Consumer Banking Statistics (2026 Data)

+1 more

Consumer banking is a changing industry. Decades of consolidation have reduced the total number of banks available to consumers, although the number of bank branches has not decreased at nearly the same rate. While the vast majority of U.S. adults use a bank account to manage their money and conduct financial transactions, their access methods have shifted. More than two-thirds of banking customers now prefer to conduct their banking business online or via a mobile app.

In the U.S., 94% of adults live in a household with access to a banking account.

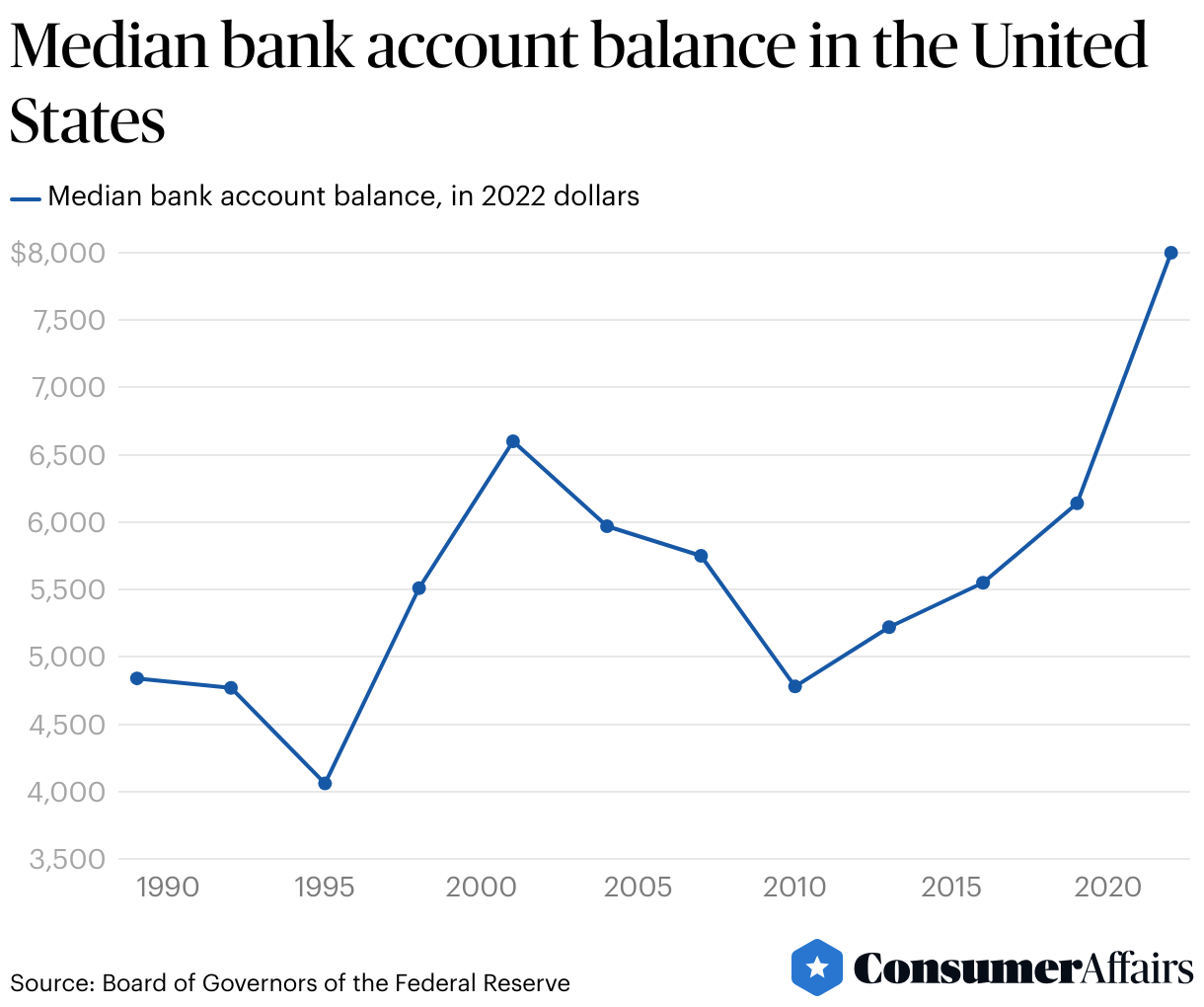

Jump to insightIn 2022, the median bank balance for a household in the U.S. was $8,000.

