Debt settlement statistics 2026

+1 more

Debt settlement, sometimes referred to as debt resolution, is a type of debt relief service that offers consumers a way to reduce the outstanding balance on their debt. The process involves negotiating with creditors — sometimes through a third-party debt settlement company — to reduce the overall amount of debt owed and then paying off the lower amount in a lump sum.

Though debt settlement can be used to avoid bankruptcy or wage garnishment, the process carries potential drawbacks. When a debtor works with a debt settlement company, they may pay back the debt settlement company in installments along with a significant service fee. Debt settlement may also cause considerable damage to your credit score.

While there are many reputable debt settlement companies, there are also many cases of such companies defrauding or overcharging vulnerable individuals.

Credit card and medical debts are the most common types of debts involved in the settlement process, while several other types — including secured debt like a mortgage, car or federal student loan — are typically not eligible for settlement.

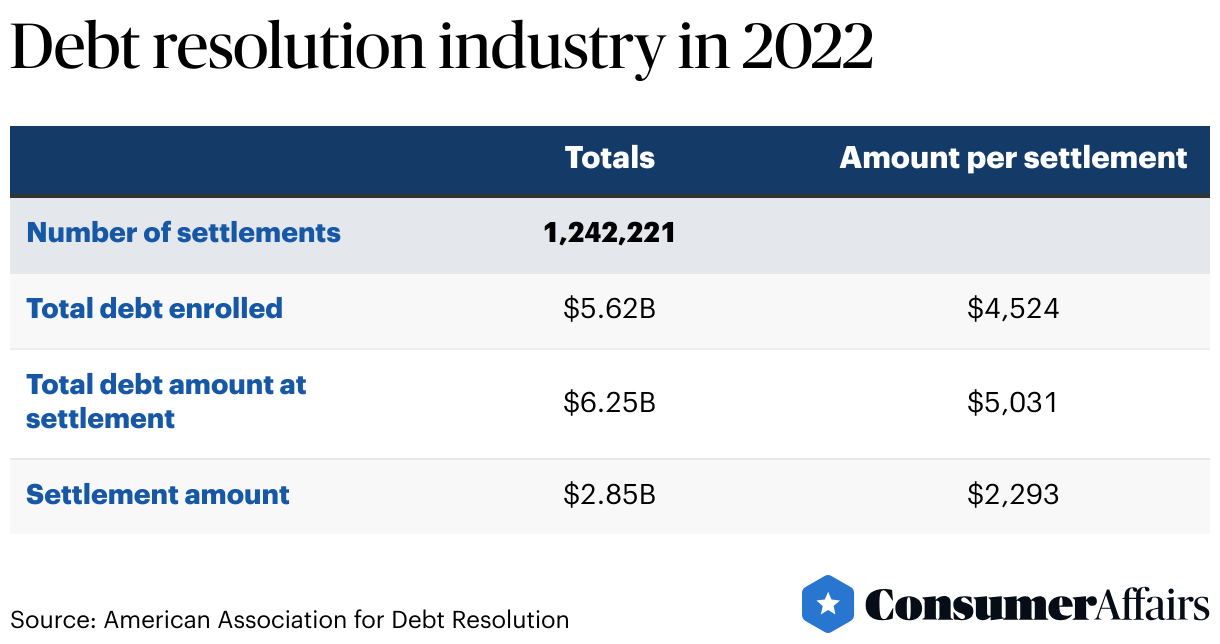

There were more than 1.2 million debt accounts settled in the U.S. in 2022, with principal balances totaling $5.6 billion.

Jump to insightThe market size of the U.S. debt relief services industry was $23.1 billion in 2023.

Jump to insightDebt settlement peaked during the Great Recession, with settled accounts totaling more than $11.4 billion in 2010.

Jump to insightA 2021 study of past debt settlements found that it takes an average of 14.3 months to settle an account.

Jump to insightUse of debt settlement for debt relief varies significantly from state to state — in 18 states, debt settlement is not widely available for consumers.

Jump to insightDebt settlement market statistics

The market size for debt relief services in the U.S. was $23.1 billion in 2023. Though that marked an increase over 2022, revenue generated by the debt relief services industry has declined by 4.6% per year, on average, between 2018 and 2023. Debt relief services are also not strictly limited to settlement, with other options for getting out of debt including bankruptcy and debt consolidation.

While household debt in the U.S. has skyrocketed in recent years, reaching a record high of $17.7 trillion in the first quarter of 2024, spending on debt relief services dropped during the COVID-19 pandemic amid low interest rates and rising disposable income. Spending on debt relief services has since begun to grow again as the economy has recovered.

