Mortgage delinquency rates 2026

+1 more

By definition, mortgage delinquency happens when a borrower fails to pay their mortgage loan on time. The Consumer Financial Protection Bureau considers mortgages that are 30-89 days delinquent as early stage delinquencies. Mortgages that are 90 or more days delinquent are referred to as serious delinquencies. It’s important to note that many mortgage delinquencies are eventually resolved — foreclosure rates are significantly lower than delinquency rates.

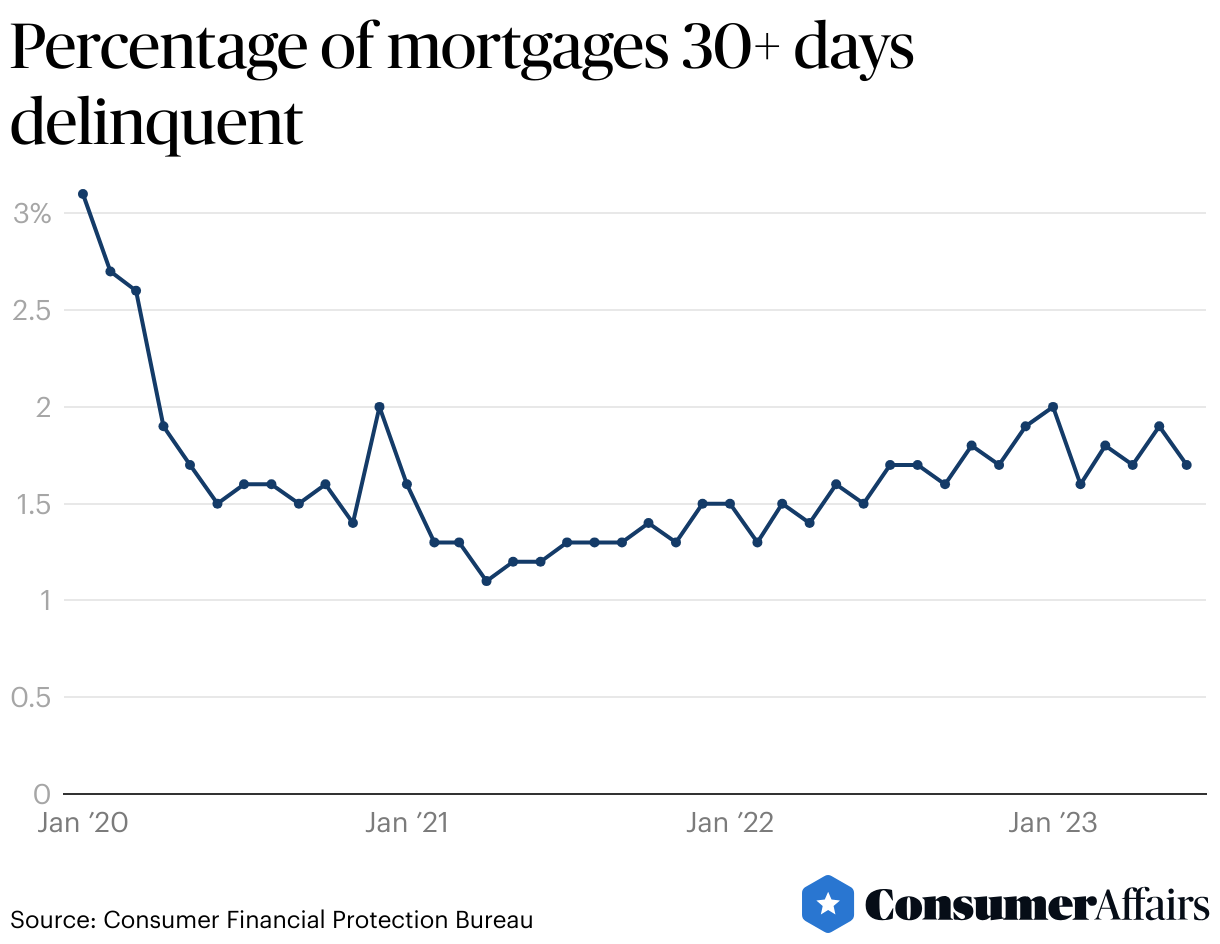

The nation’s overall delinquency rate for January 2024 was 2.8%, unchanged from January 2023.

Jump to insightThe historical average of the mortgage delinquency rate between 1979 and 2023 is 5.25%.

