Credit repair statistics 2026

+1 more

The information found in a consumer’s credit report can have a considerable impact on their housing security, professional prospects and financial trajectory. This makes accurate credit reporting critically important.

While consumers may attempt to independently rectify credit report errors, it can be a bureaucratic and time-consuming process. Interest in outsourcing this process has created a sub-industry within the financial services sector, known as “credit repair.”

There are nearly 44,000 businesses operating in the U.S. that help consumers with the credit repair process.

Jump to insightCredit repair companies’ clients are predominantly between the ages of 25 and 44.

Jump to insightAlthough the average consumer’s FICO score increased by 14 points from 2018 to 2023, revenue in the credit repair industry nonetheless grew by nearly 3% during that same period.

Jump to insightThe CFPB received around 2,600 complaints about credit repair companies in 2022, which works out to about one complaint for every 18 U.S. credit repair companies estimated to have been in operation that year.

Jump to insightCredit report errors

Credit report errors appear to be relatively common and this aligns with statements from the Consumer Financial Protection Bureau (CFPB), which receives more complaints from consumers about credit reporting than complaints about any other type of financial product or service.

The prevalence of credit report errors is alarming because derogatory errors can negatively impact a consumer’s credit score. Credit score simulations from FICO, the most widely used credit score provider, indicate that a credit payment reported as overdue by 90 days or more can reduce a credit score by up to 133 points and lower a consumer’s FICO rating from “Very Good” to “Fair,” a drop of two levels. For the average consumer interested in taking out a 30-year fixed-rate mortgage as of March 29, 2024, a credit score drop of that magnitude will increase their loan’s annual percentage rate by 0.613 percentage points. This would then increase their monthly payment on a $400,000 mortgage by $163 and the lifetime payment by $58,680.

What is credit repair?

Credit repair is the removal of inaccurate, derogatory marks from a consumer’s credit report.

The credit repair process entails reviewing credit reports issued by each of the three main credit bureaus, identifying any false information they contain and disputing that information with the reports’ issuing bureaus and the creditors involved. Consumers can complete these actions independently, or they may choose to enlist the services of a credit repair company, which will typically charge a flat fee of around $400 or monthly fees ranging from $60 to $150 for its services. Credit bureaus are required to investigate legitimate disputes and report on the results of their investigations to the initiating consumers.

The goal of the credit repair process is to improve a consumer’s credit score, which in turn can improve their chances of being approved for credit products and receiving favorable credit terms. A strong credit score may also increase your odds of being approved for a property rental, reduce your car insurance premiums and improve your employment prospects.

