Average American debt statistics 2026

+1 more

Overall household debt levels continue to hit record highs in the U.S. The largest sources of that debt are mortgages, vehicle loans, student loans and credit cards. Total amounts of debt, as well as debt to income and debt to asset ratios, vary significantly among different demographic groups.

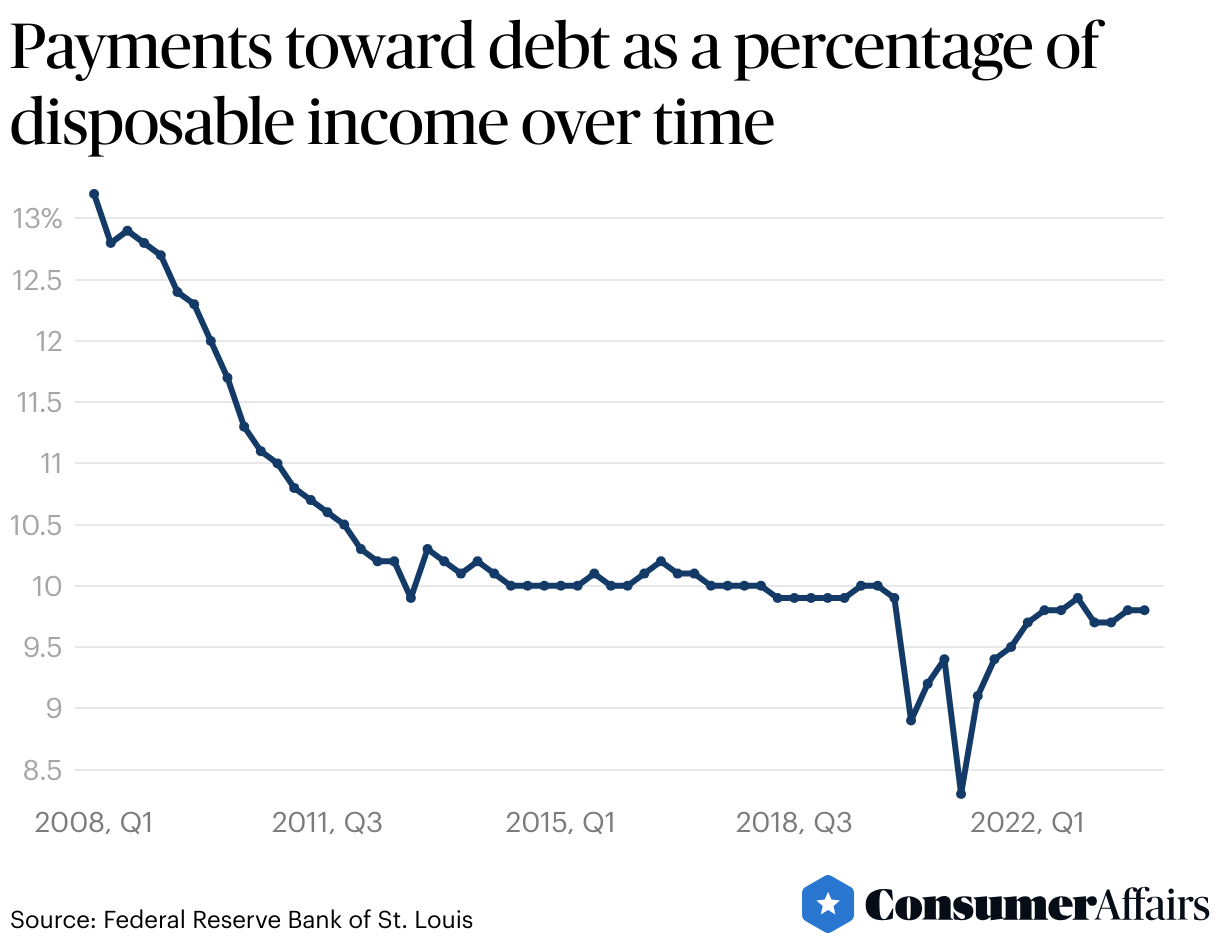

Total household debt in the U.S. reached $17.5 trillion at the end of 2023. However, debt payments as a percentage of personal income stood at only 9.8%, lower than historical averages.

