How many cars are repossessed each year? 2026

+1 more

Car repossessions, which are becoming more common after a dip during the COVID-19 pandemic era, have serious financial consequences for lenders and borrowers. Over a million cars were repossessed in 2022, with numbers rising as costs for new and used vehicles reach record highs. This trend impacts used car prices and highlights the financial strain facing many borrowers.

While there are federal protections against unfair and unethical repossession practices by dealers and lenders, consumers and experts alike are wary of what these practices mean for the availability of affordable new cars.

Over 1.2 million cars were repossessed from borrowers in 2022.

Jump to insightRepossessing a car allows lenders to retain only about 30% of their loan’s value.

Jump to insightMany states allow lenders to repossess a vehicle immediately following a missed payment.

Jump to insightA repossession remains on a credit report for seven years and can have devastating consequences for borrowers and their financial future.

Jump to insightCar repossession statistics

In 2022, over 1.2 million personal vehicles were repossessed by lenders, a slight increase from the previous year. Car ownership has become incredibly costly for consumers, as the current auto debt in the U.S. stands at over $1.6 trillion, up from about $1.34 trillion at the start of the COVID-19 pandemic in March 2020.

Repossessions are costly for lenders as well, given that cars quickly lose value. Lenders only receive about 30% of the value of a repossessed vehicle after it is sold or auctioned off.

Number of vehicle repossessions per year

| Year | Repossessions |

|---|---|

| 2010 | 1,336,600 |

| 2011 | 1,059,940 |

| 2012 | 986,013 |

| 2013 | 1,063,646 |

| 2014 | 1,180,053 |

| 2015 | 1,235,186 |

| 2016 | 1,492,428 |

| 2017 | 1,623,727 |

| 2018 | 1,610,951 |

| 2019 | 1,683,220 |

| 2020 | 1,288,199 |

| 2021 | *1,110,925 |

| 2022 | 1,228,372 |

Why are so many cars being repossessed?

Many borrowers fell short on payments during the COVID-19 pandemic as government stimuli struggled to keep Americans’ personal finances afloat. Loans taken out in 2021 and 2022 were particularly difficult to afford, due to higher vehicle prices and loan rates caused by supply chain disruptions. Lenders do not profit much from repossessions, so many lenders believed that, over time, they would make more money by forgiving borrowers during that unusual period of hardship rather than aggressively repossessing vehicles. Lender leniency caused repossessions to drop from a decade-high of nearly 1.7 million in 2019 to about 1.1 million in 2021, rising only slightly to approximately 1.2 million the following year.

As supply chains have returned to pre-pandemic norms, so have repossession rates for consumers. Some experts believe that stimulus spending and extra federal benefits led to overspending and inflation, making it difficult for borrowers to keep up with their payments.

Additionally, the global semiconductor chip shortage and limited car manufacturing during the pandemic had a long-lasting effect on the price of cars. The average price for new vehicles hit an all-time high of $49,939 in December 2022, up a sharp 32% from $37,851 in January 2020, before COVID-19 was declared a pandemic.

The average monthly payment for new vehicles has consequently increased, hitting a record high of $736 by mid-2023, compared with only $568 in November of 2019, putting consumers in a tough financial spot.