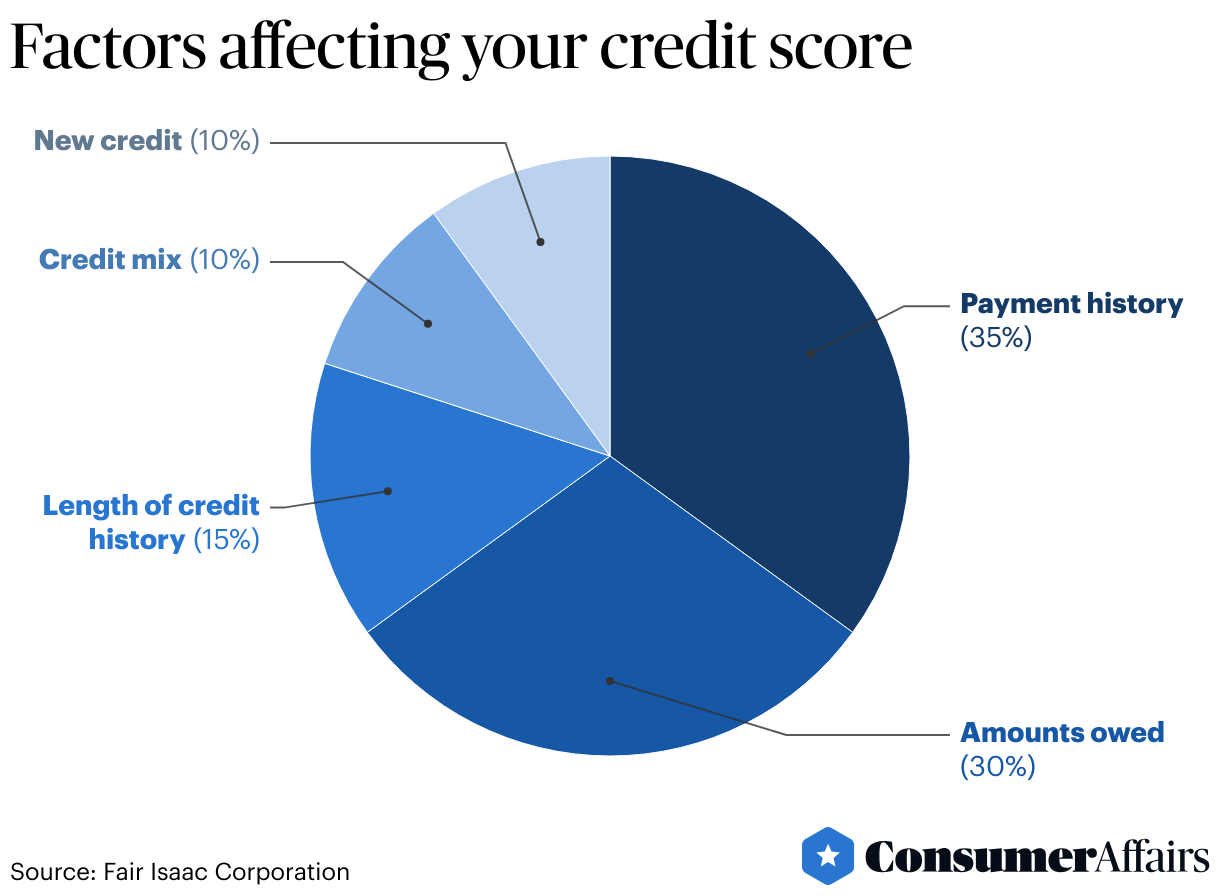

How is my credit score calculated?

FICO evaluates the information contained in credit reports and uses that information to determine a consumer’s credit score. The different elements of a credit background affect a credit score with varying levels of impact as per the percentages listed below:

Credit repair can potentially influence each of those factors in a positive manner. For instance, if a credit card is discovered to have been fraudulently opened in your name, removing that card from your credit reports can reduce the time elapsed since you’ve opened a new credit account and may positively impact your score’s new credit component. If the fraudulent card had high credit utilization and missed payments, removing the card from your reports will positively impact the amounts owed and payment history components of your credit score.

If your oldest credit account isn’t listed in your credit reports, correcting that error through credit repair can also positively affect your credit score. Ensuring that the account shows up on your reports will increase the age of your oldest account, which will improve your length of credit history. If that account was the only revolving or installment account you’ve ever had, its appearance on your credit reports will positively affect your credit mix.

Credit repair demographics

While reliable information about the credit repair industry is limited, data from two different sources may give us an idea of which consumers are most likely to patronize credit repair companies.

White Shark Media, a digital marketing agency, reports that an estimated 40% of those who pay for credit repair services are between the ages of 35 and 44, and about 25% are between the ages of 25 and 34.

