Refinancing your car

+1 more

Owning a car means having the ability to pack up and travel at a moment’s notice. It’s also a critical component of job security, especially in a country as large as the United States. Commute times to and from the office can vary widely, and not everyone is within walking distance of mass transit. These are just a few of the reasons why more than 90% of American households have access to at least one car.

With the convenience of car ownership comes the responsibility and challenge of purchasing and maintaining such a significant piece of machinery. Finding the money to purchase a new vehicle is a common concern — one way Americans overcome this hurdle is to take out a loan. Car loans allow people who might otherwise be unable to afford a new car to pay in a series of monthly installments — with interest added, of course.

Car loan terms differ widely. As a general rule, though, individuals with poor credit tend to face extremely high interest rates, while those with good credit have the opportunity to pay much less over time for the same vehicle. So we wondered: When is a good time to refinance your car for a better rate?

We surveyed 1,000 car owners in the U.S. to see what information we could glean about car loans and how they impact borrowers. Keep reading for more information about the potential benefits of pursuing new terms.

Refinancing saved Americans an average of over $3,500 in interest payments over the course of their loan term.

Jump to insightA third of Americans had been late on their monthly car payment at least once.

Jump to insightOne in 4 respondents said they would consider selling their cryptocurrency for a new car.

Jump to insightLoan lessons

For some drivers, purchasing a new vehicle is one of the most expensive decisions they’ll ever make. And, while the money they spend varies between brands as well as between new and used models, the inescapable truth is that car prices in general are increasing.

Buyers interested in used vehicles can expect to pay 45% more than they would have a year ago. New vehicles cost more too, with Cars.com finding an increase of 18% in price compared with November 2020. The root of this significant jump in price for both new and used vehicles is tied to the COVID-19 pandemic, with significant dips in supply. As workplaces continue to grapple with health crises, car manufacturing supplies have dropped along with the output of new vehicles.

What does this mean for today’s buyer? Car loans must increase in tandem with car prices, which means borrowers are looking at spending more money, potentially over a longer period of time, than they would have in the past. This can be a serious pitfall depending on the type of car loan you get. There are four main types of car loans, with varying rates:

- Secured car loans: These loans allow lenders to repossess the vehicle if the loan defaults.

- Simple interest car loans: These loans allow buyers to pay less interest overall the sooner they pay off their loan.

- In-house financing: This type of financing is done in-house at the dealership, which means buyers pay the dealership monthly car payments.

- Indirect financing: This type of financing refers to loans given by credit unions or banks.