Jump to insightDebt burden varies significantly by demographic group. People ages 40 to 49 years old carry the largest amount of debt. Black and Hispanic households have higher debt-to-asset ratios than other races.

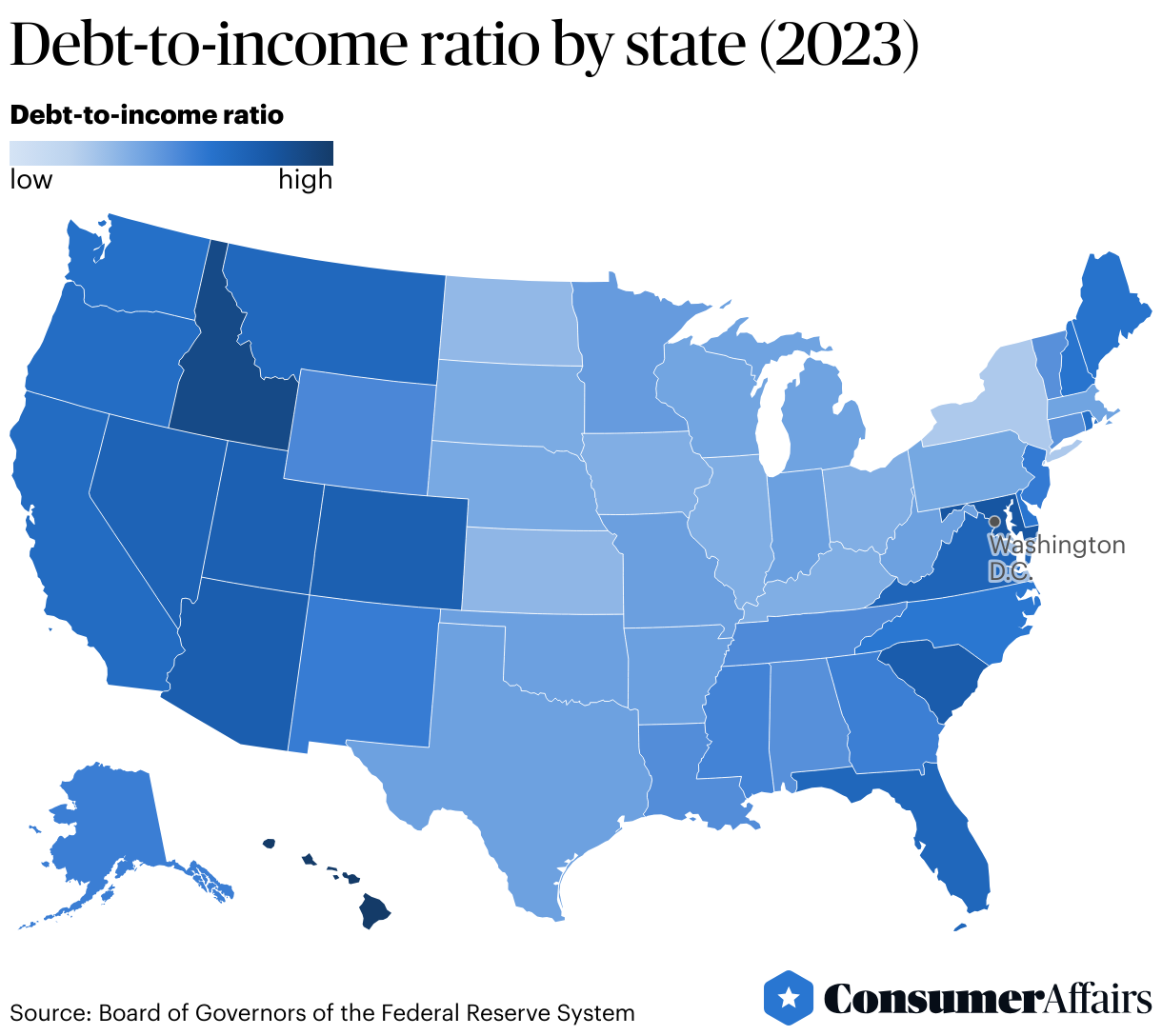

Jump to insightAmong U.S. states, residents of Hawaii and Idaho have the highest debt-to-income ratios. New York and Washington, D.C., have the lowest.