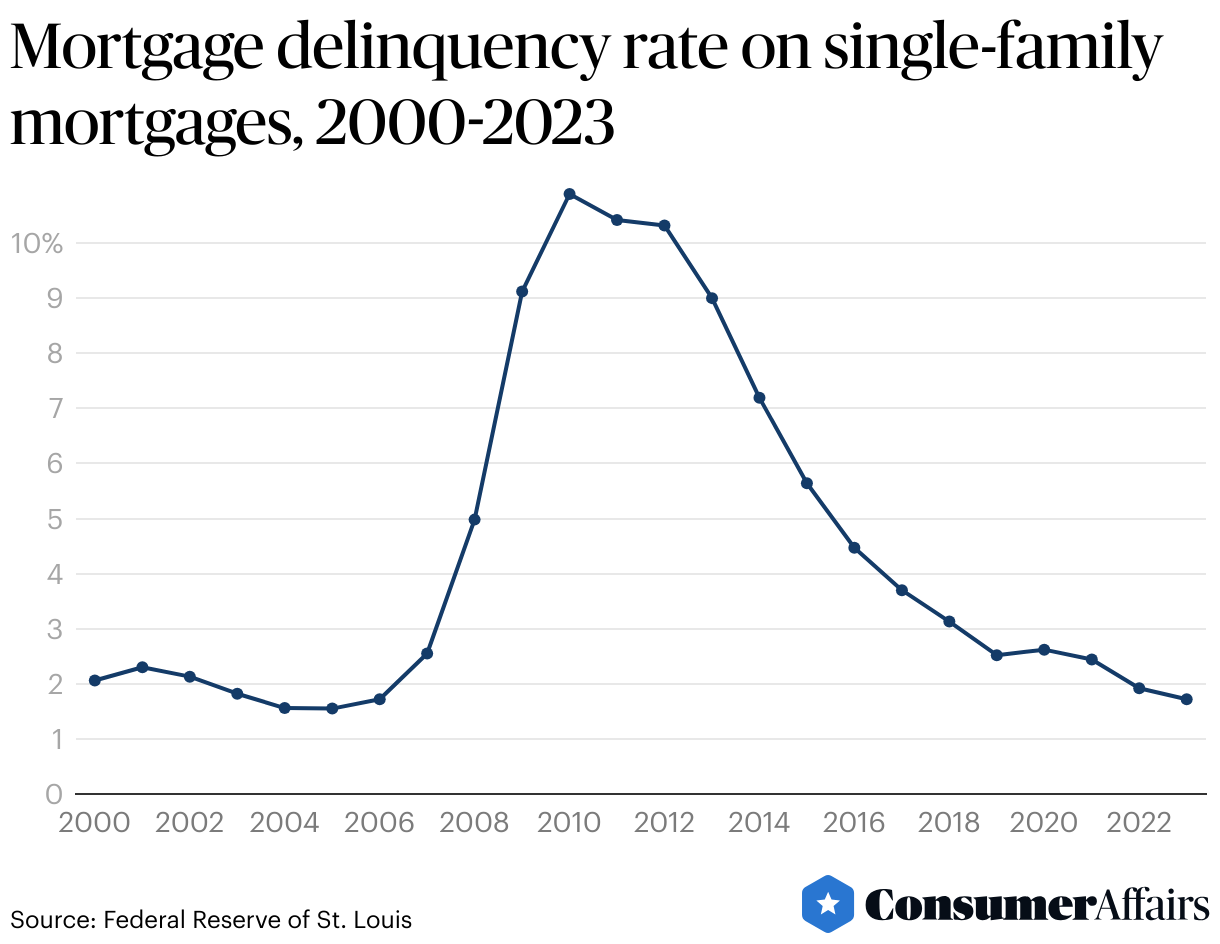

Jump to insightIn 2023, mortgage delinquency rates were near all-time lows. The delinquency rate on single-family mortgages was 1.72%.