Jump to insightThe majority of adults regularly conduct their banking business either online or with a mobile app. Seventy-one percent of adults cited digital channels as their preferred method of banking.

Jump to insightCommercial bank consolidation has decreased the number of banks available to U.S. consumers. At the end of 2022, there were 4,136 FDIC-insured commercial banks, down from 14,434 in 1980.

Jump to insightConsumer banking statistics

Most adults in the U.S. have access to some type of banking account, whether it's a savings, checking or money market account. In 2022, 94% of adults (or their spouse/partner) had a banking account, unchanged from survey data in the prior year. Notably, the number of adults who are “unbanked” (without a bank account) increases substantially for those in lower income brackets. For adults with a household income below $25,000, 17% did not have a bank account.

The Federal Deposit Insurance Corporation (FDIC) keeps statistics on the number of households that are “underbanked” (defined as an otherwise banked household that needs to use nonbank financial products, such as check cashing, rent-to-own, or tax refund anticipation services). According to the most recent data in 2021, 14.1% of U.S. households qualify as underbanked.

Average bank account balances

As of 2022, the median U.S. household had an $8,000 bank account balance. That number is the highest in the 30 years the Federal Reserve has been collecting such data.

Among demographic factors that impact bank account balances, the top criteria are education levels and family structure. The median account balance for someone without a high school diploma is $900, while that number increases to $23,100 among college graduates. Similarly, the median balance for a single adult with at least one child is $2,500, while a couple with no children holds a $16,000 balance.

Geographically, the median bank balance is highest in the Western region of the country ($11

,000) and lowest in the South ($6,000). Those who live within a metropolitan area have a median bank account balance of $8,800, while the figure for those who live outside metro areas is $5,000.How much banking is done online?

