Real estate trends 2026

+1 more

In the U.S., home prices surged at an unprecedented rate following the COVID-19 pandemic due to a combination of record-low interest rates, a significant number of millennials entering their prime homebuying years and a limited supply of available housing. The ongoing shortage of inventory, coupled with persistent demand, is expected to keep home prices at historically high levels. This situation underscores the increasing challenges of affordability that potential homebuyers are facing.

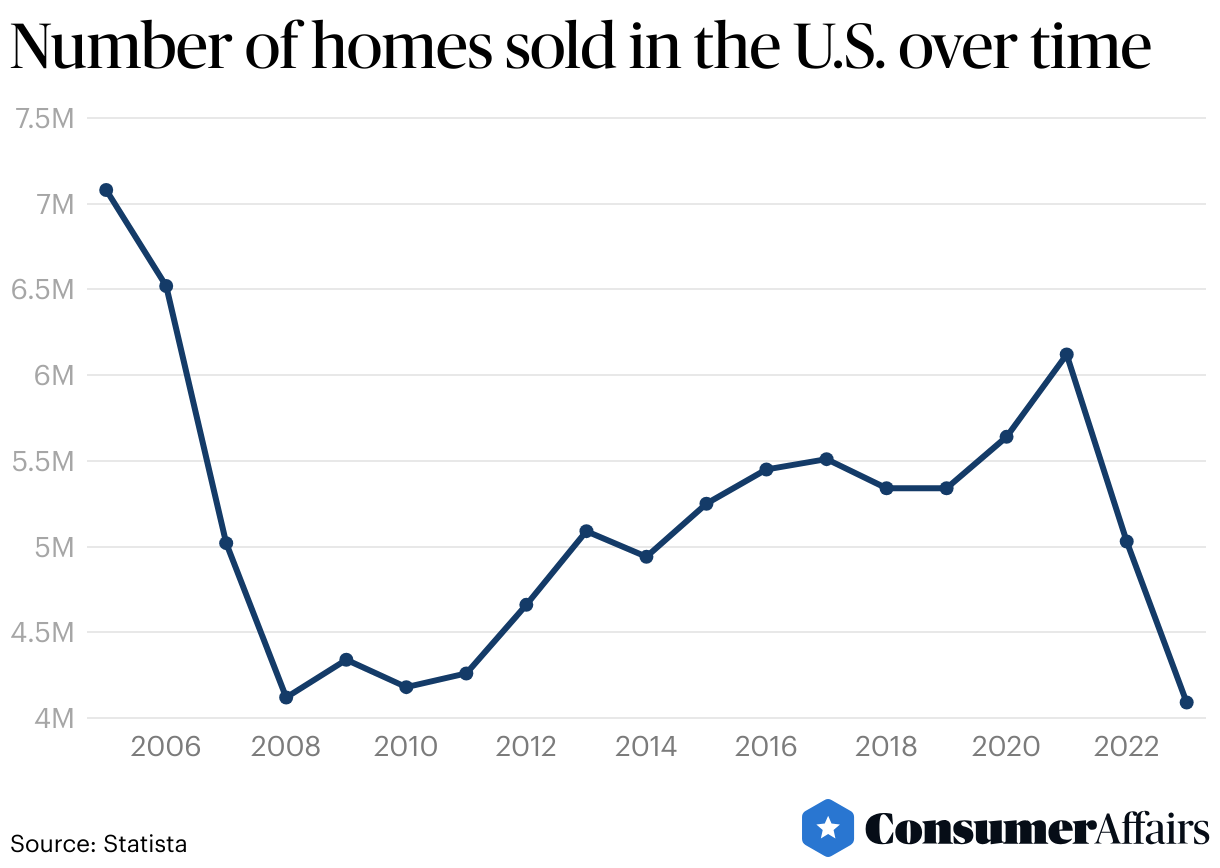

Over the past 18 years, the number of U.S. home sales plummeted to its lowest point in 2023, registering just 4.09 million transactions.