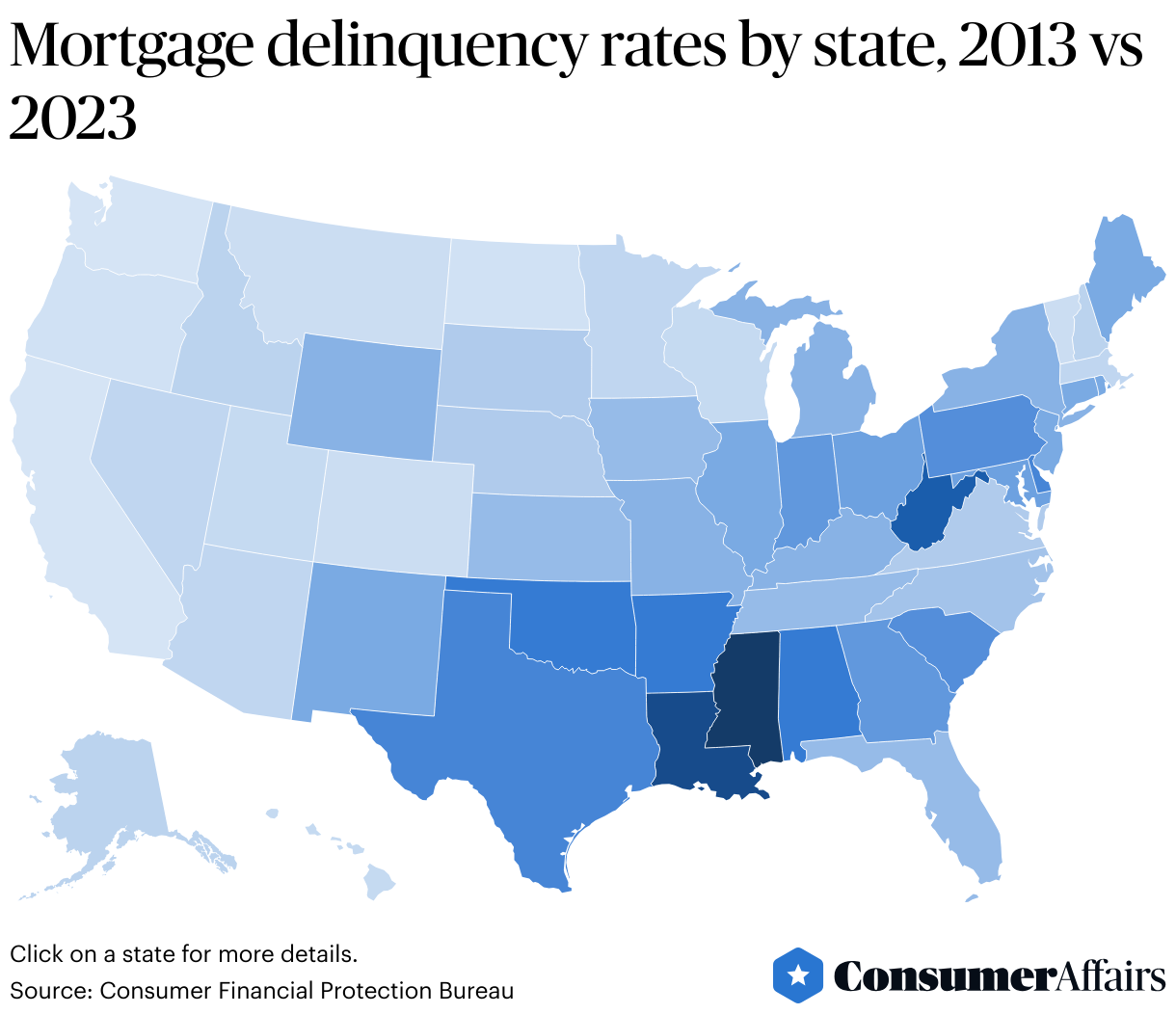

Jump to insightAs of June 2023, the mortgage delinquency rate was over 3% in only two states: Mississippi and Louisiana.

Jump to insightOver the past 10 years, mortgage delinquency rates decreased by about 7% in the state of Florida and about 5% in the state of New York.

Jump to insightGeneral mortgage delinquency rates statistics

The mortgage delinquency rate measures the percentage of home loans with payments that are overdue by 30 or more days. Between 1979 and 2023, the historical average for seasonally adjusted mortgage delinquency rates is 5.25%. As of January 2024, the nation’s overall delinquency rate was 2.8%.

These delinquency rates generally vary depending on the loan type. For example, the Mortgage Bankers Association reports that although delinquencies on all mortgage loans measured at 3.88% in the 4th quarter of 2023, there was significant variance between Federal Housing Administration (FHA) loans, Veterans Affairs (VA) loans, and Conventional loans.

