Personal loan statistics 2026

+1 more

Loans offer financial support for purchases by providing funds that you may not readily have available, allowing you to repay the amount over a specified period. There are two main types of loans: secured and unsecured. Secured loans require your property as collateral; if you fail to repay, the lender can seize the collateral to recover the funds. Common examples include mortgages, home equity loans and installment loans. Unsecured loans, on the other hand, do not involve collateral. These are deemed riskier by lenders, who therefore charge higher interest rates. Credit cards and student loans are typical examples of unsecured loans.

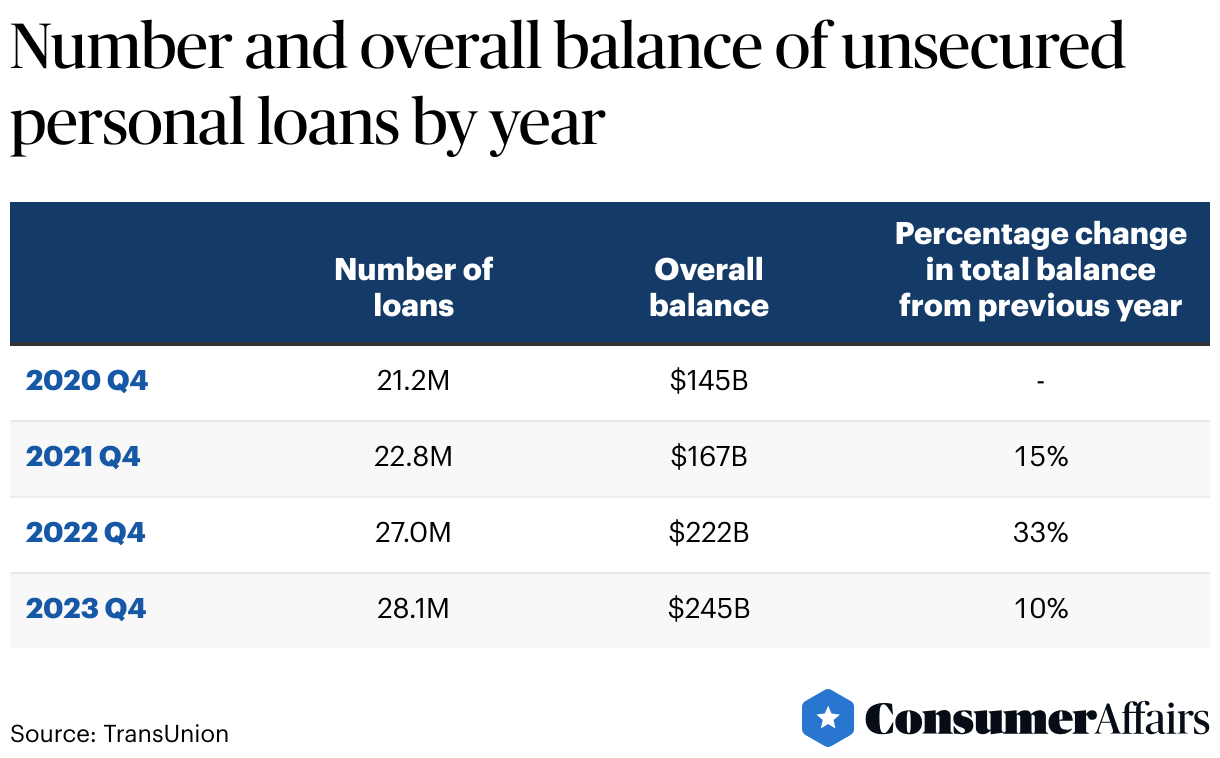

In the U.S., the total debt from unsecured personal loans reached $245 billion in the fourth quarter of 2023.