Americans’ rising household debt also means there are massive amounts of unpaid loans and credit potentially eligible for debt relief. Of the $17.7 trillion in household debt, about 6% or more than $1 trillion was from credit cards.

In 2022, an estimated 1.2 million debt accounts were settled with a principal value of $5.6 billion and a settlement value of half that amount, $2.8 billion. While the total number of accounts settled in 2022 was lower than in the most recent prior year evaluated, over 1.4 million accounts in 2019, the amount of principal debt settled was higher at $5.6 billion versus $5.4 billion in 2019.

A 2023 report on the economic output of the debt resolution industry prepared for the American Association for Debt Resolution also estimated that the industry had a total economic output of $8.3 billion in 2022 when accounting for settlement firms, creditors that settled consumer debts, and debtors freed up after the resolution of their debt.

How debt is paid in a debt settlement

Unlike debt consolidation, debt settlement involves negotiation between debtor and creditor. The goal is to agree on a reduced balance that the creditor will consider payment in full. Once the agreement is made, the debtor pays the amount in a lump sum. It is possible for the consumer to negotiate a reduced settlement without hiring a debt settlement company. In many cases, the creditor will accept as little as 50% of the original debt.

Many consumers, however, need support with the negotiation process or have difficulty getting access to the lump sum required to complete the transaction. Debt settlement firms, which are for-profit companies, charge fees as high as 25% of the total settlement to negotiate, settle with the creditor and pay the initial lump-sum debt. Creditors then pay back the settlement company over time.

Types of debt settlement services

There are two ways of resolving a debt through settlement:

- With a lump-sum settlement, the debtor or settlement firm makes one large payment to the creditor to free the debtor from the terms of the debt.

- Under a term settlement, the debtor continues to make multiple payments over a period time but may see lower monthly payments or a lower principal amount owed.

Debt settlement demographic data

The median age of Americans who used debt settlement to manage their debts in 2022 was 38.56 years old. That marks a slight downtick from 2020, when the median age of those who settled debt was 38.74 years old.

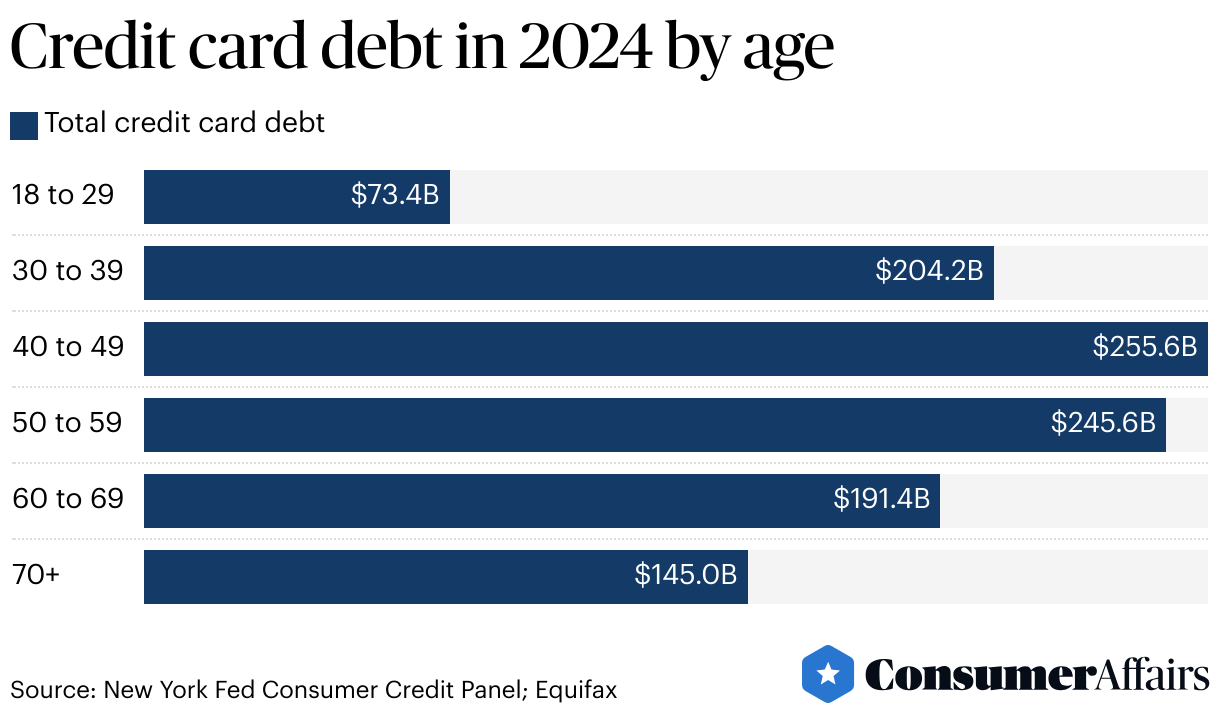

In the first quarter of 2024, 40- to 49-year-olds recorded the highest amount of credit card debt (the most common type paid off through debt settlement) of any age group.