Delinquency rates by loan type, 4th quarter 2023 (residential properties)

| Loan type | Delinquency rate |

|---|---|

| FHA loans | 10.81% |

| VA loans | 4.07% |

| Conventional loans | 2.61% |

According to the Census Bureau, 73% of new home sales were financed with conventional loans in 2023, compared to just 13% that used FHA loans and 5% that used VA loans.

Mortgage delinquency rate by year

According to data compiled by the Federal Reserve, delinquency rates have fallen significantly since the fallout from the subprime mortgage crisis. The annual mortgage delinquency rate for single-family homes peaked at 10.89% in 2010 but had fallen to 1.72% by 2023.

Loan delinquency by state

As of June 2023, the five states with the highest rates of mortgage delinquency were Mississippi, Louisiana, West Virginia, Arkansas and Alabama.

States with highest rates of mortgage delinquency, June 2023

| State | Delinquency rate |

|---|---|

| Mississippi | 3.5% |

| Louisiana | 3.2% |

| West Virginia | 2.9% |

| Arkansas | 2.4% |

| Alabama | 2.4% |

In contrast, California, North Dakota, Oregon and Washington all have mortgage delinquency rates at or below 1%.

The below chart shows how mortgage delinquency rates have changed in each state over the past 10 years.

The five states that experienced the biggest declines in mortgage delinquency rates over the last ten years include:

- Florida: -7.2%

- New Jersey: -6.1%

- Nevada: -5.9%

- District of Columbia: -5.5%

- Maryland: -5.4%

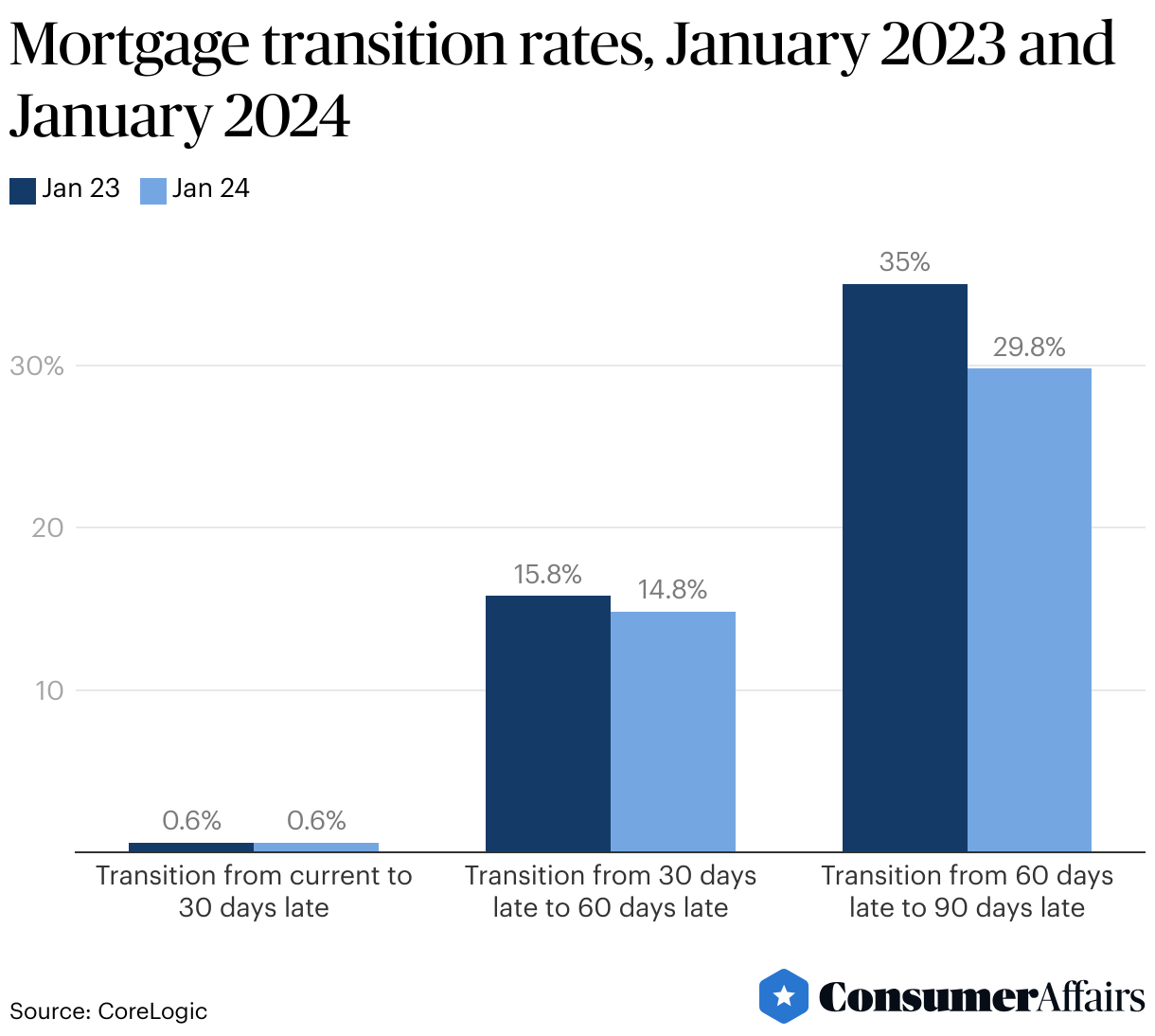

Transition Rates

Transition rates measure the number of mortgages moving from one category to another - whether that’s from current to 30 days past due, from 30 days to 60 days past due, or from 60 to 90 days past due. Transition rates get significantly higher once a borrower is already late on payments, indicating how difficult it can be to catch up on payments once behind.

Rates by month

Inflation rates fluctuated from 3.1% in January 2020 down to 1.1% in April 2021 before rising to 1.9% in June 2023, according to the monthly figures.