Jump to insightLimited housing inventory continues to drive up the prices of new homes. In March 2024, the median sales price reached $430,700, a 6.2% jump from 2023.

Jump to insightAffordability issues in the U.S. have worsened across all market types. In 2023, the ratio of home value to household income was almost 4 to 1 in rural counties. By contrast, home values in the densest urban counties reached six times the household incomes.

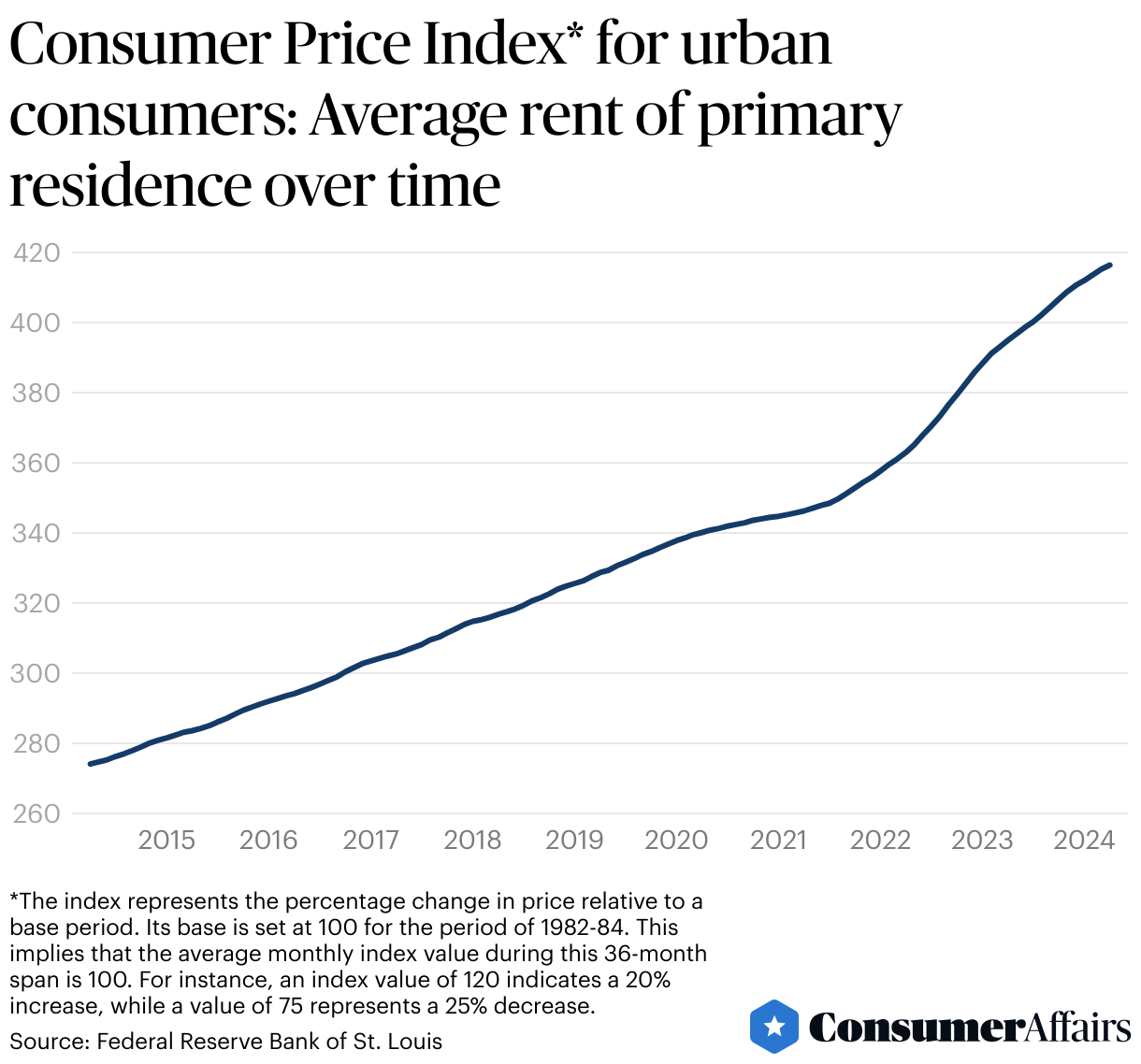

Jump to insightRental prices in the U.S. have surged to unprecedented levels, leading to a situation where half of all renters are now spending at least 30% of their income to rent, with a quarter allocating at least 50% of their income to paying rent.

Jump to insightBy the end of 2024, the U.S. real estate market is forecast to reach a valuation of $119.80 trillion dominated by residential properties, comprising 79% of the market volume.

Jump to insightReal estate trends

A recent study from the Joint Center for Housing Studies of Harvard University, based on data from March 2020 to March 2023, highlights the following findings regarding U.S. home prices and affordability:

- During the study period, home prices increased across various market types, but the sharpest rise, more than 33%, occurred in rural counties, smaller metro areas and less dense suburbs of major metro areas.

- On average, prices in denser urban counties rose by 21%. This shift marked a significant reversal from the previous decade when urban and denser areas typically saw the fastest price increases.

- In rural counties, the ratio of home value-to-income climbed from 2.5 to 1 in 2017 to 3.9 to 1 in 2023. This indicates that typical home values were nearly four times the median household income, making it increasingly difficult for many existing households to afford homes.

- Affordability issues have worsened across all market types. Home values in the densest urban counties reached six times the median household incomes in 2023.