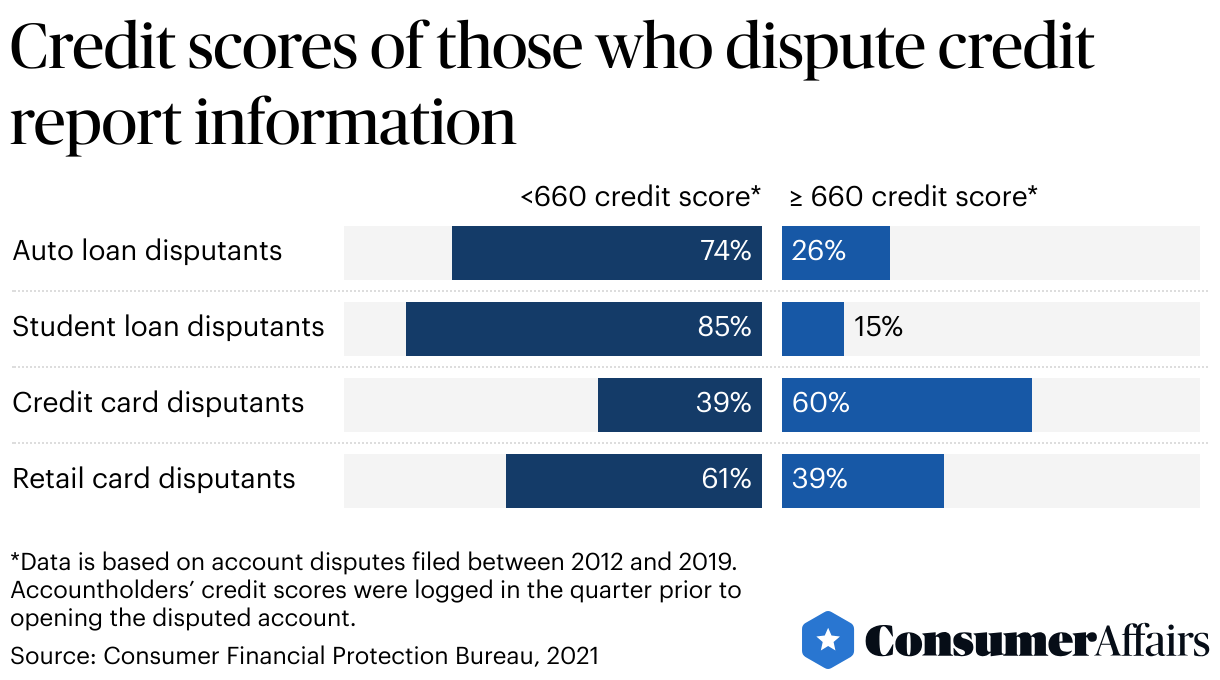

Meanwhile, data from the CFPB indicates that a majority of consumers who dispute information related to three different types of popular credit products — auto loans, student loans and retail cards — have credit scores below 660.

An interpretation of both of these sources may indicate that the typical credit repair client is a millennial with a below-average credit score. That said, it’s important to note that low credit scores are correlated with low incomes, and consumers with low credit scores may not have the financial means to pay for credit repair services.

Credit repair market size

The value of the U.S. credit repair industry reached $6.6 billion in 2023. According to IBISWorld, a business research firm, there were 43,810 credit repair businesses operating in the U.S. that year. The number of U.S. businesses in the credit repair industry dropped by 4.8% from 2022, which was in line with the average annual decrease since 2018.