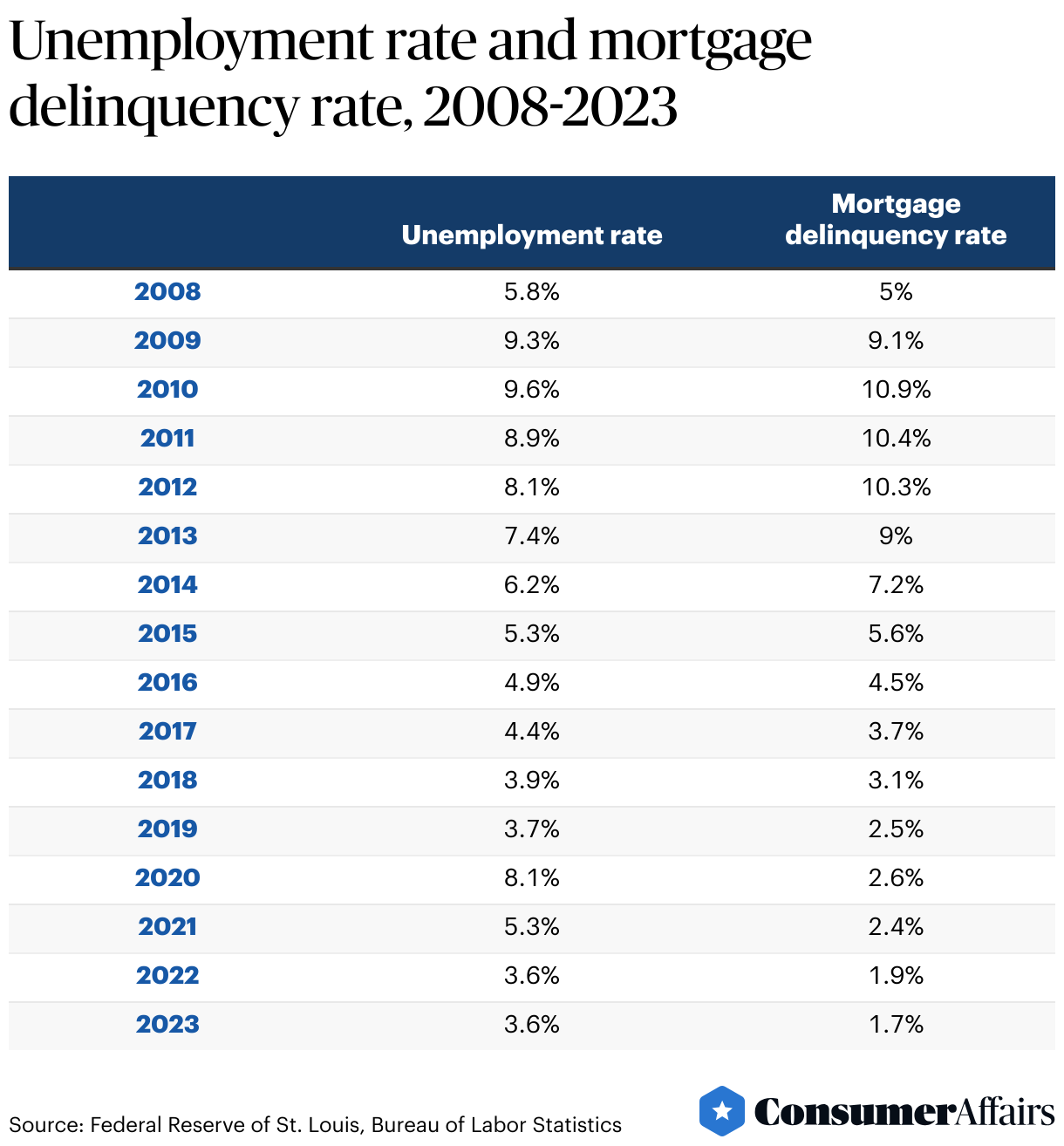

Mortgage delinquency rates compared to unemployment rates

Over time, mortgage delinquency rates have tended to track unemployment rates. In other words, when unemployment is higher, mortgage delinquencies tend to go up as well. A paper published by the Federal Reserve Bank of Philadelphia found that average mortgage default rates for the unemployed are 4% higher than default rates for those who are employed.

Mortgage delinquency demographics

Large-scale data about the racial and economic makeup of individuals with delinquent mortgages is not available. But a study of City University of New York students by the Federal Reserve Bank of New York found that Black and Hispanic students were more likely to be delinquent on their mortgage debt (despite being less likely to have mortgages in the first place). Among students with Associate’s Degrees, Black students were 6% more likely and Hispanic students 8% more likely to be delinquent on mortgage debt than their white counterparts. Among those with Bachelor’s Degrees, Black students were 9% more likely and Hispanic students 6% more likely to be delinquent on mortgage debt. Asian students were slightly less likely to be delinquent on their mortgages than white students.

FAQ

What is the mortgage delinquency rate?

The mortgage delinquency rate refers to the percentage of homeowners who are past due on their mortgage payments. According to the National Mortgage Database, the percentage of homeowners who were 30 or more days past due on their mortgage payments was 1.72%.

How much do Americans owe on their mortgages?

According to the credit reporting company Experian, average mortgage debt in the U.S. is $244,498.

Are mortgage delinquency rates increasing?

Depending on the data source, the mortgage delinquency rate was somewhere between 1.7% and 3.88% at the end of 2023. Either way, the current mortgage delinquency rate is well below the historical average of 5.25%.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Federal Reserve of St. Louis, “Delinquency Rate on Single-Family Residential Mortgages, Booked in Domestic Offices, All Commercial Banks.” Accessed Apr. 1, 2024.

- Mortgage Bankers Association, “Mortgage Delinquencies Increase in the Fourth Quarter of 2023.” Accessed Apr. 1, 2024.

- National Mortgage Database, “State Mortgages 30-89 Days Delinquent.” Accessed Apr. 1, 2024.

- National Mortgage Database, “State Mortgages 90 or more Days Delinquent.” Accessed Apr. 1, 2024.

- U.S. Census Bureau, “Quarterly Sales by Price and Financing.” Accessed Apr. 1, 2024.

- CoreLogic, “Loan Performance Insights - February 2024.” Accessed Apr. 1, 2024.

- Federal Reserve Bank of Philadelphia, “Individual and Local Effects of Unemployment on Mortgage Defaults.” Accessed Apr. 1, 2024.

- Bureau of Labor Statistics, “Employment status of the civilian noninstitutional population.” Accessed Apr. 1, 2024.

- Liberty Street Economics, “Unequal Distribution of Delinquencies by Gender, Race, and Education.” Accessed Apr. 1, 2024.

- Federal Reserve Bank of New York, “Quarterly Report on Household Debt and Credit.” Accessed Apr. 1, 2024.

- Board of Governors of the Federal Reserve, “Economic Well-Being of U.S. Households in 2022.” Accessed Apr. 1, 2024.

- Experian, “Average US Mortgage Debt Increases to $244,498 in 2023.” Accessed Apr. 1, 2024.

- CoreLogic, “Loan Performance Insights - March 2024.” Accessed Apr. 1, 2024.

Figures