Jump to insightThe per-citizen share of the U.S. national debt has climbed over $102,000 as of April 2024. While not related, this number tracks closely to the average total consumer debt balance of $104,215.2

Jump to insightGeneral American debt statistics

Household debt in the U.S. continues to hit new heights, reaching $17.5 trillion in the fourth quarter of 2023. That number includes mortgage balances of $12.25 trillion, auto loan balances of $1.61 trillion and credit card balances of $1.13 trillion.

Despite this growth in total debt, however, debt payments as a percentage of personal income have been on an overall downward trend since a peak in 2007. Debt payments fell precipitously in early 2021, likely due to COVID-19 pandemic payment pauses. The percentage has increased slightly since then but is still lower than at any other time in the past 40 years.

U.S. debt demographics

Debt balances can vary significantly by age, race and other demographic characteristics. For example, the consumer organization Debt.org estimates that consumers with children have 14% to 51% more total debt than the national average. They also report that the lowest earners pay significantly more of their income toward debt than those in higher income brackets.

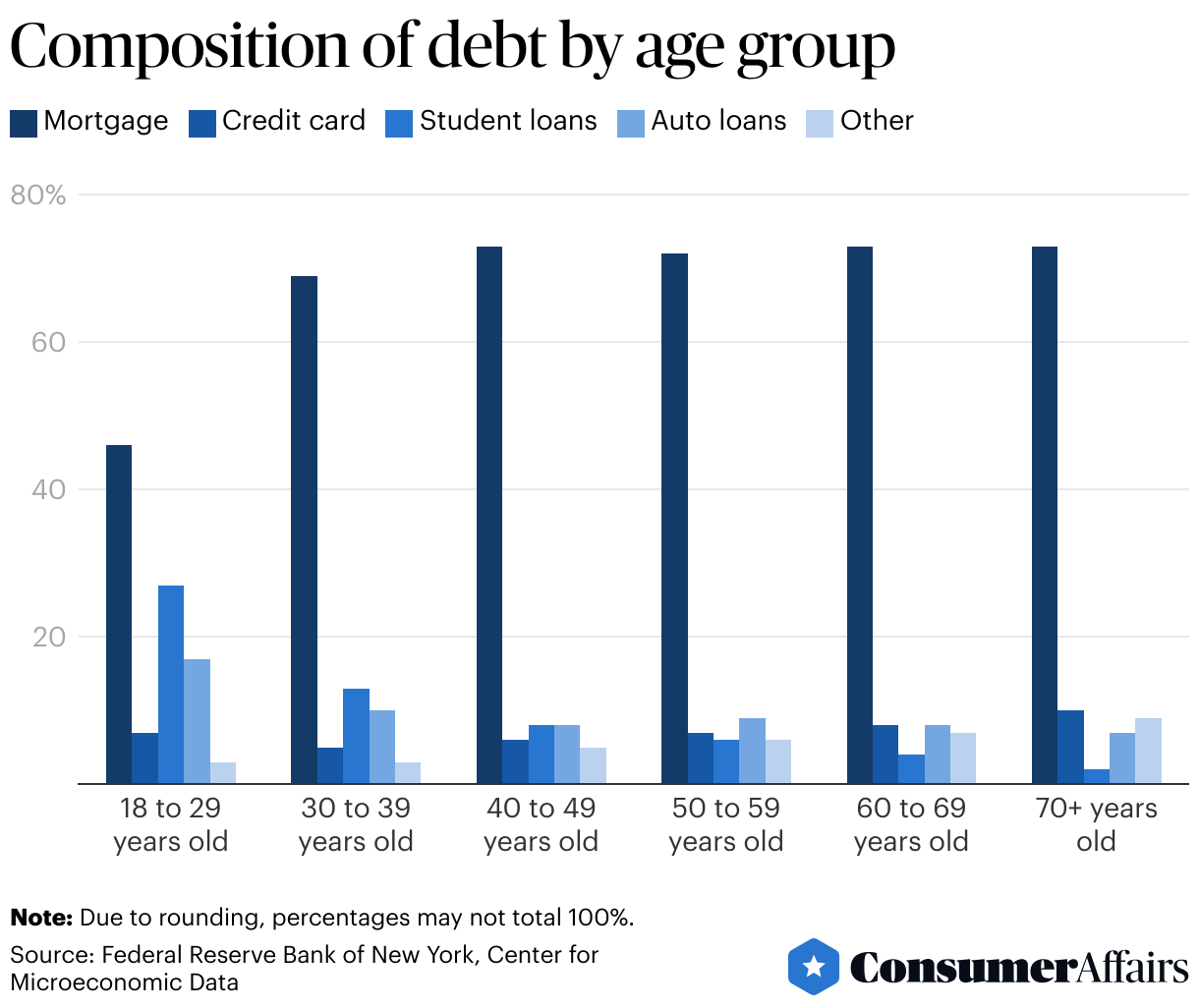

Debt balances by age show that those ages 40 to 49 years old are carrying the highest total amount of debt of any age group.

Total debt balance* by age group (in trillions USD)

| Age group | Total debt balance |

|---|---|

| 18 to 29 years old | $1.27 |

| 30 to 39 years old | $3.94 |

| 40 to 49 years old | $4.49 |

| 50 to 59 years old | $3.80 |

| 60 to 69 years old | $2.53 |

| 50 to 59 years old | $1.47 |

While mortgage loans make up the largest single source of debt among all age groups, it is a smaller share of overall debt for those under the age of 40. Conversely, student loans make up a larger proportion of overall debt for that age group than the older cohort.