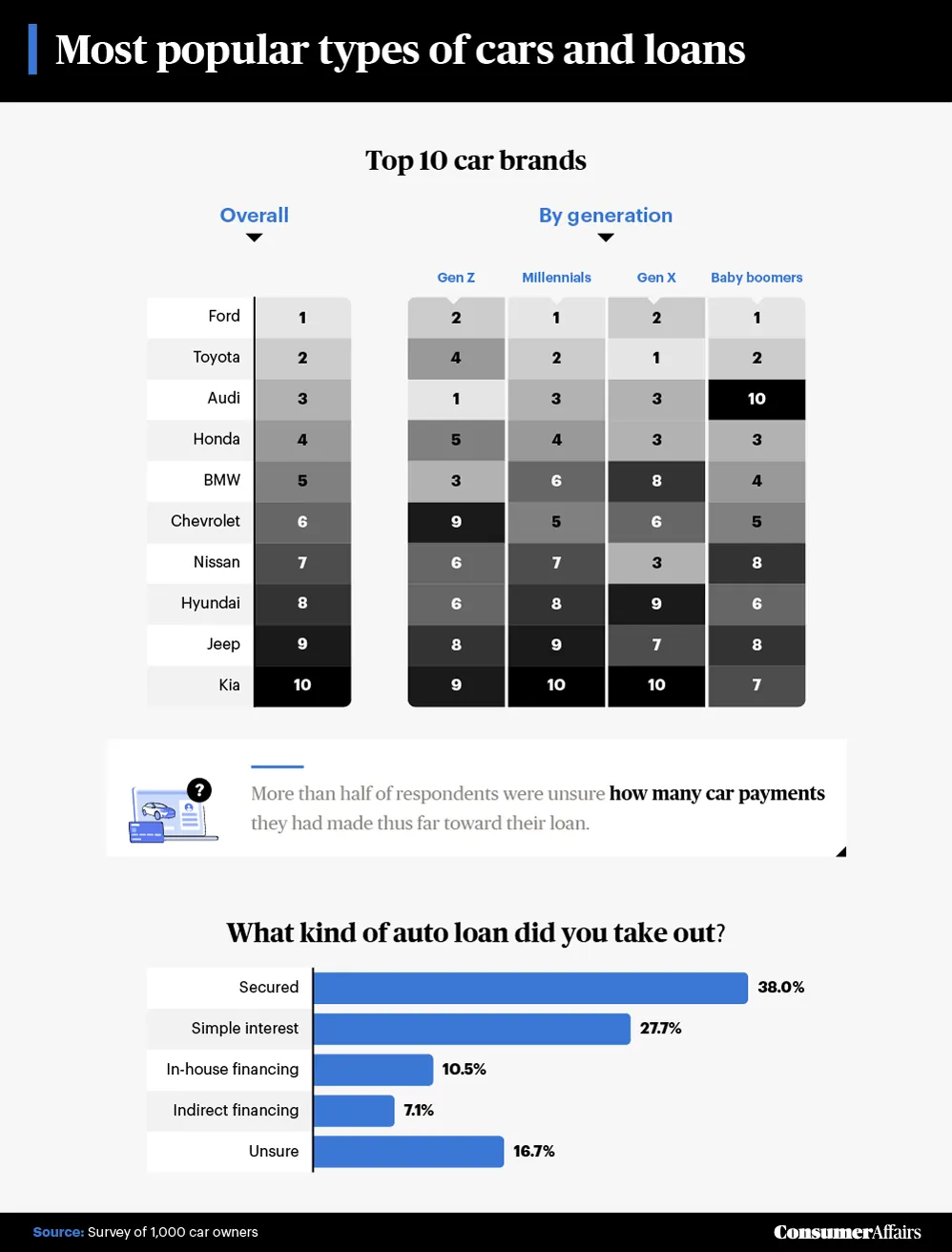

Thirty-eight percent of respondents in our survey reported their loan as secured, which means they could lose their vehicle if they’re unable to make payments on time. The next most common car loan was a simple interest loan, with 27.7% of participants paying monthly interest (which can amount to thousands of dollars over time). In-house financing and indirect financing came in last among American car owners, at 10.5% and 7.1%, respectively.

Overall, most American drivers stand to lose money on their loans if they miss payments or pay for their vehicle over a long period of time (accruing interest every month). This makes the question of when and how to refinance for better terms an important one to explore.

Reflecting on refinancing

Getting the best terms right off the bat might be ideal, but for many borrowers, securing better terms after the initial loan is more achievable. So, is it time to refinance your car?

There are a few different scenarios where refinancing makes sense — for instance, if your credit score has improved since the loan was initially signed.

This increase can be small. Bankrate found that customers with credit scores of 500 or lower paid 12.53% APR, on average, on a loan for a new car, while those with scores between 501 and 600 were charged just 9.41%.

The difference between a significantly lower interest rate is sometimes just a single point away. Credit scores from 601 and higher received better loan terms, with an average 6.07% APR, but great credit really pays off, with 2.47% APR rates for those with a score of 781 or higher.