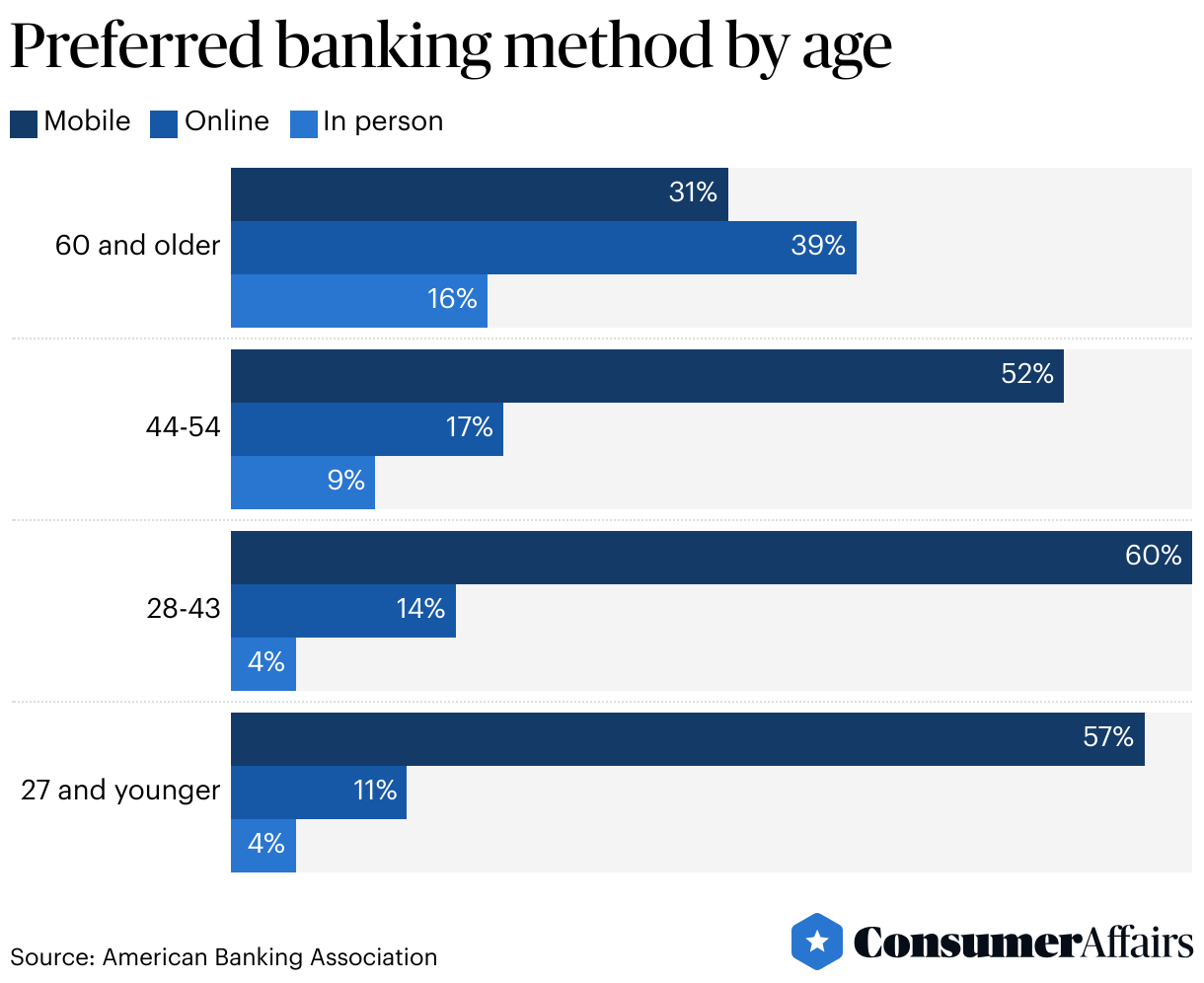

The share of adults in the U.S. who conduct some or all of their banking online or with a mobile app substantially continues to rise. A survey commissioned by the American Bankers Association (ABA) found that 71% of adults prefer to use mobile apps or online banking to manage their bank accounts. Comparatively, only 9% indicated that their preferred method of banking was in person at a physical bank branch.

The ABA survey tracks with data released by Statista showing that in the final quarter of 2023, 64% of bank account holders used their smartphone or tablet to conduct banking. Statista also reports that 47% of consumers conducted banking business in person at a branch.

Not surprisingly, preferred banking methods are correlated with age.

Banking system alternatives

Cryptocurrency is considered by some as an alternative to the traditional banking system. While data on the usage of cryptocurrency doesn’t go back very far, the Federal Reserve reports that in 2022, 10% of adults held or used cryptocurrency. This number was slightly lower than it had been in 2021, when 12% held or used crypto. Comparable data is not available for prior years.

Largest banks in the United States

The largest banks in the U.S. have been getting bigger over time. The table below shows the 10 largest banks in the country, ranked by their domestic deposits. Between them, these banks account for nearly half of all deposit value in the U.S., at 49.04%.

| Banking institution | Domestic deposits ($ in millions) | % share of domestic deposits |

|---|---|---|

| JPMorgan Chase | $2,068,042 | 11.98% |

| Bank of America | $1,879,161 | 10.88% |

| Wells Fargo Bank | $1,360,215 | 7.88% |

| Citibank | $757,135 | 4.38% |

| U.S. Bank | $526,742 | 3.05% |

| PNC Bank | $434,511 | 2.52% |

| Truist Bank | $418,239 | 2.42% |

| Capital One | $367,821 | 2.13% |

| Goldman Sachs | $352,195 | 2.04% |

| TD Bank | $303,901 | 1.76% |

How many FDIC-insured banks are there?

As of the third quarter of 2023, there were a total of 4,049 FDIC-insured commercial banks in the U.S. These include different types of banks, from community banks to online banks to larger, nationwide banks. Since 1980, bank consolidations have significantly decreased the total number of banks in the country.

Although the number of commercial banks in the U.S. has fallen due to consolidation, the number of total bank branches has actually increased over the past 45 years. In 1980, there were 38,738 total bank branches; in 2022, that number had more than doubled to 69,905. The below table shows the total number of commercial banks and branches in the United States

| Commercial banks | Bank branches | |

|---|---|---|

| 2022 | 4,136 | 69,905 |

| 2021 | 4,238 | 70,644 |

| 2020 | 4,379 | 73,107 |

| 2010 | 6,519 | 82,011 |

| 2000 | 8,315 | 64,213 |

| 1990 | 12,347 | 50,199 |

| 1980 | 14,434 | 38,738 |

Note that these numbers do not include credit unions. Credit unions are insured by a separate agency, the National Credit Union Administration (NCUA). According to the NCUA, as of the third quarter of 2023, there were 4,645 credit unions in the U.S.