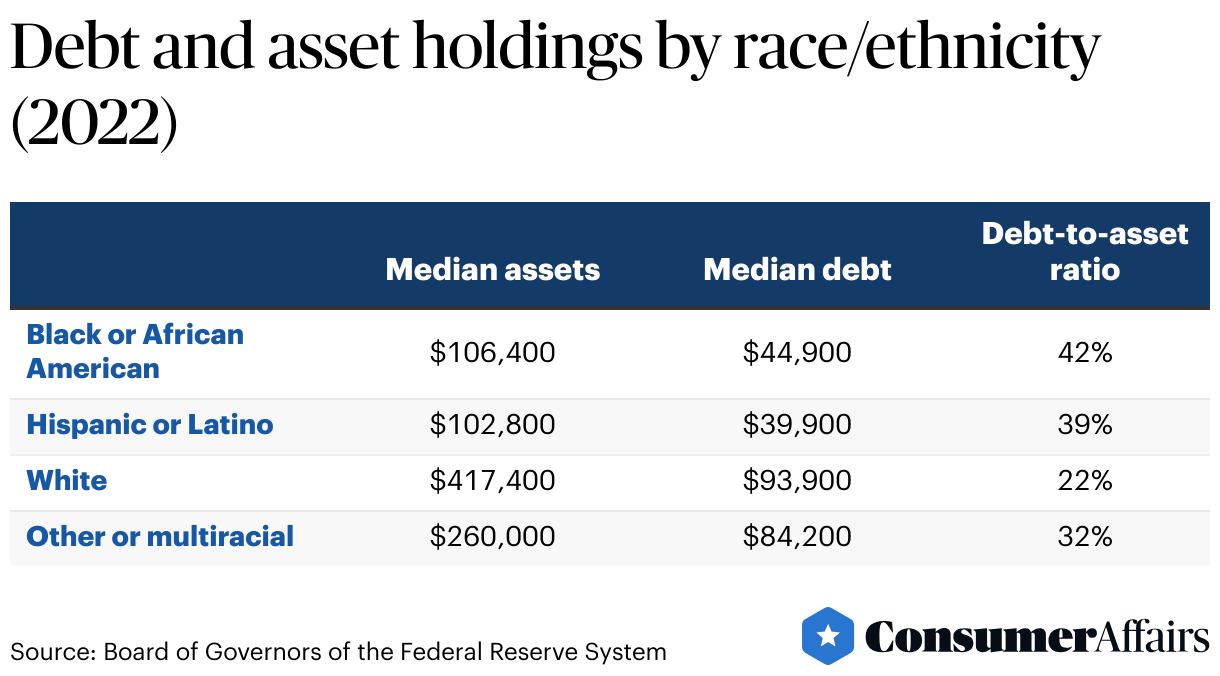

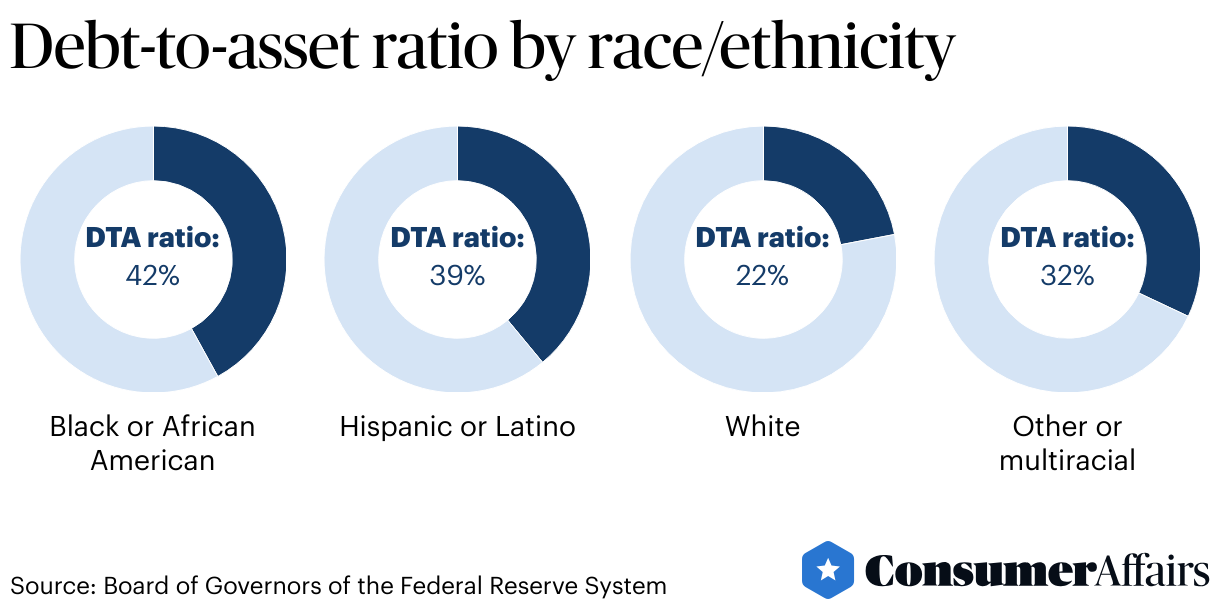

Calculating the total amount of debt doesn’t always paint the full financial picture. According to data from the Federal Reserve, the median debt for households identifying as white is higher than that of other races.

However, the median white household also owns significantly more assets, giving them a healthier debt-to-asset ratio.

Average debt of Americans

Another way to consider the amount of debt in the U.S. is through calculations based on the overall U.S. national debt. As of April 2024, the U.S. national debt was above $34.6 trillion. Given the total population of the U.S., that means the average citizen’s share of the national debt is more than $100,000.

While this number has no relation to actual household debt, it does track with statistics about average consumer debt. The consumer credit agency Experian reports that, according to its internal data, the average total debt balance among Americans is $104,215. Interestingly, this data shows that all types of consumer debt (mortgage debt, credit card debt, etc.) are growing, with the exception of student loan debt, which has fallen slightly over the past two years. This is likely due to the debt forgiveness initiatives enacted following the COVID-19 pandemic.

Average debt vs. income in the U.S.

According to the U.S. Census Bureau, the median household income in the U.S. was $74,580 in 2022. In the same year, the Survey of Consumer Finances found that median household debt was $80,200. While these numbers come from different surveys, they would put the median yearly debt-to-income ratio in the U.S. at 1.07, or 107%.

- While there is no single standard of what a healthy DTI should be, the Federal Deposit Insurance Corporation (FDIC) says that mortgage lenders typically require applicants to have DTIs no higher than between 33% and 36%.

- The Federal Housing Authority generally requires qualifying loanees to maintain a DTI of 43% or less (although lenders can use discretion if prospective borrowers have “compensating factors,” such as significant cash reserves).

Debt to income (DTI) ratios measure an individual or household’s income level as compared to the amount of debt they hold. This can be measured based on monthly income by taking your monthly gross income and comparing it to your monthly debt payments. For example, if you had a monthly gross income of $10,000 and monthly debt payments of $3,000, your DTI would be 30%.