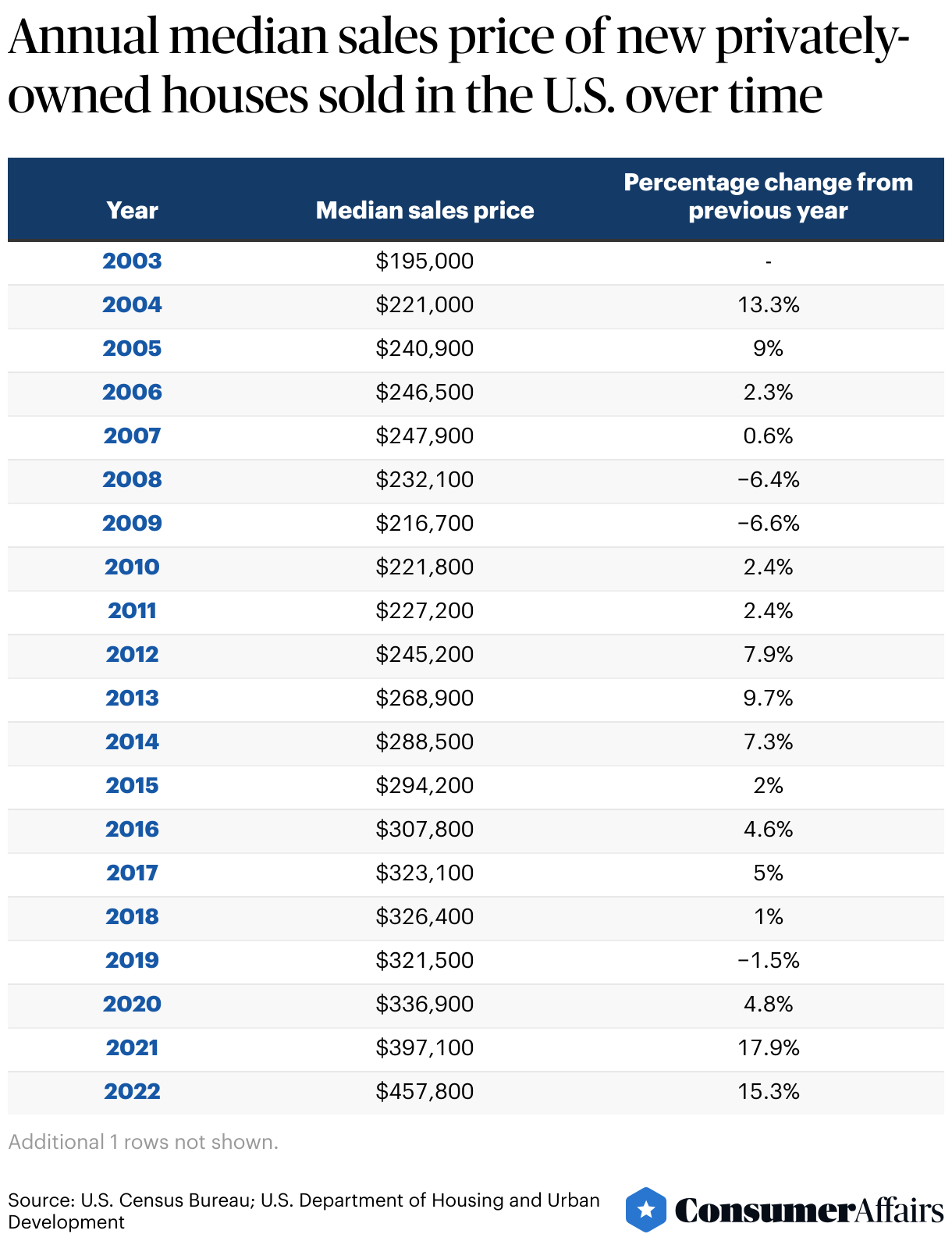

Housing cost averages by year

Although today's housing market has slowed compared to the pandemic-driven homebuying boom, home prices are still rising due to a persistent shortage of available properties. Despite the small decline in the median sales prices of new homes from $457,800 in 2022 to $428,600 in 2023, the median sales price rose to $430,700 in March 2024. This marked a 6% increase from the median sales price reported in February 2024, suggesting that the trend toward higher prices continues.

This is further emphasized by the S&P/Case-Shiller U.S. National Home Price Index, which tracks changes in the prices of single-family homes across the U.S. and provides a clear picture of the overall value of domestic housing. Based on the most recent data, the S&P/Case-Shiller U.S. National Home Price Index showed a 6.4% year-over-year increase rising from 528,235.2 in February 2023 to 561,922.2 in February 2024. The February 2024 index also showed a 6% increase over January 2024.

Houses sold yearly since 2005

According to National Association of Realtors data from 2005 to 2023, U.S. home sales reached their peak in 2005, with 7.08 million transactions. They fell to their lowest in 2023, with 4.09 million sales recorded. This data covers transactions of existing homes, which include single-family homes, condos and co-ops.

The housing market experienced a boom during the COVID-19 pandemic, reaching 6.12 million transactions in 2021. However, home sales began to decline in the latter half of 2022. Several factors contributed to this shift, most notably the dramatic increase in house prices. A survey highlighted high home prices and adverse economic conditions as the primary barriers to home purchases. In particular, 2022 saw an unprecedented surge in mortgage rates, further increasing the overall cost of homeownership.

Looking ahead, projections suggest that 4.62 million homes will be sold in 2024, with an increase to 5.35 million in 2025.

Should I buy or rent with the current trends?

Deciding whether to rent or buy a home is a significant financial and lifestyle choice that requires weighing the advantages and disadvantages of each option, based on your current circumstances and future goals. Buying a home provides equity, stability and independence from landlords, along with the freedom to make alterations. However, homeownership also entails greater responsibilities, including taxes and maintenance challenges.

For many, particularly in the early stages of adulthood, renting may be a more viable option. Renting eliminates the responsibility for maintenance and provides greater flexibility to relocate as needed. On the downside, renters do not benefit from tax deductions, do not build equity and face potential challenges like rent increases and the possibility of eviction.