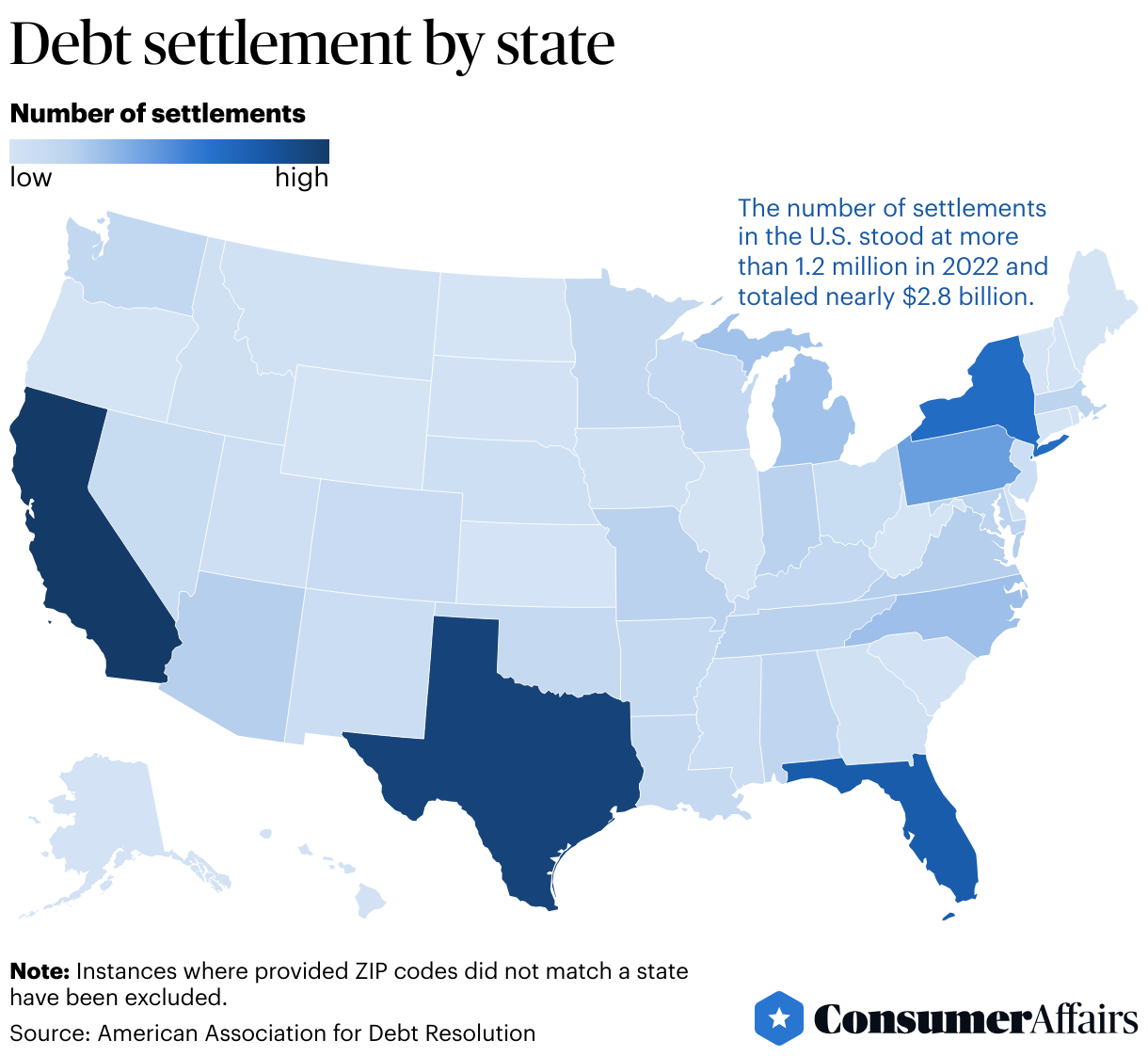

In 2022, California had the highest number of debt settlements at 157,518, followed by Texas, Florida and New York. Some states have very few debt settlements, with less than 100 occurring in Maine, Vermont and Wyoming in 2022. Because of the laws and regulations in certain states, there are 18 states where debt settlement is not broadly available.