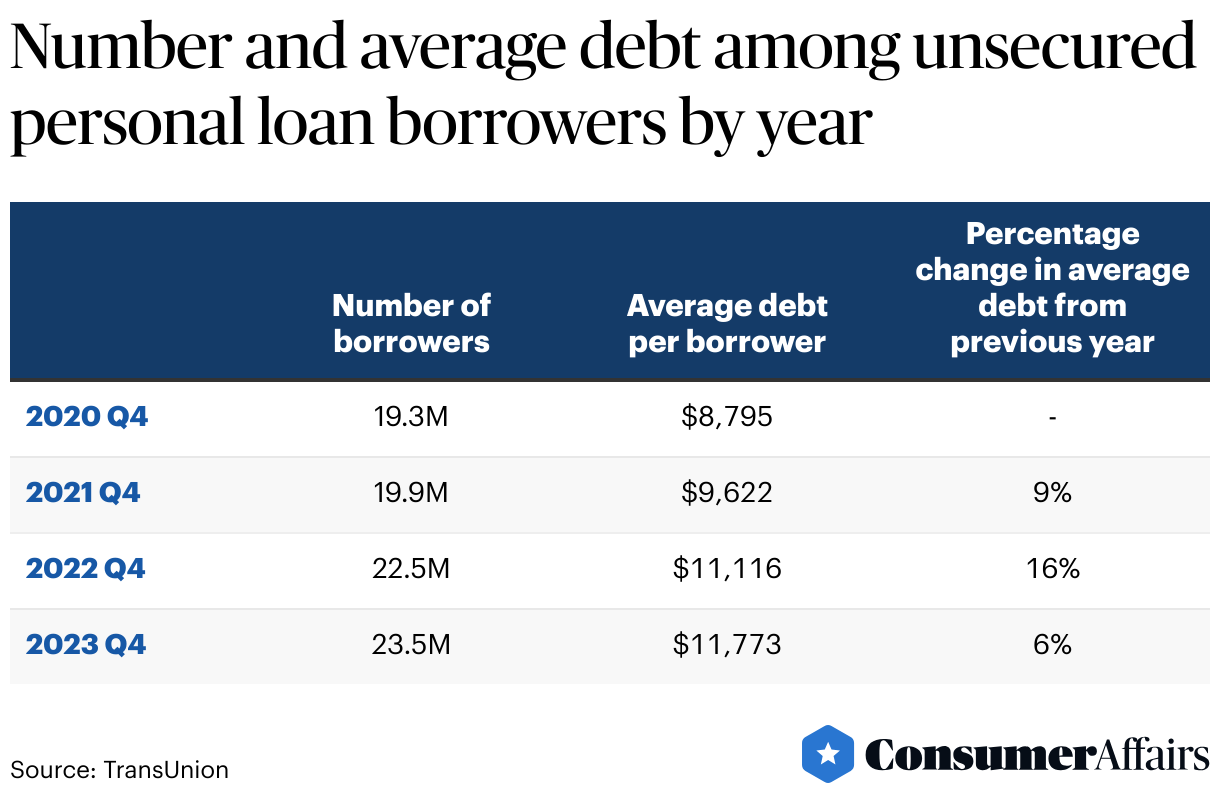

Jump to insightIn the last quarter of 2023, there were 23.5 million Americans with unsecured personal loans.

Jump to insightDuring this period, the average debt per borrower for unsecured personal loans was $11,773.

Jump to insightThe interest rate for personal loans varies significantly based on the borrower’s credit score, currently ranging from an average of 11.3% for scores of 720 or higher to 25.2% for scores below 630.