Debt-to-income ratios can also be calculated by comparing total household debt to yearly household income. If your annual income was $100,000 and you had $150,000 in total debt, your yearly debt-to-income ratio would be 1.5, or 150%.

Debt to income by state

The Federal Reserve produces state-level data that compares yearly debt to income rates in each state. According to 2023 data, the only areas with debt-to-income ratios below 1.0 were New York (.989) and Washington, D.C. (.563).6 The only states with debt-to-income ratios above 2.0 were Hawaii (2.332), Idaho (2.149) and Maryland (2.002).

How can I get out of debt?

Getting out of debt isn’t always a simple process, but it can be accomplished with a disciplined approach. Here are some tips:

- Set a budget: You can’t set aside funds to pay off debt until you understand how much money you have coming in compared to how much money you’re spending. Setting a budget can help you separate necessary costs like housing and food from less necessary costs, like meals at nice restaurants or morning lattes from the coffee shop.

- Trim costs: Take a look at costs you incur every month. Evaluate which ones are most important to you. Decide whether you might be able to do without that extra streaming service. Find a home workout routine you like, so you can exercise without the gym membership.

- Pay bills on time: This one is pretty straightforward. Paying late fees is the equivalent of throwing your money away. If your bills are late because you’re consistently waiting for your paycheck to clear, negotiate to change the due dates. Many providers will work with you.

- Find new ways to earn: Bringing in more money every month will increase the pace at which you can pay off debts. Side hustles are extremely popular and common. Find one that’s right for you and start earning a little extra.

- Pay down your credit cards first: You may have multiple loans or sources of debt. Aim to pay off the ones with the highest interest rates first. Average credit card rates are higher than they’ve ever been, so that’s often a good place to start.

FAQ

How much debt is the average American in?

According to data from the consumer reporting agency Experian, average debt among Americans reached $104,215 in 2023.

What percentage of Americans are debt free?

The 2022 Survey of Consumer Finances showed that 77.4% of households held some debt. This includes 45.2% with credit card balances and 46.6% with mortgage or HELOC debt. The survey also found that 21.8% of households had education loan debt.

What is the No. 1 debt for American households?

Mortgage debt is the largest single debt for households in the U.S. As of the fourth quarter of 2023, housing debt represented 72% of overall household debt.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- US Debt Clock, “Debt Per Citizen.” Accessed Apr. 10, 2024.

- Experian, “Experian Study: Average U.S. Consumer Debt and Statistics.” Accessed Apr. 10, 2024.

- Federal Reserve Bank of New York, Center for Microeconomic Data, “Quarterly Report on Household Debt and Credit - 2023: Q4.” Accessed Apr. 10, 2024.

- Federal Reserve Bank of New York, Center for Microeconomic Data, “Quarterly Report on Household Debt and Credit - 2023: Q4 (detailed tables, #20 & 21).” Accessed Apr. 10, 2024.

- Housing and Urban Development Department, “Borrower Qualifying Ratios.” Accessed Apr. 10, 2024.

- Board of Governors of the Federal Reserve System, “State Level Debt to Income Ratio, 1999-2023.” Accessed Apr. 10, 2024.

- Federal Deposit Insurance Corporation, “Loans and Mortgages: How Much Mortgage Can I Afford?” Accessed Apr. 10, 2024.

- Housing and Urban Development Department, “HUD 4155.1, Mortgage Credit Analysis for Mortgage Insurance.” Accessed Apr. 10, 2024.

- U.S. Census Bureau, “Income in the United States: 2022.” Accessed Apr. 10, 2024.

- Board of Governors of the Federal Reserve System, “Changes in U.S. Family Finances from 2019 to 2022.” Accessed Apr. 10, 2024.

- Board of Governors of the Federal Reserve System, “Survey of Consumer Finances 2022 - historic tables.” Accessed Apr. 10, 2024.

- Consumer Protection Financial Protection Bureau, “Credit card interest rate margins at all-time high.” Accessed Apr. 10, 2024.

- Debt.org, “Demographics of Debt.” Accessed Apr. 10, 2024.

- Federal Reserve Bank of St. Louis, “Household Debt Service Payments as a Percent of Disposable Personal Income.” Accessed Apr. 10, 2024.

Figures