Life insurance statistics 2026

+1 more

Life insurance policyholders agree to make regular payments to insurance companies in exchange for a guaranteed death benefit. That benefit is paid to the policyholder’s beneficiaries if the policyholder dies while their policy is still active.

Although many Americans can benefit from life insurance, its use has declined in recent years. This dip in coverage may be attributable to misconceptions about the cost of life insurance and a lack of knowledge of the varieties of life insurance products that exist.

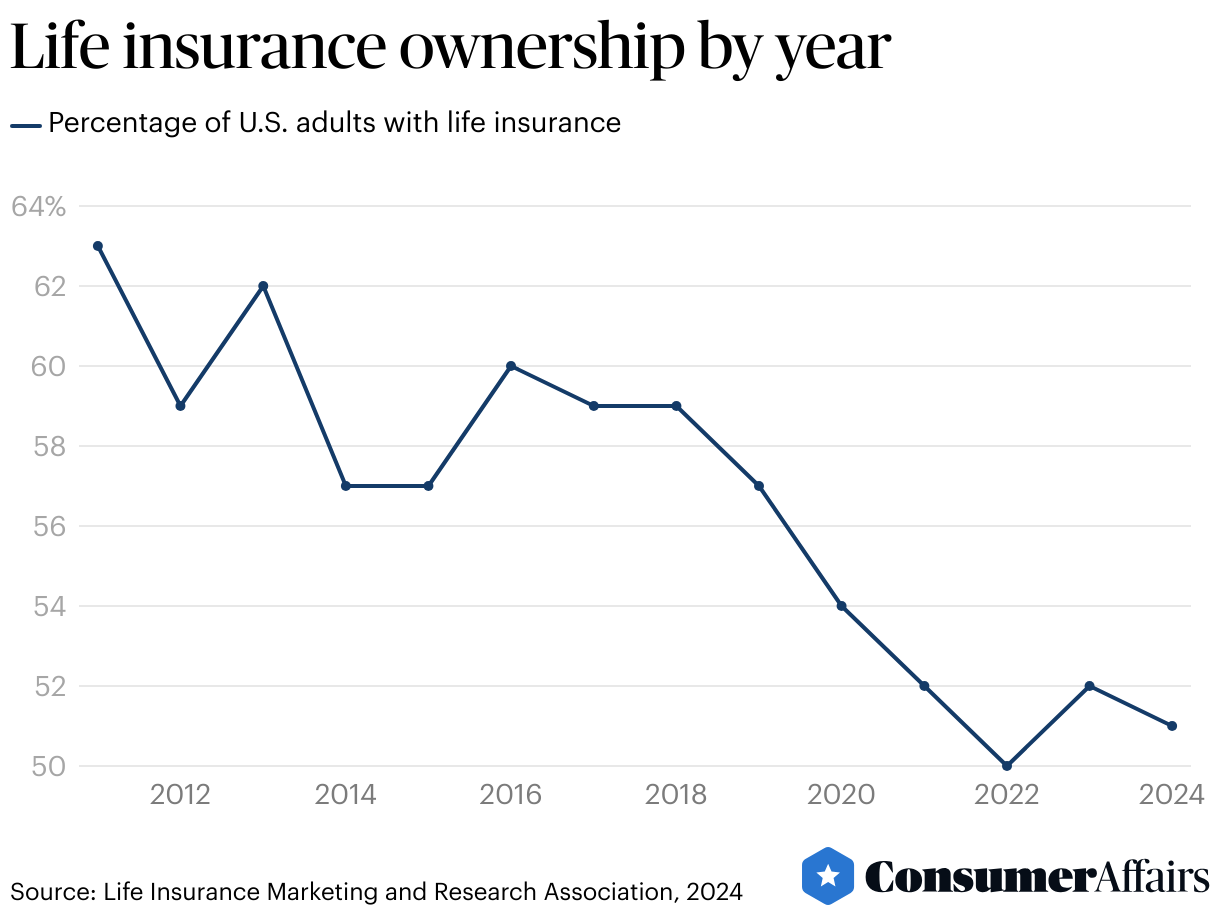

The share of American adults who reported having life insurance dropped from 63% in 2011 to 51% in 2024.

Jump to insightThere are an estimated 102 million adults in the U.S. who want more life insurance coverage.

Jump to insightAmericans identifying as Black, male, members of the baby boomer generation and those who have high incomes are more likely to have life insurance than members of other demographic sectors.