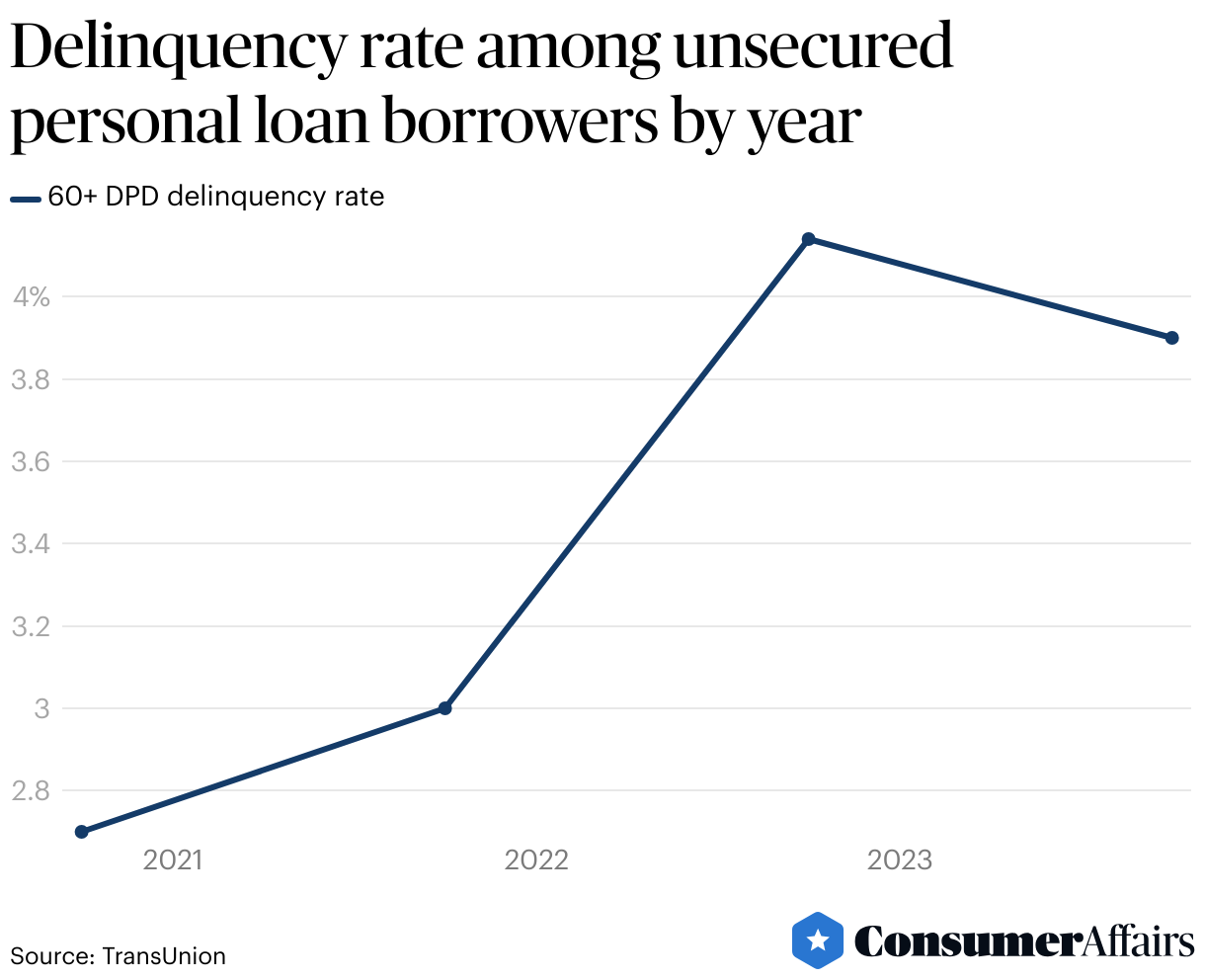

Jump to insightAt the end of 2023, the delinquency rate for unsecured personal loans, specifically among borrowers who were 60 or more days past due, was 3.9%.

Jump to insightHow many Americans have personal loans?

Data from the last quarter of 2023 shows that in the U.S., there were 23.5 million consumers with unsecured personal loans. The average debt per borrower reached $11,773, marking a 6% increase from the previous year.

What is the total debt from personal loans in the U.S.?