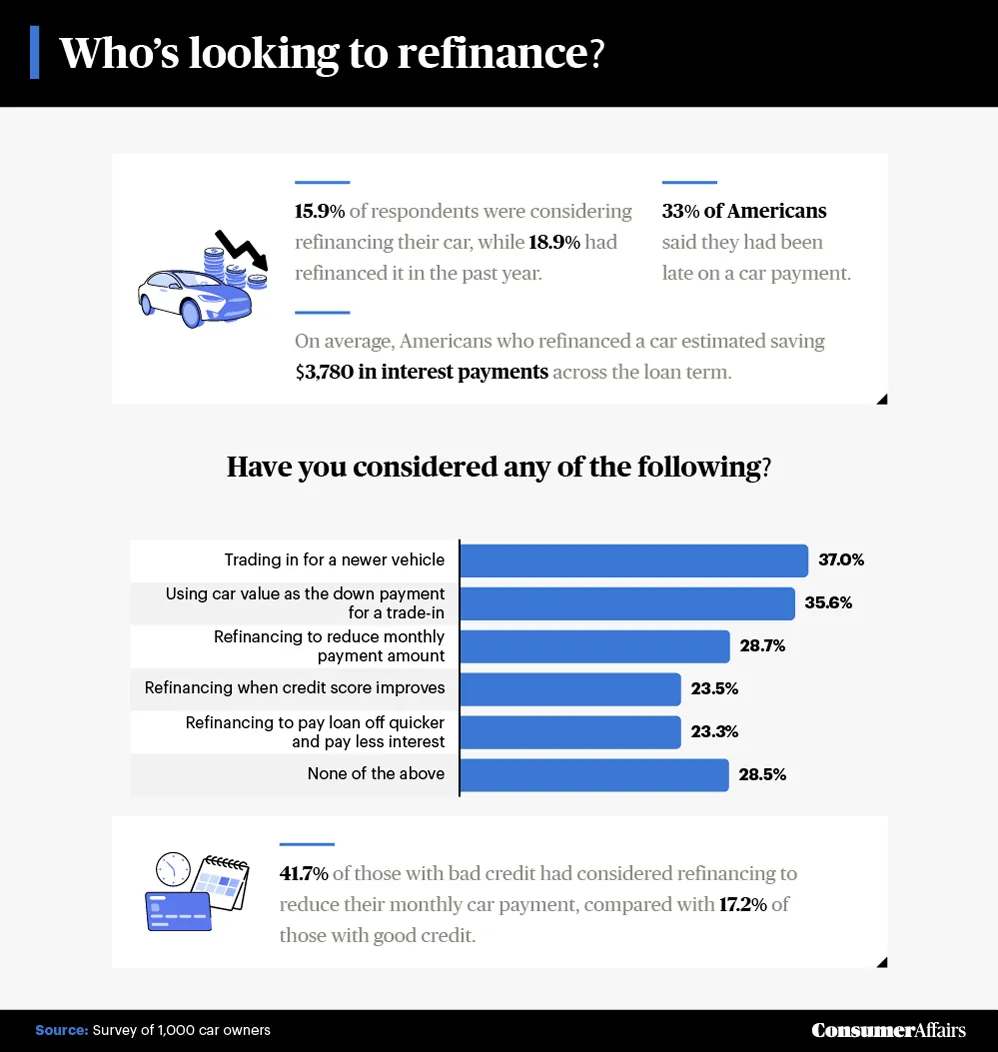

Taking advantage of interest rates that have dropped since a loan was signed, reducing loan repayment time and lowering monthly payments are other common reasons customers refinance. The latter was one of the most popular motives for refinancing among our respondents. Results showed, on average, refinancing saved car owners $3,780 in interest payments across their loan term, so it seems this strategy can be very effective.

In general, buyers with poor credit were more likely than those with good credit to consider refinancing specifically to lower monthly payments (at response rates of 41.7% and 17.2%, respectively).

For those with a secured car loan, missing a payment is a risky move. Unfortunately, 33% of our respondents admitted to having done so. Given that the majority of our respondents had this type of loan and that two or three missed car payments in a row could mean a vehicle gets repossessed, these numbers are a little concerning.

Cutting down costs

If refinancing isn’t an option, or if you’re a car owner and want additional ways to save on car-related expenses, there are a few tips to keep in mind.