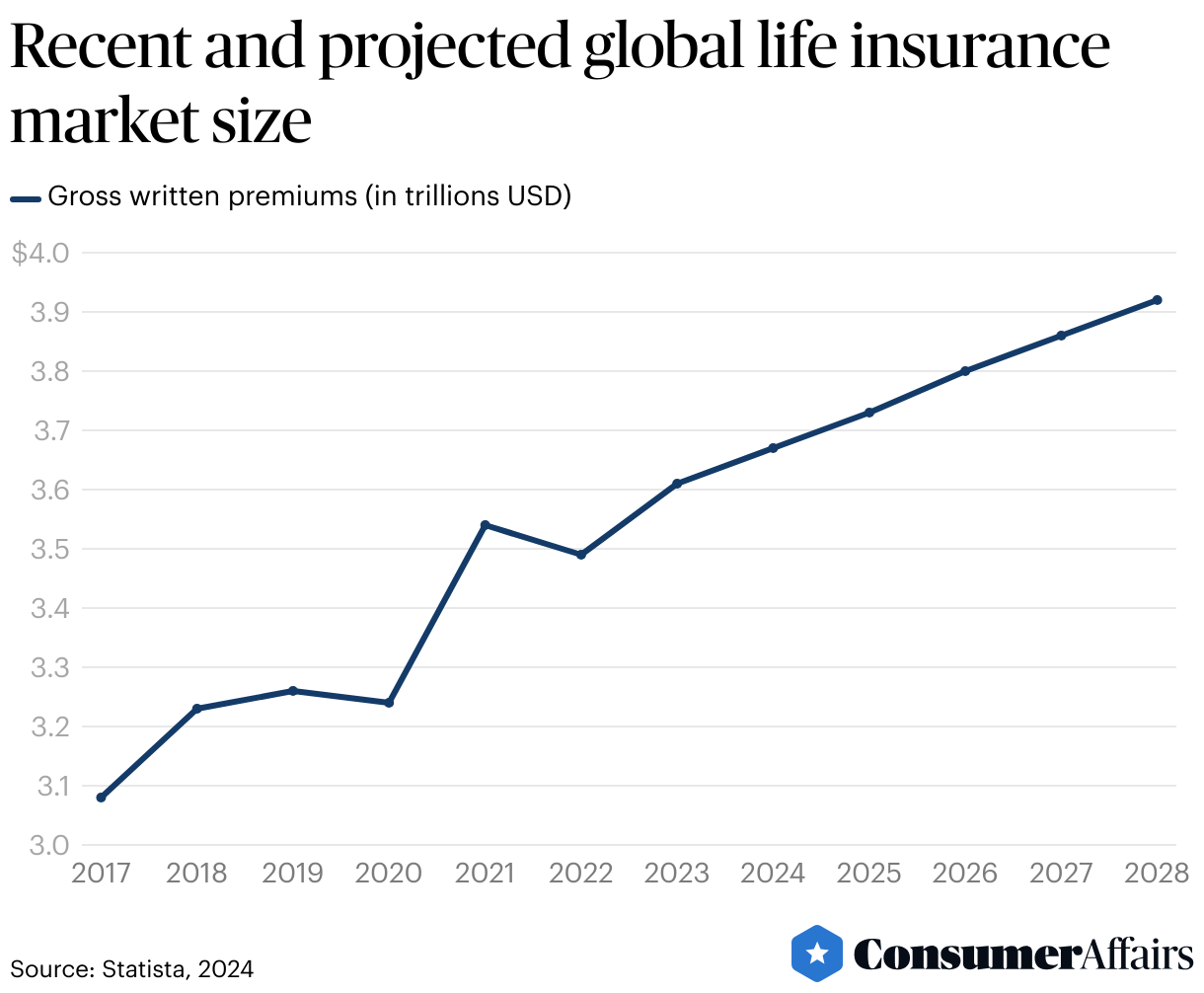

Jump to insightThe global life insurance market size is projected to reach $3.92 trillion in 2028.

Jump to insightLife insurance statistics

There are two ways to get life insurance: You can either purchase it yourself as an individual or receive it through your employer. Individual coverage is more common. Of all the Americans who report having some kind of life insurance, 55% have individual coverage only, 26% solely have workplace coverage and 19% have both.

Perceived expense is the most frequently cited explanation for why consumers don’t purchase life insurance. However, 72% of American adults overestimate the price of a standard term life insurance policy, according to a study by the Life Insurance Marketing and Research Association (LIMRA).