In the fourth quarter of 2023, the number of unsecured personal loans was approximately 28.1 million, with borrowers owing a total of $245 billion. This represented the 11th consecutive quarter of growth, reaching a record high in 2023. When compared to the same period in 2022, there was a 10% increase in the overall amount owed by borrowers.

What are the delinquency rates for personal loans?

The 60+ DPD (days past due) delinquency rate measures the percentage of borrowers who are at least 60 days behind on their payments. The 60+ DPD delinquency rate was 3.9% in the last quarter of 2023, down from the 4.1% delinquency reported during the same period in the previous year.

Expectations for 2024 forecast a gradual improvement in the unsecured personal loans market. That said, lenders and investors will closely monitor delinquency rates and continue to target consumers with lower risk profiles.

Personal loan interest rates

Interest rates are a crucial aspect of personal loans, as they directly affect the cost of borrowing money. The primary factor influencing interest rates is the borrower's credit score. Those with higher scores typically receive lower rates due to being perceived as more reliable by lenders. However, other elements also play a role in determining personal loan interest rates. These include the borrower’s income, debt-to-income ratio, level of education, whether collateral is involved, the loan's repayment terms, any negative marks on the credit report (such as missed payments or recent collections) and the type of lender.

Interest rates and loan costs

When considering a personal loan, it's important to be aware of potential fees and additional charges that could increase your overall cost of borrowing. These costs can be included in your loan, meaning you will pay interest not only on the principal amount but also on these added fees. Common charges associated with personal loans include the following:

- Application fee: This fee is charged by lenders at the time of the loan application to cover the initial processing of your loan request. Typically, application fees range from 1% to 8% of the loan amount.

- Origination fee: Paid upfront, this fee compensates the lender for processing the approved loan application. It varies based on the loan type and the associated costs of setting it up, generally amounting to 1% to 10% of the loan amount.

- Prepayment penalty: If you pay off your loan early, you may incur a prepayment penalty, typically ranging from 1% to 2% of the loan amount. This fee compensates the lender for the lost interest income that would have been earned if the loan had continued as originally scheduled.

- Late fee: If a payment is not made on time, a late fee may be charged based on the terms of the loan agreement. This fee usually ranges from $10 to $100 or a percentage of the monthly payment.

Understanding these fees can help you better manage the costs associated with a personal loan.

FAQ

What percentage of Americans have personal loans?

As reported in the last quarter of 2023, approximately 23.5 million Americans had unsecured personal loans, accounting for nearly 7% of the U.S. population.

What is the delinquency rate on personal loans?

Among borrowers, the delinquency rate stood at 3.9% in the fourth quarter of 2023 for unsecured personal loans that were at least 60 days past due (60+ DPD).

Is a 7% interest rate high for a personal loan?

Based on the current economic context, a 7% interest rate is not high for a personal loan. The interest rate for someone with an excellent credit score (720 to 850) is around 11.3%.

In terms of interest rates, how high is too high for a personal loan?

What is considered a high interest rate for a personal loan depends on your credit score. Ideally, you should aim for an interest rate that is below the average for your specific credit score category (as listed above). If you are offered a rate that is higher than this average, it is wise to compare offers from different lenders before making a decision.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- MyCreditUnion.gov, “Personal Loans: Secured vs. Unsecured.” Accessed May 23, 2024.

- TransUnion, “Bankcard Balances Surpass $1 Trillion as Millennials Increasingly Turn to Cards.” Accessed May 23, 2024.

- LendEDU, “Average Personal Loan Interest Rates.” Accessed May 24, 2024.

- LISC National, “Loan Terminology.” Accessed May 25, 2024.

- Cornell Law School Legal Information Institute, “Origination fee.” Accessed May 25, 2024.

- Cornell Law School Legal Information Institute, “Prepayment penalty.” Accessed May 25, 2024.

- Justia US Law, “2010 Maryland Code Commercial Law.” Accessed May 25, 2024.

- United States Census Bureau, “U.S. and World Population Clock.” Accessed May 25, 2024.

Figures