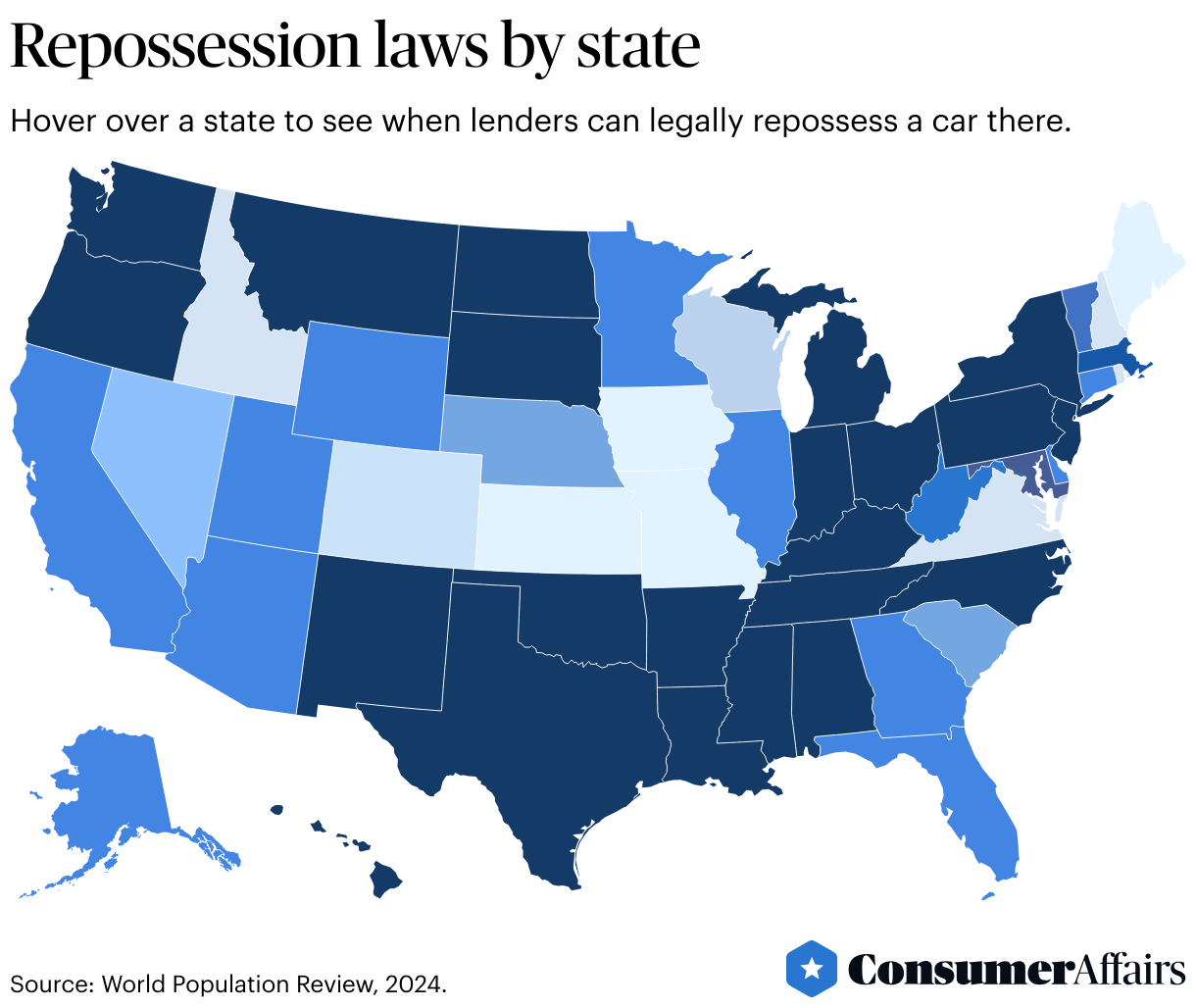

When can a car be repossessed?

There is no nationally applicable time frame for when your car can be repossessed. In many states, a lender can immediately reclaim your vehicle upon default, as defined by your auto lease or loan agreement terms. In Alaska, Arizona, California, Connecticut, Delaware, Florida, Georgia, Illinois and Minnesota, the law is explicitly defined: Lenders in these states can begin the repossession process immediately after your first missed payment. Some states require lenders to give borrowers a grace period of up to 20 days to make their payments current. The notice that lenders send informing borrowers of this grace period may be referred to as a “right-to-cure” notice.

The right to cure is a legal provision that gives a borrower in danger of repossession the opportunity to rectify their late payments within a given time frame. Iowa, Kansas, Maine, Missouri, Nebraska, South Carolina and Wisconsin are all right-to-cure states. In general, lenders don’t need a court order to begin the repossession process for car loans that are in default. However, a court order must be obtained first if the borrower is an active-duty service member in the military.

Consumers facing repossession are federally protected from unfair business practices through the Dodd-Frank Act. After the COVID-19 pandemic, federal financial institutions took notice of the strong demand for used vehicles and the subsequent rise in prices of those vehicles. Government officials appeared to be concerned that such high consumer demand would lead to more aggressive repossession practices by auto lenders, who stood to benefit from repossessing vehicles and reselling them at high prices.

In April 2022, the Consumer Financial Protection Bureau (CFPB) issued a bulletin reminding consumers, dealers and lenders about federal financial protections for consumers through the Dodd-Frank Act, preemptively warning against potential abuses or unfair practices during the repossession process.

Repossessions and kill switches

The starter interrupt, or “kill switch,” is a device that allows a user to remotely disable a vehicle for any reason. Some lenders install these devices in vehicles they sell to stop borrowers from using them if loan payments are not made on time.

Lenders have been known to use kill switches in a predatory manner. In 2023, the CFPB sued a large auto loan servicer that illegally engaged kill switches in the cars of borrowers who were not in default. In some cases, the auto loan servicer engaged kill switches after telling customers it would not do so.

How repossession works

Although you will be notified once your car loan is officially in default, your lender may not alert you when a repossession is initiated. A lender will typically contract a third-party towing service to take your vehicle wherever it’s found. Those who execute the repossession are not allowed to “breach the peace,” meaning they are prohibited from threatening you, disturbing your neighbors, using physical force or taking the vehicle from your garage without your consent.

After the vehicle is repossessed, the lender may choose to either auction it off, sell it privately or keep it. Some states require that a lender inform a dispossessed borrower of the date that their vehicle will go to auction or that a private sale of their vehicle will be executed. This gives the dispossessed borrower a chance to get their vehicle back by either bidding on it or paying what they owe in full, including any towing, storage or extra fees related to the repossession.

Additionally, some states have a mandatory right-to-cure period before repossession, and others give dispossessed borrowers the chance to reinstate their loans by paying what they owe, including any fees, within an agreed-upon time frame.