Number and percentage of people with life insurance

About 51% of adults in the U.S. had life insurance as of January 2024, according to LIMRA. The share of American adults who report having life insurance has been generally trending downward for several years. In 2011, 63% of American adults reported having life insurance, but only 50% reported having life insurance in 2022.

Among those who didn’t have life insurance policies in January 2024, about 30% said they needed life insurance. Among those who did have life insurance of some kind, 11% said they needed more coverage. In total, that makes about 102 million American adults who lack satisfaction with their level of life insurance coverage.

Life insurance owner demographics

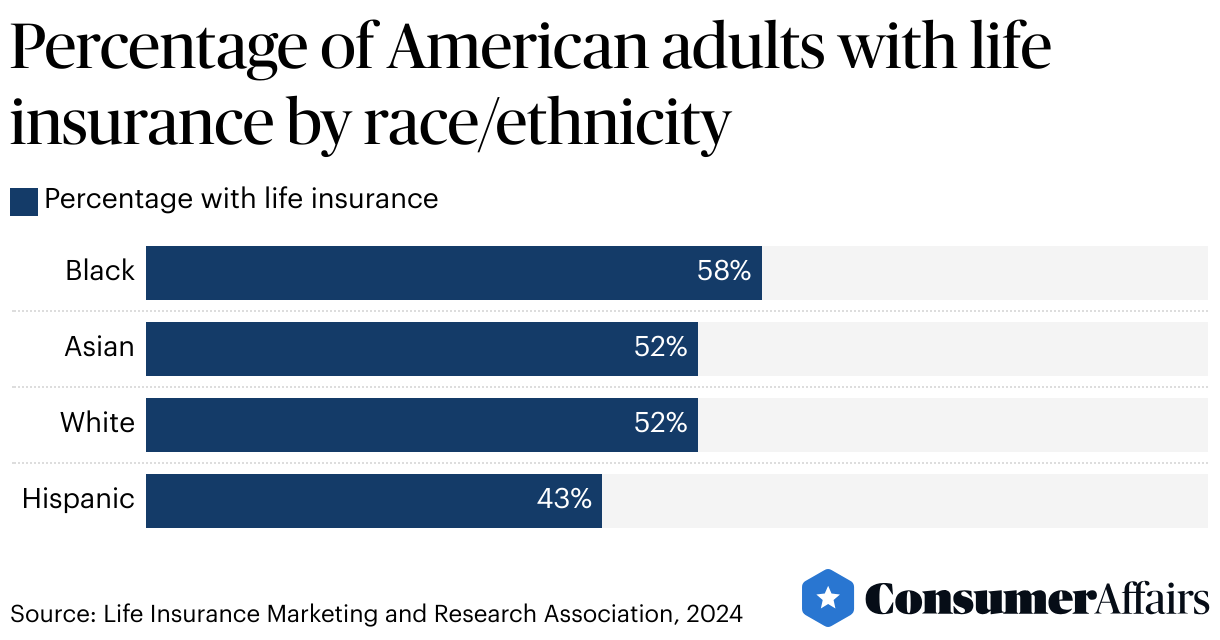

Ownership rates of life insurance vary by racial and ethnic group, income, gender and generation.

Adults identifying as Black have the highest life insurance ownership rate of the four racial and ethnic groups in the U.S. that were surveyed by LIMRA. In January 2024, 58% of Black Americans had life insurance. On the other hand, only 43% of Hispanic Americans had life insurance — the least covered among the four racial and ethnic groups surveyed.

High earners are another group that enjoys a higher-than-usual share of life insurance coverage. About 71% of Americans who make $150,000 or more per year have life insurance.

