jousing Characteristics.” Accessed Apr. 2, 2024.

Figures