Repossessions can have very negative financial repercussions for consumers. They stay on credit reports for seven years and can disqualify borrowers outright from receiving certain loans. Some states also allow lenders to pursue a borrower for a repossession’s deficiency balance, which is the amount of the loan that is left over once the borrower sells the repossessed vehicle in addition to any costs incurred during the repossession.

Repossessions and used car prices

Before the COVID-19 pandemic, lenders often hesitated to repossess cars after consumers defaulted on their loans, as the cost and effort associated with the repossession process weren’t always worth the potential proceeds from reselling the car. However, global semiconductor chip shortages limited the production of new vehicles and increased demand for used cars in good condition. High used car prices make repossession a financially attractive move if a dealer can quickly repossess and resell a vehicle.

The general financial rules of thumb when purchasing a vehicle are to put at least 20% down, never spend more than 35% of your annual income and limit your loan term to 48 months or less. However, rising car costs have made these guidelines difficult for many consumers to abide by.

The average used car payment now exceeds $560, and used car buyers made a record-high average down payment of $4,111 during the third quarter of 2023. Used cars have only become marginally cheaper in recent years, but some experts believe their prices could drop a bit if repossession rates continue to increase and more used cars are added to the market.

FAQ

What is repossession?

Repossession is when a lender retakes its property from a borrower.

When you finance a vehicle with a loan, your lender typically holds on to the title of that vehicle until you repay the loan in full. When you miss loan payments and default on the loan, the lender can take back (repossess) the vehicle from you, often without notice.

How many cars get repossessed every year?

Approximately 1.2 million vehicles were repossessed in 2022.

Why would my car be repossessed?

A car that you finance can be repossessed if you fall behind on your payments.1 You don’t own your car until your loan is repaid in full and you possess the car’s title, at which point the car can no longer be repossessed.

How does car repossession affect my credit?

An auto loan is considered one of the most important financial obligations you can take on as a consumer, and timely loan payments are among the most critical factors in determining creditworthiness. Because car repossession is associated with late car payments, it brands dispossessed borrowers as a liability to creditors and can severely limit your ability to qualify for new credit. Additionally, a repossession will stay on your credit report for seven years, creating long-term barriers to certain financial goals.

How can I avoid repossession?

If you’re having trouble making car payments, you should reach out to your lender immediately. Your lender might be able to work with you to allow slightly delayed payments or even a revision of your payment schedule in extenuating circumstances.

If you know that you will be unable to make your car payments even with negotiation, you can voluntarily return the vehicle, which may allow you to pay less in fees than you would in an involuntary repossession. However, if you choose voluntary repossession, you may still be responsible for paying what’s owed on the loan after the vehicle is resold.

Article sources

ConsumerAffairs writers primarily rely on government data, industry experts, and original research from other reputable publications to inform their work. Specific sources for this article include:

- Debt.org, “Car Repossession.” Accessed Feb. 1, 2024.

- Kelley Blue Book, “Car Repossessions on the Rise.” Accessed Feb. 1, 2024.

- Cox Automotive, “Average New-Vehicle Transaction Prices Up 3.5% Year Over Year in January.” Accessed Feb. 1, 2024.

- Cox Automotive, “Data Tables for December 2023 Kelley Blue Book Average Transaction Prices Report.” Accessed Feb. 1, 2024.

- Consumer Financial Protection Bureau, “Bulletin 2022-04: Mitigating Harm from Repossession of Automobiles.” Accessed Feb. 1, 2024.

- Edmunds, “New-vehicle Monthly Payments Climb to New Heights in Q3, According to Edmunds.” Accessed Feb. 1, 2024.

- Federal Trade Commission, “Vehicle Repossession.” Accessed Feb. 1, 2024.

- Cox Automotive, “Repossessions are Down, Thanks to Accommodations and Stimulus.” Accessed Feb. 1, 2024.

- Cox Automotive, “Loan Defaults and Repossessions Returned to Historical Norms in 2022.” Accessed Feb. 1, 2024.

- World Population Review, “Vehicle Repossession Laws by State 2024.” Accessed Feb. 1, 2024.

- MyLawQuestions, “What does ‘Right to Cure’ Mean? Understanding Your Legal Remedies and Protections.” Accessed Feb. 2, 2024.

- Iowa Legislature, “CONSUMER CREDIT CODE, §537.5110 Cure of default.” Accessed Feb. 2, 2024.

- Cox Automotive, “Auto Loan Defaults Are Increasing, But We Are Not Heading Into A Repo Crisis.” Accessed Feb. 12, 2024.

- Edmunds, “Auto Loan Interest Rates Drop to Lowest Level of 2019 in November, According to Edmunds.” Accessed Feb. 2, 2024.

- Insurance Journal, “Kill the Kill Switch: CFPB Says Dealer Illegally Locked Cars and Repossessed Them.” Accessed Feb. 2, 2024.

- Associated Press, “Posts distort infrastructure law’s rule on impaired driving technology.” Accessed Feb. 2, 2024.

- Los Angeles Times, “In another pandemic fallout, used-car prices are way up, and the repo man is back.” Accessed Feb. 2, 2024.

- YCharts, “US Auto Loan Debt (I:USALD).” Accessed Feb. 2, 2024.

Figures