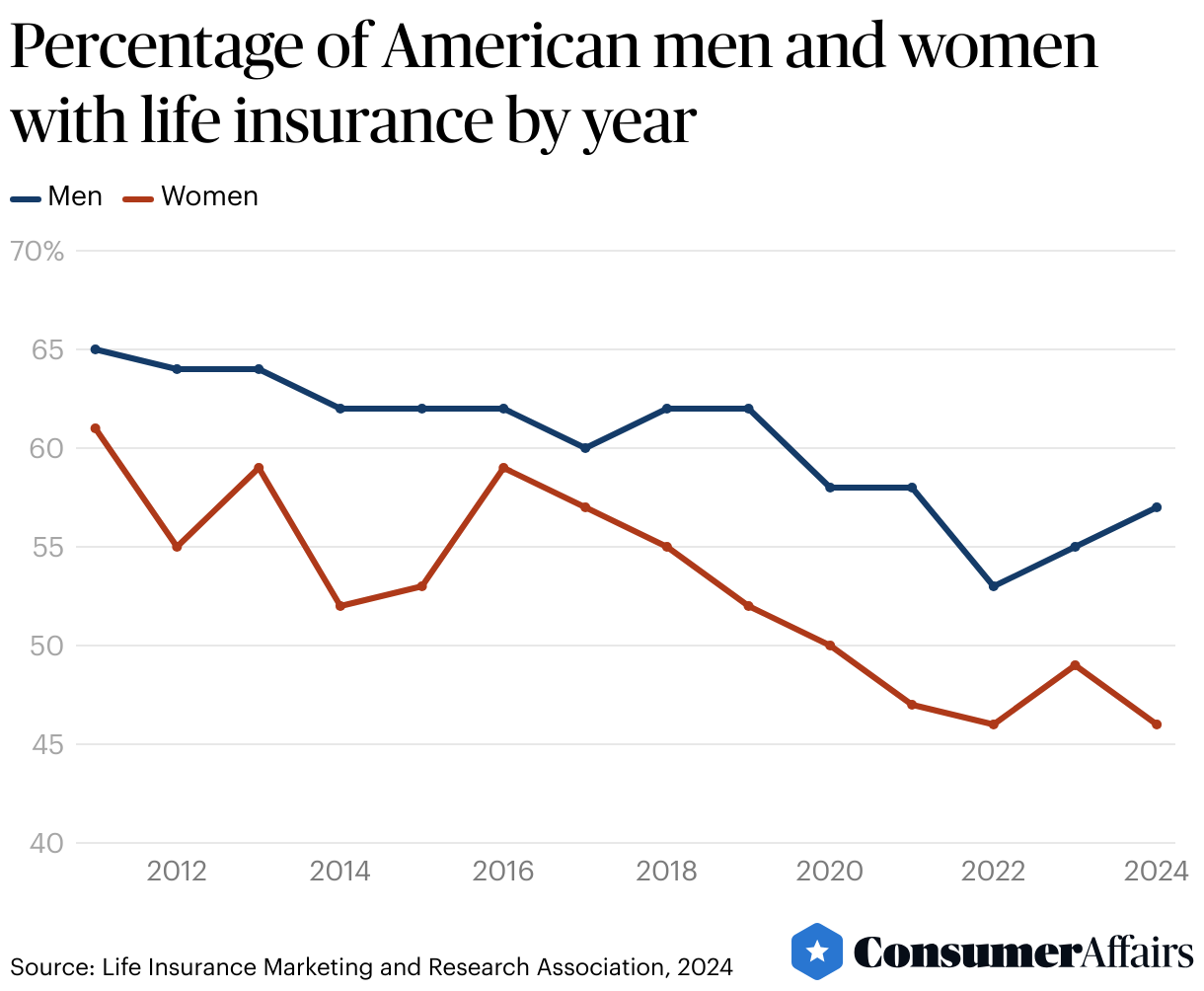

By gender

Men are more likely to have life insurance than women. In January 2024, 57% of American men had life insurance, compared with only 46% of American women. An estimated 56 million American women feel that they need more life insurance coverage.

Although the life insurance gender gap has varied over time, men are consistently more likely to be covered by life insurance than women.

In 2023, less than one-fourth (22%) of women surveyed by LIMRA said they felt “very knowledgeable about life insurance,” while 33% of men said the same. Men are more likely than women to identify life insurance as a financial priority, and men also express greater certainty regarding the type of life insurance policy they should buy.