In the wake of the Great Depression in 1933, the Federal Deposit Insurance Corporation (FDIC) was founded to boost public confidence in the U.S. financial system. One of the primary ways the FDIC accomplished this goal was by insuring deposits in financial institutions. Currently, the FDIC insures deposits up to $250,000 per customer.

Banks obtain FDIC insurance by becoming members and paying into the system. This helps banks attract consumers, by providing them with the assurance that their bank deposits are insured.

Average FDIC national rates over time

The FDIC is responsible for providing regular updates to national deposit rates and setting rate caps for financial products. Over time, those rates fluctuate in response to the interest rates set by the Federal Reserve, and other economic factors.

Generally speaking, when the Federal Reserve sets higher interest rates, consumers receive greater returns on money they have deposited in interest-bearing accounts, such as savings accounts, money market accounts and certificates of deposit (CDs).

Between March 2022 and July 2023, the Federal Reserve raised interest rates from 0.25% to 5.25%, the fastest pace in recent history. Prior to this series of increases, rates had been near all-time lows to encourage recovery from the COVID-19 recession.

As a result, rates of return on consumer deposit accounts have also been rising. For example, the national deposit rate on savings accounts grew from .06% in May of 2022 to .46% in February of 2024.

FAQ

How much does the average person have in their bank account?

According to the 2022 Federal Reserve’s Survey of Consumer Finances, the median household bank account balance in 2022 in the U.S. was $8,000.

What percentage of consumers use online banking?

Consumer surveys report that more than 60% of adults use either online banking platforms or mobile apps to conduct their banking business. Seventy-one percent of adults identified mobile and online banking as their preferred methods of banking. More adults use online banking than in-person banking.

What percentage of Americans have a personal banking account?

The Federal Reserve released data showing that 94% of U.S. adults live in a household where either they, their partner, or spouse have a bank account. When household income is below $25,000, that number drops to 83%.

How many banks are there in the United States?

At the end of 2022, there were 4,136 FDIC-insured commercial banks in the U.S. Those banks had a total of 69,905 bank branches.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Board of Governors of the Federal Reserve, “Report on the Economic Well-Being of US Households in 2022.” Accessed Mar. 6, 2024.

- Board of Governors of the Federal Reserve, “Survey of Consumer Finances. Board of Governors of the Federal Reserve.” Accessed Mar. 6, 2024.

- American Banking Association, “Consumer Survey Banking Methods 2023.” Accessed Mar. 6, 2024.

- Federal Deposit Insurance Corporation, “BankFind Suite: Annual Historical Bank Data.” Accessed Mar. 6, 2024.

- Federal Deposit Insurance Corporation, “FDIC National Survey of Unbanked and Underbanked Households.” Accessed Mar. 6, 2024.

- Board of Governors of the Federal Reserve, “Survey of Consumer Finances (historic data tables).” Accessed Mar. 6, 2024.

- Statista, “Mobile banking usage in the U.S. 2019-2023, by quarter.” Statista. Accessed Mar. 6, 2024.

- Statista, “Branch banking usage in the U.S. 2019-2023, by quarter.” Accessed Mar. 6, 2024.

- Federal Deposit Insurance Corporation, “Top 50 Commercial Banks and Savings Institutions by Total Domestic Deposits.” Accessed Mar. 6, 2024.

- Federal Deposit Insurance Corporation, “Deposit Market Share Reports - Summary of Deposits.” Accessed Mar. 6, 2024.

- Federal Deposit Insurance Corporation, “Statistics at a Glance.” Accessed Mar. 6, 2024.

- National Credit Union Administration, “Quarterly Credit Union Data Summary 2023 Q3.” National Credit Union Administration. Accessed Mar. 6, 2024.

- Board of Governors of the Federal Reserve System, “FOMC’s target federal funds rate or range, change (basis points) and level.” Accessed Mar. 7, 2024.

- Federal Reserve Bank of St. Louis, “National Deposit Rates: Savings.” Accessed Mar. 7, 2024.

Figures