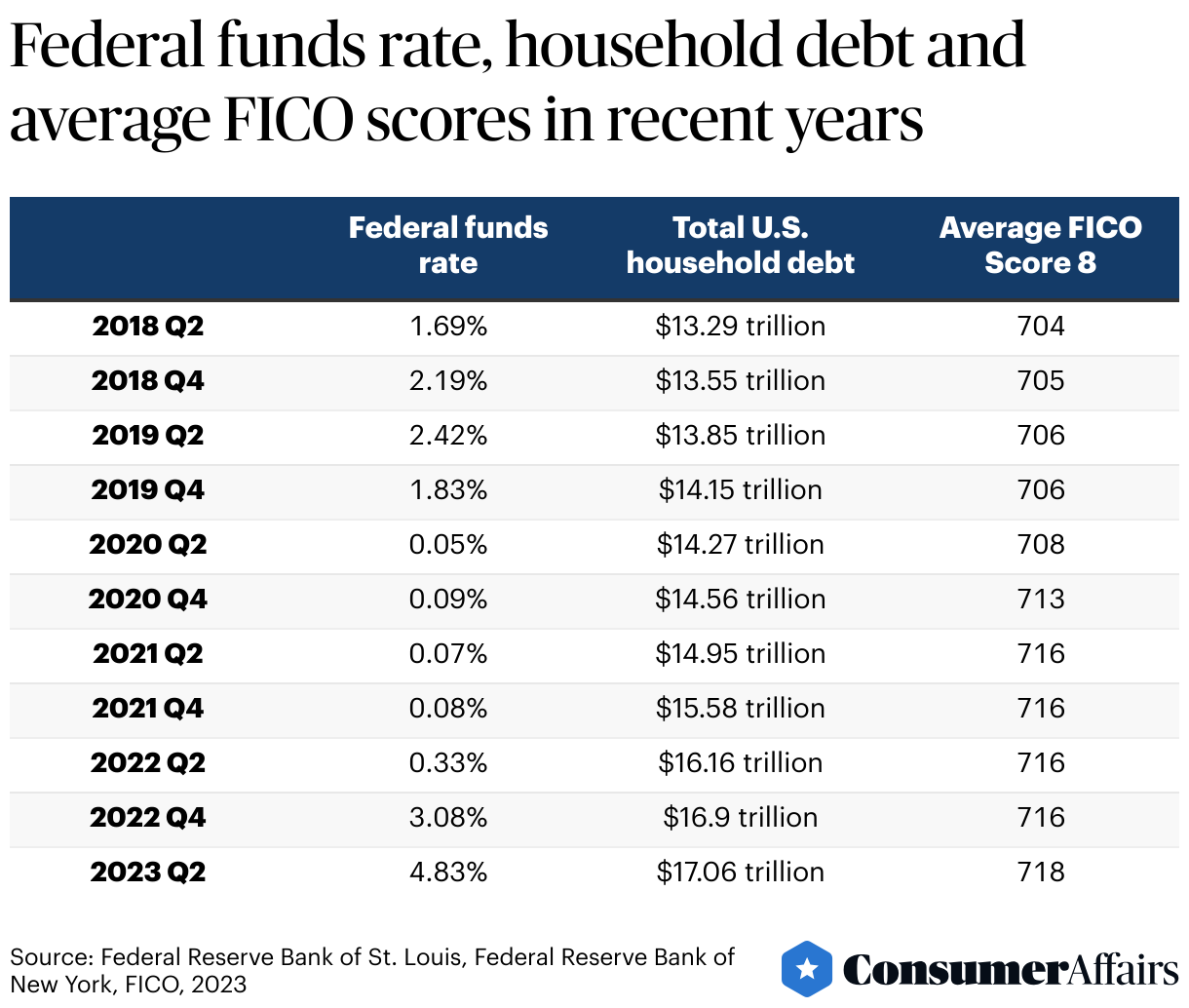

Revenue in the credit repair industry, however, reportedly grew during that period by 2.8%, which IBISWorld partly attributes to interest rate increases in recent years. The firm hypothesizes that an atmosphere of rising interest rates makes it harder for debtors to make their payments, which can hurt their credit scores and increase demand for credit repair.

But although both interest rates and household debt have indeed increased in recent years, this does not seem to have negatively affected the average consumer’s creditworthiness the way IBISWorld theorizes.

In this environment of improving credit scores, those who have subprime credit scores may feel additional pressure to boost their credit profiles in order to compete with fellow credit applicants. This pressure may have motivated more consumers to patronize credit repair companies, thus increasing the credit repair industry’s revenue in recent years.

FAQ

How do credit repair companies remove negative items?

Credit repair companies themselves cannot remove negative items from a credit report. They can, however, dispute inaccurate information listed on a credit report. If the credit bureau responsible for the report investigates the contested information and determines that it is indeed inaccurate, it will remove or revise the information.

Is credit repair the same thing as credit counseling?