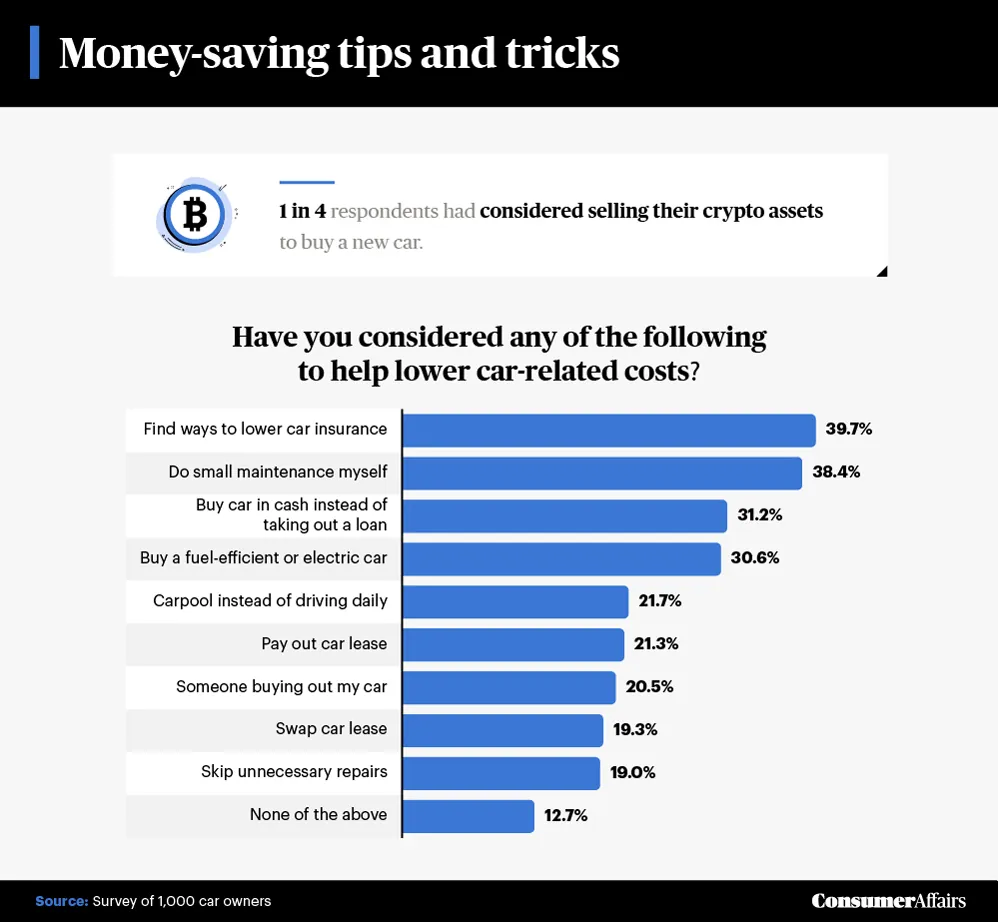

Annual maintenance can cost car owners from several hundred to a few thousand dollars, depending on how many miles driven. Car owners who make small repairs and maintain their vehicle themselves stand to save in the long run: More than 38% of Americans were considering taking a more active role and doing more on their own. This includes tasks like the following:

- Changing the oil

- Replacing the windshield wipers

- Changing the car battery (depending on owner knowledge)

The first two are simple tasks that take little time and can be done at home for cheaper than they would cost in a shop. The latter might be a bit too advanced for some owners, and it’s important to be honest about skill level and knowledge before attempting any maintenance or repairs. Doing something incorrectly can cost a lot more in repair fees than having it done by a professional in the first place. When in doubt, opt for experienced help.

Carpooling is another great way to save. The average price of gas is increasing rapidly, with customers paying a nationwide average of $4.29 per gallon in March 2022. (In 2021, the average was just $2.89.) Many car owners are finding it difficult to cover monthly gas expenses given the dramatic increase in price, and riding with other people (with co-workers or via a ride-share app) can cut down on the amount owners spend on gas per month.

Taking the wheel

Owning a vehicle is often the only way to ensure reliable transportation to and from work, but purchasing and maintaining a car is an increasingly costly endeavor. With skyrocketing gas prices and a rise in both used and new car prices, it’s important for buyers to understand their options when it comes to favorable loan terms and lower monthly expenses through refinancing.

Methodology and limitations

For this analysis, we asked 1,000 car owners in America to complete a survey. The data collected required respondents to accurately respond to an attention-check question in order to ensure they were participating properly in the survey. Self-reporting issues, such as telescoping, selective memory and exaggeration, are always a concern, however, and should be considered a research limitation.

Fair use statement

Would you like to spread the word about reducing car expenses? Sharing our data is free — all we ask is that you do so for noncommercial purposes and that you link back to this article to provide proper attribution.