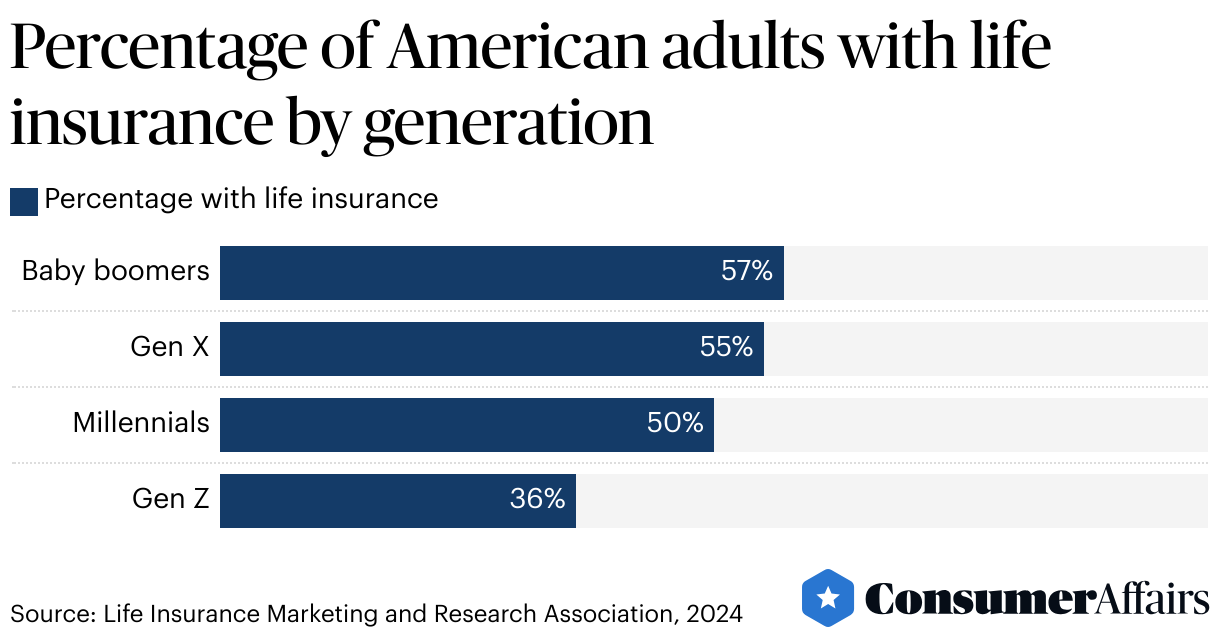

By generation

Baby boomers are more likely to own life insurance than the other three generations surveyed by LIMRA. Baby boomers, 57% of who own life insurance, are followed closely by members of Generation X with a 55% rate of ownership. Only 36% of adults who belong to Gen Z, the youngest generation surveyed, have life insurance.

Though younger Americans are currently less likely to own life insurance than their elders, that doesn’t mean they’re altogether disinterested in life insurance. In January 2023, 44% of Gen Z adults indicated that they intended to buy life insurance within a year.

Life insurance market size

Insurance markets are measured in gross written premiums, which refers to the combined amount that insurance companies earn from policy premiums each year. A premium is the amount of money that a policyholder pays for their policy.

The global life insurance market is projected to reach $3.67 trillion in gross written premiums this year. From 2024 to 2028, the market is expected to have a compound annual growth rate of 1.66% and reach a market size of $3.92 trillion in 2028.

The U.S. life insurance market is expected to generate more than $1.27 trillion in gross written premiums in 2024, making it the largest life insurance market of any country in the world. But other countries with sizable elderly populations, like Japan, have also experienced fast growth rates in their life insurance markets.

FAQ

What is the largest life insurance company?

MetLife, Inc. was the largest life insurance company in the U.S. by direct premiums written as of 2022.

What are the types of life insurance?

There are seven main types of life insurance:

- Term

- Whole

- Universal

- Variable

- Simplified issue

- Guaranteed

- Group

What’s the difference between life insurance and an annuity?

The main difference between life insurance and an annuity is that each is intended to protect people from different outcomes. Life insurance allows you to make regular payments to an insurance company in exchange for a guaranteed death benefit. That death benefit will be paid out to your beneficiaries if you die from a covered cause while your policy is active.

Annuities also involve the payment of premiums to an insurance company, but the insurer then makes a series of payments to the annuity’s purchaser. These payments may last for either a limited period of time or until the purchaser dies, giving them a revenue stream that can prevent them from running out of money in retirement.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Life Insurance Marketing and Research Association, “2024 Insurance Barometer Study.” Accessed May 1, 2024.

- Life Insurance Marketing and Research Association, “2023 Life Insurance Fact Sheet.” Accessed May 1, 2024.

- Life Insurance Marketing and Research Association, “Women and Life Insurance.” Accessed May 1, 2024.

- Life Insurance Marketing and Research Association, Life Happens, “New Study Shows Interest in Life Insurance at All-Time High in 2023.” Accessed May 1, 2024.

- Statista, “Life insurance - Worldwide.” Accessed May 1, 2024.

- Insurance Information Institute, “The Difference Between Annuities And Life Insurance.” Accessed May 1, 2024.

- Wisconsin Office of the Commissioner of Insurance, “Consumer’s Guide to Understanding Annuities.” Accessed May 1, 2024.

Figures