No, credit repair is not the same thing as credit counseling. Whereas credit repair companies attempt to get negative and inaccurate items removed from their clients’ credit reports, credit counseling organizations provide debtors with a broader range of services, including budgeting, bankruptcy counseling and the creation of a debt management plan.

Credit repair and credit counseling differ in other ways as well. One of the most notable differences is that credit repair companies are for-profit enterprises, whereas credit counseling services are typically offered by nonprofit organizations.

Is credit repair legit?

Credit repair companies can help consumers improve their credit scores by disputing inaccurate information listed on credit reports for an affordable fee. Legitimate credit repair companies will clearly communicate their workflow, timeline and fee structure to potential clients in a written contract and will not request payment in advance of providing credit repair services. However, there are illegitimate actors within the credit repair industry.

The Consumer Financial Protection Bureau received an estimated 2,600 complaints about credit repair companies in 2022, which made up approximately 0.2% of the total complaints it received about U.S. financial products and services. About 82% of these complaints were determined to be actionable. Those who filed complaints against credit repair companies most commonly complained of fraud and scams.

You can avoid credit repair fraud by familiarizing yourself with the rules that govern the credit repair industry. It’s a good idea to only work with reputable credit repair companies that offer free initial consultations and have strong reviews from past clients published on consumer advocacy sites like ConsumerAffairs.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Consumer Financial Protection Bureau, “Consumer Response Annual Report.” Accessed Mar. 29, 2024.

- Federal Trade Commission, “Credit Scores.” Accessed Mar. 27, 2024.

- FICO, “How Credit Actions Impact FICO Scores.” Accessed Mar. 30, 2024.

- FICO, “What is a FICO Score?” Accessed Mar. 30, 2024.

- FICO, “Home Purchase Center.” Accessed Mar. 30, 2024.

- IBISWorld, “Credit Repair Services in the US - Market Size, Industry Analysis, Trends and Forecasts (2024-2029).” Accessed Mar. 29, 2024.

- White Shark Media, “Credit Repair: Who Is Your Audience?” Accessed Mar. 29, 2024.

- FICO, “Average U.S. FICO Score at 718.” Accessed Mar. 29, 2024.

- IBISWorld, “Credit Repair Services in the US - Number of Businesses.” Accessed Mar. 29, 2024.

- Consumer Financial Protection Bureau, “How do I dispute an error on my credit report?” Accessed Mar. 30, 2024.

- Capital One, “What credit score do you need to rent an apartment?” Accessed Mar. 29, 2024.

- Allstate, “Does your credit score affect your car insurance rate?” Accessed Mar. 29, 2024.

- FICO, “What's in my FICO Scores?” Accessed Mar. 29, 2024.

- FICO, “What is New Credit?” Accessed Mar. 29, 2024.

- FICO, “What is the Length of Your Credit History?” Accessed Mar. 29, 2024.

- FICO, “What Does Credit Mix Mean?” Accessed Mar. 29, 2024.

- Consumer Financial Protection Bureau, “Disputes on Consumer Credit Reports.” Accessed Mar. 30, 2024

- Britannica, “Millennial: demographic group.” Accessed Mar. 30, 2024.

- Urban Institute, “Busting credit myths can help low-income Americans strengthen their financial health.” Accessed Mar. 30, 2024.

- IBISWorld, “IBISWorld’s Story.” Accessed Mar. 29, 2024.

- Consumer Financial Protection Bureau, “List of consumer reporting companies.” Accessed Mar. 30, 2024.

- Federal Reserve Bank of St. Louis, “Federal Funds Effective Rate (FEDFUNDS).” Accessed Mar. 29, 2024.

- Federal Reserve Bank of New York, “Household Debt and Credit Report (Q4 2023).” Accessed Mar. 29, 2024.

- Office of the Law Revision Counsel of the U.S. House of Representatives, “15 USC CHAPTER 41, SUBCHAPTER II-A: CREDIT REPAIR ORGANIZATIONS.” Accessed Mar. 30, 2024.

Figures