Moreover, as seen in the table below, average rent prices in urban areas have shown a consistent upward trend over the last decade. The Consumer Price Index (CPI), which tracks monthly price changes paid by U.S. consumers (including housing rents), supports this observation. Across the U.S., rents have soared to record highs, with half of all renters now allocating at least 30% of their income to rent and a quarter spending 50% or more.

A significant factor contributing to this issue is a shortage of housing supply. There are several reasons for this shortage. One major factor is restrictive zoning regulations. Particularly in higher-cost areas, zoning laws make it difficult to build affordable, smaller homes or densely packed apartments. At the same time, millennials are increasingly looking to form households and secure their own living spaces, further driving up demand.

Real estate predictions

By the end of 2024, the U.S. real estate market is projected to reach a valuation of $119.8 trillion. The residential properties segment is expected to lead, accounting for 79% of the market volume. This growth is largely fueled by an increasing demand for suburban homes, a trend driven by the widespread adoption of remote work. Furthermore, from 2024 to 2028, the market is set to grow at a compound annual growth rate (CAGR) of 4.51%, reaching a market size of $142.9 trillion by the end of the period.

In a global context, China’s real estate market is anticipated to surpass the U.S. in 2024, projected to be valued at $135.7 trillion.

FAQ

Will 2024 be a good time to buy a house?

Housing prices are expected to continue rising, indicating that now might be a good time to consider buying a home.

Is 2024 a good time to sell my house?

As home prices are expected to increase, it might be wise to postpone selling for the time being.

Is it better to buy a house when interest rates are high?

It depends on your circumstances and what you can afford. It’s worth considering purchasing a home now if you have the financial capacity to afford higher mortgage rates and are open to the possibility of refinancing later. This is especially true if you come across an affordable property, find your ideal home in a desirable location or if the alternative is indefinitely continuing to rent.

Why is the number of home sales declining in the U.S.?

There are several reasons for declining home sales, but the primary factors are high home prices and adverse economic conditions, including rising mortgage rates.

Is the U.S. housing market going up?

Yes, between 2024 and 2028, the housing market is expected to rise with a CAGR of 4.51%.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Joint Center for Housing Studies of Harvard University, “The Geography of Pandemic-Era Home Price Trends and the Implications for Affordability.” Accessed May 15, 2024.

- Joint Center for Housing Studies of Harvard University, “Home Price-to-Income Ratio Reaches Record High.” Accessed May 15, 2024.

- Statista, “Number of existing homes sold in the United States from 2005 to 2023, with a forecast until 2025.” Accessed May 16, 2024.

- Redfin, “U.S. Home Prices Hit an All-Time High in April.” Accessed May 16, 2024.

- U.S. Census Bureau, “Historical Time Series.” Accessed May 16, 2024.

- The Pew Charitable Trusts, “How Housing Costs Drive Levels of Homelessness.” Accessed May 16, 2024.

- Statista, “Real Estate - United States.” Accessed May 17, 2024.

- IBISWorld, “House Price Index.” Accessed May 23, 2024.

- Federal Reserve Bank of St. Louis, “S&P CoreLogic Case-Shiller U.S. National Home Price Index.” Accessed May 17, 2024.

- MyCreditUnion.gov, “Buying vs. Renting a Home.” Accessed May 17, 2024.

- NPR, “It's not just home prices. Rents rise sharply across the U.S.” Accessed May 18, 2024.

- Moody’s Analytics, “United States - CPI: Urban Consumer - Rent of primary residence.” Accessed May 18, 2024.

- Federal Reserve Bank of St. Louis, “Consumer Price Index for All Urban Consumers: Rent of Primary Residence in U.S. City Average.” Accessed May 19, 2024.

- Moneywatch, CBS News, “4 times you should buy a home with interest rates high.” Accessed May 19, 2024.

Figures