Timelines to reach settlements

A 2021 Harvard Kennedy School report that studied the use of debt settlement programs among approximately 453,000 individuals and more than 3.1 million accounts found that it takes, on average, 14.3 months to settle an account.

Most people in debt settlement are settling multiple accounts, which are typically not all settled at once. The study, which examined individuals who entered debt settlement between January 2011 and March 2020, found that about three-fourths of people settle at least one account within their first two years of entering into settlement. Fewer than 1 in 4 people settled all of their accounts within three years, however.

Among the group studied, people entering debt settlement had an average of 6.93 accounts with a typical balance of $4,006, equaling an average balance across accounts of nearly $28,000.

Fees vs. debt reduced

The 2021 study found that fees paid to settlement companies averaged $848 per account. Settlement allows individuals to save a good deal of money. The study found that an average settlement (involving 3.8 accounts) results in $5,440 in savings over the course of 36 months after fees are taken into account.

Debt settlement taxes

When debt is settled, any debt that is forgiven is considered income and is taxed as such. For example, a debt reduction of $1,000 would be considered $1,000 in taxable income. This is the case unless the savings total less than $600. The amount of tax due depends on the tax bracket of the individual whose debt is settled.

The process of debt settlement comes with various pros and cons that each individual should evaluate before entering into a settlement. These include the possibility of reducing the amount you owe but the potential for a hit to your credit score and increased taxes owed.

Debt settlement over time

The amount of debt Americans settled sharply increased during the Great Recession, more than doubling from $5.4 billion in 2007 to $11.4 billion in 2010.

The increase was a result of a greater number of debt settlements and higher amounts of debt being settled. Following the end of the recession and tightening access to credit, the number dropped rapidly. Between 2011 and 2015, totals dropped significantly, and by 2016, the amount of debt settled was $3.7 billion — an amount that reflected a trend of debts being settled later into delinquency (when a borrower is past due on payment).

After 2010, there was a drop in credit counseling, which may also have contributed to the drop in debt settlement accounts. Between 2017 and 2019, debt settlements grew again. The percentage of accounts in delinquency rose to a slightly higher rate than before the Great Recession.

FAQ

How big is the debt settlement industry?

Debt relief services recorded more than $23 billion in market revenue in 2023. In 2022, there were more than 1.2 million accounts settled in the U.S., with a principal value of $5.6 billion and a settlement value of $2.8 billion. Eighteen states, however, do not have debt settlement services widely available to consumers.

Is debt settlement really worth it?

Debt settlement may be a good choice if you’re in debt greater than $10,000, you’re having trouble making minimum payments each month and you’re considering bankruptcy as an alternative. While it may have a negative impact on your credit rating and cost a good deal in fees, debt settlement can cut debt by as much as 50%. It’s important to know, however, that debt relief counts as income on taxes: A person who saves $5,000 in debt will owe taxes on that $5,000 as if it were earned income.

How long does debt settlement take?

While the time it takes to settle your debt may vary significantly depending on the amount owed, number of accounts involved and your ability to make payments, the average time to settle one account is 14.3 months. However, a 2021 study found that fewer than 25% of individuals who entered settlement were able to resolve all of their accounts within three years.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Debt.org, “What Is Debt Settlement and How Does it Work?” Accessed May 22, 2024.

- American Association for Debt Resolution, “Economic Impact Report 2023.” Accessed May 22, 2024.

- Harvard Kennedy School, “Financial Outcomes for Debt Settlement Programs: Estimates for 2011–2020.” Accessed May 22, 2024.

- American Fair Credit Council, “Economic Impact Report 2020.” Accessed May 22, 2024.

- IBISWorld, “Debt Relief Services in the US - Market Size (2004–2028).” Accessed May 22, 2024.

- Debt.org, “Debt Settlement vs. Debt Consolidation.” Accessed May 22, 2024.

- National Foundation for Credit Counseling, “Does Debt Settlement Make Sense for You?” Accessed May 22, 2024.

- Consumer Financial Protection Bureau, “Recent trends in debt settlement and credit counseling.” Accessed May 22, 2024.

- IBISWorld, “Debt Relief Services in the US - Market Size, Industry Analysis, Trends and Forecasts (2024-2029).” Accessed May 22, 2024.

- Incharge.org, “Debt Settlement.” Accessed May 22, 2024.

- U.S. Federal Trade Commission, “How to get out of debt.” Accessed May 22, 2024.

- Federal Reserve Bank of New York, “Quarterly Report on Household Debt And Credit.” Accessed May 22, 2024.

- Debt.org, “Is Debt Settlement Worth It?” Accessed May 22, 2024.

Figures